101

249) On July 1, 2021, a company loans one of its employees $20,000 and accepts a nine-month,

8% note receivable. Calculate the amount of interest revenue the company will recognize in 2021

and 2022.

250) On April 1, 2021, a company loans one of its suppliers $50,000 and accepts a 24-month, 12%

note receivable. Calculate the amount of interest revenue the company will recognize in 2021,

2022, and 2023.

251) On April 14, a company lends $10,000 cash to one of its employees and accepts a six-month,

12% note in return. Record the acceptance of the note receivable.

102

252) On April 1, a company provides services to one of its customers for $12,000. As payment for

the services, the company accepts a six-month, 10% note from the customer. Record the

acceptance of the note receivable on April 1 and the cash collection on October 1.

253) On May 1, 2021, a company lends $100,000 to one of its main suppliers and accepts a

12-month, 6% note. Record the acceptance of the note on May 1, 2021, the adjustment on

December 31, 2021, and the cash collection on May 1, 2022.

103

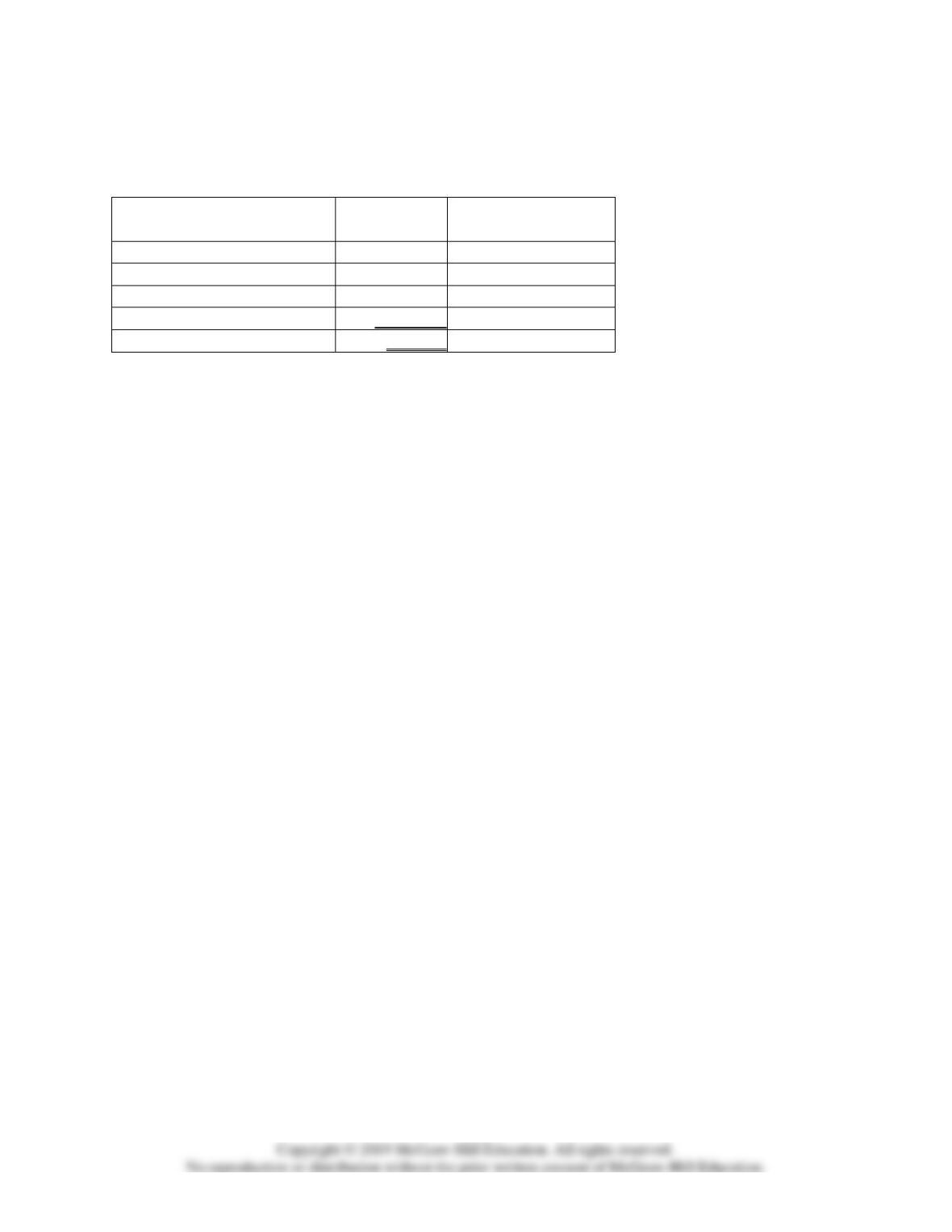

254) Below are amounts for two companies:

Beginning

Accounts

Receivable

(net)

Ending

Accounts

Receivable

(net)

Net Sales

Company 1

$1,500

$1,200

$29,700

Company 2

3,100

3,300

80,000

For each company, calculate the receivables turnover ratio. Which company appears more

efficient in collecting cash from sales?

255) At the end of the year, a company reports a balance in its Allowance for Uncollectible

Accounts of $1,400 (credit) before any year-end adjustment. The company estimates future

uncollectible accounts to be 3% of credit sales for the year. Credit sales for the year total $280,000.

Record the adjustment for the allowance for uncollectible accounts using the

percentage-of-credit-sales method.

Bad Debt Expense

104

256) At the end of the year, a company reports a balance in its Allowance for Uncollectible

Accounts of $1,400 (debit) before any year-end adjustment. The company estimates future

uncollectible accounts to be 3% of credit sales for the year. Credit sales for the year total $280,000.

Record the adjustment for the allowance for uncollectible accounts using the

percentage-of-credit-sales method.

105

257) Assume the following scenarios.

Scenario 1. During 2021, Makers Consulting provides services of $100,000. The company

receives an initial payment of $75,000 with the balance to be received the following year.

Scenario 2. People-R-Us typically charges $75 for a one-year subscription. On January 1, 2021,

Georgette, age 72, purchases a one-year subscription to the magazine and receives a 20% senior

citizen discount.

Scenario 3. During 2021, Waste Control provides services on account for $15,000. The customer

pays for those services in 2022.

Scenario 4. During 2021, Tasty Foods sells grocery items to one of its customers for $125,000 on

account. Cash collections on those sales are $80,000 in 2021 and $30,000 in 2022. The remaining

$15,000 is written off as uncollectible in 2022.

Required:

For each scenario, calculate the amount of revenue to be recognized in 2021.

106

258) Recovery Experts (RE) specializes in data recovery from crashed hard drives. The price

charged varies based on the extent of damage and the amount of data being recovered. RE offers a

10% discount to students and faculty at educational institutions. Consider the following

transactions during the month of June.

June 10

Luke’s hard drive crashes and he sends it to RE.

June 12

After initial evaluation, RE e-mails Luke to let him know that full

data recovery will cost $1,600.

June 13

Luke informs RE that he would like them to recover the data and

that he is a student at USC, qualifying him for a 10% educational

discount and reducing the cost by $160 ($1,600 × 10%).

June 16

RE performs the work and claims to be successful in recovering all

data. RE asks Luke to pay within 30 days of today’s date, offering a

5% discount for payment within 10 days.

June 19

When Luke receives the hard drive, he notices that RE did not

successfully recover all data. Approximately 25% of the data has

not been recovered and he informs RE.

June 20

RE reduces the amount Luke owes by 25%.

June 30

Luke pays the amount owed.

Required:

1. Record the necessary transactions(s) for Recovery Experts on each date.

2. Calculate net revenues.

3. Show how net revenues would be presented in the income statement.

4. Calculate net revenues if Luke had paid his bill on June 25.

107

259) By the end of its first year of operations, Gallen Corporation has credit sales of $580,000 and

accounts receivable of $200,000. Given it’s the first year of operations, Gallen’s management is

unsure how much allowance for uncollectible accounts it should establish. One of the company’s

competitors, which has been in the same industry for an extended period, estimates uncollectible

accounts to be 3% of ending accounts receivable, so Gallen decides to use that same amount.

However, actual write-offs in the following year were 10% of the $200,000 ($20,000). Gallen’s

inexperience in the industry led to making sales to high credit risk customers.

Required:

1. Record the adjustment for uncollectible accounts at the end of the first year of operations using

the 3% estimate of accounts receivable.

2. By the end of the second year, Gallen has the benefit of hindsight to know that estimates of

uncollectible accounts in the first year were too low. By how much did Gallen underestimate

uncollectible accounts in the first year? How did this underestimation affect the reported amounts

of total assets and expenses at the end of the first year? Ignore tax effects.

3. Should Gallen prepare new financial statements for the first year of operations to show the

correct amount of uncollectible accounts? Explain.

110

260) The following events occur for Wortham Landscape Design during 2021 and 2022, its first

two years of operations.

February 2, 2021

Provide services to customers on account for $26,000.

July 23, 2021

Receive $20,000 from customers on account.

December 31, 2021

Estimate that 10% of uncollected accounts will not be received.

April 12, 2022

Provide services to customers on account for $40,000.

June 28, 2022

Receive $5,000 from customers for services provided in 2021.

September 13, 2022

Write off the remaining amounts owed from services provided in

2021.

October 5, 2022

Receive $33,000 from customers for services provided in 2022.

December 31, 2022

Estimate that 10% of uncollected accounts will not be received.

Required:

1. Record transactions for each date.

2. Post transactions to the following accounts: Cash, Accounts Receivable, and Allowance for

Uncollectible Accounts.

3. Calculate net accounts receivable at the end of 2021 and 2022.

113

261) Gable Incorporated provides legal services. During 2021, the company provides services of

$500,000 on account. Of this amount, $70,000 remains uncollected at the end of the year. An aging

schedule as of December 31, 2021, is provided below.

Age Group

Amount

Receivable

Estimated Percent

Uncollectible

Not yet due

$40,000

5%

0-30 days past due

19,000

10%

31-60 days past due

9,000

20%

More than 60 days past due

6,000

40%

Total

$74,000

Required:

1. Calculate the allowance for uncollectible accounts.

2. Record the December 31, 2021 adjustment, assuming the balance of Allowance for

Uncollectible Accounts before adjustment is $500 (debit).

3. On April 3, 2022, a customer’s account balance of $600 is written off as uncollectible. Record

the write-off.

4. On July 17, 2022, the customer whose account was written off in Requirement 3 unexpectedly

pays $200 of the amount but does not expect to pay any additional amounts. Record the cash

collection.