161)

On March 12, Klein Company sold merchandise in the amount of $7,800 to Babson Company,

with credit terms of 2/10, n/30. The cost of the items sold is $4,500. Klein uses the perpetual

inventory system and the gross method of accounting for sales. On March 15, Babson returns some

of the merchandise. The selling price of the merchandise is $600 and the cost of the merchandise

returned is $350. Babson pays the invoice on March 20, and takes the appropriate discount. The

amount that Klein receives from Babson on March 20 is:

A) $7,200. B) $7,800. C) $7,056. D) $7,644. E) $7,044.

162)

On March 12, Klein Company sold merchandise in the amount of $7,800 to Babson Company,

with credit terms of 2/10, n/30. The cost of the items sold is $4,500. Klein uses the perpetual

inventory system and the gross method of accounting for sales. On March 15, Babson returns some

of the merchandise. The selling price of the merchandise is $600 and the cost of the merchandise

returned is $350. Babson pays the invoice on March 20, and takes the appropriate discount. The

journal entry that Klein makes on March 20 is:

A)

Cash

7,056

Accounts receivable

7,056

B)

Cash

7,800

Accounts receivable

7,800

C)

Cash

7,644

Sales discounts

156

Accounts receivable

7,800

D)

Cash

4,500

Accounts receivable

4,500

E)

Cash

7,056

Sales discounts

144

Accounts receivable

7,200

163)

Zenith Company’s Merchandise Inventory account at year-end has a balance of $91,820, but a

physical count reveals that only $90,450 of inventory exists. The adjusting entry to record this

$1,370 of inventory shrinkage is:

A)

Purchases discounts

1,370

Cost of goods sold

1,370

B)

Inventory shrinkage expense

1,370

Cost of goods sold

1,370

C)

Merchandise inventory

1,370

Inventory shrinkage expense

1,370

D)

Cost of goods sold

90,450

Merchandise inventory

90,450

E)

Cost of goods sold

1,370

Merchandise inventory

1,370

164)

All of the following statements regarding sales returns and allowances are true except:

A)

Sales returns and allowances estimates are typically made as period-end adjustments.

B)

When sales returns and allowances adjustments are made to sales, an estimate must also be

made for the cost side.

C)

The Inventory Returns Estimated account is a current liability account.

D)

New revenue recognition rules require sellers to report sales net of expected returns and

allowances for annual periods.

E)

Sales Refund Payable is a current liability account.

165)

In its first year of business, Borden Corporation had sales of $2,000,000 and cost of goods sold of

$1,200,000. Borden expects returns in the following year to equal 8% of sales. The adjusting entry

or entries to record the expected sales returns is (are):

A)

Sales returns and allowances

160,000

Sales

160,000

Cost of Goods Sold

96,000

Inventory Returns Estimated

96,000

B)

Sales Refund Payable

160,000

Accounts receivable

160,000

C)

Sales

2,000,000

Sales Refund Payable

160,000

Accounts receivable

1,840,000

D)

Sales Returns and Allowances

160,000

Sales Refund Payable

160,000

Inventory Returns Estimated

96,000

Cost of goods sold

96,000

E)

Accounts Receivable

2,000,000

Sales

2,000,000

166)

In the current year, Borden Corporation had sales of $2,000,000 and cost of goods sold of

$1,200,000. Borden expects returns in the following year to equal 8% of sales. The unadjusted

balance in Inventory Returns Estimated is a debit of $6,000, and the unadjusted balance in Sales

Refund Payable is a credit of $10,000. The adjusting entry or entries to record the expected sales

returns is (are):

A)

Sales Returns and Allowances

150,000

Sales Refund Payable

150,000

Inventory Returns Estimated

90,000

Cost of goods sold

90,000

B)

Sales

2,000,000

Sales Refund Payable

160,000

Accounts receivable

1,840,000

C)

Accounts Receivable

2,000,000

Sales

2,000,000

D)

Sales Refund Payable

150,0000

Accounts receivable

150,000

E)

Sales returns and allowances

150,000

Sales

150,000

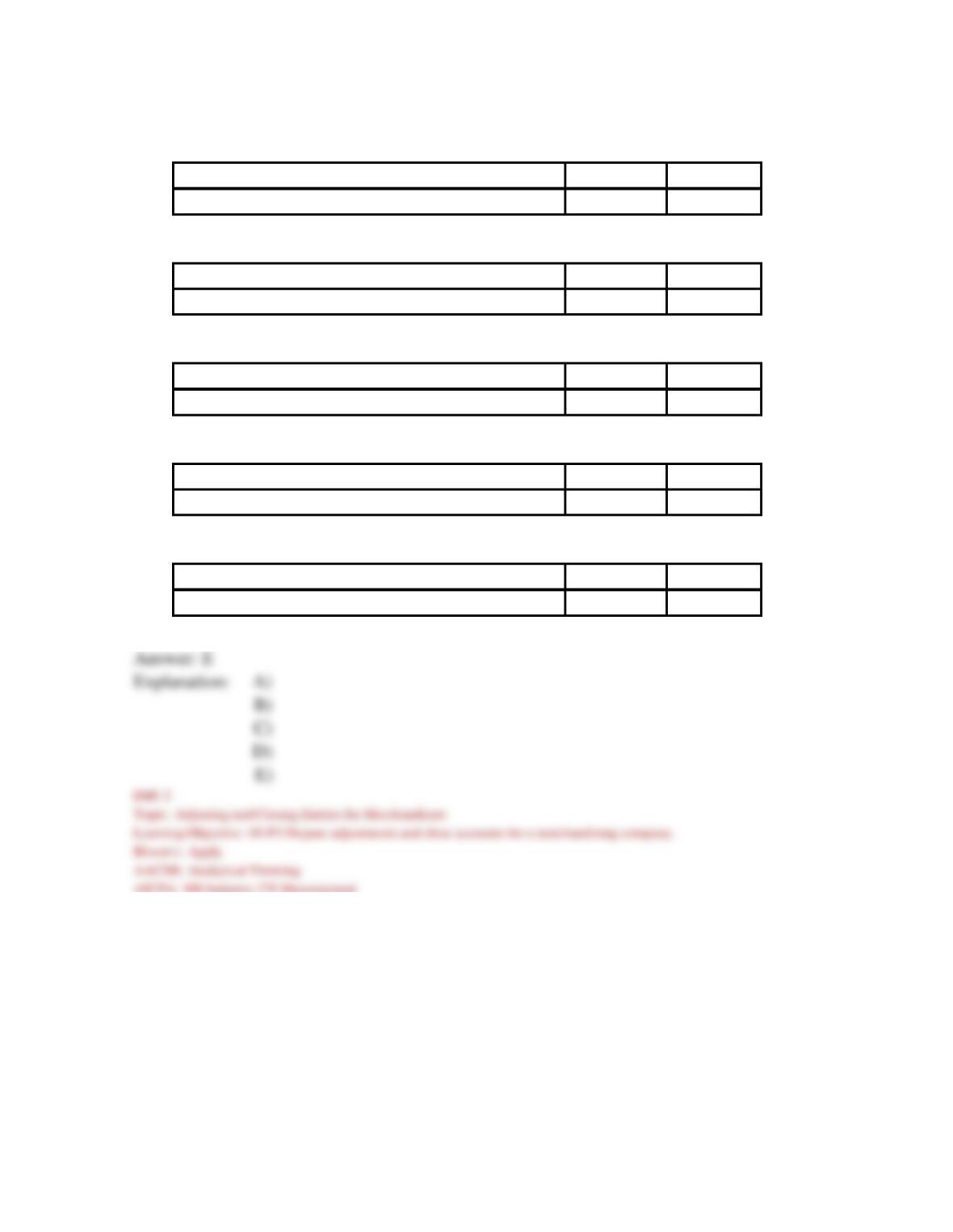

Cost of Goods Sold

90,000

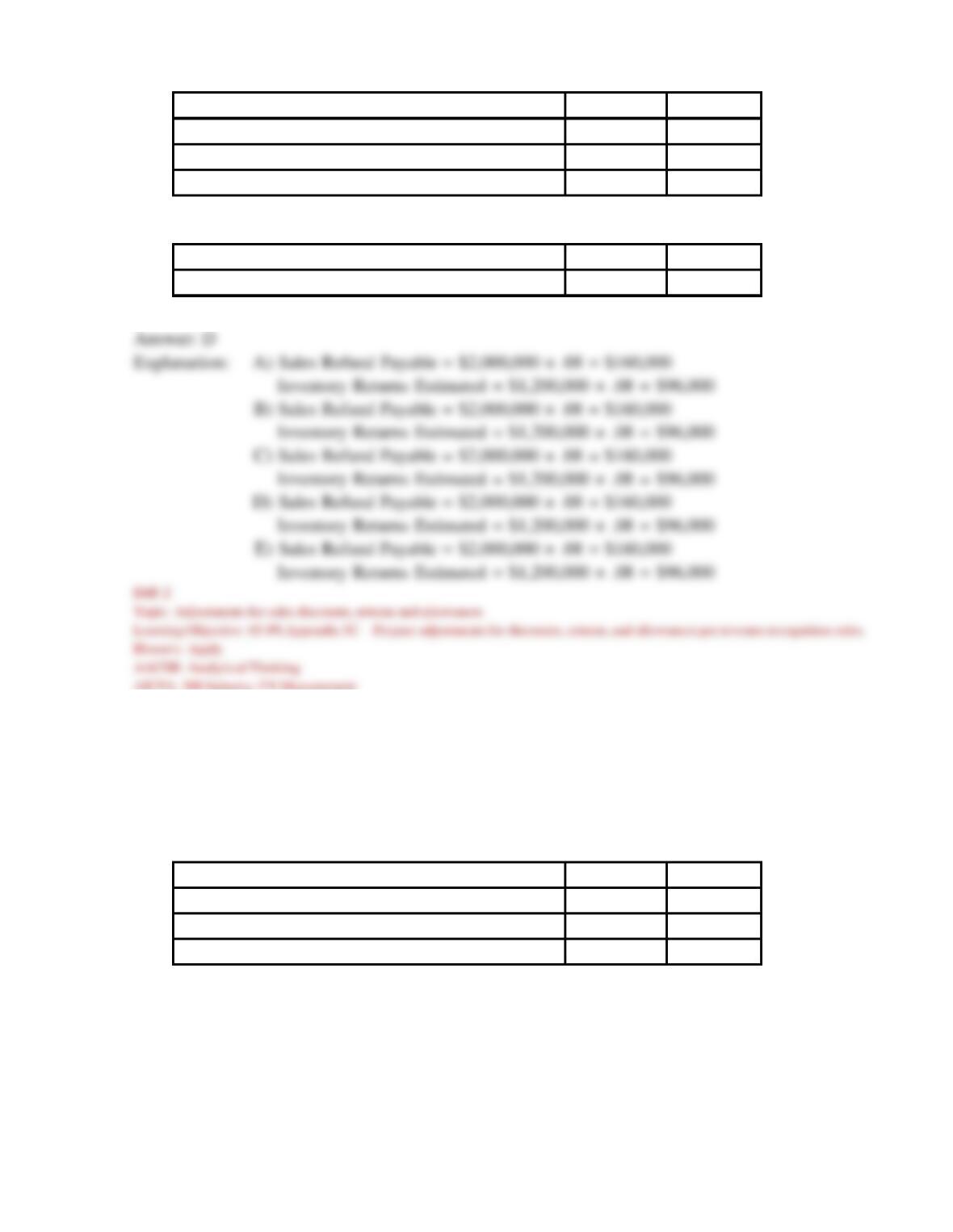

Inventory Returns Estimated

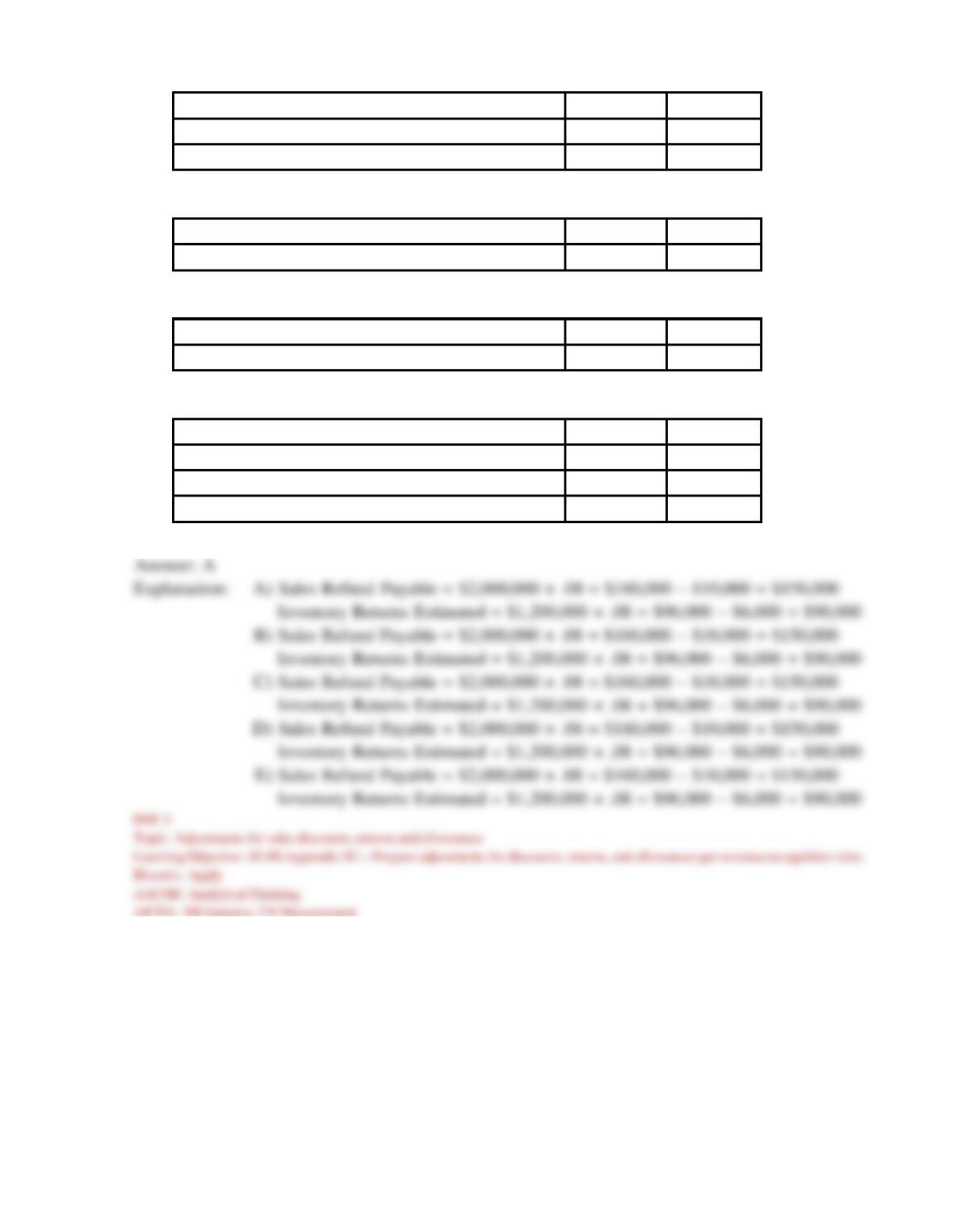

90,000

167)

Netherland Corporation has the following unadjusted balances: Accounts Receivable, $80,000

(debit), and Allowance for Sales Discounts $300 (credit). Of the receivables, $50,000 of them are

within the 2% discount period, and Netherland expects buyers to take $1,000 in future-period

discounts ($50,000 × 2%) arising from this period’s sales. The adjusting entry to estimate sales

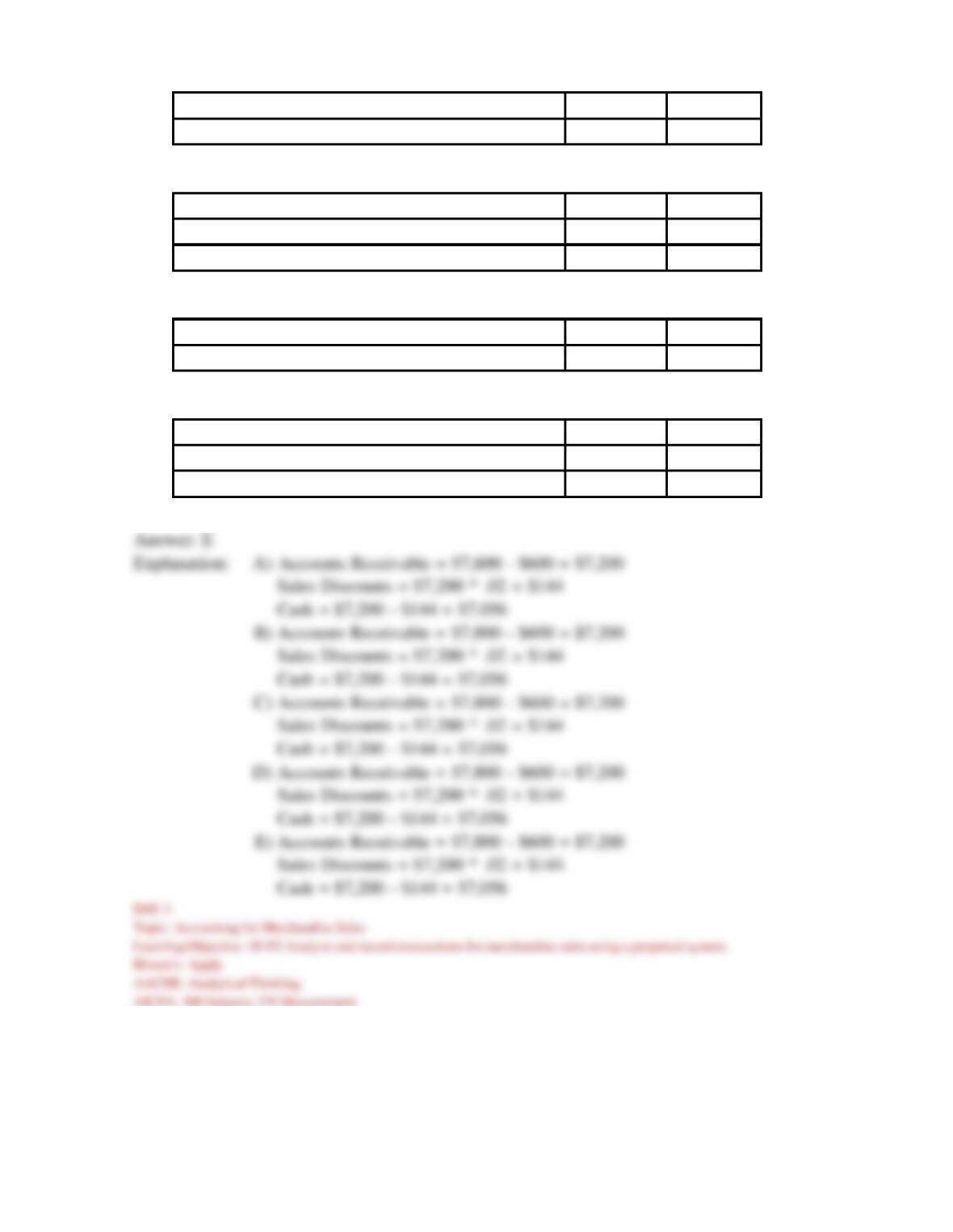

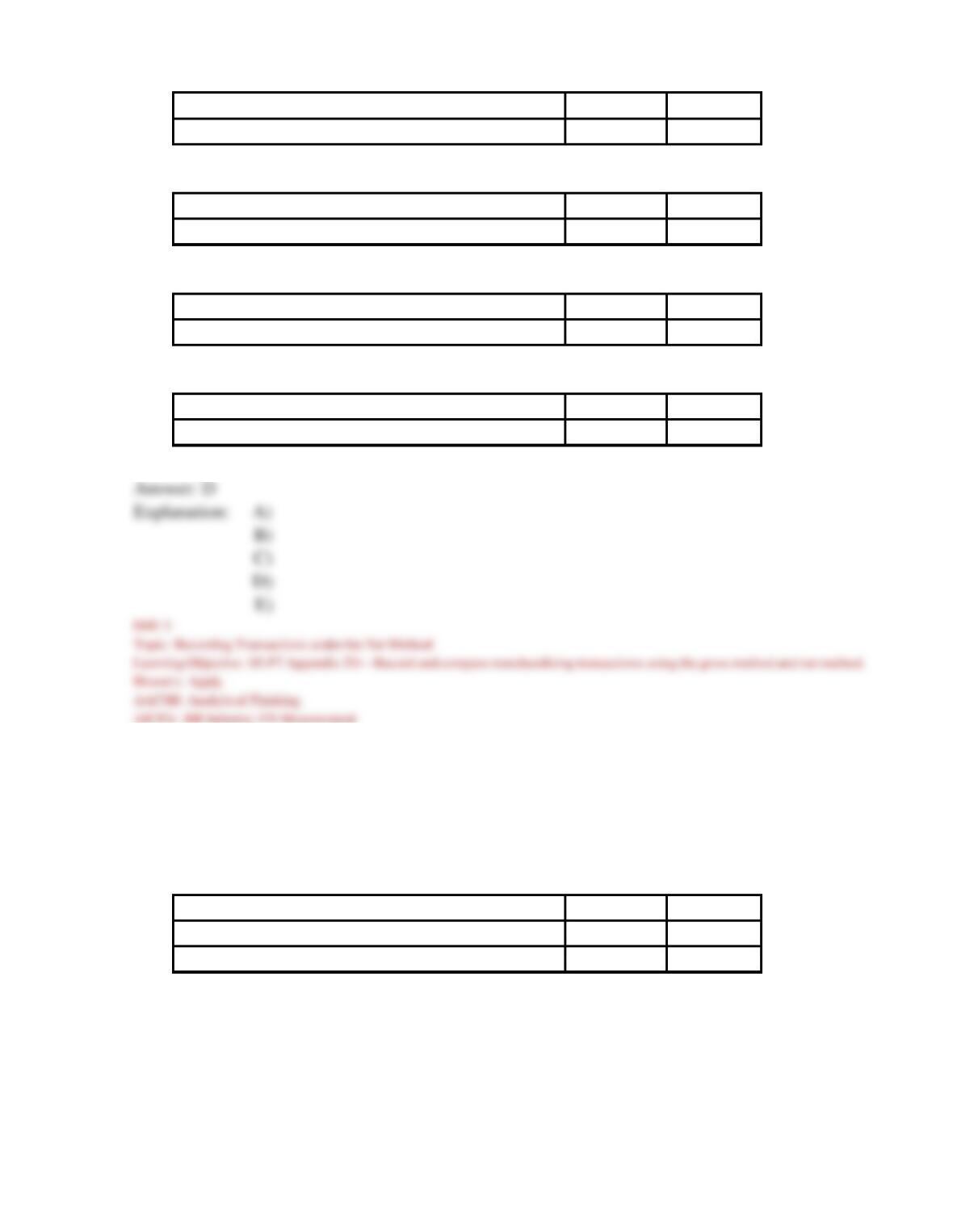

discounts is (are):

A)

Accounts Receivable

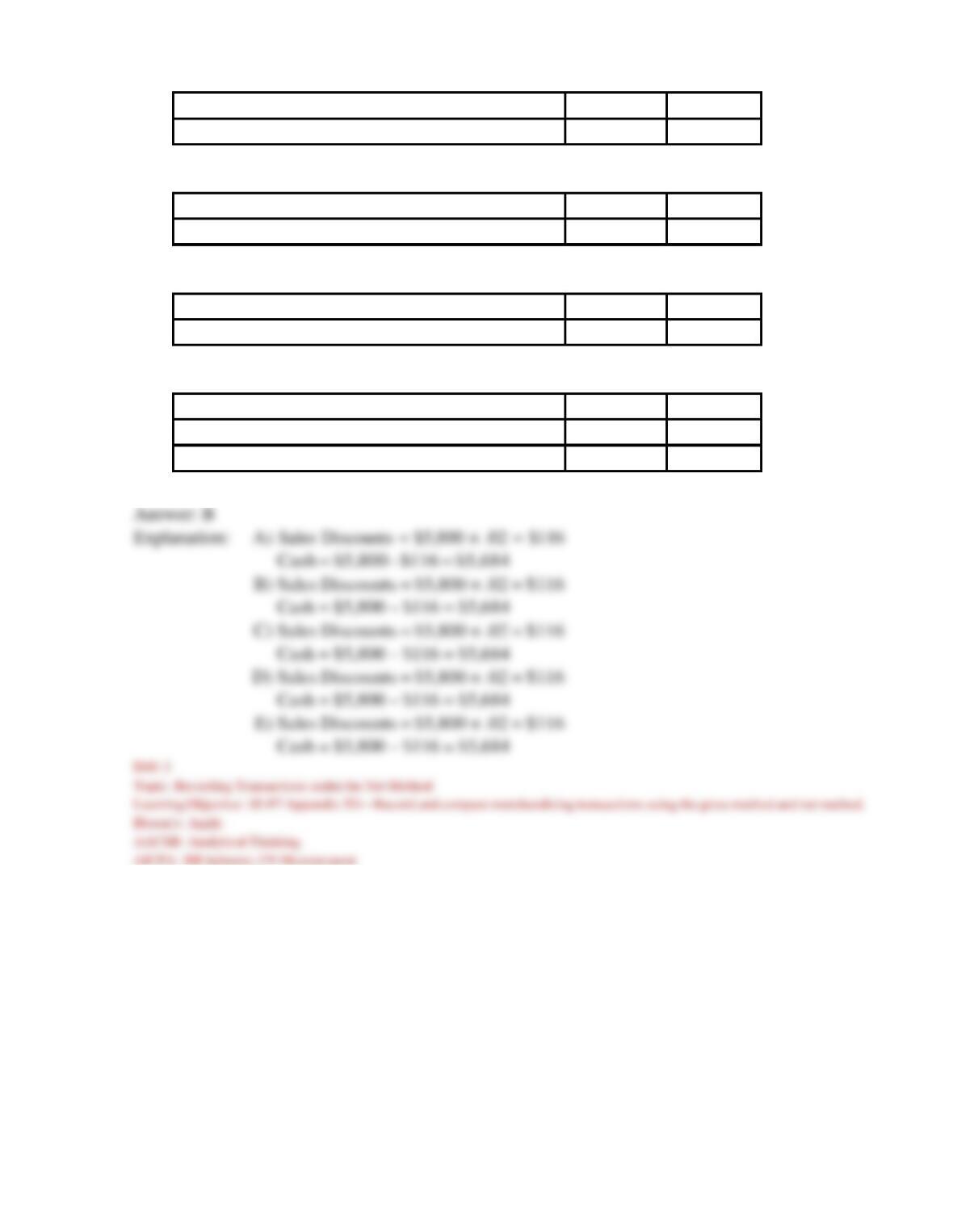

80,000

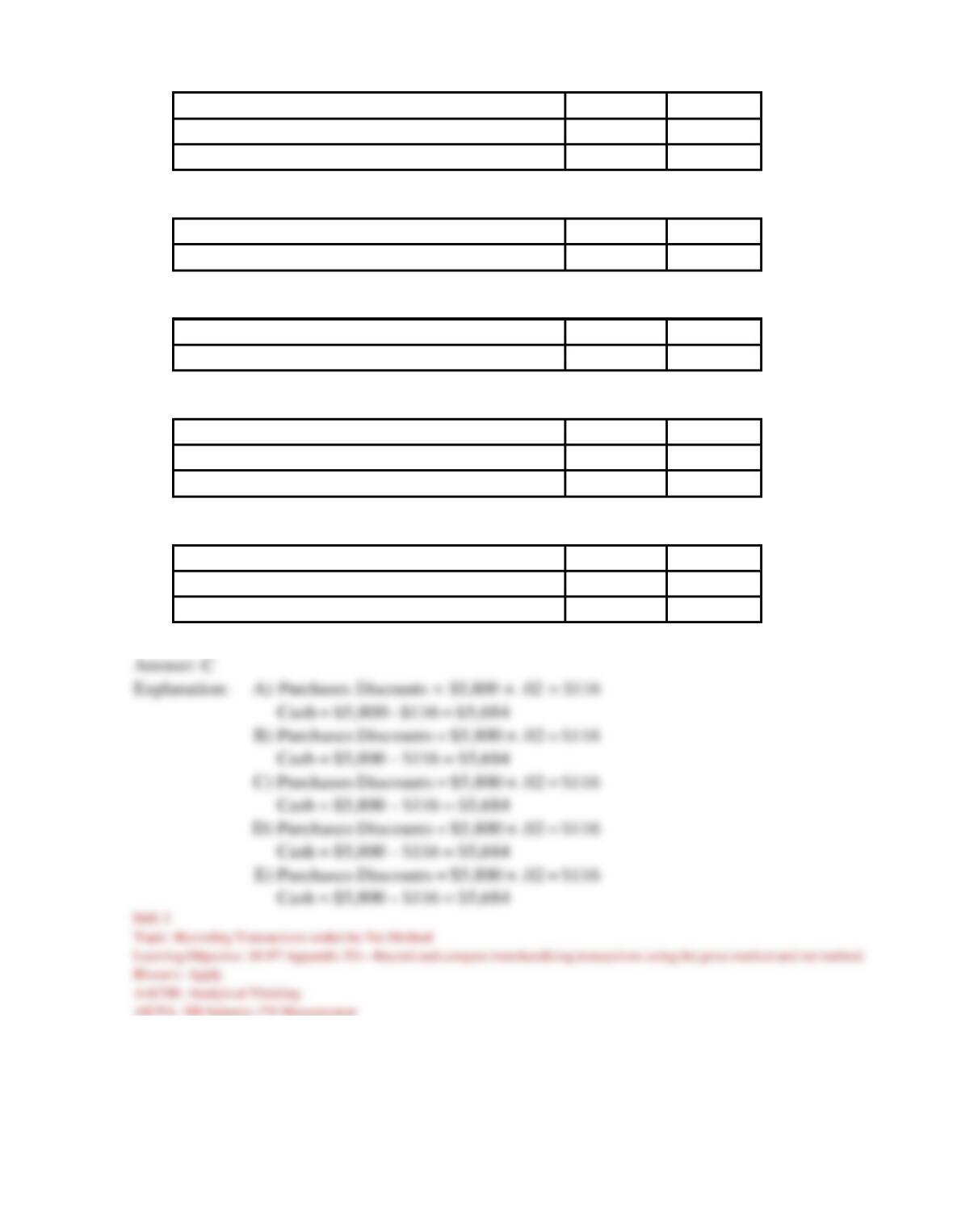

Sales

80,000

B)

Sales Discounts

700

Allowance for Sales Discounts

700

C)

Sales Discounts

50,000

Sales

50,000

Cost of Goods Sold

1,000

Inventory Returns Estimated

1,000

D)

Sales Discounts

1,000

Allowance for Sales Discounts

1,000

E)

Sales Discounts

1,000

Accounts receivable

1,000

168)

An expense resulting from failing to take advantage of cash discounts when using the net method

of recording purchases is called:

A)

Trade discounts.

B)

Discounts earned.

C)

Purchases discounts.

D)

Discounts lost.

E)

Sales discounts.

169)

A company that uses the net method of recording purchases and a perpetual inventory system

purchased $1,800 of merchandise on July 5 with terms 2/10, n/30. On July 7, it returned $200

worth of merchandise. On July 28, it paid the full amount due. The correct journal entry to record

the payment on July 28 is:

A)

Debit Accounts Payable $1,600; credit Merchandise Inventory $32; credit Cash $1,568.

B)

Debit Cash $1,600; credit Accounts Payable $1,600.

C)

Debit Merchandise Inventory $1,600; credit Cash $1,600.

D)

Debit Accounts Payable $1,568; debit Discounts Lost $32; credit Cash $1,600.

E)

Debit Accounts Payable $1,800; credit Cash $1,800.

170)

Morgan, Inc. uses a perpetual inventory system and the net method of recording purchases. On

May 12, a merchandise purchase of $15,000 was made on credit, 2/10, n/30. The journal entry to

record this purchase is:

A)

Merchandise Inventory

15,000

Accounts Payable

15,000

B)

Accounts Payable

15,000

Merchandise Inventory

15,000

C)

Merchandise Inventory

14,700

Accounts Payable

14,700

D)

Purchases

14,700

Accounts Payable

14,700

E)

Purchases

15,000

Accounts Payable

15,000

171)

The net method of recording purchases refers to recording:

A)

Specified amounts and timing of payments that a buyer agrees to in return for being granted

credit.

B)

Purchases at the invoice price less any cash discounts.

C)

Inventory at the lower of cost or market.

D)

Purchases at the full invoice price, without deducting any cash discounts.

E)

Inventory at its selling price.

172)

On March 12, Klein Company sold merchandise in the amount of $7,800 to Babson Company,

with credit terms of 2/10, n/30. The cost of the items sold is $4,500. Klein uses the perpetual

inventory system and the net method of accounting for sales. On March 15, Babson returns some of

the merchandise, which is not defective. The selling price of the returned merchandise is $600 and

the cost of the merchandise returned is $350. The entry(ies) that Klein must make on March 15 is

(are):

A)

Accounts receivable

600

Sales returns and allowances

600

B)

Sales returns and allowances

350

Accounts receivable

350

C)

Sales returns and allowances

588

Accounts receivable

588

Merchandise inventory

350

Cost of goods sold

350

D)

Accounts receivable

600

Sales returns and allowances

600

Cost of Goods Sold

350

Merchandise inventory

350

E)

Sales returns and allowances

588

Accounts receivable

588

Merchandise inventory

343

Cost of goods sold

343

173)

On September 12, Ryan Company sold merchandise in the amount of $5,800 to Johnson Company,

with credit terms of 2/10, n/30. The cost of the items sold is $4,000. Ryan uses the periodic

inventory system and the net method of accounting for sales. The journal entry or entries that Ryan

will make on September 12 is (are):

A)

Accounts receivable

5,684

Sales

5,684

Cost of goods sold

4,000

Merchandise Inventory

4,000

B)

Accounts receivable

5,800

Sales

5,800

C)

Accounts receivable

5,800

Sales

5,800

Cost of Goods Sold

4,000

Merchandise inventory

4,000

D)

Sales

5,800

Accounts receivable

5,800

E)

Accounts receivable

5,684

Sales

5,684

174)

On September 12, Ryan Company sold merchandise in the amount of $5,800 to Johnson Company,

with credit terms of 2/10, n/30. The cost of the items sold is $4,000. Johnson uses the periodic

inventory system and the net method of accounting for purchases. The journal entry that Johnson

will make on September 12 is:

A)

Merchandise inventory

5,800

Accounts payable

5,800

B)

Purchases

5,800

Accounts payable

5,800

C)

Merchandise inventory

5,684

Accounts payable

5,684

D)

Purchases

5,684

Accounts payable

5,684

E)

Accounts payable

4,000

Merchandise inventory

4,000

175)

On September 12, Ryan Company sold merchandise in the amount of $5,800 to Johnson Company,

with credit terms of 2/10, n/30. The cost of the items sold is $4,000. Ryan uses the periodic

inventory system and the net method of accounting for sales. Johnson pays the invoice on

September 18, and takes the appropriate discount. The journal entry that Ryan makes on September

18 is:

A)

Cash

5,684

Sales discounts

116

Accounts receivable

5,800

B)

Cash

5,684

Accounts receivable

5,684

C)

Cash

5,800

Accounts receivable

5,800

D)

Cash

4,000

Accounts receivable

4,000

E)

Cash

3,920

Sales discounts

80

Accounts receivable

4,000

176)

On September 12, Ryan Company sold merchandise in the amount of $5,800 to Johnson Company,

with credit terms of 2/10, n/30. The cost of the items sold is $4,000. Johnson uses the periodic

inventory system and the net method of accounting for purchases. Johnson pays the invoice on

September 18, and takes the appropriate discount. The journal entry that Johnson makes on

September 18 is:

A)

Sales

4,000

Sales Refund Payable

80

Accounts receivable

3,920

B)

Purchases

5,684

Cash

5,684

C)

Accounts payable

5,684

Cash

5,684

D)

Sales

5,800

Sales Refund Payable

116

Accounts receivable

5,684

E)

Cash

5,684

Purchases discounts

116

Accounts payable

5,800

177)

On September 12, Ryan Company sold merchandise in the amount of $5,800 to Johnson Company,

with credit terms of 2/10, n/30. The cost of the items sold is $4,000. Ryan uses the periodic

inventory system and the net method of accounting for sales. On September 14, Johnson returns

some of the non-defective merchandise, which is restored to inventory. The selling price of the

returned merchandise is $500 and the cost of the merchandise returned is $350. The entry or entries

that Ryan must make on September 14 is (are):

A)

Sales returns and allowances

500

Accounts receivable

500

B)

Sales returns and allowances

490

Accounts receivable

490

Merchandise inventory

350

Cost of goods sold

350

C)

Sales returns and allowances

350

Accounts receivable

350

D)

Sales returns and allowances

490

Accounts receivable

490

E)

Sales returns and allowances

490

Accounts receivable

490

Merchandise inventory

343

Cost of goods sold

343

178)

On September 12, Ryan Company sold merchandise in the amount of $5,800 to Johnson Company,

with credit terms of 2/10, n/30. The cost of the items sold is $4,000. Ryan uses the periodic

inventory system and the net method of accounting for sales. On September 14, Johnson returns

some of the merchandise. The selling price of the merchandise is $500 and the cost of the

merchandise returned is $350. Johnson pays the invoice on September 18, and takes the

appropriate discount. The journal entry that Ryan makes on September 18 is:

A)

Cash

5,684

Sales discounts

116

Accounts receivable

5,800

B)

Cash

5,194

Sales discounts

106

Accounts receivable

5,300

C)

Cash

5,800

Accounts receivable

5,800

D)

Cash

5,684

Accounts receivable

5,684

E)

Cash

5,194

Accounts receivable

5,194

_____

1. A measure of a company’s ability to pay its current liabilities that

excludes less liquid current assets such as inventory and prepaid expenses.

_____

2. A widely used income statement format that lists cost of goods sold as

another expense and shows only one subtotal for total expenses.

_____

3. The point of transfer from seller to buyer that takes place when the

goods arrive at the buyer’s place of business.

_____

4. Products a company owns and intends to sell.

_____

5. The expenses that support a company’s overall operations and include

costs related to accounting, human resource management and financial

management.

_____

6. The point of transfer from seller to buyer that takes place when goods

depart the seller’s place of business.

_____

7. Inventory losses that can occur as a result of theft or deterioration and

require an adjusting entry to account for those losses.

_____

8. An income statement format that shows detailed computations of net

sales and other costs and expenses, and reports subtotals for various classe

of items.

_____

9. A given percent deducted from a list price often granted to customers

purchasing large quantities of merchandise.

_____

10. The expenses of promoting sales by displaying and advertising

merchandise, making sales, and delivering goods to customers.

SHORT ANSWER QUESTIONS

179)

Match the following definitions and terms by placing the letter for the terms A through J in the

blank space next to the best definition.

A. Trade discount F. Acid-test ratio

B. General and administrative expenses G. Merchandise inventory

C. FOB shipping point H. Selling expenses

D. Single-step income statement I. Multiple-step income statement

E. FOB destination J. Inventory shrinkage

s

180)

Match the following terms with the appropriate definition.

A. Debit memorandum

B. Credit period

C. Credit terms

D. Credit memorandum

E. Discount period

F. Gross profit

G. Periodic inventory system

H. Perpetual inventory system

I. Sales discount

J. Purchase discount

_____

1. An inventory accounting method that continually updates accounting

records for inventory available for sale and inventory sold.

_____

2. An inventory accounting method that updates the accounting records for

merchandise transactions only at the end of a period.

_____

3. The time period in which reduced payment can be made by the buyer

because of a cash discount offered by a seller of goods on credit.

_____

4. A notification that informs the seller of a debit made to the seller’s

account payable in the buyer’s records.

_____

5. A cash discount granted, from the view of the purchaser intended to

encourage buyers to pay amounts owed earlier.

_____

6. A notification that informs a buyer of a seller’s credit to a buyer’s

account.

_____

7. A cash discount granted from the view of the seller, indicated in the

credit terms on the invoice.

_____

8. The calculation of net sales less cost of goods sold.

_____

9. The description of the amounts and timing of payments from a buyer to

a seller for a purchase.

_____

10. The amount of time allowed before full payment is due.

ESSAY QUESTIONS

181)

Identify and explain the key components of a merchandiser’s net income.

182)

Describe the difference between wholesalers and retailers.

183)

Describe the key attributes of inventory for a merchandising company.