Chapter 5

80. A check drawn by a depositor for $810 in payment of a liability was recorded by the depositor as $180. The $630

difference would be included on the bank reconciliation as a(n):

a.

addition to the cash balance per books.

b.

addition to the cash balance per bank.

c.

deduction from the cash balance per bank.

d.

deduction from the cash balance per books.

Multiple Choice

SACC.WARR.18.5-5 – LO: 05.05

United States – BUSPROG: Analytic

Bloom’s: Applying

7/19/2016 9:49 AM

7/19/2016 9:49 AM

81. The amount of deposits in transit is included on the bank statement as a(n):

a.

deduction from the cash balance per books.

b.

deduction from the cash balance per bank.

c.

addition to the cash balance per bank.

d.

addition to the cash balance per books.

Multiple Choice

SACC.WARR.18.5-5 – LO: 05.05

United States – BUSPROG: Analytic

Bloom’s: Understanding

7/19/2016 9:49 AM

Chapter 5

82. Accompanying the bank statement was a debit memorandum for an NSF check received from a customer. This item

would require an adjusting entry including a:

a.

debit to Accounts Receivable.

b.

debit to Cash.

c.

debit to Accounts Payable.

d.

credit to Accounts Payable.

Multiple Choice

SACC.WARR.18.5-5 – LO: 05.05

United States – BUSPROG: Analytic

Bloom’s: Understanding

7/19/2016 9:49 AM

7/19/2016 9:49 AM

83. Which of the following would be deducted from the cash balance per books on a bank reconciliation?

a.

Service charges

b.

Outstanding checks

c.

Deposits in transit

d.

Notes collected by the bank

Multiple Choice

SACC.WARR.18.5-5 – LO: 05.05

United States – BUSPROG: Analytic

Bloom’s: Understanding

7/19/2016 9:49 AM

Chapter 5

84. A canceled check for $1,900 was erroneously recorded by the bank as $9,100. How is the error adjusted in a bank

reconciliation?

a.

The amount is deducted from the cash balance in the bank section of the reconciliation.

b.

The amount is deducted from the cash balance in the company section of the reconciliation.

c.

The amount is added to the cash balance in the bank section of the reconciliation.

d.

The amount is added to the cash balance in the company section of the reconciliation.

Multiple Choice

SACC.WARR.18.5-5 – LO: 05.05

United States – BUSPROG: Analytic

United States – AK – DISC: AICPA: FN-Measurement

Bloom’s: Applying

7/19/2016 9:49 AM

11/8/2016 3:35 AM

85. WFC Co.’s petty cash receipts indicate the following expenditures for the end of October:

Office supplies

$500

Miscellaneous selling expense

$350

Miscellaneous administrative expense

$160

As a result of these transactions, WFC Co.’s stockholders’ equity:

a.

remains unchanged.

b.

increases by $500.

c.

decreases by $1,010.

d.

decreases by $510.

Multiple Choice

SACC.WARR.18.5-6 – LO: 05.06

7/19/2016 9:49 AM

Chapter 5

86. A special cash fund used to make small payments that occur frequently is called a(n):

a.

operating expenses fund.

b.

change fund.

c.

market fund.

d.

petty cash fund.

Multiple Choice

SACC.WARR.18.5-6 – LO: 05.06

United States – BUSPROG: Analytic

Bloom’s: Remembering

7/19/2016 9:49 AM

7/19/2016 9:49 AM

87. Terri Co. established a petty cash fund of $2,300. What is the effect of this transaction?

a.

Accounts payable increases

b.

Retained earnings decreases

c.

Cash decreases

d.

Expenses increases

Multiple Choice

United States – BUSPROG: Analytic

Bloom’s: Applying

7/19/2016 9:49 AM

11/8/2016 5:06 AM

Chapter 5

88. ABC Co.’s petty cash receipts indicate the following expenditures for the end of October:

Office supplies

$490

Miscellaneous selling expense

$300

Miscellaneous administrative expense

$120

What is the cumulative effect of these transactions on the statement of cash flows?

a.

$420 decrease in financing activities

b.

$490 increase in operating activities

c.

$910 decrease in operating activities

d.

No effect on the statement of cash flows

Multiple Choice

SACC.WARR.18.5-6 – LO: 05.06

United States – BUSPROG: Analytic

Bloom’s: Applying

7/19/2016 9:49 AM

11/8/2016 3:09 AM

89. XYZ Co.’s petty cash receipts indicate the following expenditures for the end of October:

Office supplies

$490

Miscellaneous selling expense

$300

Miscellaneous administrative expense

$120

These transactions would result in a:

SACC.WARR.18.5-6 – LO: 05.06

United States – BUSPROG: Analytic

Bloom’s: Applying

7/19/2016 9:49 AM

11/8/2016 2:44 AM

Chapter 5

a.

$910 increase in total assets.

b.

$490 decrease in stockholders’ equity.

c.

$420 decrease in total assets.

d.

$910 increase in stockholders’ equity.

c

Moderate

Multiple Choice

False

SACC.WARR.18.5-6 – LO: 05.06

United States – BUSPROG: Analytic

Bloom’s: Applying

7/19/2016 9:49 AM

11/8/2016 4:38 AM

JFND-GO3A-EW4R-EP4G

90. The highly liquid investments that a company may invest in when they temporarily have excess cash are called _____.

a.

cash equivalents

b.

bank overdrafts

c.

cash short and over

d.

vouchers

a

Easy

Multiple Choice

False

SACC.WARR.18.5-7 – LO: 05.07

United States – BUSPROG: Analytic

Bloom’s: Remembering

7/19/2016 9:49 AM

11/8/2016 4:42 AM

JFND-GO3A-EW4R-EP3I

Chapter 5

91. The following data is given for DGR Company:

Net cash flows from operating activities

$6,000,000

Cash and cash equivalents at end of year

$2,700,000

DGR Company’s ratio of cash to monthly cash expenses is:

a.

4.5 months.

b.

5.4 months.

c.

8.1 months.

d.

3.2 months.

Multiple Choice

SACC.WARR.18.5-8 – LO: 05.08

United States – BUSPROG: Analytic

United States – AK – DISC: AICPA: FN-Measurement

Bloom’s: Applying

7/19/2016 9:49 AM

11/8/2016 7:48 AM

92. The ratio of cash to monthly cash expenses can be used to _____.

a.

assess how long a company with positive cash flows from investing activities can continue to operate

b.

assess how long a company with negative cash flows from operations can continue to operate

c.

assess how long a company with negative cash flows from investing activities can continue to operate

d.

assess how long a company with positive cash flows from financing activities can continue to operate

Multiple Choice

SACC.WARR.18.5-8 – LO: 05.08

United States – BUSPROG: Analytic

Bloom’s: Understanding

7/19/2016 9:49 AM

7/19/2016 9:49 AM

Chapter 5

93. The ratio of cash to monthly cash expenses is computed as _____.

a.

monthly cash expenses divided by cash

b.

current assets divided by monthly cash expenses

c.

cash divided by cash equivalents

d.

cash and cash equivalents divided by monthly cash expenses

Multiple Choice

SACC.WARR.18.5-8 – LO: 05.08

United States – BUSPROG: Analytic

Bloom’s: Remembering

7/19/2016 9:49 AM

7/19/2016 9:49 AM

94. Denominator in the ratio of cash to monthly cash expense is calculated as _____.

a.

total revenues divided by 12

b.

net cash flows from investing activities divided by 12

c.

earnings before taxes divided by 12

d.

net cash flows from operations divided by 12

Multiple Choice

SACC.WARR.18.5-8 – LO: 05.08

United States – BUSPROG: Analytic

Bloom’s: Remembering

7/19/2016 9:49 AM

7/19/2016 9:49 AM

Chapter 5

95. If a company’s net cash flows from operating activities is $1,500,000 for a year and its end of the year cash and cash

equivalents balance is $750,000, determine the company’s ratio of cash to monthly cash expenses.

a.

6 months

b.

2 months

c.

5 months

d.

9 months

Multiple Choice

SACC.WARR.18.5-8 – LO: 05.08

United States – BUSPROG: Analytic

Bloom’s: Applying

7/19/2016 9:49 AM

11/8/2016 4:43 AM

96. When a company reports negative net cash flows from operations _____.

a.

ratio of equity to annual cash expenses helps in assessing the survival of the company

b.

ratio of equity to monthly cash expenses helps in assessing the survival of the company

c.

ratio of cash to monthly cash expenses helps in assessing the survival of the company

d.

ratio of accounts payable to annual financing expenses helps in assessing the survival of the company

Multiple Choice

SACC.WARR.18.5-8 – LO: 05.08

United States – BUSPROG: Analytic

United States – AK – DISC: AICPA: FN-Measurement

Bloom’s: Understanding

Chapter 5

97. List the objectives of internal control and give an example of how each is implemented.

(1)

Assets are safeguarded and used for business purposes.

(2)

Business information is accurate.

(3)

Employees comply with laws and regulations.

(1)

Duties are separated.

(2)

Duties are rotated.

(3)

Reports are submitted to management.

There are many other examples that would be correct.

Moderate

Subjective Short Answer

False

SACC.WARR.18.5-2 – LO: 05.02

United States – BUSPROG: Analytic

Bloom’s: Understanding

7/19/2016 9:49 AM

7/19/2016 9:49 AM

JFND-GO3A-EW4R-EPNR

4OTI-GO4W-NQNBEE

98. For each of the following procedures, indicate whether it is an internal control strength or a weakness. Also, for each

weakness, explain why it is a weakness and how it can be corrected.

(a)

Only the best accounting graduates are hired to eliminate the need for training.

(b)

The person responsible for order supplies also records the receipt of the supplies.

(c)

Company policy mandates that all employees take vacation time.

(d)

Internal auditors constantly monitor the internal control system.

(e)

The accountant deposits cash at least once each day.

receiving supplies. The company must assign this task to someone else.

(c)

Strength.

(d)

Strength.

7/19/2016 9:49 AM

7/19/2016 9:49 AM

JFND-GO3A-EW4R-EPNF

Chapter 5

99. List and define each of the five elements of internal control set forth by the Integrated Framework.

Chapter 5

100. Identify each of the following as related to (a) the control environment, (b) risk assessment, or (c) control procedures.

(1) Mandatory vacations

(2) Personnel policies

(3) Report of outside consultants on future market changes

101. Describe the features of a voucher system and list typical supporting documents for a voucher.

Chapter 5

102. List the advantages of Electronic Funds Transfers.

Easy

Subjective Short Answer

False

SACC.WARR.18.5-3 – LO: 05.03

United States – BUSPROG: Analytic

Bloom’s: Understanding

7/19/2016 9:49 AM

7/19/2016 9:49 AM

JFND-GO3A-EW4R-EPBT

4OTI-GO4W-NQNBEE

103. From the following particulars of Purple New Co., prepare the bank reconciliation statement as on May 31, 2016.

(a)

The bank statement balance is $4,000.

(b)

The cash account balance is $3,950.

(c)

Outstanding checks amounted to $960.

(d)

Deposits in transit are $900.

(e)

The bank service charge is $75.

(f)

Interest added to the checking account by the bank is $150.

(g)

A check drawn for $65 was incorrectly charged by the bank as $150.

Cash balance according to bank statement

Deduct: Outstanding checks

7/19/2016 9:49 AM

7/19/2016 9:49 AM

JFND-GO3A-EW4R-EPB1

Chapter 5

104. Using the following information, list the items that will require adjustments to the accounts of Salem Co. Also,

indicate which accounts will increase or decrease due to the adjustment.

(a)

The bank statement balance is $2,597.

(b)

The cash account balance is $2,680.

(c)

Outstanding checks amounted to $703.

(d)

Deposits in transit are $732.

(e)

The bank service charge is $25.

(f)

Interest added to the checking account by the bank is $7.

(g)

A check drawn for $59 was incorrectly charged by the bank as $95.

Service charge $25; Cash will decrease by $25 and Retained Earnings decrease by $25.

(f)

Interest income $7; Cash will increase by $7 and Retained Earnings will increase by $7.

Moderate

Subjective Short Answer

False

SACC.WARR.18.5-5 – LO: 05.05

United States – BUSPROG: Analytic

Bloom’s: Applying

7/19/2016 9:49 AM

7/19/2016 9:49 AM

Adjusted balance

Cash balance according to Purple New Co.

Add: Interest credited by bank

Deduct: Bank service charge

Challenging

Subjective Short Answer

False

SACC.WARR.18.5-5 – LO: 05.05

United States – BUSPROG: Analytic

Bloom’s: Applying

7/19/2016 9:49 AM

11/9/2016 1:02 AM

JFND-GO3A-EW4R-EPBO

Chapter 5

Cash balance according to bank statement

Add: Deposits in transit not recorded by bank

Deduct: Outstanding checks

Adjusted balance

Cash balance according to Exible Co.

Add: Note collected by bank, including $63 interest

Error in recording cash sales of $351 as $315

Deduct: NSF check from BlueInk

Adjusted balance

Challenging

Subjective Short Answer

False

SACC.WARR.18.5-5 – LO: 05.05

United States – BUSPROG: Analytic

United States – DISC: – ACBSP: APC–11 – Bank Reconciliation

Bloom’s: Applying

7/19/2016 9:49 AM

11/8/2016 4:04 AM

JFND-GO3A-EW4R-EPBS

105. The bank statement for Exible Co. indicates a balance of $10,252.50 on June 30, 2016. The cash account for the

company had a balance of $4,787.10. Prepare a bank reconciliation on the basis of the following reconciling items:

(a)

Cash sales of $351 had been erroneously recorded as $315.

(b)

Deposits in transit not recorded by bank, $500.

(c)

Bank debit memorandum for service charges, $45.

(d)

Bank credit memorandum for note collected by bank, $2,782, including $63 interest.

(e)

Bank debit memorandum for $223.40 NSF (not sufficient funds) check from Alice

Martin, a customer.

(f)

Checks outstanding, $3,415.80.

JFND-GO3A-EW4R-EPBZ

Chapter 5

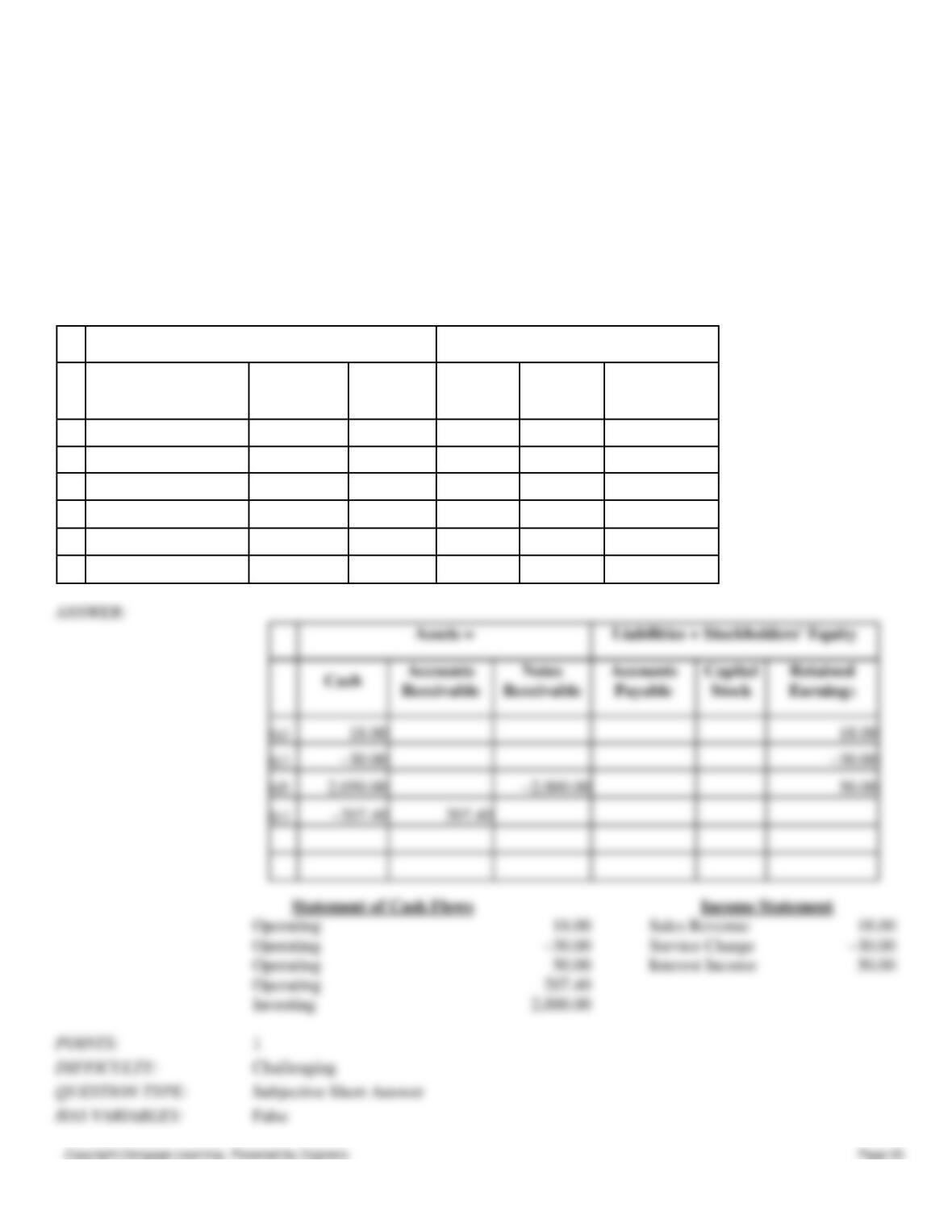

106. The bank statement for Marley Co. indicates a cash balance of $10,000.50 on June 30, 2016. The cash account in

Marley’s records had a balance of $4,677.10. Illustrate the adjustments to the accounts and their effect on Marley’s

financial statements, based on the following reconciling items:

(a)

Cash sales of $342 had been erroneously recorded in the cash receipts journal as $324.

(b)

Deposits in transit not recorded by bank, $700.

(c)

Bank debit memorandum for service charges, $30.

(d)

Bank credit memorandum for note collected by bank, $2,050, including $50 interest.

(e)

Bank debit memorandum for $207.40 NSF (not sufficient funds) check from Alice

Martin, a customer.

(f)

Checks outstanding, $4,192.80.

Operating

Sales Revenue

Operating

Service Charge

Operating

Interest Income

Operating

Investing

Capital

Retained

(a)

(c)

(d)

(e)

Subjective Short Answer

False

Assets =

Liabilities + Stockholders’ Equity

Cash

Accounts

Receivable

Notes

Receivable

Accounts

Payable

Capital

Stock

Retained

Earnings

Chapter 5

107. Using the following information, prepare a bank reconciliation for Murack Co. for May 31, 2016:

(a)

The bank statement balance is $4,063.

(b)

The cash account balance is $3,735.

(c)

Outstanding checks amounted to $640.

(d)

Deposits in transit are $245.

(e)

The bank service charge is $40.

(f)

A check for $74 for supplies was recorded on the depositor’s books as $47.

Cash balance according to bank statement

Add: Deposits in transit not recorded by bank

Deduct: Outstanding checks

Adjusted balance

Cash balance according to Murack Co.

Deduct: Bank service charge

Adjusted balance

Moderate

Subjective Short Answer

False

SACC.WARR.18.5-5 – LO: 05.05

United States – BUSPROG: Analytic

Bloom’s: Applying

11/8/2016 6:13 AM

JFND-GO3A-EW4R-EPKR

SACC.WARR.18.5-5 – LO: 05.05

United States – BUSPROG: Analytic

Bloom’s: Applying

7/19/2016 9:49 AM

11/8/2016 5:14 AM

JFND-GO3A-EW4R-EPBI

GO4W-NQNBEE

Chapter 5

108.

(a)

Where are cash equivalents disclosed in the financial statements?

(b)

List three examples of cash equivalents.

(a)

Cash account on the balance sheet.

Bills.

Easy

Subjective Short Answer

False

SACC.WARR.18.5-7 – LO: 05.07

United States – BUSPROG: Analytic

Bloom’s: Understanding

7/19/2016 9:49 AM

7/19/2016 9:49 AM

JFND-GO3A-EW4R-EPBW

109. Why would a bank require a company to maintain a compensating balance?

Usually it is part of a loan agreement or line of credit.

Easy

Subjective Short Answer

False

SACC.WARR.18.5-7 – LO: 05.07

United States – BUSPROG: Analytic

United States – AK – DISC: AICPA: FN-Measurement

Bloom’s: Understanding

7/19/2016 9:49 AM

7/19/2016 9:49 AM

JFND-GO3A-EW4R-EPKN

Chapter 5