118. McGraw Corp. owned all of the voting common stock of both Ritter Co. and

Lawler Co. During 2011, Ritter sold inventory to Lawler. The goods had cost Ritter

$65,000, and they were sold to Lawler for $100,000. At the end of 2011, Lawler

still held 30% of the inventory.

Required:

How should the sale between Lawler and Ritter be accounted for in a

consolidation worksheet? Show worksheet entries to support your answer.

119. Virginia Corp. owned all of the voting common stock of Stateside Co. Both

companies use the

perpetual inventory method

, and Virginia decided to use the

partial equity method

to account for this investment. During 2010, Virginia made

cash sales of $400,000 to Stateside. The gross profit rate was 30% of the selling

price. By the end of 2010, Stateside had sold 75% of the goods to outside parties

for $420,000 cash.

Prepare

journal entries

for Virginia and Stateside to record the sales/purchases

during 2010.

120. Virginia Corp. owned all of the voting common stock of Stateside Co. Both

companies use the

perpetual inventory method

, and Virginia decided to use the

partial equity method

to account for this investment. During 2010, Virginia made

cash sales of $400,000 to Stateside. The gross profit rate was 30% of the selling

price. By the end of 2010, Stateside had sold 75% of the goods to outside parties

for $420,000 cash.

Prepare the

consolidation entries

that should be made at the end of 2010.

121. Virginia Corp. owned all of the voting common stock of Stateside Co. Both

companies use the

perpetual inventory method

, and Virginia decided to use the

partial equity method

to account for this investment. During 2010, Virginia made

cash sales of $400,000 to Stateside. The gross profit rate was 30% of the selling

price. By the end of 2010, Stateside had sold 75% of the goods to outside parties

for $420,000 cash.

Prepare any 2011

consolidation worksheet entries

that would be required

regarding the 2010 inventory transfer.

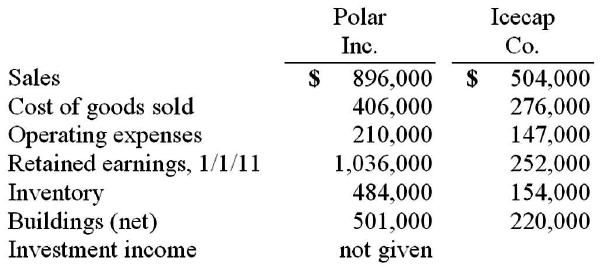

122. Several years ago Polar Inc. acquired an 80% interest in Icecap Co. The

book values of Icecap’s asset and liability accounts at that time were considered

to be equal to their fair values. Polar’s acquisition value corresponded to the

underlying book value of Icecap so that no allocations or goodwill resulted from

the transaction.

The following selected account balances were from the individual financial

records of these two companies as of December 31, 2011:

Assume that Polar sold inventory to Icecap at a markup equal to 25% of cost.

Intra-entity transfers were $130,000 in 2010 and $165,000 in 2011. Of this

inventory, $39,000 of the 2010 transfers were retained and then sold by Icecap in

2011, while $55,000 of the 2011 transfers were held until 2012.

Required:

For the consolidated financial statements for 2011, determine the balances that

would appear for the following accounts: (1) Cost of Goods Sold, (2) Inventory,

and (3) Non-controlling Interest in Subsidiary’s Net Income.

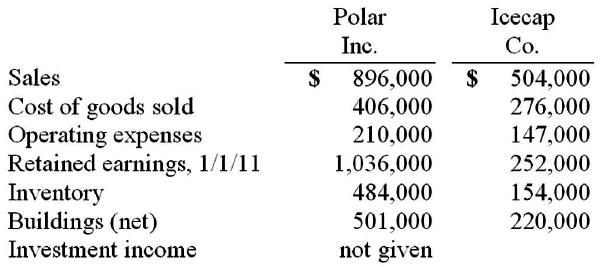

123. Several years ago Polar Inc. acquired an 80% interest in Icecap Co. The

book values of Icecap’s asset and liability accounts at that time were considered

to be equal to their fair values. Polar’s acquisition value corresponded to the

underlying book value of Icecap so that no allocations or goodwill resulted from

the transaction.

The following selected account balances were from the individual financial

records of these two companies as of December 31, 2011:

Assume that Icecap sold inventory to Polar at a markup equal to 25% of cost.

Intra-entity transfers were $70,000 in 2010 and $112,000 in 2011. Of this

inventory, $29,000 of the 2010 transfers were retained and then sold by Polar in

2011, whereas $49,000 of the 2011 transfers were held until 2012.

Required:

For the consolidated financial statements for 2011, determine the balances that

would appear for the following accounts: (1) Cost of Goods Sold, (2) Inventory,

and (3) Non-controlling Interest in Subsidiary’s Net Income.

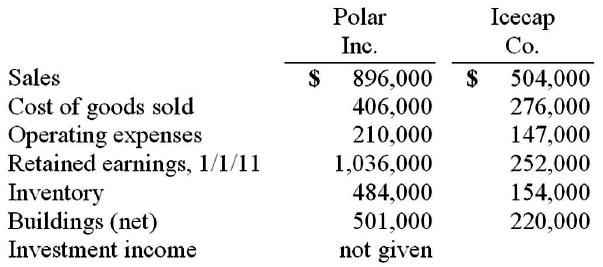

124. Several years ago Polar Inc. acquired an 80% interest in Icecap Co. The

book values of Icecap’s asset and liability accounts at that time were considered

to be equal to their fair values. Polar’s acquisition value corresponded to the

underlying book value of Icecap so that no allocations or goodwill resulted from

the transaction.

The following selected account balances were from the individual financial

records of these two companies as of December 31, 2011:

Polar sold a building to Icecap on January 1, 2010 for $112,000, although the book

value of this asset was only $70,000 on that date. The building had a five-year

remaining useful life and was to be depreciated using the

straight-line method

with

no salvage value

.

Required:

For the consolidated financial statements for 2011, determine the balances that

would appear for the following accounts: (1) Buildings (net), (2) Operating

expenses, and (3) Non-controlling Interest in Subsidiary’s Net Income.

125. On January 1, 2011, Musial Corp. sold equipment to Matin Inc. (a wholly-

owned subsidiary) for $168,000 in cash. The equipment originally cost $140,000

but had a book value of only $98,000 when transferred. On that date, the

equipment had a five-year remaining life. Depreciation expense was calculated

using the straight-line method.

Musial earned $308,000 in net income in 2011 (not including any investment

income) while Matin reported $126,000. Assume there is no amortization related

to the original investment.

What is consolidated net income for 2011?

126. On January 1, 2011, Musial Corp. sold equipment to Matin Inc. (a wholly-

owned subsidiary) for $168,000 in cash. The equipment originally cost $140,000

but had a book value of only $98,000 when transferred. On that date, the

equipment had a five-year remaining life. Depreciation expense was calculated

using the straight-line method.

Musial earned $308,000 in net income in 2011 (not including any investment

income) while Matin reported $126,000. Assume there is no amortization related

to the original investment.

Assuming that Musial owned only 90% of Matin, what is consolidated net income

for 2011?

127. On January 1, 2011, Musial Corp. sold equipment to Matin Inc. (a wholly-

owned subsidiary) for $168,000 in cash. The equipment originally cost $140,000

but had a book value of only $98,000 when transferred. On that date, the

equipment had a five-year remaining life. Depreciation expense was calculated

using the straight-line method.

Musial earned $308,000 in net income in 2011 (not including any investment

income) while Matin reported $126,000. Assume there is no amortization related

to the original investment.

Prepare a schedule of consolidated net income and the share to controlling and

non-controlling interests for 2011, assuming that Musial owned only 90% of Matin

and the equipment transfer had been upstream