162. Listed below are ten terms followed by a list of phrases that describe or characterize five

of the terms. Match each phrase with the best term placing the letter designating the term in

the space provided.

Terms:

a. Accounts receivable

b. Allowance method

c. No effect

d. Direct write-off method

e. Net realizable value

f. Aging method

g. Bad debt expense

h. Receivables written off

i. Decrease assets and increase expenses

j. Allowance for uncollectible accounts

_____ Accounts receivable less allowance for uncollectible accounts.

163. A company uses the allowance method to account for uncollectible accounts. During the

year, the company has actual bad debts of $25,000. Record the write-off of the uncollectible

accounts.

164. At the beginning of the year, a company had an Allowance for Uncollectible Accounts of

$22,000. By the end of the year, actual bad debts total $24,000. What is the balance of the

Allowance for Uncollectible Accounts after the write-offs (before any year-end adjustment)?

165. On March 13, a company writes off a customer’s account of $3,800. On June 3, the

customer unexpectedly pays the $3,800 balance. Using the allowance method, record the

write-off on March 13 and the cash collection on June 3.

166. A company has the following accounts receivable and estimates of uncollectible

accounts:

Compute the total estimated uncollectible accounts.

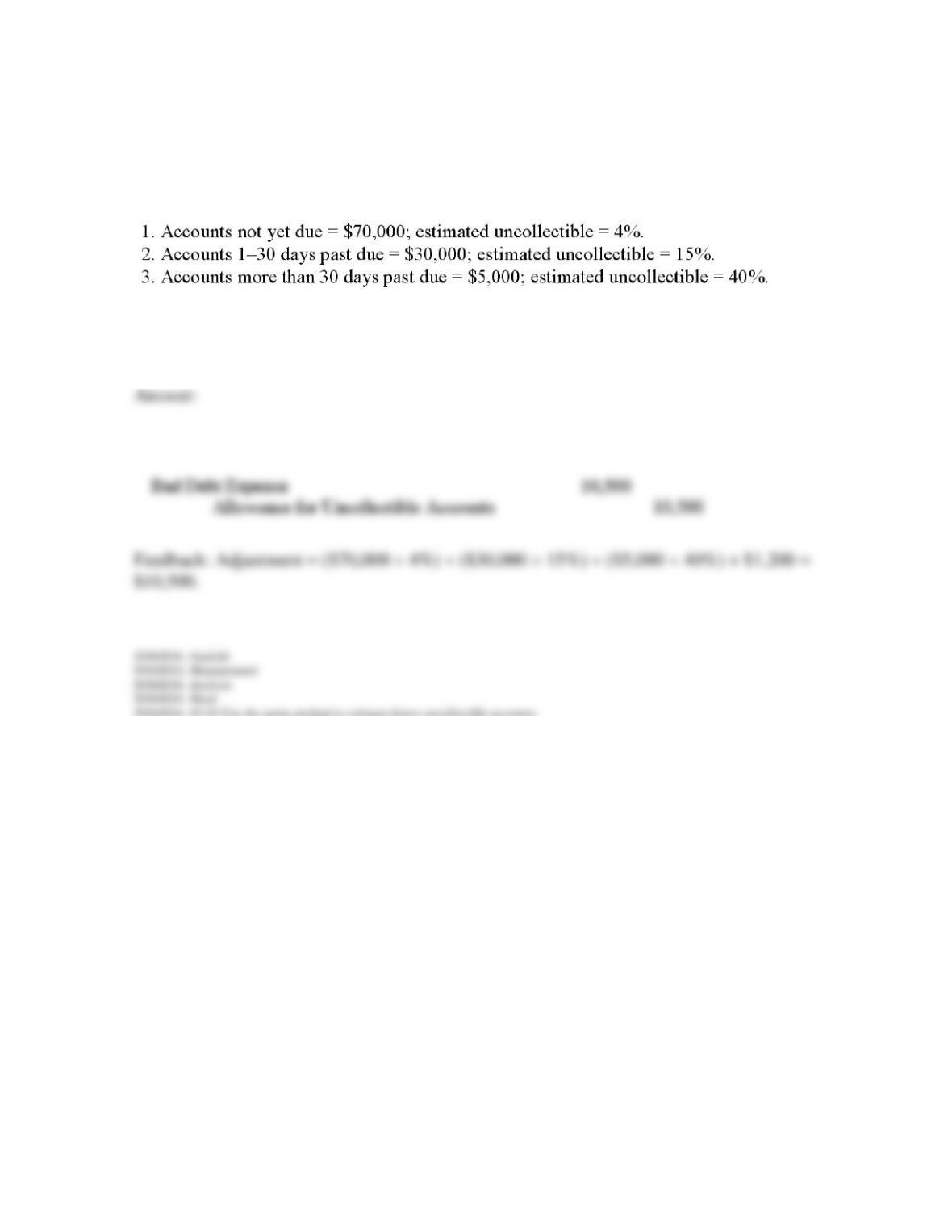

167. At the end of the year, a company has the following accounts receivable and estimates of

uncollectible accounts:

Record the year-end adjustment for uncollectible accounts, assuming the current balance of

the Allowance for Uncollectible Accounts is $900 (credit).

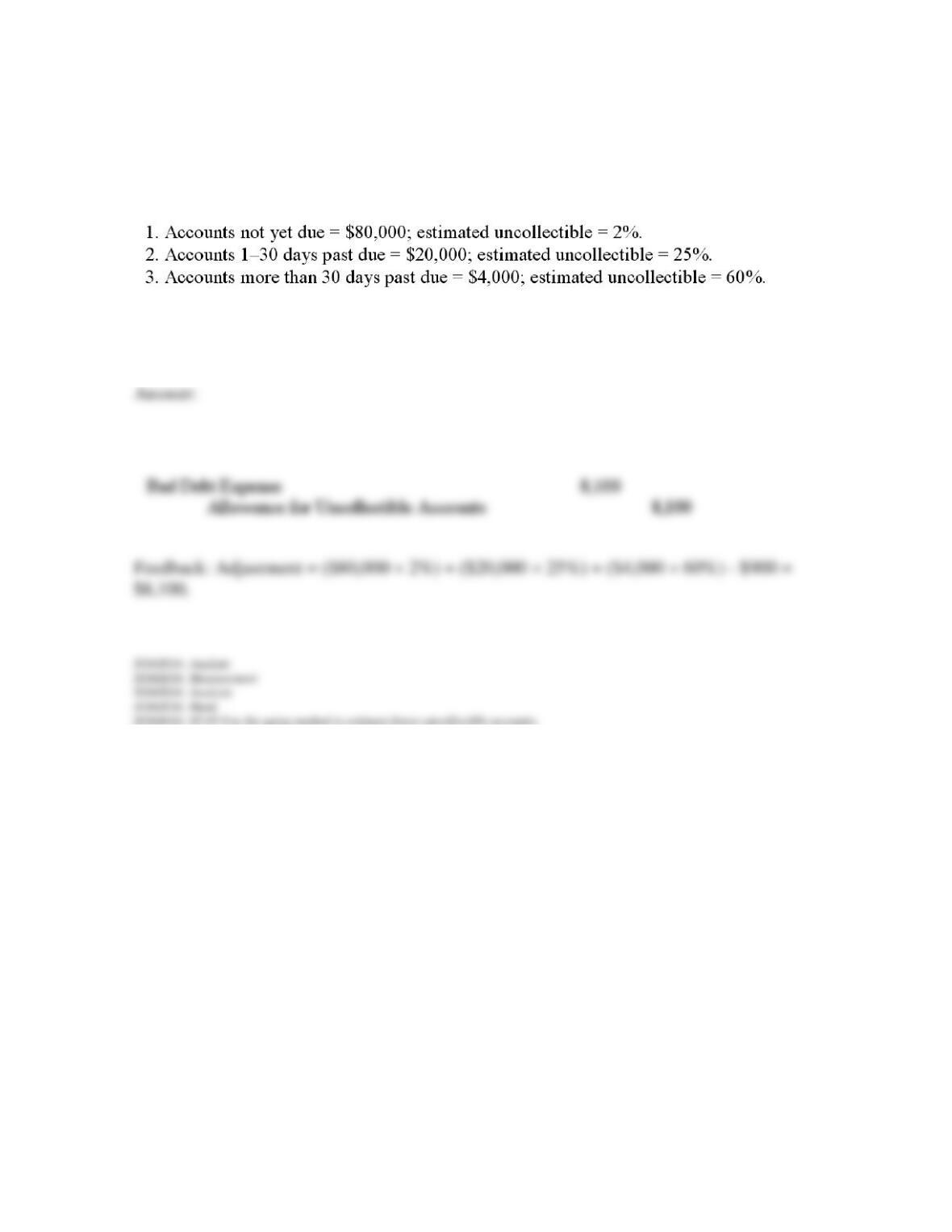

168. At the end of the year, a company has the following accounts receivable and estimates of

uncollectible accounts:

Record the year-end adjustment for uncollectible accounts, assuming the current balance of

the Allowance for Uncollectible Accounts is $1,200 (debit).

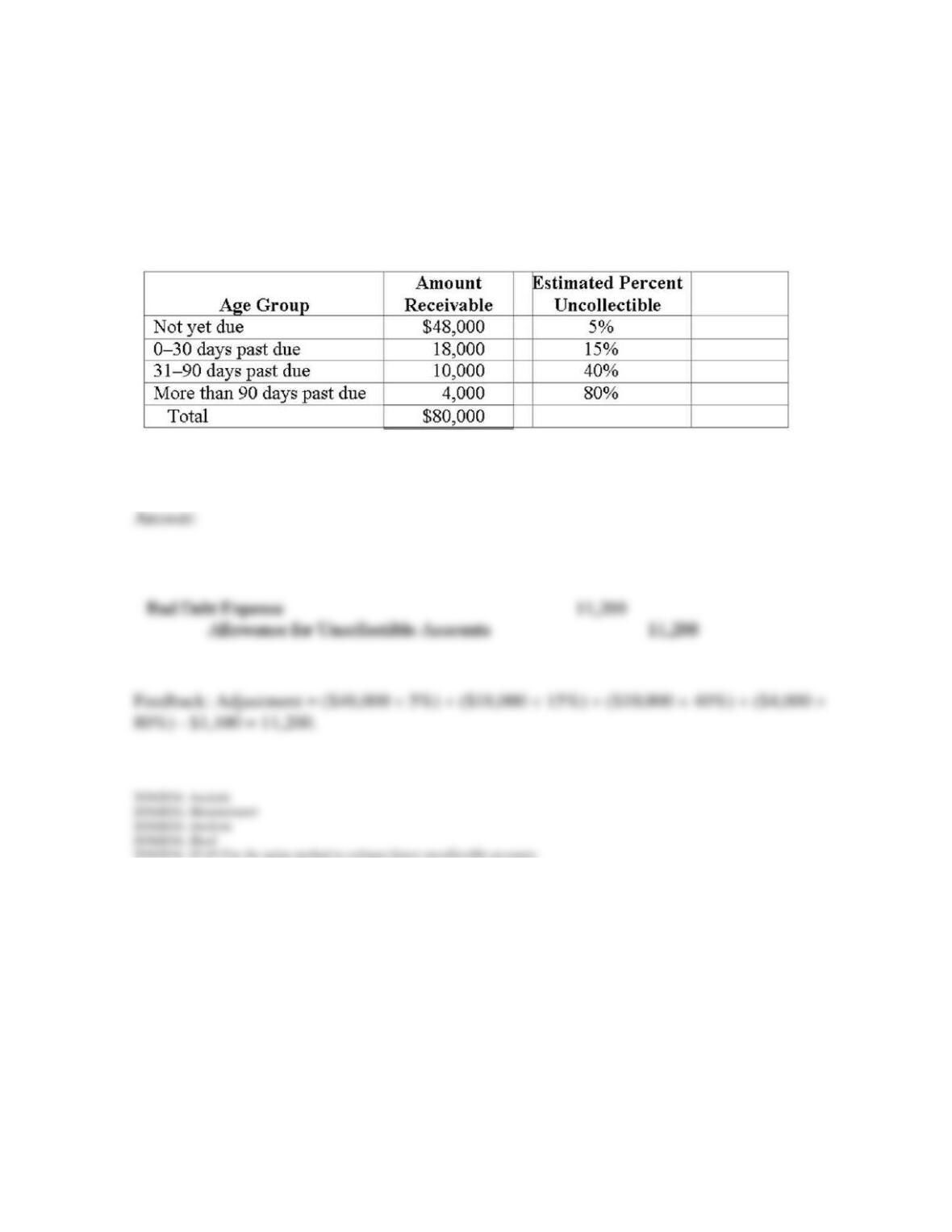

169. A company has the following balances on December 31, 2012, before any year-end

adjustments: Accounts Receivable = $80,000; Allowance for Uncollectible Accounts =

$1,100 (credit). The company estimates uncollectible accounts based on an aging of accounts

receivable as shown below:

Record the adjustment for uncollectible accounts on December 31, 2012.

170. Discuss the differences between the allowance method and the direct write-off method

for recording uncollectible accounts. Which of the two is acceptable under financial

accounting rules?

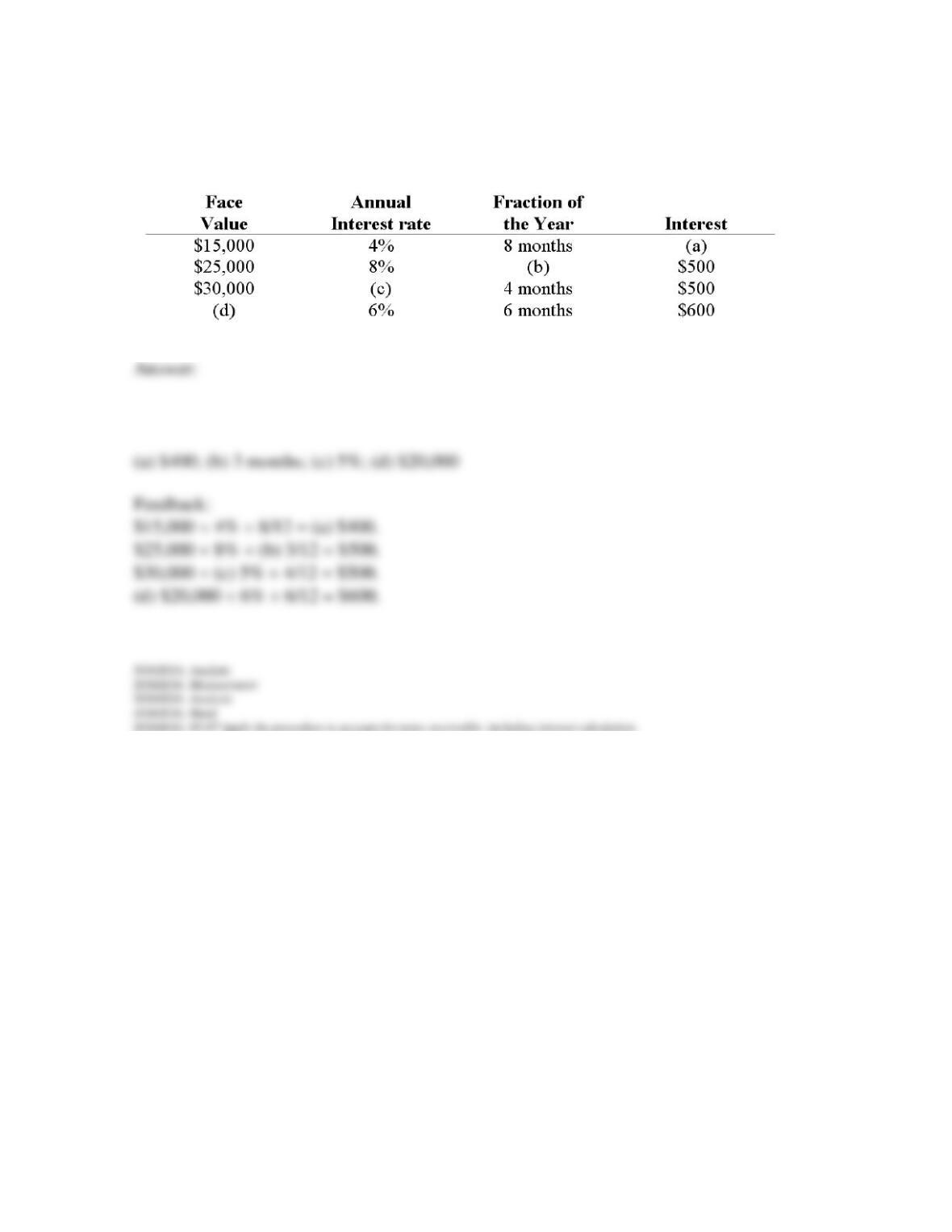

171. Calculate the missing amount for each of the following notes receivable.

172. On February 1, 2012, a company loans one of its employees $20,000 and accepts a nine-

month, 8% note receivable. Calculate the amount of interest revenue the company will

recognize in 2012.

173. On July 1, 2012, a company loans one of its employees $20,000 and accepts a nine-

month, 8% note receivable. Calculate the amount of interest revenue the company will

recognize in 2012 and 2013.

174. On April 1, 2012, a company loans one of its suppliers $50,000 and accepts a 24-month,

12% note receivable. Calculate the amount of interest revenue the company will recognize in

2012, 2013, and 2014.

175. On April 14, a company lends $10,000 cash to one of its employees and accepts a six-

month, 12% note in return. Record the acceptance of the note receivable.

176. On April 1, a company provides services to one of its customers for $12,000. As

payment for the services, the company accepts a six-month, 10% note from the customer.

Record the acceptance of the note receivable on April 1 and the cash collection on October 1.

177. On May 1, 2012, a company lends $100,000 to one of its main suppliers and accepts a

12-month, 6% note. Record the acceptance of the note on May 1, 2012, the adjustment on

December 31, 2012, and the cash collection on May 1, 2013.

178. Below are amounts for two companies:

For each company, calculate the receivables turnover ratio. Which company appears more

efficient in collecting cash from sales?

179. How is the receivables turnover ratio measured? What does this ratio indicate? Is a

higher or lower receivables turnover preferable?

180. At the end of the year, a company reports a balance in its Allowance for Uncollectible

Accounts of $1,400 (credit) before any year-end adjustment. The company estimates future

uncollectible accounts to be 3% of credit sales for the year. Credit sales for the year total

$280,000. Record the adjustment for the allowance for uncollectible accounts using the

percentage-of-credit-sales method.

181. At the end of the year, a company reports a balance in its Allowance for Uncollectible

Accounts of $1,400 (debit) before any year-end adjustment. The company estimates future

uncollectible accounts to be 3% of credit sales for the year. Credit sales for the year total

$280,000. Record the adjustment for the allowance for uncollectible accounts using the

percentage-of-credit-sales method.

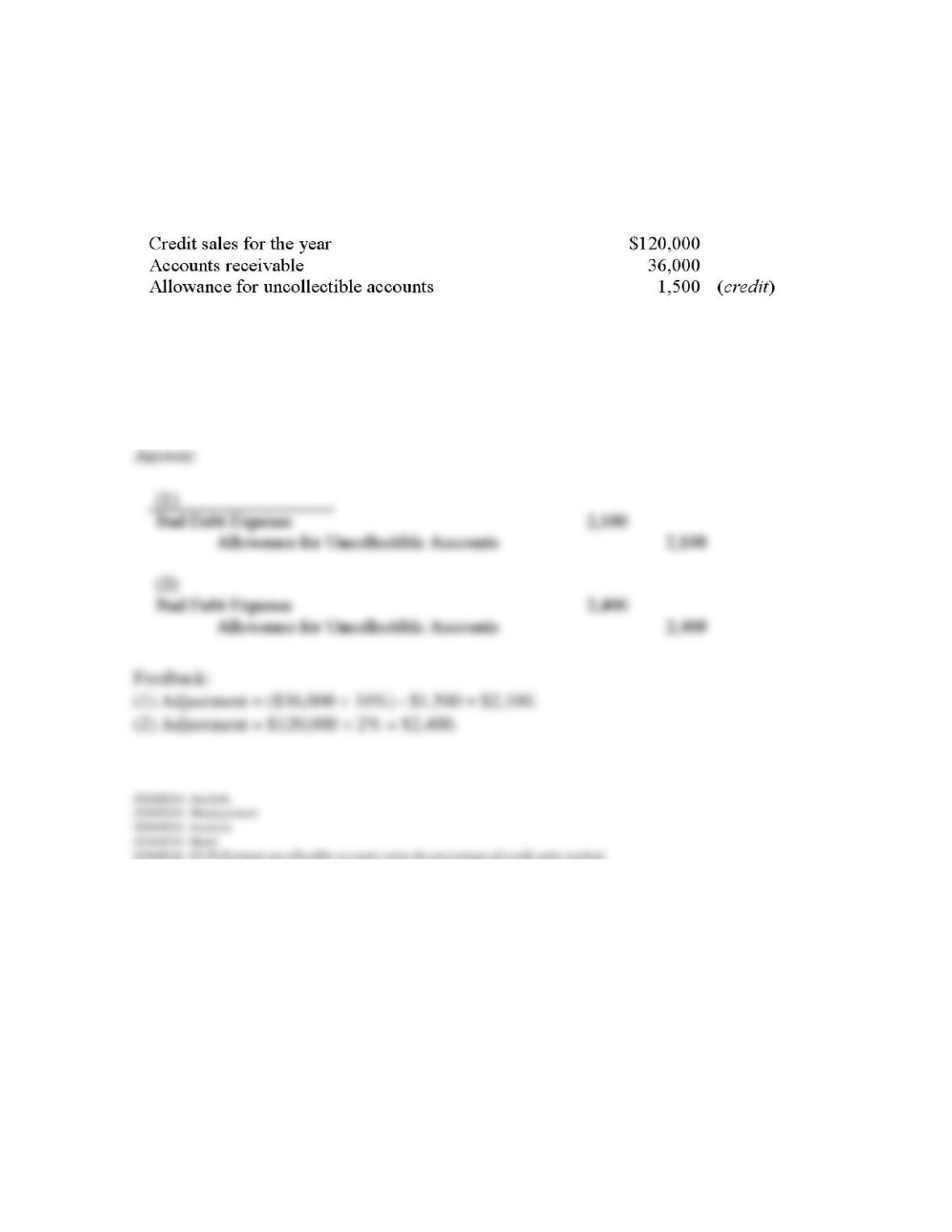

182. A company reports the following amounts at the end of the year (before any year-end

adjustment).

Record the adjustment for uncollectible accounts (1) using the percentage-of-receivables

method, assuming the company estimates 10% of receivables will not be collected, and (2)

using the percentage-of-credit-sales method, assuming the company estimates 2% of credit

sales will not be collected.

183. Explain why the percentage-of-receivables method is referred to as the balance sheet

method and the percentage-of-credit-sales method is referred to as the income statement

method. Which method is typically used in practice? Why?

1.#