64. Patti Company owns 80% of the common stock of Shannon, Inc. In the

current year, Patti reports sales of $10,000,000 and cost of goods sold of

$7,500,000. For the same period, Shannon has sales of $200,000 and cost of

goods sold of $160,000. During the year, Patti sold merchandise to Shannon for

$60,000 at a price based on the normal markup. At the end of the year, Shannon

still possesses 30 percent of this inventory.

Assume the same information, except Shannon sold inventory to Patti. Compute

consolidated sales.

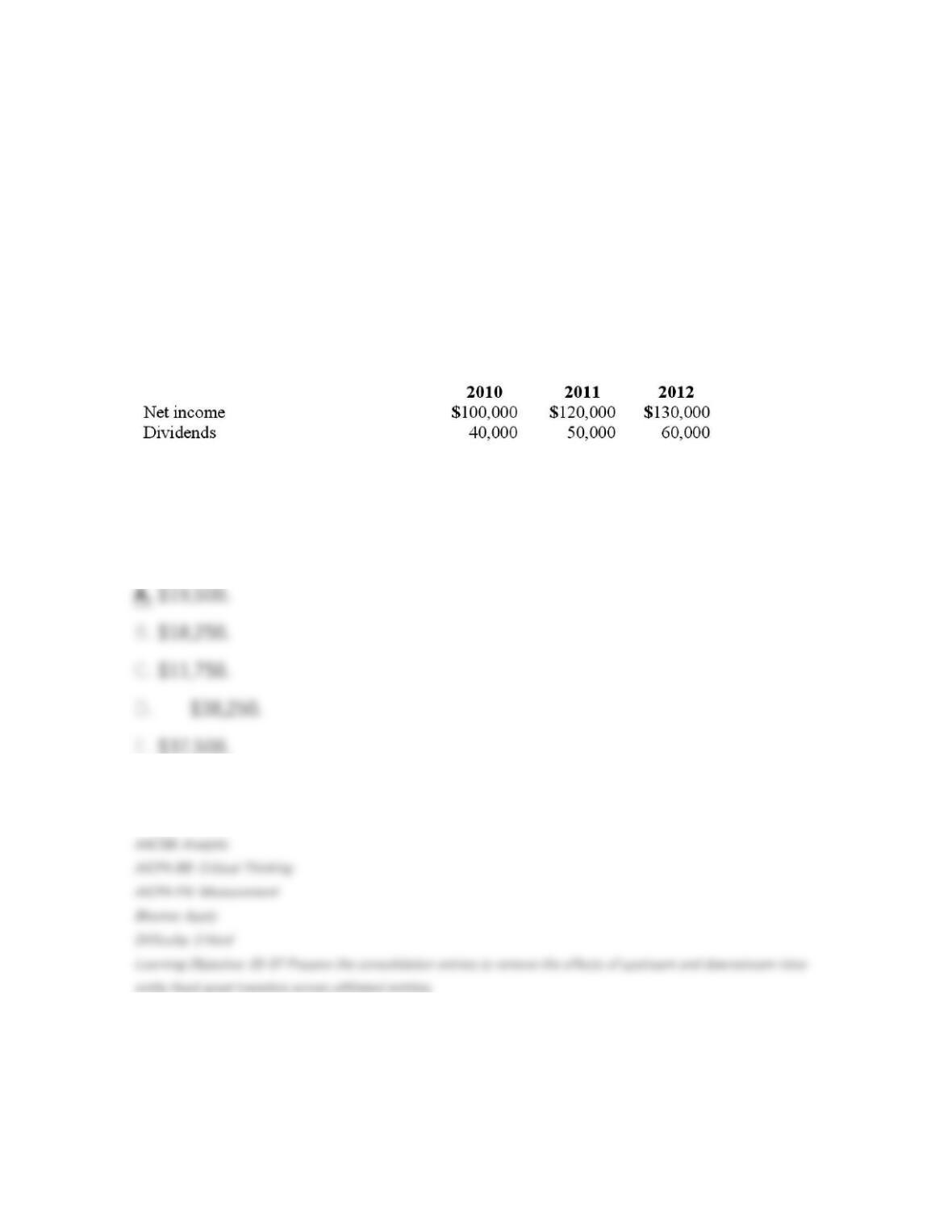

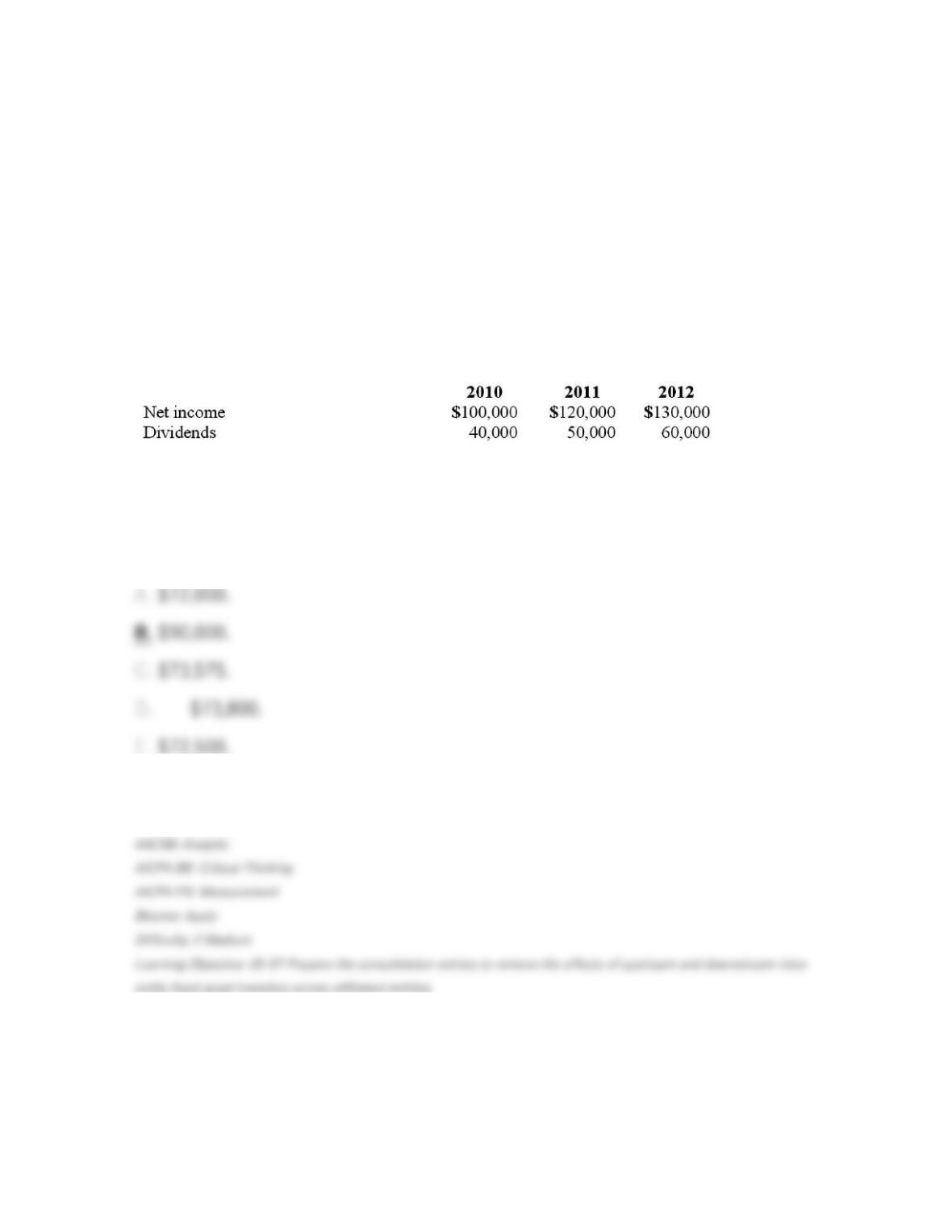

65. Wilson owned equipment with an estimated life of 10 years when it was

acquired for an original cost of $80,000. The equipment had a book value of

$50,000 at January 1, 2010. On January 1, 2010, Wilson realized that the useful life

of the equipment was longer than originally anticipated, at ten remaining years.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company,

bought the equipment from Wilson for $68,250 and for depreciation purposes

used the estimated remaining life as of that date. The following data are available

pertaining to Simon’s income and dividends:

Compute the gain on transfer of equipment reported by Wilson for 2010.

66. Wilson owned equipment with an estimated life of 10 years when it was

acquired for an original cost of $80,000. The equipment had a book value of

$50,000 at January 1, 2010. On January 1, 2010, Wilson realized that the useful life

of the equipment was longer than originally anticipated, at ten remaining years.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company,

bought the equipment from Wilson for $68,250 and for depreciation purposes

used the estimated remaining life as of that date. The following data are available

pertaining to Simon’s income and dividends:

Compute the amortization of gain through a depreciation adjustment for 2010 for

consolidation purposes.

67. Wilson owned equipment with an estimated life of 10 years when it was

acquired for an original cost of $80,000. The equipment had a book value of

$50,000 at January 1, 2010. On January 1, 2010, Wilson realized that the useful life

of the equipment was longer than originally anticipated, at ten remaining years.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company,

bought the equipment from Wilson for $68,250 and for depreciation purposes

used the estimated remaining life as of that date. The following data are available

pertaining to Simon’s income and dividends:

Compute the amortization of gain through a depreciation adjustment for 2011 for

consolidation purposes.

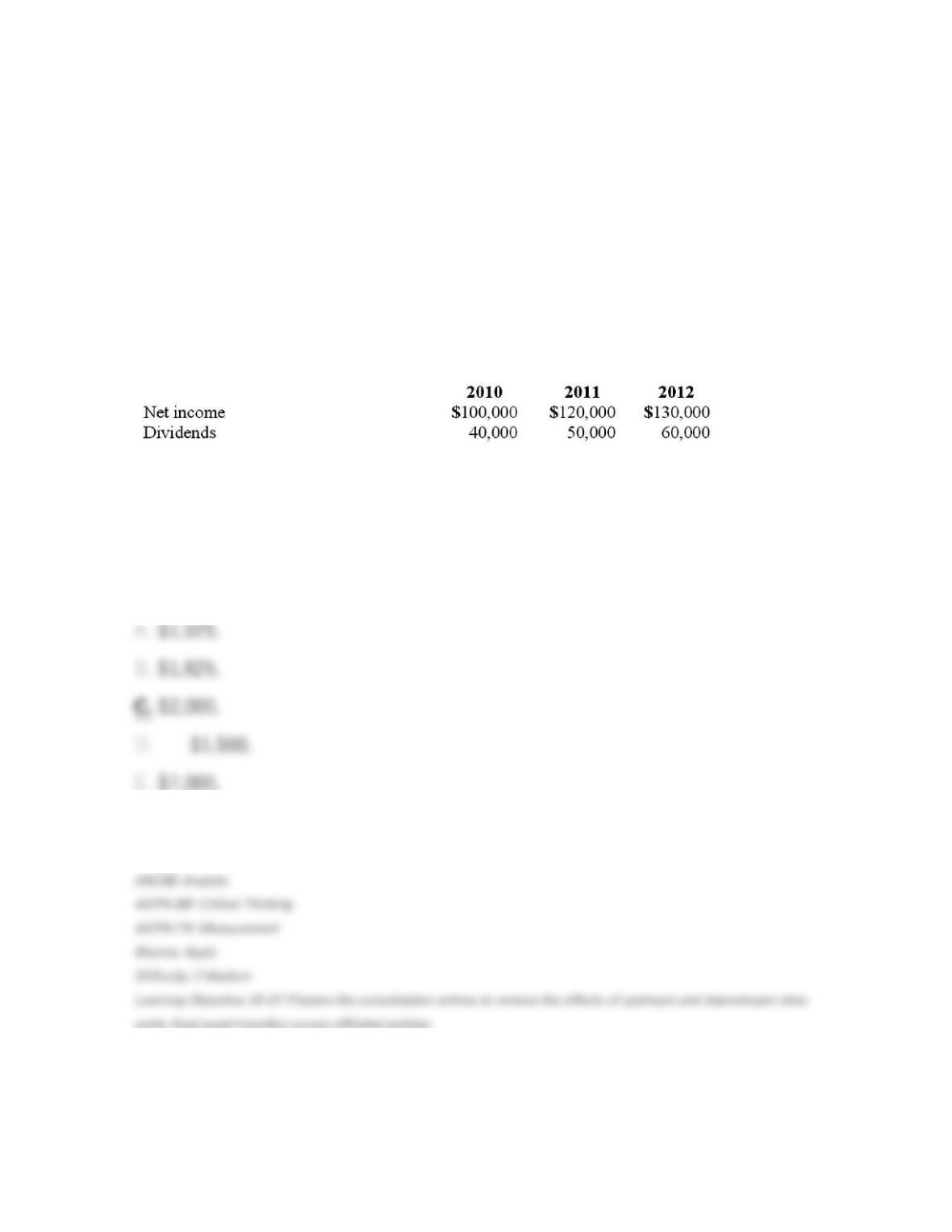

68. Wilson owned equipment with an estimated life of 10 years when it was

acquired for an original cost of $80,000. The equipment had a book value of

$50,000 at January 1, 2010. On January 1, 2010, Wilson realized that the useful life

of the equipment was longer than originally anticipated, at ten remaining years.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company,

bought the equipment from Wilson for $68,250 and for depreciation purposes

used the estimated remaining life as of that date. The following data are available

pertaining to Simon’s income and dividends:

Compute the amortization of gain through a depreciation adjustment for 2012 for

consolidation purposes.

69. Wilson owned equipment with an estimated life of 10 years when it was

acquired for an original cost of $80,000. The equipment had a book value of

$50,000 at January 1, 2010. On January 1, 2010, Wilson realized that the useful life

of the equipment was longer than originally anticipated, at ten remaining years.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company,

bought the equipment from Wilson for $68,250 and for depreciation purposes

used the estimated remaining life as of that date. The following data are available

pertaining to Simon’s income and dividends:

Compute Wilson’s share of income from Simon for consolidation for 2010.

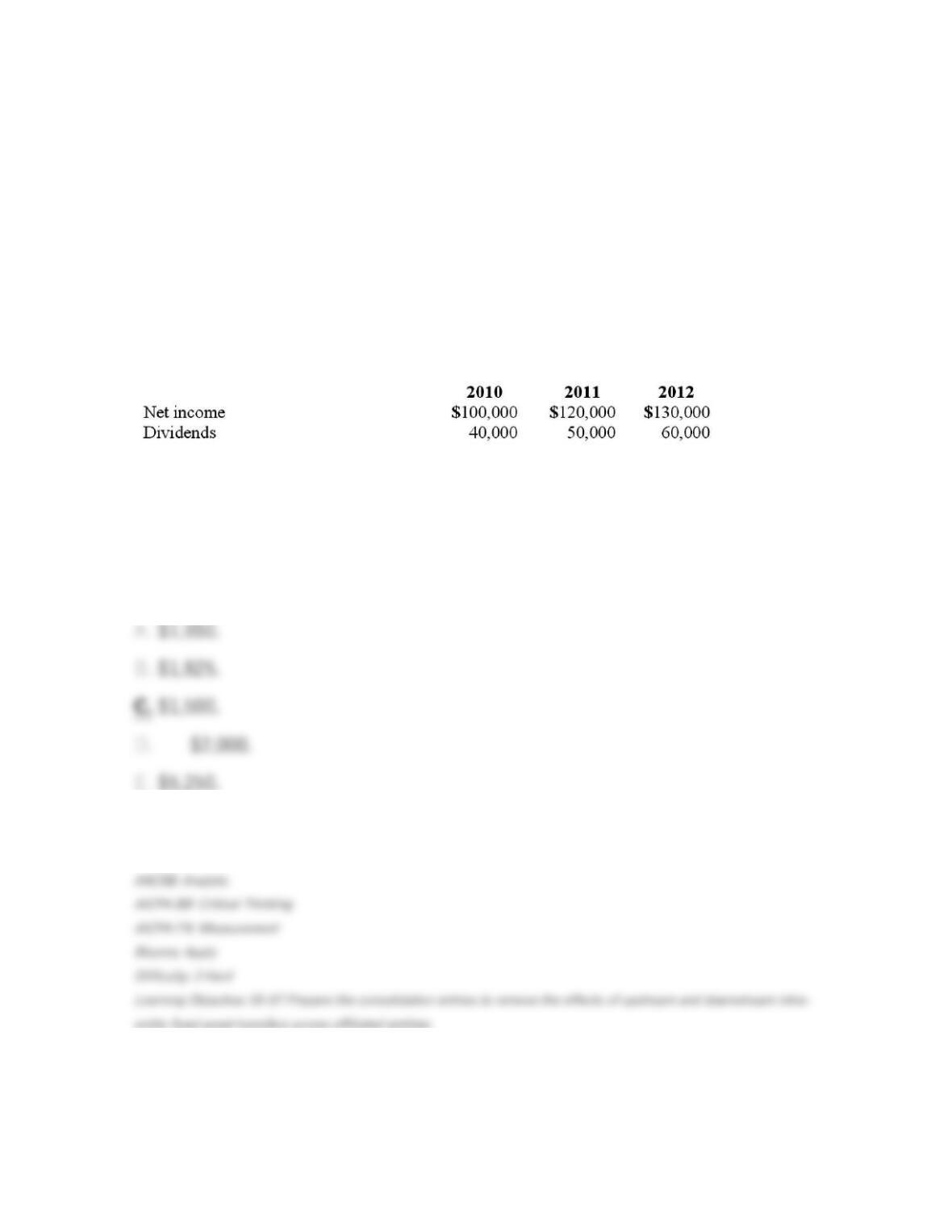

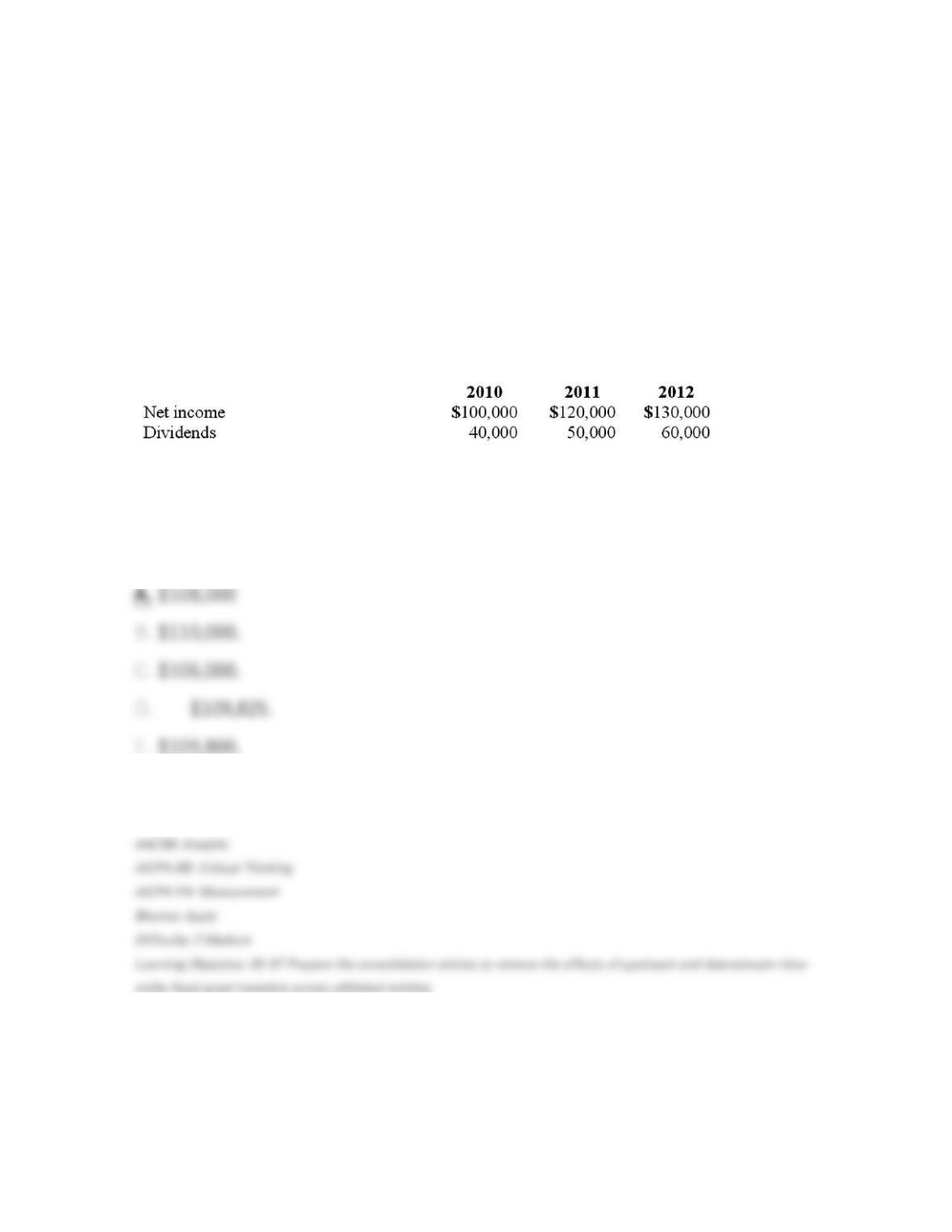

70. Wilson owned equipment with an estimated life of 10 years when it was

acquired for an original cost of $80,000. The equipment had a book value of

$50,000 at January 1, 2010. On January 1, 2010, Wilson realized that the useful life

of the equipment was longer than originally anticipated, at ten remaining years.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company,

bought the equipment from Wilson for $68,250 and for depreciation purposes

used the estimated remaining life as of that date. The following data are available

pertaining to Simon’s income and dividends:

Compute Wilson’s share of income from Simon for consolidation for 2011.

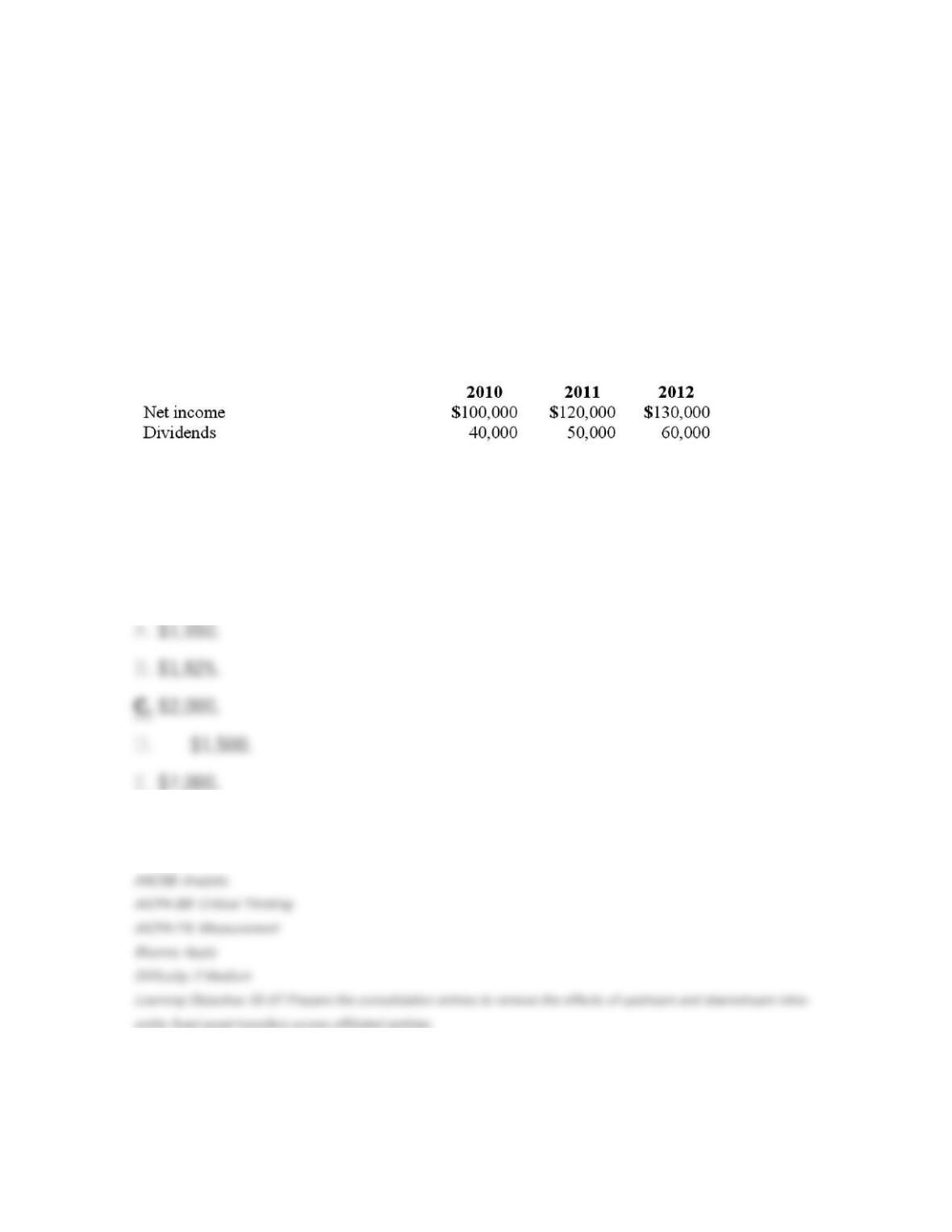

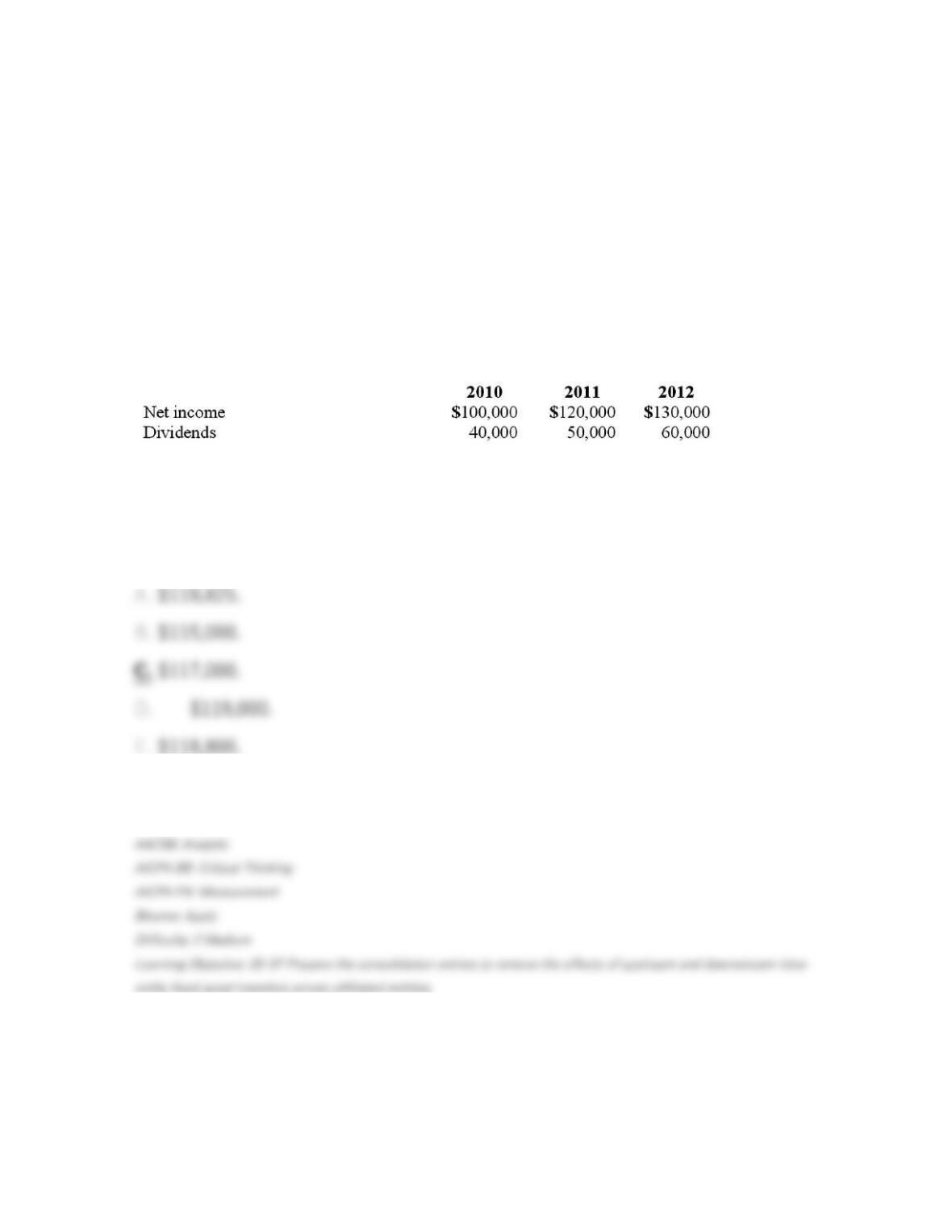

71. Wilson owned equipment with an estimated life of 10 years when it was

acquired for an original cost of $80,000. The equipment had a book value of

$50,000 at January 1, 2010. On January 1, 2010, Wilson realized that the useful life

of the equipment was longer than originally anticipated, at ten remaining years.

On April 1, 2010 Simon Company, a 90% owned subsidiary of Wilson Company,

bought the equipment from Wilson for $68,250 and for depreciation purposes

used the estimated remaining life as of that date. The following data are available

pertaining to Simon’s income and dividends:

Compute Wilson’s share of income from Simon for consolidation for 2012.

72. On January 1, 2010, Smeder Company, an 80% owned subsidiary of Collins,

Inc., transferred equipment with a 10-year life (six of which remain with no

salvage value) to Collins in exchange for $84,000 cash. At the date of transfer,

Smeder’s records carried the equipment at a cost of $120,000 less accumulated

depreciation of $48,000. Straight-line depreciation is used. Smeder reported net

income of $28,000 and $32,000 for 2010 and 2011, respectively. All net income

effects of the intra-entity transfer are attributed to the seller for consolidation

purposes.

Compute the gain recognized by Smeder Company relating to the equipment for

2010.

73. On January 1, 2010, Smeder Company, an 80% owned subsidiary of Collins,

Inc., transferred equipment with a 10-year life (six of which remain with no

salvage value) to Collins in exchange for $84,000 cash. At the date of transfer,

Smeder’s records carried the equipment at a cost of $120,000 less accumulated

depreciation of $48,000. Straight-line depreciation is used. Smeder reported net

income of $28,000 and $32,000 for 2010 and 2011, respectively. All net income

effects of the intra-entity transfer are attributed to the seller for consolidation

purposes.

Compute Collins’ share of Smeder’s net income for 2010.

74. On January 1, 2010, Smeder Company, an 80% owned subsidiary of Collins,

Inc., transferred equipment with a 10-year life (six of which remain with no

salvage value) to Collins in exchange for $84,000 cash. At the date of transfer,

Smeder’s records carried the equipment at a cost of $120,000 less accumulated

depreciation of $48,000. Straight-line depreciation is used. Smeder reported net

income of $28,000 and $32,000 for 2010 and 2011, respectively. All net income

effects of the intra-entity transfer are attributed to the seller for consolidation

purposes.

Compute Collins’ share of Smeder’s net income for 2011.

75. On January 1, 2010, Smeder Company, an 80% owned subsidiary of Collins,

Inc., transferred equipment with a 10-year life (six of which remain with no

salvage value) to Collins in exchange for $84,000 cash. At the date of transfer,

Smeder’s records carried the equipment at a cost of $120,000 less accumulated

depreciation of $48,000. Straight-line depreciation is used. Smeder reported net

income of $28,000 and $32,000 for 2010 and 2011, respectively. All net income

effects of the intra-entity transfer are attributed to the seller for consolidation

purposes.

For consolidation purposes, what net debit or credit will be made for the year

2010 relating to the accumulated depreciation for the equipment transfer?

76. On January 1, 2010, Smeder Company, an 80% owned subsidiary of Collins,

Inc., transferred equipment with a 10-year life (six of which remain with no

salvage value) to Collins in exchange for $84,000 cash. At the date of transfer,

Smeder’s records carried the equipment at a cost of $120,000 less accumulated

depreciation of $48,000. Straight-line depreciation is used. Smeder reported net

income of $28,000 and $32,000 for 2010 and 2011, respectively. All net income

effects of the intra-entity transfer are attributed to the seller for consolidation

purposes.

What is the net effect on consolidated net income in 2010 due to the equipment

transfer?

77. Stiller Company, an 80% owned subsidiary of Leo Company, purchased

land from Leo on March 1, 2010, for $75,000. The land originally cost Leo $60,000.

Stiller reported net income of $125,000 and $140,000 for 2010 and 2011,

respectively. Leo uses the equity method to account for its investment.

Compute the gain or loss on the intra-entity sale of land.

78. Stiller Company, an 80% owned subsidiary of Leo Company, purchased

land from Leo on March 1, 2010, for $75,000. The land originally cost Leo $60,000.

Stiller reported net income of $125,000 and $140,000 for 2010 and 2011,

respectively. Leo uses the equity method to account for its investment.

On a consolidation worksheet, what adjustment would be made for 2010

regarding the land transfer?

79. Stiller Company, an 80% owned subsidiary of Leo Company, purchased

land from Leo on March 1, 2010, for $75,000. The land originally cost Leo $60,000.

Stiller reported net income of $125,000 and $140,000 for 2010 and 2011,

respectively. Leo uses the equity method to account for its investment.

On a consolidation worksheet, having used the equity method, what adjustment

would be made for 2011 regarding the land transfer?

80. Stiller Company, an 80% owned subsidiary of Leo Company, purchased

land from Leo on March 1, 2010, for $75,000. The land originally cost Leo $60,000.

Stiller reported net income of $125,000 and $140,000 for 2010 and 2011,

respectively. Leo uses the equity method to account for its investment.

Compute income from Stiller on Leo’s books for 2010.

81. Stiller Company, an 80% owned subsidiary of Leo Company, purchased

land from Leo on March 1, 2010, for $75,000. The land originally cost Leo $60,000.

Stiller reported net income of $125,000 and $140,000 for 2010 and 2011,

respectively. Leo uses the equity method to account for its investment.

Compute income from Stiller on Leo’s books for 2011.

82. Stark Company, a 90% owned subsidiary of Parker, Inc., sold land to Parker

on May 1, 2010, for $80,000. The land originally cost Stark $85,000. Stark reported

net income of $200,000, $180,000, and $220,000 for 2010, 2011, and 2012,

respectively. Parker sold the land purchased from Stark in 2010 for $92,000 in

2012.

Compute the gain or loss on the intra-entity sale of land.

83. Stark Company, a 90% owned subsidiary of Parker, Inc., sold land to Parker

on May 1, 2010, for $80,000. The land originally cost Stark $85,000. Stark reported

net income of $200,000, $180,000, and $220,000 for 2010, 2011, and 2012,

respectively. Parker sold the land purchased from Stark in 2010 for $92,000 in

2012.

Which of the following will be included in a consolidation entry for 2010?