1. If predetermined overhead rates are based on budgeted activity and overhead includes

significant fixed costs, then the unit product costs will fluctuate depending on the budgeted level

of activity for the period.

2. When the fixed costs of capacity are spread over the level of activity at capacity rather

than the estimated activity for the period, the units that are produced must shoulder the costs of

unused capacity.

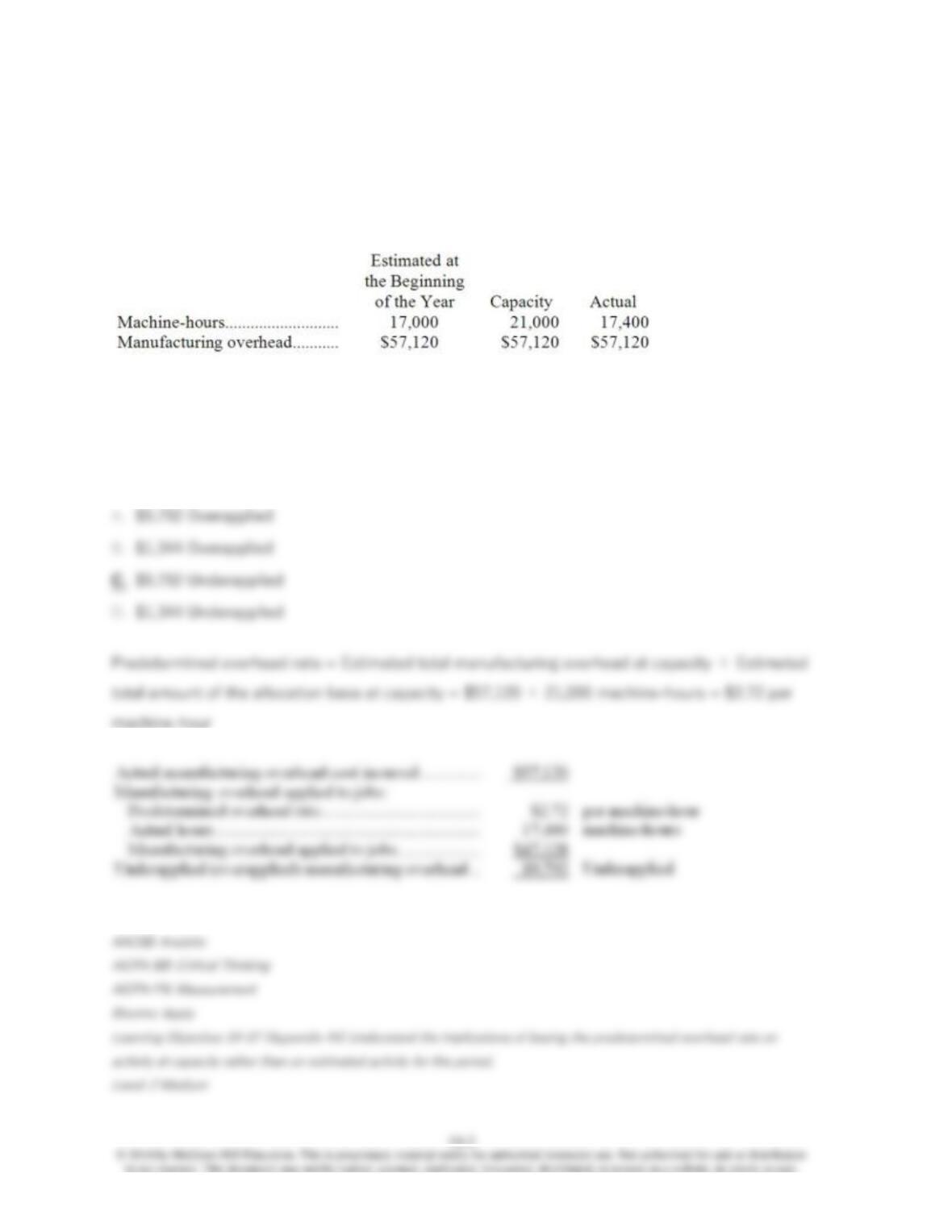

3. The management of Chaloux Corporation would like to investigate the possibility of

basing its predetermined overhead rate on activity at capacity. The company’s controller has

provided an example to illustrate how this new system would work. In this example, the allocation

base is machine-hours.

If the company bases its predetermined overhead rate on capacity, by how much was

manufacturing overhead underapplied or overapplied?

4. The management of Griswell Corporation would like to investigate the possibility of

basing its predetermined overhead rate on activity at capacity. The company’s controller has

provided an example to illustrate how this new system would work. In this example, the allocation

base is machine-hours and the estimated amount of the allocation base for the upcoming year is

39,000 machine-hours. In addition, capacity is 45,000 machine-hours and the actual level of

activity for the year is 40,200 machine-hours. All of the manufacturing overhead is fixed and is

$702,000 per year. For simplicity, it is assumed that this is the estimated manufacturing overhead

for the year as well as the manufacturing overhead at capacity. It is further assumed that this is

also the actual amount of manufacturing overhead for the year. If the company bases its

predetermined overhead rate on capacity, by how much was manufacturing overhead

underapplied or overapplied?

The management of Keeter Corporation would like to investigate the possibility of basing

its predetermined overhead rate on activity at capacity. The company’s controller has provided an

example to illustrate how this new system would work. In this example, the allocation base is

machine-hours and the estimated amount of the allocation base for the upcoming year is 89,000

machine-hours. In addition, capacity is 96,000 machine-hours and the actual level of activity for

the year is 88,600 machine-hours. All of the manufacturing overhead is fixed and is $7,176,960

per year. For simplicity, it is assumed that this is the estimated manufacturing overhead for the

year as well as the manufacturing overhead at capacity. It is further assumed that this is also the

actual amount of manufacturing overhead for the year.

5. If the company bases its predetermined overhead rate on the estimated amount of the

allocation base for the upcoming year, the predetermined overhead rate is closest to:

6. If the company bases its predetermined overhead rate on the estimated amount of the

allocation base for the upcoming year, by how much was manufacturing overhead underapplied

or overapplied?

7. If the company bases its predetermined overhead rate on capacity, the predetermined

overhead rate is closest to:

4A-7

8. If the company bases its predetermined overhead rate on capacity, by how much was

manufacturing overhead underapplied or overapplied?

The management of Daguio Corporation would like to investigate the possibility of basing

its predetermined overhead rate on activity at capacity. The company’s controller has provided an

example to illustrate how this new system would work. In this example, the allocation base is

machine-hours and the estimated amount of the allocation base for the upcoming year is 54,000

machine-hours. In addition, capacity is 63,000 machine-hours and the actual level of activity for

the year is 53,000 machine-hours. All of the manufacturing overhead is fixed and is $1,871,100

per year. For simplicity, it is assumed that this is the estimated manufacturing overhead for the

year as well as the manufacturing overhead at capacity. It is further assumed that this is also the

actual amount of manufacturing overhead for the year.

9. If the company bases its predetermined overhead rate on capacity, the predetermined

overhead rate is closest to:

4A-9

10. If the company bases its predetermined overhead rate on capacity, by how much was

manufacturing overhead underapplied or overapplied?

The management of Foy Corporation would like to investigate the possibility of basing its

predetermined overhead rate on activity at capacity. The company’s controller has provided an

example to illustrate how this new system would work. In this example, the allocation base is

machine-hours and the estimated amount of the allocation base for the upcoming year is 86,000

machine-hours. In addition, capacity is 94,000 machine-hours and the actual level of activity for

the year is 88,200 machine-hours. All of the manufacturing overhead is fixed and is $6,790,560

per year. For simplicity, it is assumed that this is the estimated manufacturing overhead for the

year as well as the manufacturing overhead at capacity. It is further assumed that this is also the

actual amount of manufacturing overhead for the year.

11. If the company bases its predetermined overhead rate on the estimated amount of the

allocation base for the upcoming year, by how much was manufacturing overhead underapplied

or overapplied?

12. If the company bases its predetermined overhead rate on capacity, by how much was

manufacturing overhead underapplied or overapplied?

The management of Bellon Corporation would like to investigate the possibility of basing

its predetermined overhead rate on activity at capacity. The company’s controller has provided an

example to illustrate how this new system would work. In this example, the allocation base is

machine-hours and the estimated amount of the allocation base for the upcoming year is 23,000

machine-hours. In addition, capacity is 27,000 machine-hours and the actual level of activity for

the year is 23,300 machine-hours. All of the manufacturing overhead is fixed and is $142,830 per

year. For simplicity, it is assumed that this is the estimated manufacturing overhead for the year

as well as the manufacturing overhead at capacity. It is further assumed that this is also the

actual amount of manufacturing overhead for the year. A number of jobs were worked on during

the year, one of which was Job P50E. This job required 160 machine-hours.

13. If the company bases its predetermined overhead rate on the estimated amount of the

allocation base for the upcoming year, the predetermined overhead rate is closest to:

14. If the company bases its predetermined overhead rate on the estimated amount of the

allocation base for the upcoming year the amount of manufacturing overhead charged to the Job

P50E is closest to:

15. If the company bases its predetermined overhead rate on the estimated amount of the

allocation base for the upcoming year, by how much was manufacturing overhead underapplied

or overapplied?

16. If the company bases its predetermined overhead rate on capacity, the predetermined

overhead rate is closest to: