Chapter 4: Accounting for Merchandising Businesses

101. Sales to customers who use bank credit cards such as MasterCard and Visa are usually

recorded by a(n):

a. decrease in Bank Credit Card Sales, increase in Credit Card Expense, and increase in Sales.

b. increase in Cash, increase in Credit Card Expense, and increase in Sales.

c. increase in Cash, decrease in Credit Card Expense, and increase in Sales.

d. decrease in Sales, increase in Credit Card Expense, and decrease in Cash.

102. In recording the cost of merchandise sold for cash using a perpetual inventory system, the

effect on the accounts is:

a. increase Cost of Merchandise Sold; increase Cash.

b. increase Cost of Merchandise Sold; decrease Merchandise Inventory.

c. increase Merchandise Inventory; decrease Cost of Merchandise Sold.

d. increase Accounts Receivable; decrease Merchandise Inventory.

103. When merchandise that was sold on account is returned, which accounts are affected?

a. Cash, accounts receivable, cost of goods sold, and sales returns

b. Sales returns, accounts receivable, merchandise inventory, and cost of goods sold

c. Sales returns, accounts receivable, purchases, and cost of goods sold

d. Sales returns, accounts receivable, purchases, and merchandise inventory

104. For the perpetual inventory system, which of the following effects does not occur upon the

return from a customer of merchandise sold on account?

a. Increases Sales Returns and Allowances and decreases Accounts Receivable

b. Decreases Cost of Merchandise Sold and increases Merchandise Inventory

c. Increases Purchase Returns and Allowances and decreases Merchandise Inventory

d. All of these occur.

105. If merchandise sold on account is returned to the seller, the seller may inform the customer of

the details by issuing a:

a. sales invoice.

b. purchase invoice.

c. credit memorandum.

d. debit memorandum.

Chapter 4: Accounting for Merchandising Businesses

106. Merchandise subject to terms 2/10, n/30, FOB shipping point, is sold on account to a customer

for $35,000. The seller issued a credit memorandum for $8,000 prior to payment. What is the

amount of the cash discount allowable?

a. $700

b. $540

c. $860

d. $350

107. Orange Co. sells merchandise on credit to Zea Co. in the amount of $9,000. The invoice is

dated on September 15 with terms of 1/15, net 45. What is the amount of the discount, and up

to what date must the invoice be paid in order for the buyer to take advantage of the discount?

a. $180, September 30

b. $180, September 25

c. $90, September 30

d. $90, September 25

108. Based on the following information, what would be recorded as purchases discount if the

invoice is paid within the discount period?

1. $5,000 of merchandise inventory was ordered on April 2, 2015.

2. $2,000 of this merchandise was received on April 5, 2015.

3. On April 6, 2015, an invoice dated April 4, 2015, with terms of 2/10, net 30 for $2,150

which included a $150 prepaid freight cost, was received.

4. On April 10, 2015, $500 of the merchandise was returned to the seller.

a. $100

b. $30

c. $43

d. $33

109. In credit terms of 1/10, n/30, the “10” represents the:

a. number of days in the discount period.

b. full amount of the invoice.

c. number of days when the entire amount is due.

d. percent of the cash discount.

Chapter 4: Accounting for Merchandising Businesses

110. When purchases of merchandise are made for cash, under the perpetual inventory system, the

transaction:

a. increases Cash; decreases Merchandise Inventory.

b. increases Merchandise Inventory; decreases Cash.

c. increases Merchandise Inventory; decreases Cash Discounts.

d. increases Merchandise Inventory; decreases Purchases.

111. When merchandise is purchased to resell to customers, it is recorded in the account entitled:

a. Supplies.

b. Cost of Goods Sold.

c. Merchandise Inventory.

d. Sales.

112. Using a perpetual inventory system, the purchase of $30,000 of merchandise on account would

include a(n):

a. increase in Sales.

b. increase in Merchandise Inventory.

c. decrease in Merchandise Inventory.

d. decrease in Sales.

113. Using a perpetual inventory system, the return of merchandise purchased on account includes

a(n):

a. increase in Sales.

b. increase in Merchandise Inventory.

c. decrease in Merchandise Inventory.

d. decrease in Sales.

114. The amount of the total cash paid to the seller for merchandise purchased would normally

include:

a. only the list price.

b. only the sales tax.

c. the list price plus the sales tax.

d. the list price less the sales tax.

Chapter 4: Accounting for Merchandising Businesses

115. A sales invoice included the following information: merchandise price, $8,000; terms 2/10,

n/eom. Assuming that a credit for merchandise returned of $1,000 is granted prior to payment,

and that the invoice is paid within the discount period, what is the amount of cash received by

the seller?

a. $6,840

b. $7,000

c. $6,860

d. $7,840

116. A sales invoice included the following information: merchandise price, $6,000; terms 2/10,

n/eom. Assuming that a credit for merchandise returned of $600 is granted prior to payment,

and that the invoice is paid within the discount period, what is the amount of cash received by

the seller?

a. $5,880

b. $5,292

c. $5,586

d. $5,592

117. Merchandise subject to terms 1/10, n/30, FOB shipping point, is sold on account to a customer

for $17,500. The seller issued a credit memorandum for $4,000 prior to payment. What is the

amount of the cash discount allowable?

a. $215

b. $175

c. $135

d. $140

118. If the buyer is to pay the delivery expense of delivering merchandise, delivery terms are stated

as:

a. FOB shipping point.

b. FOB destination.

c. FOB n/30.

d. FOB buyer.

119. If the seller is to pay the delivery expense of delivering merchandise, the delivery terms are

stated as:

a. FOB shipping point.

b. FOB destination.

c. FOB n/30.

d. FOB seller.

Chapter 4: Accounting for Merchandising Businesses

120. If title to merchandise purchases passes to the buyer when the goods are shipped from the

seller, the terms are:

a. n/30.

b. FOB shipping point.

c. FOB destination.

d. consigned.

121. If title to merchandise purchases passes to the buyer when the goods are delivered to the

buyer, the terms are:

a. consigned.

b. b. n/30.

c. FOB shipping point.

d. FOB destination.

122. Merchandise with an invoice price of $10,000 is purchased subject to terms of 2/10, n/30, FOB

destination. Transportation costs paid by the seller totaled $300. What is the net cost of the

merchandise?

a. $10,300

b. $10,100

c. $9,800

d. $9,506

123. Which term indicates that merchandise is free of transportation charges to the buyer?

a. FOB destination

b. Transportation out

c. FOB shipping point

d. Transportation in

124. Inventory shortage is recorded when:

a. merchandise is returned by a buyer.

b. merchandise purchased from a seller is incomplete or short.

c. merchandise is returned to a seller.

d. there is a difference between a physical count of inventory and inventory records.

Chapter 4: Accounting for Merchandising Businesses

125. By dividing gross profit by cost of merchandise sold we arrive at:

a. gross profit percent.

b. average markup percent.

c. ratio of sales to assets.

d. sales percent.

126. Ratio of sales to assets is calculated by:

a. dividing average total assets by net sales.

b. dividing net sales by total current assets.

c. dividing net sales by average total assets.

d. dividing total current assets by net sales.

127. If sales is $50,000 and cost of merchandise sold is $35,000, how much would be the markup

percent?

a. 30.0%

b. 70.0%

c. 42.9%

d. 14.3%

128. If net sales is $100,000, total assets at the beginning of the year is $45,000, and total assets at

end of the end of the year is $55,000, how much would be the ratio of sales to assets?

a. 1.0

b. 1.8

c. 2.2

d. 2.0

129. Cash paid to purchase long-term investments would be reported in the statement of cash flows

in:

a. the cash flows from operating activities section.

b. the cash flows from financing activities section.

c. the cash flows from investing activities section.

d. a separate schedule.

Chapter 4: Accounting for Merchandising Businesses

130. Which of the following should be shown on a statement of cash flows under the financing

activity section?

a. The purchase of a long-term investment in the common stock of another company

b. The payment of cash to retire a long-term note

c. The proceeds from the sale of a building

d. The issuance of a long-term note to acquire land

131. Under the indirect method for preparing the statement of cash flows, increases in current

liabilities are the net income in the cash flows from operating activities section.

a. subtracted from

b. added to

c. not used when calculating

d. equal to

132. Which of the following would not affect the operating activities section of the statement of

cash flows, using the indirect method?

a. Decrease in merchandise inventory

b. Payment on a note payable

c. Decrease in unearned rent

d. Depreciation expense

133. A company has a net income of $70,000 and depreciation expenses of $20,000. During the

year, its accounts payable balance decreased by $15,000. What is the net cash flow from

operating activities using the indirect method for preparing the statement of cash flows?

a. $90,000

b. $105,000

c. $50,000

d. $75,000

134. Under the indirect method for preparing the statement of cash flows, decreases in current

assets are net income in the cash flows from operating activities section.

a. subtracted from

b. added to

c. not used in calculating

d. cannot tell from the information given

Chapter 4: Accounting for Merchandising Businesses

135. A payment of dividends decreases which section on the statement of cash flows?

a. Operating activities

b. Investing activities

c. Financing activities

d. None of these

136. ONI, Inc. purchased $60,000 of equipment for cash. How does this transaction impact the

statement of cash flows?

a. Decreases the cash flow from operating activities by $60,000

b. Decreases equipment by $60,000

c. Decreases the cash flow from investing activities section by $60,000

d. This transaction would not affect the statement of cash flows.

137. Investing activities include:

a. collecting cash on loans made.

b. obtaining cash from creditors.

c. obtaining capital from owners.

d. repaying money previously borrowed.

138. The following data for the year ended June 30, 2016, were extracted from the accounting

records of Roof Co.:

Cost of merchandise sold

$300,000

Operating expenses

95,000

Sales

450,000

Prepare a multiple-step income statement for the current year ended June 30, 2016.

Gross profit

Chapter 4: Accounting for Merchandising Businesses

139. The following data for the current year ended December 31, 2016, were extracted from the

accounting records of Gilbert Co.:

Cost of merchandise sold

$710,000

Operating expenses

250,000

Sales

925,000

Prepare a multiple-step income statement for the year ended December 31, 2016.

Gross profit

140. Prepare a multiple-step income statement for Surry Co. from the following data for the year

ended December 31, 2016.

Sales, $915,000; cost of merchandise sold, $670,000; administrative expenses, $30,000;

interest expense, $12,000; rent revenue, $19,000; sales returns and allowances, $55,000;

selling expenses, $120,000.

Cost of merchandise sold

Operating expenses:

Income from operations

Chapter 4: Accounting for Merchandising Businesses

141. Selected data from the ledger of Jones Co. after adjustment at June 30, the end of the fiscal

year, are listed as follows:

Accounts Receivable

$ 25,000

Prepaid Insurance

$ 2,250

Accumulated Depreciation

35,200

Notes Payable

60,150

Administrative Expenses

80,000

Retained Earnings

55,000

Capital Stock

40,000

Salaries Payable

3,000

Cost of Merchandise Sold

320,000

Sales (net)

550,000

Dividends

22,000

Selling Expenses

65,000

Interest Revenue

3,000

Supplies

2,750

Office Equipment

70,500

Prepare a single-step income statement for the year ended June 30, 2016.

Interest revenue

Selling expenses

Chapter 4: Accounting for Merchandising Businesses

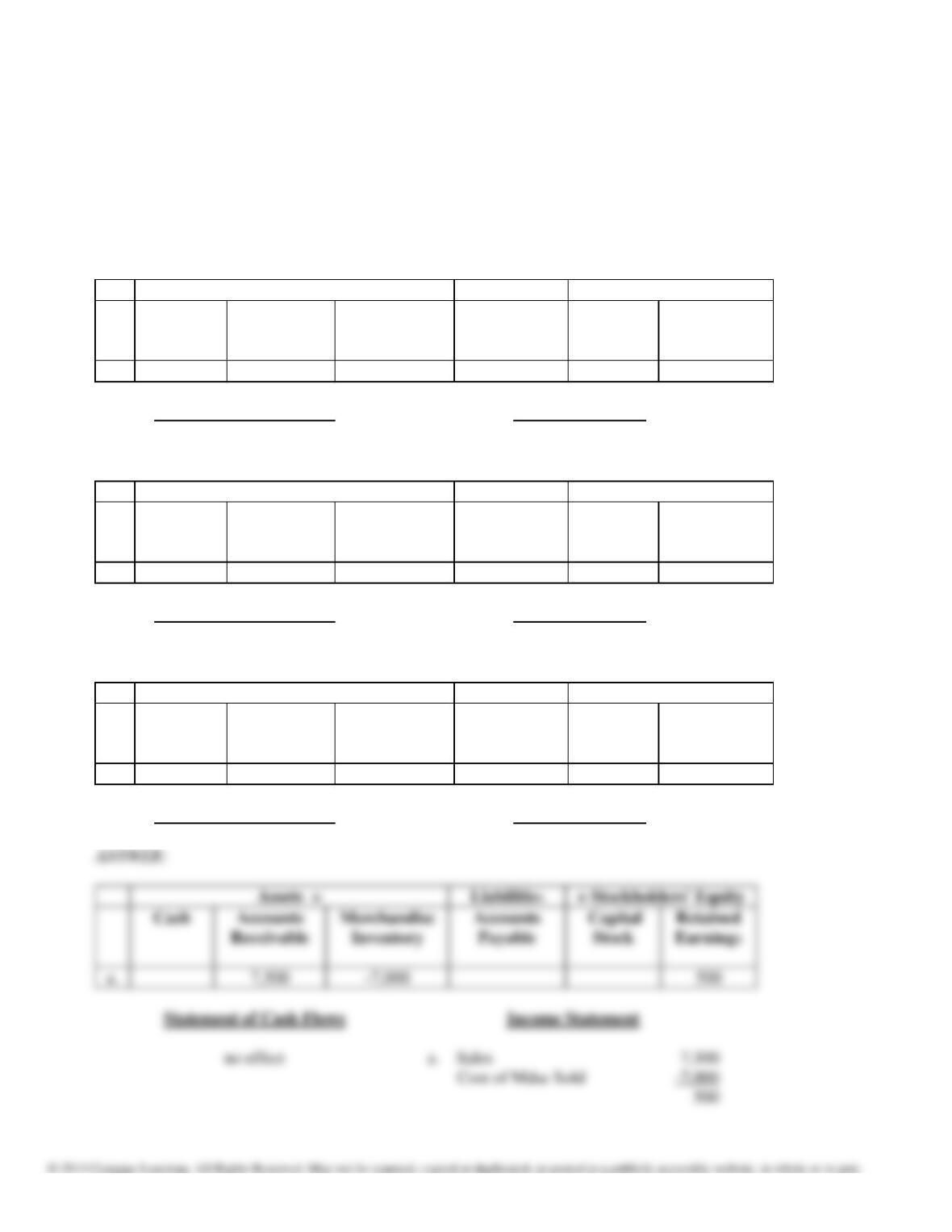

142. Merchandise with a list price of $7,500 and a cost of $7,000 is sold on account, terms 1/10,

n/30. Prior to payment, merchandise with a list price of $1,000 and a cost of $800 is returned.

The correct amount is paid within the discount period.

Record the following transactions, using the integrated financial statement framework that

follows:

(a) Sold the merchandise.

(b) Received the returned merchandise

(c) Received the amount owed.

Assets =

Liabilities

+ Stockholders’ Equity

Cash

Accounts

Receivable

Merchandise

Inventory

Accounts

Payable

Capital

Stock

Retained

Earnings

a.

Statement of Cash Flows

Income Statement

Assets =

Liabilities

+ Stockholders’ Equity

Cash

Accounts

Receivable

Merchandise

Inventory

Accounts

Payable

Capital

Stock

Retained

Earnings

b.

Statement of Cash Flows

Income Statement

Assets =

Liabilities

+ Stockholders’ Equity

Cash

Accounts

Receivable

Merchandise

Inventory

Accounts

Payable

Capital

Stock

Retained

Earnings

c.

Statement of Cash Flows

Income Statement

Assets =

Cash

Accounts

Cost of Mdse Sold

Chapter 4: Accounting for Merchandising Businesses

800

-6,500

143. Details of invoices for purchases of merchandise are as follows:

Merchandise

Transportation

Terms

Returns and

Allowances

a. $1,000

$25

FOB shipping point, 1/10, n/30

$200

b. 5,000

—

FOB destination, n/30

400

c. 4,000

50

FOB shipping point, 2/10, n/30

150

d. 5,000

—

FOB destination, 1/10, n/30

—

Determine the amount to be paid in full settlement of each of the invoices, assuming that credit

for returns and allowances was received prior to payment and that all invoices were paid

within the discount period. Also assume that the seller has prepaid the transportation expenses.

Chapter 4: Accounting for Merchandising Businesses

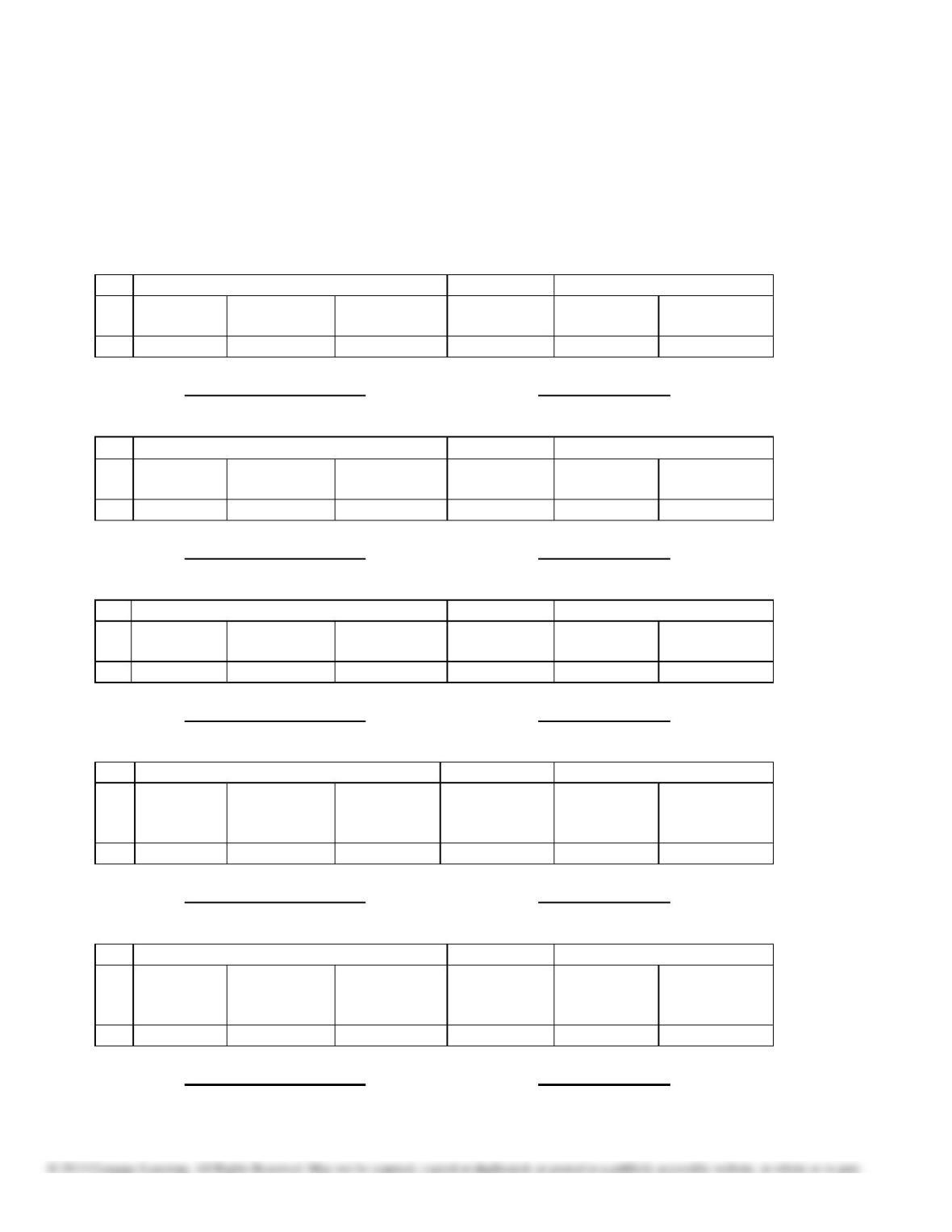

144. Based on the information below, illustrate the effects on the accounts and financial statements

of the Seller and the Buyer. Both use a perpetual inventory system.

(a)

Seller sells Buyer on account merchandise costing $300 for $500, terms 2/10, net 30, FOB

destination. The transportation charge is $50.

(b)

Buyer returns as defective $100 worth of the $500 merchandise received. The seller’s cost

is $60.

(c)

Buyer pays within the discount period.

(a) Seller

Assets =

Liabilities

+ Stockholders‘ Equity

Cash

Accounts

Receivable

Merchandise

Inventory

Accounts

Payable

Capital

Stock

Retained

Earnings

Statement of Cash Flows

Income Statement

(a) Buyer

Assets =

Liabilities

+ Stockholders‘ Equity

Cash

Accounts

Receivable

Merchandise

Inventory

Accounts

Payable

Capital

Stock

Retained

Earnings

Statement of Cash Flows

Income Statement

(b) Seller

Assets =

Liabilities

+ Stockholders‘ Equity

Cash

Accounts

Receivable

Merchandise

Inventory

Accounts

Payable

Capital

Stock

Retained

Earnings

Statement of Cash Flows

Income Statement

(b) Buyer

Assets =

Liabilities

+ Stockholders‘ Equity

Cash

Accounts

Receivable

Merchandise

Inventory

Accounts

Payable

Capital

Stock

Retained

Earnings

Statement of Cash Flows

Income Statement

(c) Seller

Assets =

Liabilities

+ Stockholders‘ Equity

Cash

Accounts

Receivable

Merchandise

Inventory

Accounts

Payable

Capital

Stock

Retained

Earnings

Statement of Cash Flows

Income Statement

Chapter 4: Accounting for Merchandising Businesses

(c) Buyer

Assets =

Liabilities

+ Stockholders‘ Equity

Cash

Accounts

Receivable

Merchandise

Inventory

Accounts

Payable

Capital

Stock

Retained

Earnings

Statement of Cash Flows

Income Statement

Statement of Cash Flows

Income Statement

+ Stockholders‘ Equity

Statement of Cash Flows

Income Statement

Chapter 4: Accounting for Merchandising Businesses

145. State the section(s) of the statement of cash flows prepared by the indirect method (operating

activities, investing activities, financing activities, or not reported) and the amount that would

be reported for each of the following transactions:

(a) Received $145,000 from the sale of land costing $70,000.

(b) Purchased investments for $50,000.

(c) Declared $35,000 cash dividends on stock. $5,000 dividends were payable at the

beginning of the year, and $6,000 were payable at the end of the year.

(d) Acquired equipment for $32,000 cash.

(e) Declared and issued 100 shares of $20 par common stock as a stock dividend, when the

market price of the stock was $32 a share.

(f) Recognized by an adjusting entry depreciation for the year, $48,000.

(g) Issued 85,000 shares of $10 par common stock for $25 a share, receiving cash.

(h) Issued $500,000 of 20-year, 10% bonds payable at 99.

(i) Borrowed $43,000 from Busey National Bank, issuing a 5-year, 8% note for that

amount.

Chapter 4: Accounting for Merchandising Businesses

Merchandise Inventory, October 1

$ 98,560

Merchandise Inventory, October 31

102,330

Purchases

433,880

Purchases Returns & Allowances

12,760

Purchases Discounts

9,900

Transportation In

7,620

146. Based on the following data, determine the cost of merchandise sold for October.

147. Gold Co. sold merchandise to Bronze Co. on account, $23,000, terms 2/15, net 45. The cost of

the merchandise sold is $18,500. Gold Co. issued a credit memorandum for $2,500 for

merchandise returned that originally cost $1,900. Bronze Co. paid the invoice within the

discount period. What is the amount of net income earned by Gold Co. on the transactions?