Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

103. Tosco Co. paid $540,000 for 80% of the stock of Martz Co. when the book

value of Martz's net assets was $600,000. For all of Martz's assets and liabilities,

book value and fair value were approximately equal.

Required:

Using the acquisition method, what amount of goodwill should appear in a

consolidated balance sheet prepared immediately after the combination?

104. On January 1, 2011, Elva Corp. paid $750,000 for 80% of Fenton Co. when

the book value of Fenton's net assets was $800,000. Fenton owned a building

with a fair value of $150,000 and a book value of $120,000.

Required:

At what amount would the building appear on a consolidated balance sheet

prepared immediately after the combination, under the acquisition method of

accounting for business combinations?

105. Pennant Corp. owns 70% of the common stock of Scarvens Co. Scarvens'

revenues for 2011 totaled $200,000.

Required:

What amount of Scarvens' revenues would be included in the consolidated

revenues under the acquisition method of accounting for business combinations?

106. Caldwell Inc. acquired 65% of Club Corp. for $2,600,000. Club owned a

building and equipment with ten-year useful lives. The book value of these assets

was $830,000, and the fair value was $950,000. For Club's other assets and

liabilities, book value was equal to fair value. The total fair value of Club's net

assets was $3,500,000.

Using the acquisition method, determine the amount of goodwill associated with

Caldwell's purchase of Club.

107. Caldwell Inc. acquired 65% of Club Corp. for $2,600,000. Club owned a

building and equipment with ten-year useful lives. The book value of these assets

was $830,000, and the fair value was $950,000. For Club's other assets and

liabilities, book value was equal to fair value. The total fair value of Club's net

assets was $3,500,000.

Determine the amount of the non-controlling interest as of the date of the

acquisition.

108. On January 1, 2010, Glenville Co. acquired an 80% interest in Acron Corp.

for $500,000. There is no active trading market for Acron's stock. The fair value of

Acron's net assets was $600,000 and Glenville accounts for its interest using the

acquisition method.

Determine the amount of goodwill to be recognized in this acquisition.

109. On January 1, 2010, Glenville Co. acquired an 80% interest in Acron Corp.

for $500,000. There is no active trading market for Acron's stock. The fair value of

Acron's net assets was $600,000 and Glenville accounts for its interest using the

acquisition method.

Determine the value assigned to the non-controlling interest as of the date of the

acquisition.

110. On January 1, 2010, Jannison Inc. acquired 90% of Techron Co. by paying

$477,000 cash. There is no active trading market for Techron stock. Techron Co.

reported a Common Stock account balance of $140,000 and Retained Earnings of

$280,000 at that date. The fair value of Techron Co. was appraised at $530,000.

The total annual amortization was $11,000 as a result of this transaction. The

subsidiary earned $98,000 in 2010 and $126,000 in 2011 with dividend payments

of $42,000 each year. Without regard for this investment, Jannison had income of

$308,000 in 2010 and $364,000 in 2011. Use the economic unit concept to

account for this acquisition.

Prepare a proper presentation of consolidated net income for 2010.

111. On January 1, 2010, Jannison Inc. acquired 90% of Techron Co. by paying

$477,000 cash. There is no active trading market for Techron stock. Techron Co.

reported a Common Stock account balance of $140,000 and Retained Earnings of

$280,000 at that date. The fair value of Techron Co. was appraised at $530,000.

The total annual amortization was $11,000 as a result of this transaction. The

subsidiary earned $98,000 in 2010 and $126,000 in 2011 with dividend payments

of $42,000 each year. Without regard for this investment, Jannison had income of

$308,000 in 2010 and $364,000 in 2011. Use the economic unit concept to

account for this acquisition.

Prepare a proper presentation of consolidated net income for 2011.

112. On January 1, 2010, Jannison Inc. acquired 90% of Techron Co. by paying

$477,000 cash. There is no active trading market for Techron stock. Techron Co.

reported a Common Stock account balance of $140,000 and Retained Earnings of

$280,000 at that date. The fair value of Techron Co. was appraised at $530,000.

The total annual amortization was $11,000 as a result of this transaction. The

subsidiary earned $98,000 in 2010 and $126,000 in 2011 with dividend payments

of $42,000 each year. Without regard for this investment, Jannison had income of

$308,000 in 2010 and $364,000 in 2011. Use the economic unit concept to

account for this acquisition.

What is the non-controlling interest balance as of December 31, 2011?

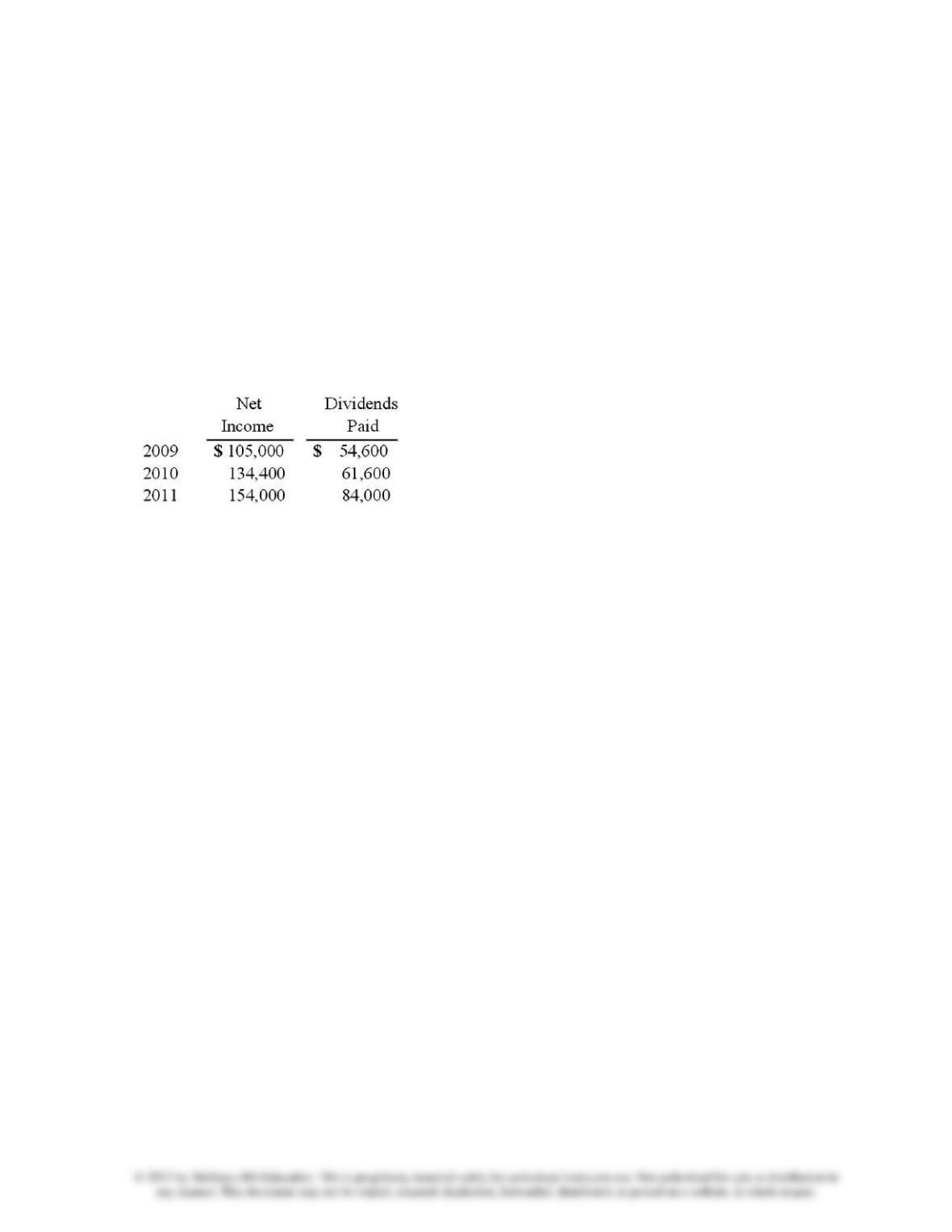

113. On January 1, 2009, Vacker Co. acquired 70% of Carper Inc. by paying

$650,000. This included a $20,000 control premium. Carper reported common

stock on that date of $420,000 with retained earnings of $252,000. A building was

undervalued in the company's financial records by $28,000. This building had a

ten-year remaining life. Copyrights of $80,000 were to be recognized and

amortized over 20 years.

Carper earned income and paid cash dividends as follows:

On December 31, 2011, Vacker owed $30,800 to Carper. There have been no

changes in Carper's common stock account since the acquisition.

Required:

If the equity method had been applied by Vacker for this acquisition, what were

the consolidation entries needed as of December 31, 2011?

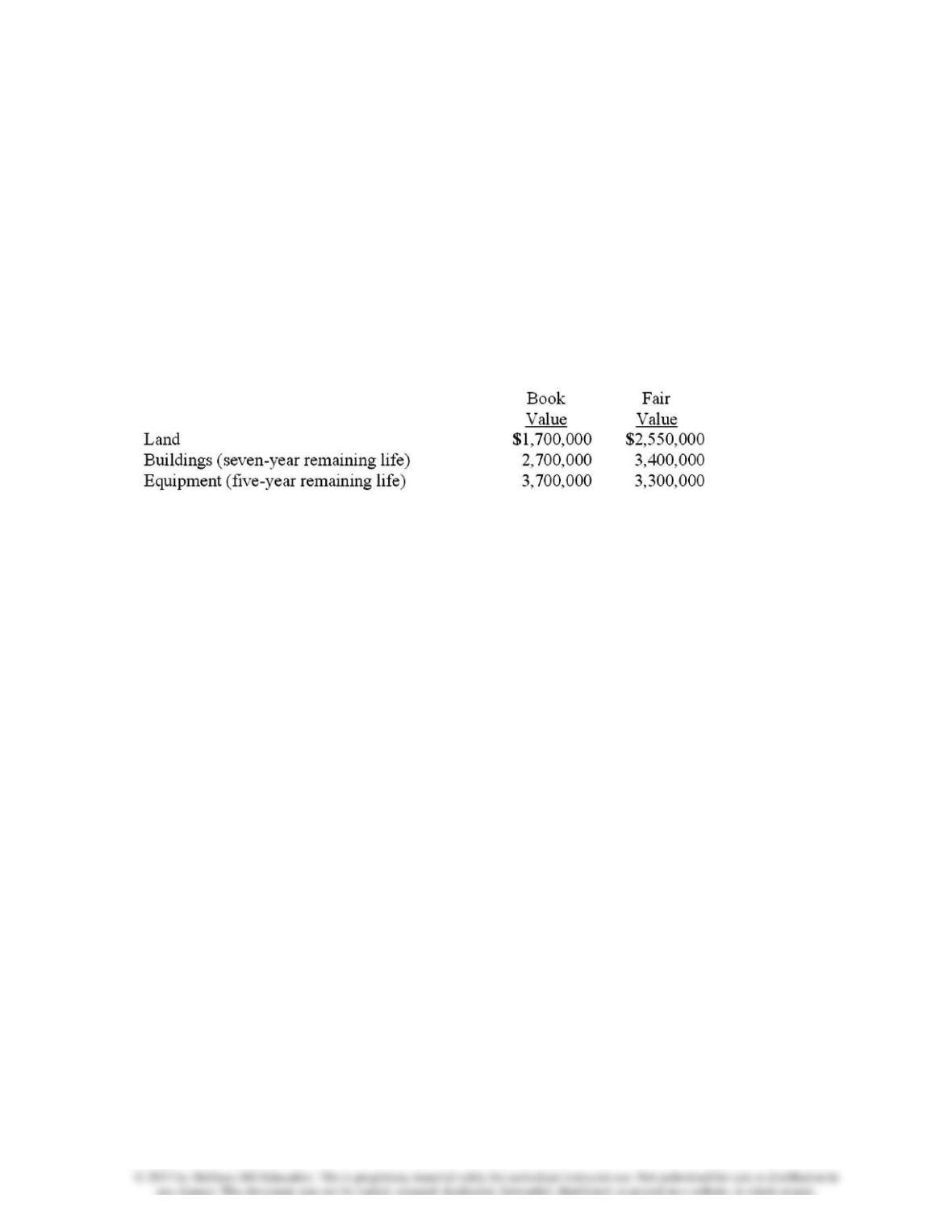

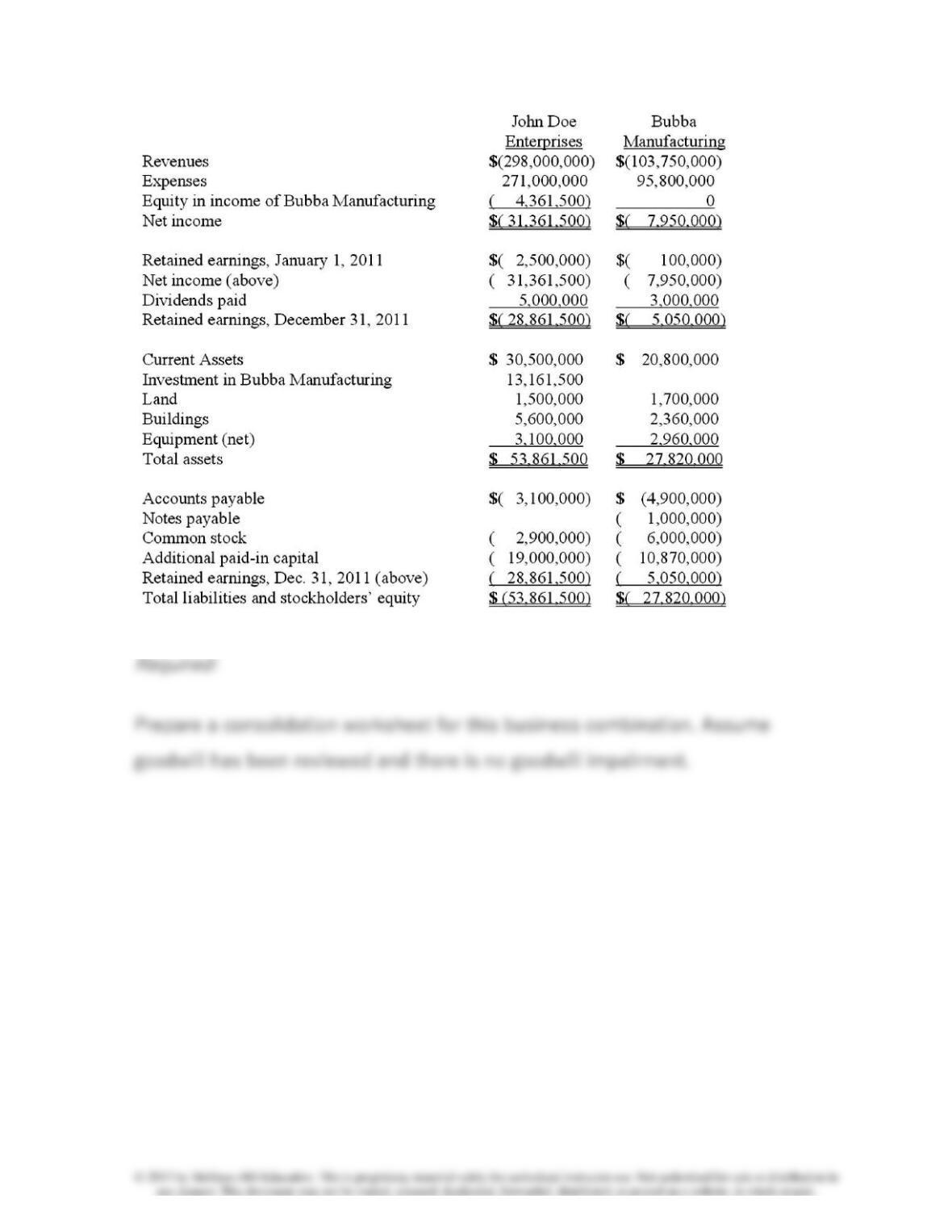

114. On January 1, 2011, John Doe Enterprises (JDE) acquired a 55% interest in

Bubba Manufacturing, Inc. (BMI). JDE paid for the transaction with $3 million

cash and 500,000 shares of JDE common stock (par value $1.00 per share). At the

time of the acquisition, BMI's book value was $16,970,000.

On January 1, JDE stock had a market value of $14.90 per share and there was no

control premium in this transaction. Any consideration transferred over book

value is assigned to goodwill. BMI had the following balances on January 1, 2011.

115. On January 1, 2011, John Doe Enterprises (JDE) acquired a 55% interest in

Bubba Manufacturing, Inc. (BMI). JDE paid for the transaction with $3 million

cash and 500,000 shares of JDE common stock (par value $1.00 per share). At the

time of the acquisition, BMI's book value was $16,970,000.

On January 1, JDE stock had a market value of $14.90 per share and there was no

control premium in this transaction. Any consideration transferred over book

value is assigned to goodwill. BMI had the following balances on January 1, 2011.

For internal reporting purposes, JDE employed the equity method to account for

this investment.

The following account balances are for the year ending December 31, 2011 for

both companies.

116. McLaughlin, Inc. acquires 70 percent of Ellis Corporation on September 1,

2010, and an additional 10 percent on November 1, 2011. Annual amortization of

$8,400 attributed to the controlling interest relates to the first acquisition. Ellis

reports the following figures for 2011:

Without regard for this investment, McLaughlin earns $480,000 in net income

($840,000 revenues less $360,000 expenses; incurred evenly through the year)

during 2011.

Required: Prepare a schedule of consolidated net income and apportionment to

non-controlling and controlling interests for 2011.

117. Select True (T) or False (F) for each of the following statements:

_____ 1. A parent will recognize a gain or loss if it sells a portion of its investment

in a subsidiary and maintains control after the sale.

_____ 2. A parent sells a portion of its investment in a subsidiary and no longer

maintains control. This sale of shares represents a remeasurement event for the

investee.

_____ 3. International financial reporting standards (IFRS) allow an option to value

the non-controlling interest with goodwill or to value the non-controlling interest

without goodwill.

_____ 4. Consolidated net income represents the combined net income of the

parent and subsidiary after subtracting the non-controlling interest in the net

income of the subsidiary.

_____ 5. The total acquisition-date fair value of an acquired firm is the sum of the

fair value of the controlling interest and the fair value of the non-controlling

interest.

_____ 6. When control of a subsidiary is acquired on a date other than the first

day of a fiscal year, excess amortization expenses are pro-rated to include only

the post-acquisition period.

_____ 7. For a mid-year acquisition following an equity method investment of the

same company, the consolidated income statement will report consolidated

revenues and expenses for the entire year.

_____ 8. In a step acquisition where the parent previously held a non-controlling

interest in the acquired firm, the parent remeasures the prior interest to fair

value.

_____ 9. When a parent has control over a subsidiary with less than 100 percent

ownership, and thereafter increases its ownership, the parent remeasures the

prior interest to fair value.