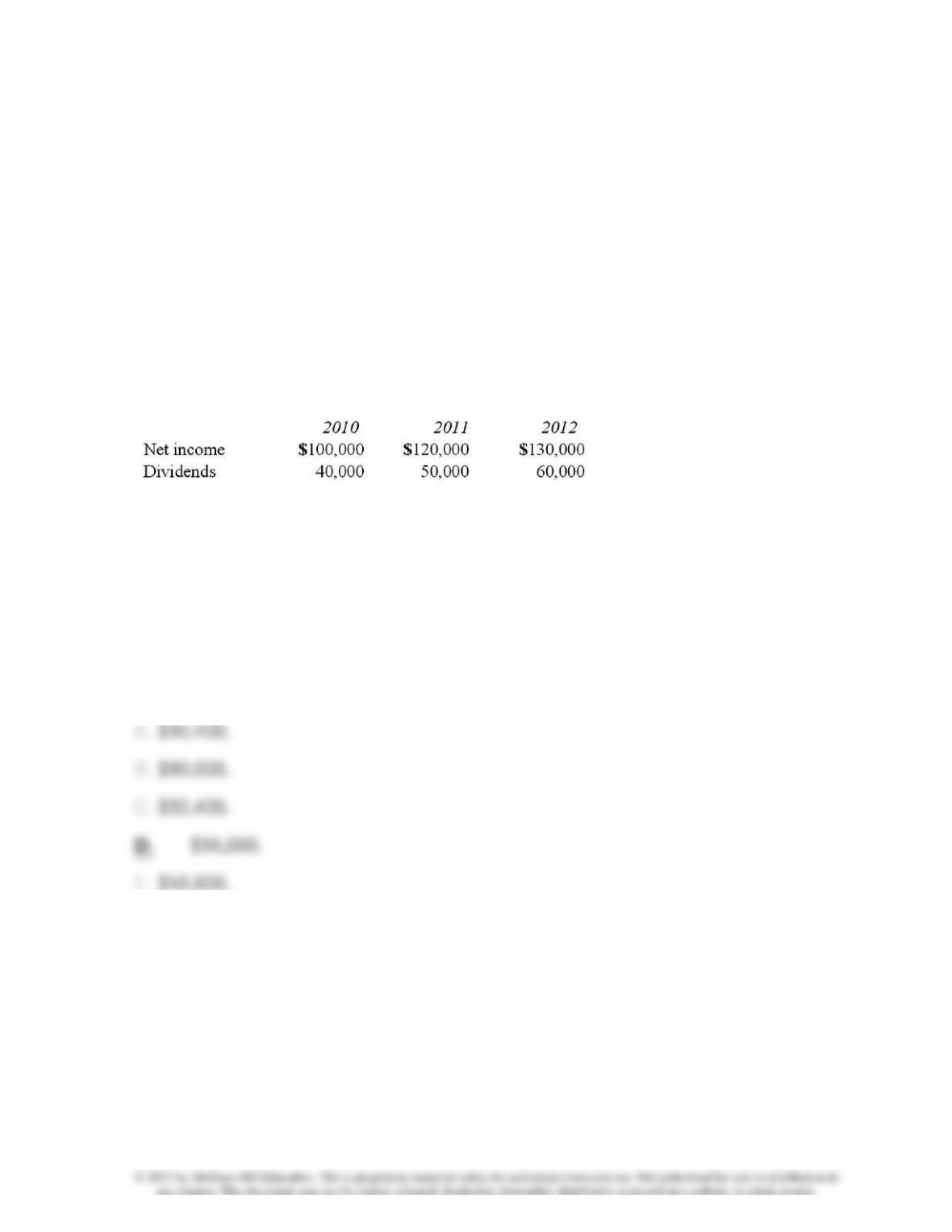

82. Pell Company acquires 80% of Demers Company for $500,000 on January 1,

2010. Demers reported common stock of $300,000 and retained earnings of

$210,000 on that date. Equipment was undervalued by $30,000 and buildings

were undervalued by $40,000, each having a 10-year remaining life. Any excess

consideration transferred over fair value was attributed to goodwill with an

indefinite life.

Demers earns income and pays dividends as follows:

Assume the partial equity method is applied.

How much does Pell record as income from Demers for the year ended December

31, 2011?

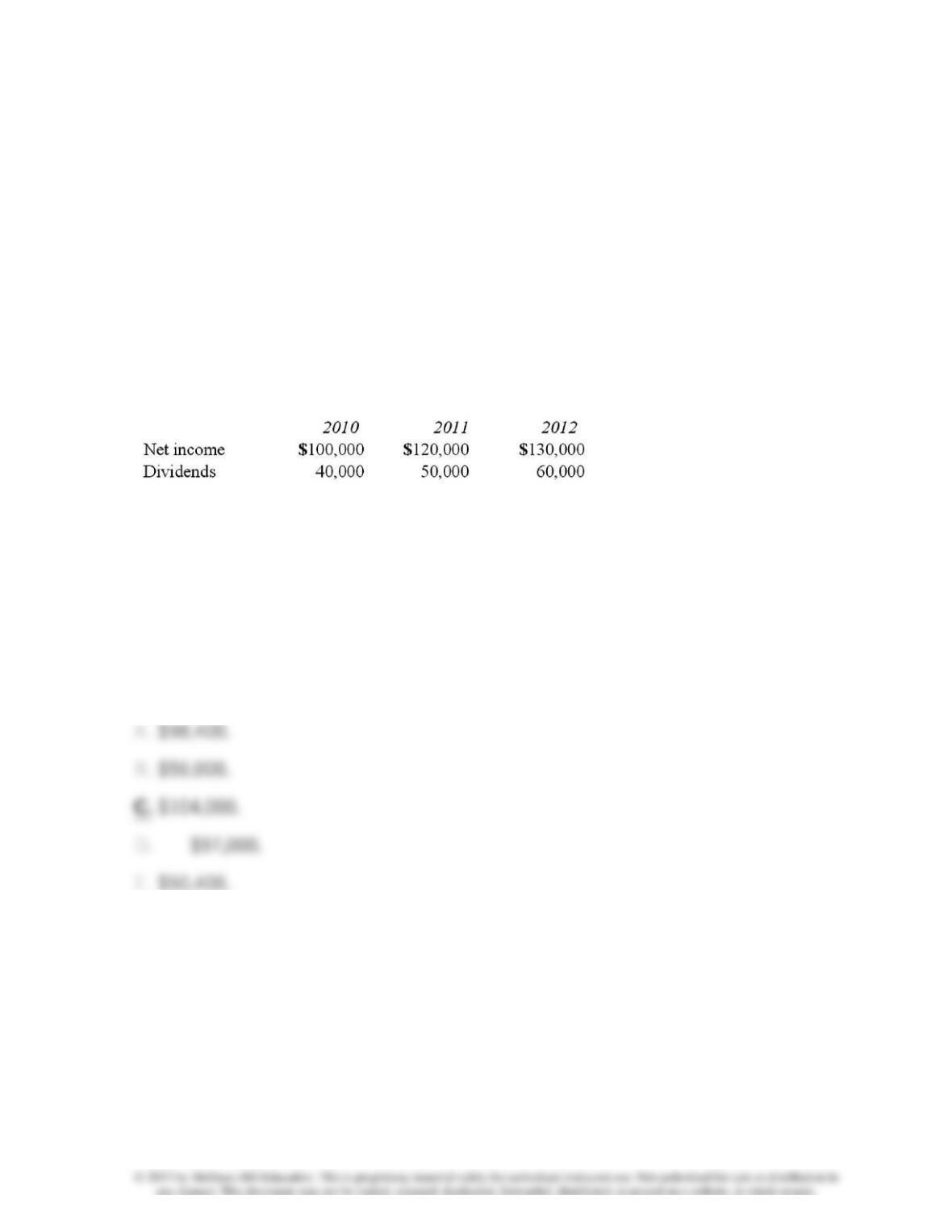

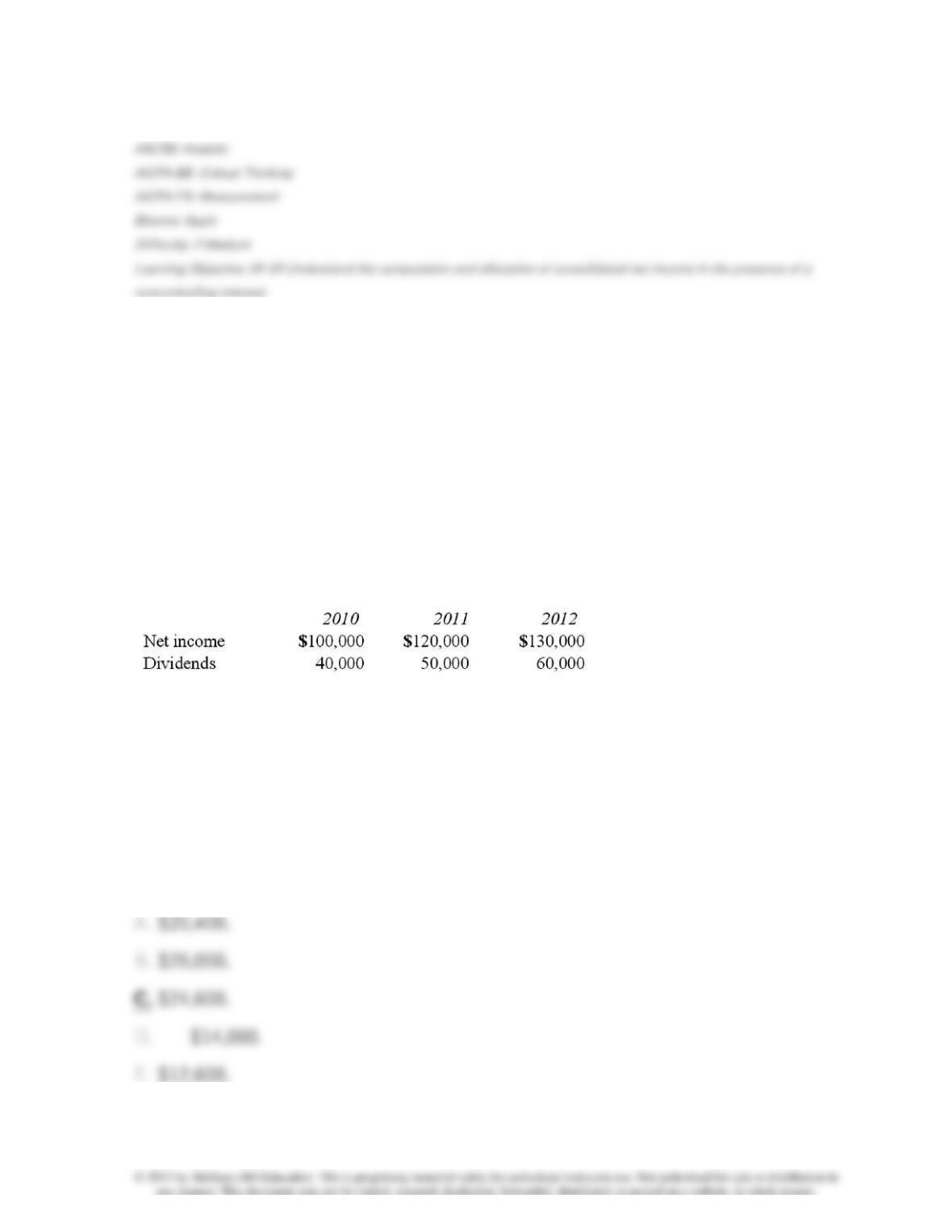

83. Pell Company acquires 80% of Demers Company for $500,000 on January 1,

2010. Demers reported common stock of $300,000 and retained earnings of

$210,000 on that date. Equipment was undervalued by $30,000 and buildings

were undervalued by $40,000, each having a 10-year remaining life. Any excess

consideration transferred over fair value was attributed to goodwill with an

indefinite life.

Demers earns income and pays dividends as follows:

Assume the partial equity method is applied.

How much does Pell record as income from Demers for the year ended December

31, 2012?

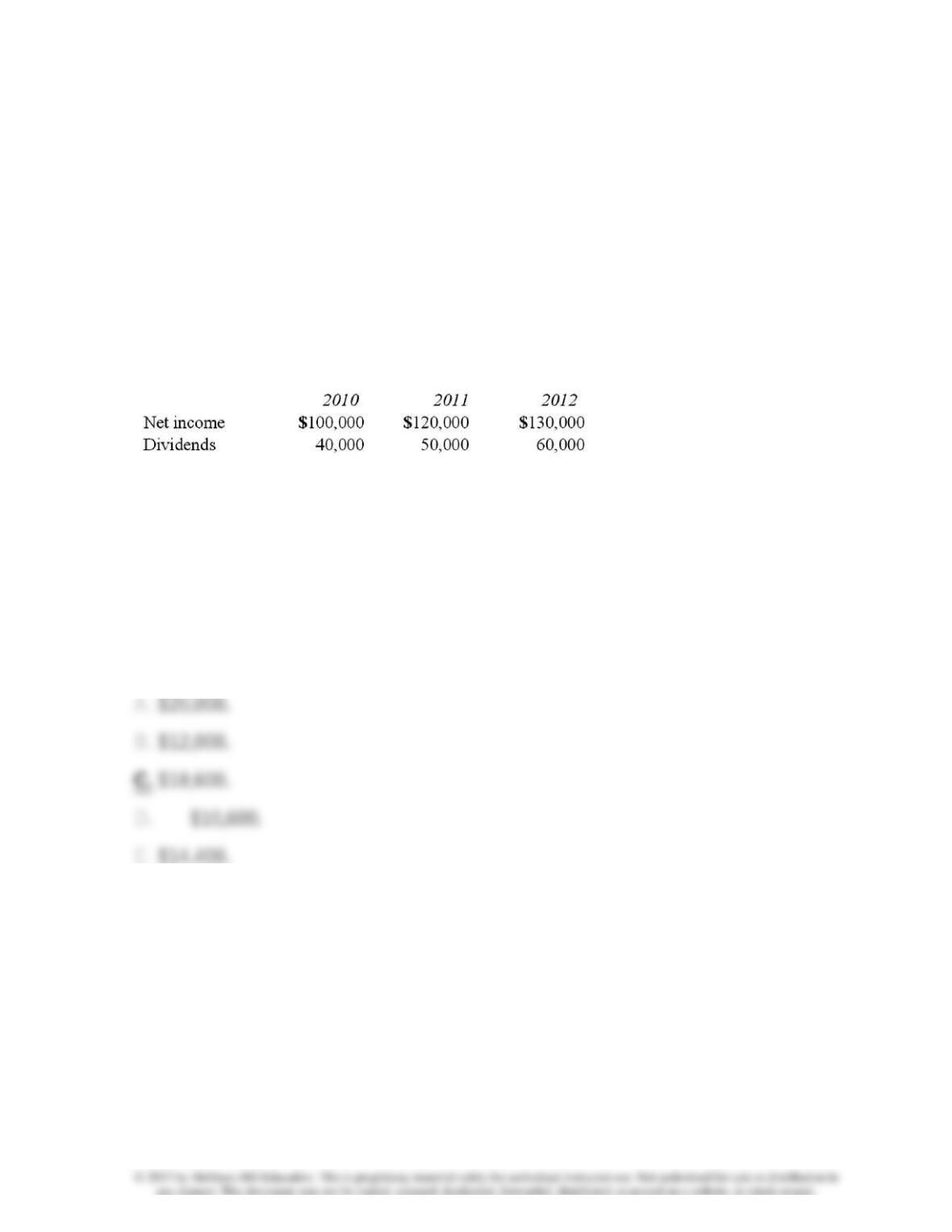

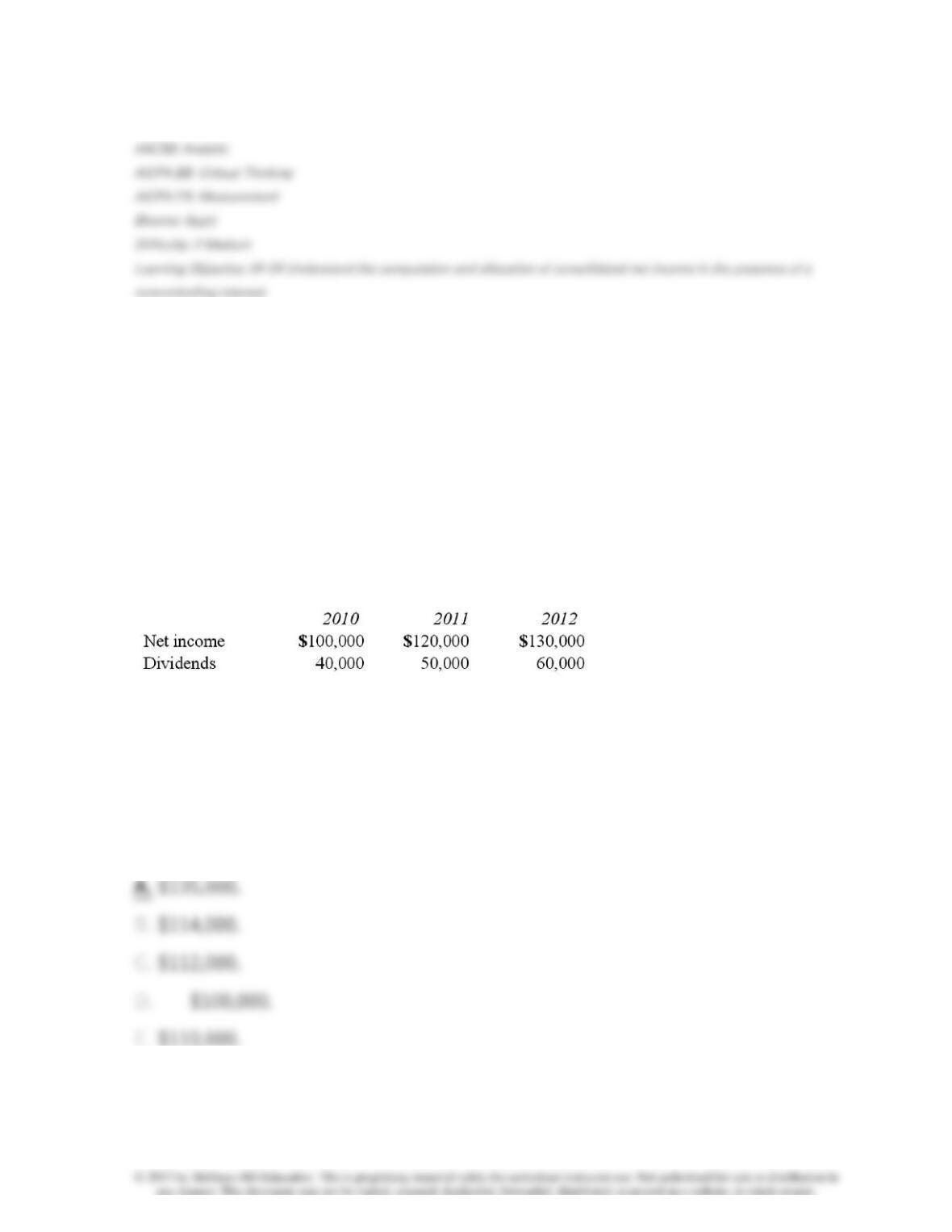

84. Pell Company acquires 80% of Demers Company for $500,000 on January 1,

2010. Demers reported common stock of $300,000 and retained earnings of

$210,000 on that date. Equipment was undervalued by $30,000 and buildings

were undervalued by $40,000, each having a 10-year remaining life. Any excess

consideration transferred over fair value was attributed to goodwill with an

indefinite life.

Demers earns income and pays dividends as follows:

Assume the partial equity method is applied.

Compute the non-controlling interest in the net income of Demers at December

31, 2010.

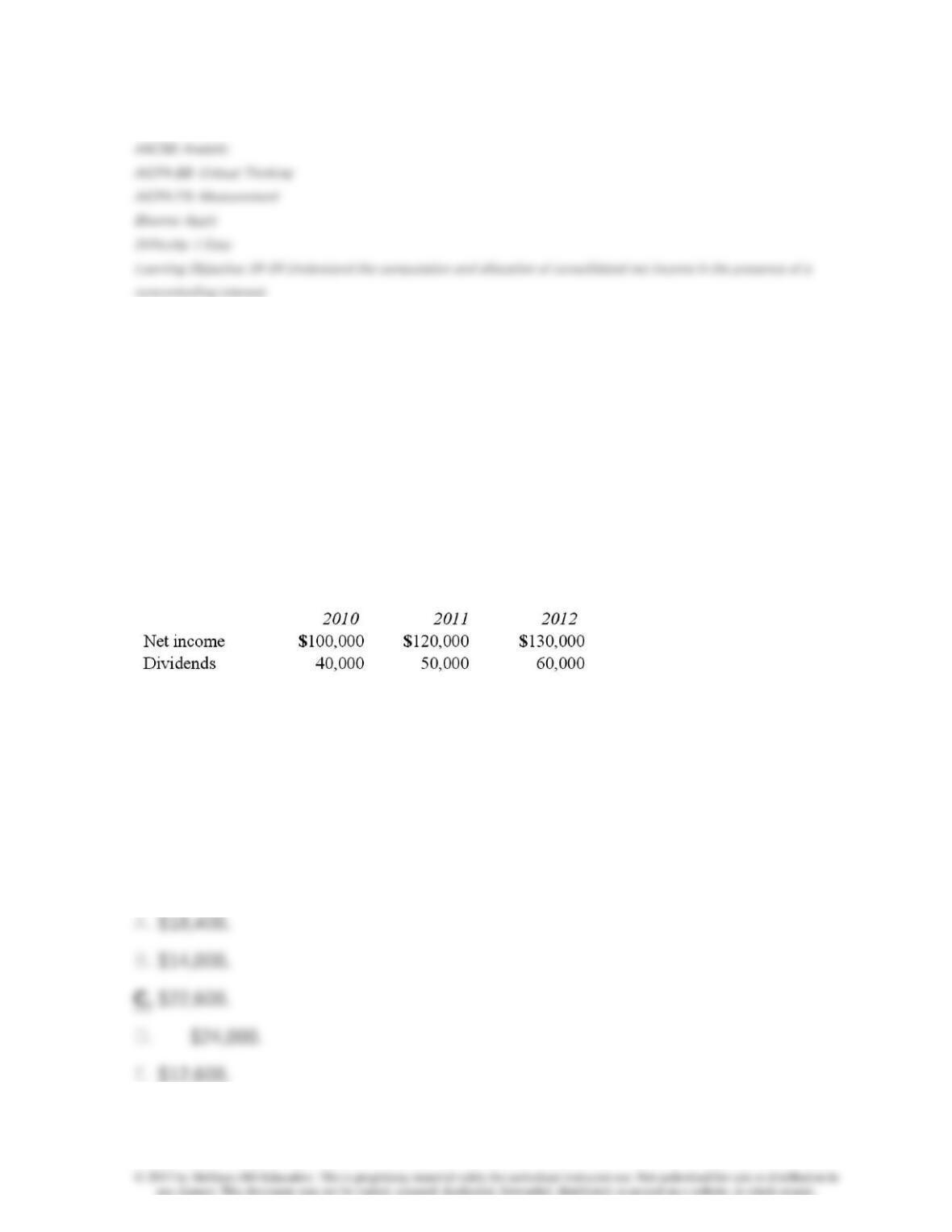

85. Pell Company acquires 80% of Demers Company for $500,000 on January 1,

2010. Demers reported common stock of $300,000 and retained earnings of

$210,000 on that date. Equipment was undervalued by $30,000 and buildings

were undervalued by $40,000, each having a 10-year remaining life. Any excess

consideration transferred over fair value was attributed to goodwill with an

indefinite life.

Demers earns income and pays dividends as follows:

Assume the partial equity method is applied.

Compute the non-controlling interest in the net income of Demers at December

31, 2011.

86. Pell Company acquires 80% of Demers Company for $500,000 on January 1,

2010. Demers reported common stock of $300,000 and retained earnings of

$210,000 on that date. Equipment was undervalued by $30,000 and buildings

were undervalued by $40,000, each having a 10-year remaining life. Any excess

consideration transferred over fair value was attributed to goodwill with an

indefinite life.

Demers earns income and pays dividends as follows:

Assume the partial equity method is applied.

Compute the non-controlling interest in the net income of Demers at December

31, 2012.

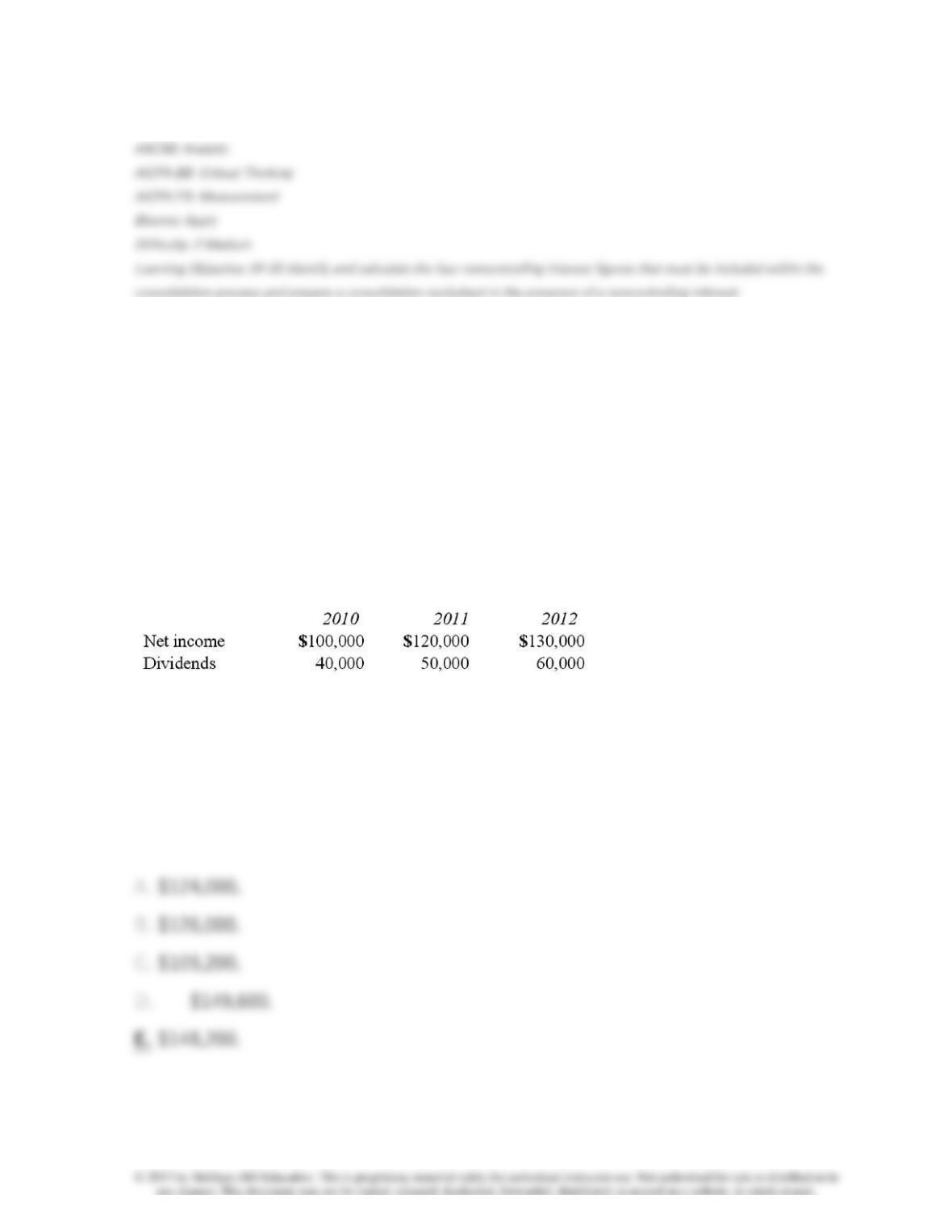

87. Pell Company acquires 80% of Demers Company for $500,000 on January 1,

2010. Demers reported common stock of $300,000 and retained earnings of

$210,000 on that date. Equipment was undervalued by $30,000 and buildings

were undervalued by $40,000, each having a 10-year remaining life. Any excess

consideration transferred over fair value was attributed to goodwill with an

indefinite life.

Demers earns income and pays dividends as follows:

Assume the partial equity method is applied.

Compute the non-controlling interest in Demers at December 31, 2010.

88. Pell Company acquires 80% of Demers Company for $500,000 on January 1,

2010. Demers reported common stock of $300,000 and retained earnings of

$210,000 on that date. Equipment was undervalued by $30,000 and buildings

were undervalued by $40,000, each having a 10-year remaining life. Any excess

consideration transferred over fair value was attributed to goodwill with an

indefinite life.

Demers earns income and pays dividends as follows:

Assume the partial equity method is applied.

Compute the non-controlling interest in Demers at December 31, 2011.

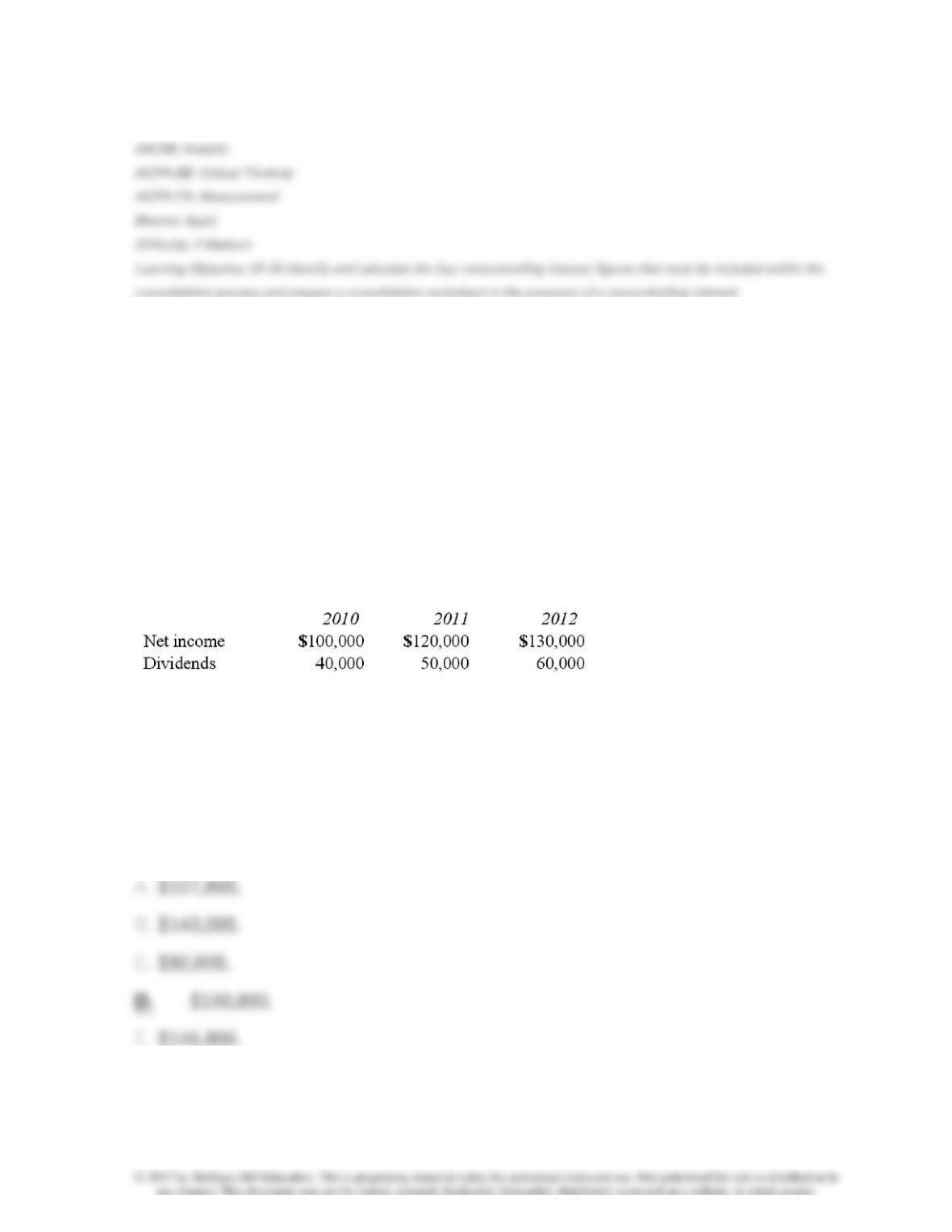

89. Pell Company acquires 80% of Demers Company for $500,000 on January 1,

2010. Demers reported common stock of $300,000 and retained earnings of

$210,000 on that date. Equipment was undervalued by $30,000 and buildings

were undervalued by $40,000, each having a 10-year remaining life. Any excess

consideration transferred over fair value was attributed to goodwill with an

indefinite life.

Demers earns income and pays dividends as follows:

Assume the partial equity method is applied.

Compute the non-controlling interest in Demers at December 31, 2012.

90. Parsons Company acquired 90% of Roxy Company several years ago and

recorded goodwill of $200,000 at that date. During 2013 an analysis of the fair

value of Roxy’s assets determined an impairment of goodwill in the amount of

$50,000.

At what amount would consolidated goodwill be reported for 2013?

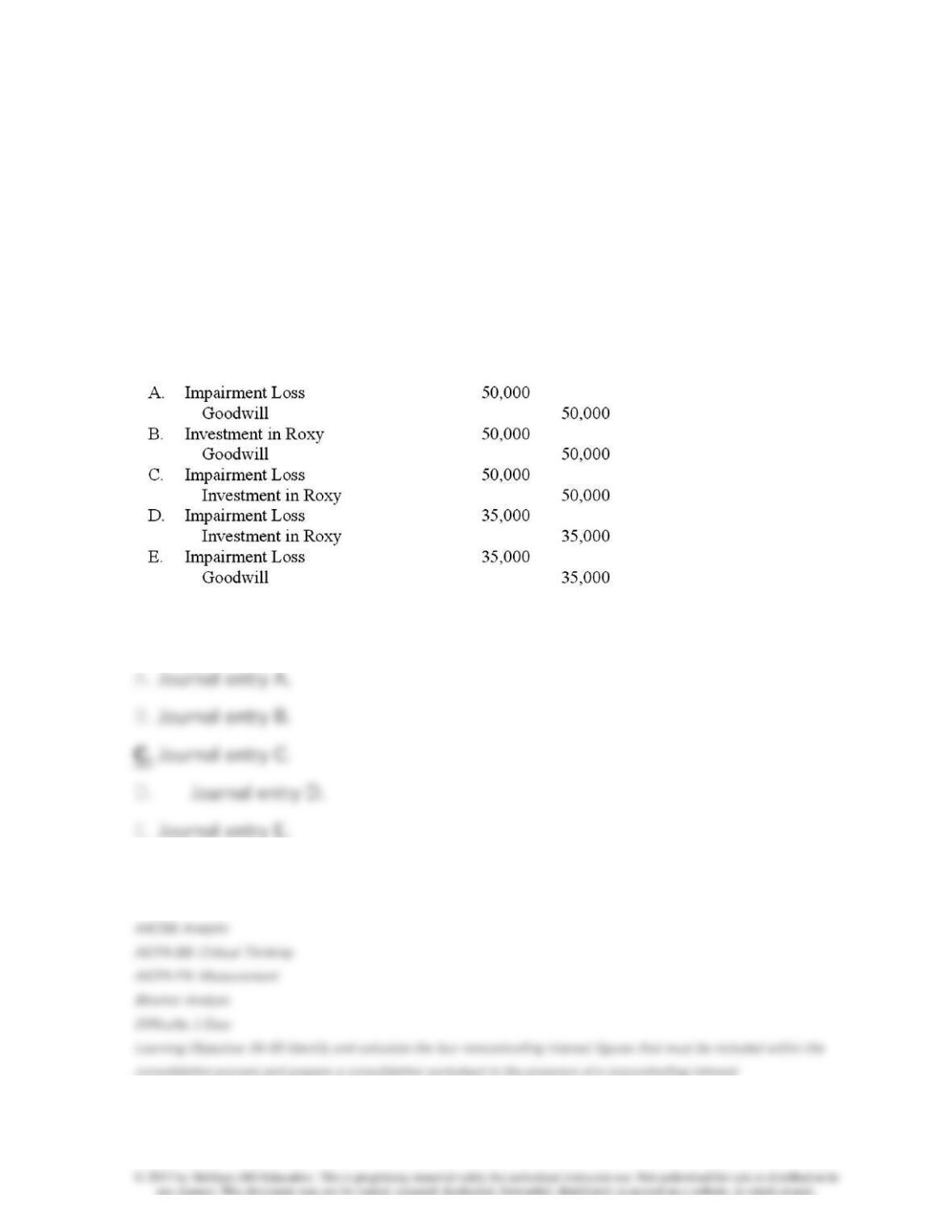

91. Parsons Company acquired 90% of Roxy Company several years ago and

recorded goodwill of $200,000 at that date. During 2013 an analysis of the fair

value of Roxy’s assets determined an impairment of goodwill in the amount of

$50,000.

What journal entry would be made by Parsons regarding the impairment of

goodwill?

92. In comparing U.S. GAAP and international financial reporting standards

(IFRS) with regard to a basis for measurement of a non-controlling interest,

93. Where should a non-controlling interest appear on a consolidated balance

sheet?

94. What is preacquisition income?

95. Beta Corp. owns less than one hundred percent of the voting common

stock of Shedds Co. Under what conditions will Beta be required to prepare

consolidated financial statements?

96. Where may a non-controlling interest be presented in a consolidated

balance sheet?

97. How would you determine the amount of goodwill to be recognized at date

of acquisition when there is a non-controlling interest present?

98. How is a non-controlling interest in the net income of an entity reported in

the income statement?

99. One company buys a controlling interest in another company on April 1.

How should the preacquisition subsidiary revenues and expenses be handled in

the consolidated balances for the year of acquisition?

100. Prevatt, Inc. owns 80% of Franklin Company. During the current year, a

portion of the investment in Franklin is sold. Prior to recording the sale, Prevatt

adjusts the carrying value of its investment. What is the purpose of the

adjustment?

101. How does a parent company account for the sale of a portion of an

investment in a subsidiary?

102. Alonzo Co. acquired 60% of Beazley Corp. by paying $240,000 cash. There

is no active trading market for Beazley Corp. At the time of the acquisition, the

book value of Beazley’s net assets was $300,000.

Required:

What amount should have been assigned to the non-controlling interest

immediately after the combination?