20. The accountant at Abco, Inc. made an adjusting entry at the end of February to accrue

interest on a note receivable from a customer. The effect of this entry is to:

21. The accounting concept/principle being applied when an adjustment is made is usually:

22. The Interest Receivable account for February showed transactions totaling $8,500 and an

adjustment of $11,200.

23. The balance in the Wages Payable account increased from $12,200 at the beginning of

the month to $15,000 at the end of the month. Wages accrued during the month totaled $61,000.

24. When a firm purchases supplies for use in its business, and the cost of the supplies

purchased is recorded as an asset, the following adjustment to recognize the cost of supplies

used will probably be required:

25. When a firm purchases supplies for its business:

26. The effect of an adjustment on the financial statements is usually to:

27. At the beginning of the current fiscal year, Surrey Corp.’s balance sheet showed assets of

$675,000 and liabilities of $525,000. During the year, liabilities decreased by $35,000. Net Income

for the year was $175,000, and net assets at the end of the year were $193,000. There were no

changes in paid-in capital during the year.

Calculate the dividends, if any, declared during the year.

Calculate the total assets at the end of the year.

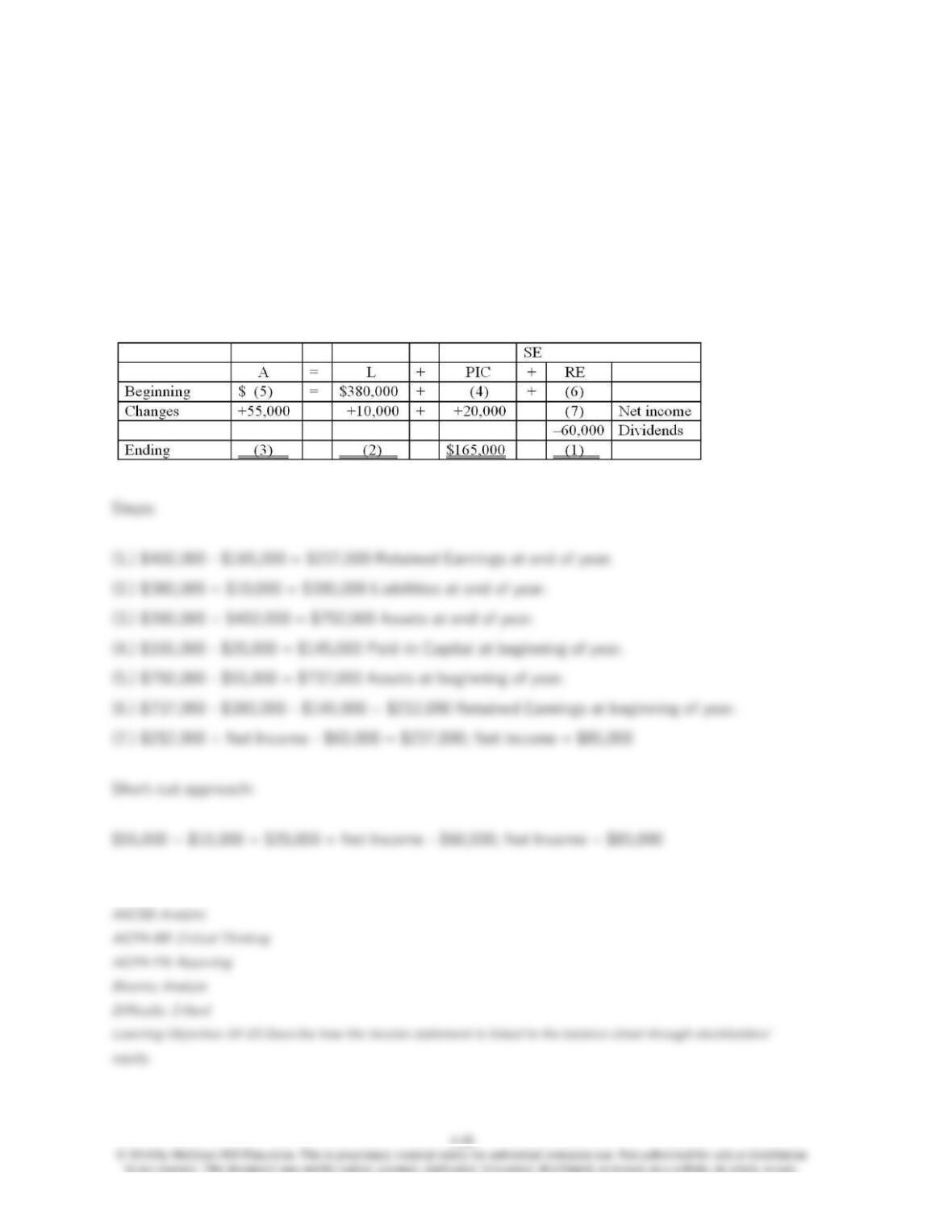

28. At the beginning of the current fiscal year, the balance sheet of Arches Co. showed

liabilities of $380,000. During the year liabilities increased by $10,000, assets increased by

$55,000, and paid-in capital increased by $20,000 to $165,000. Dividends declared and paid

during the year were $60,000. At the end of the year, stockholders’ equity totaled $402,000.

Calculate net income or loss for the year.

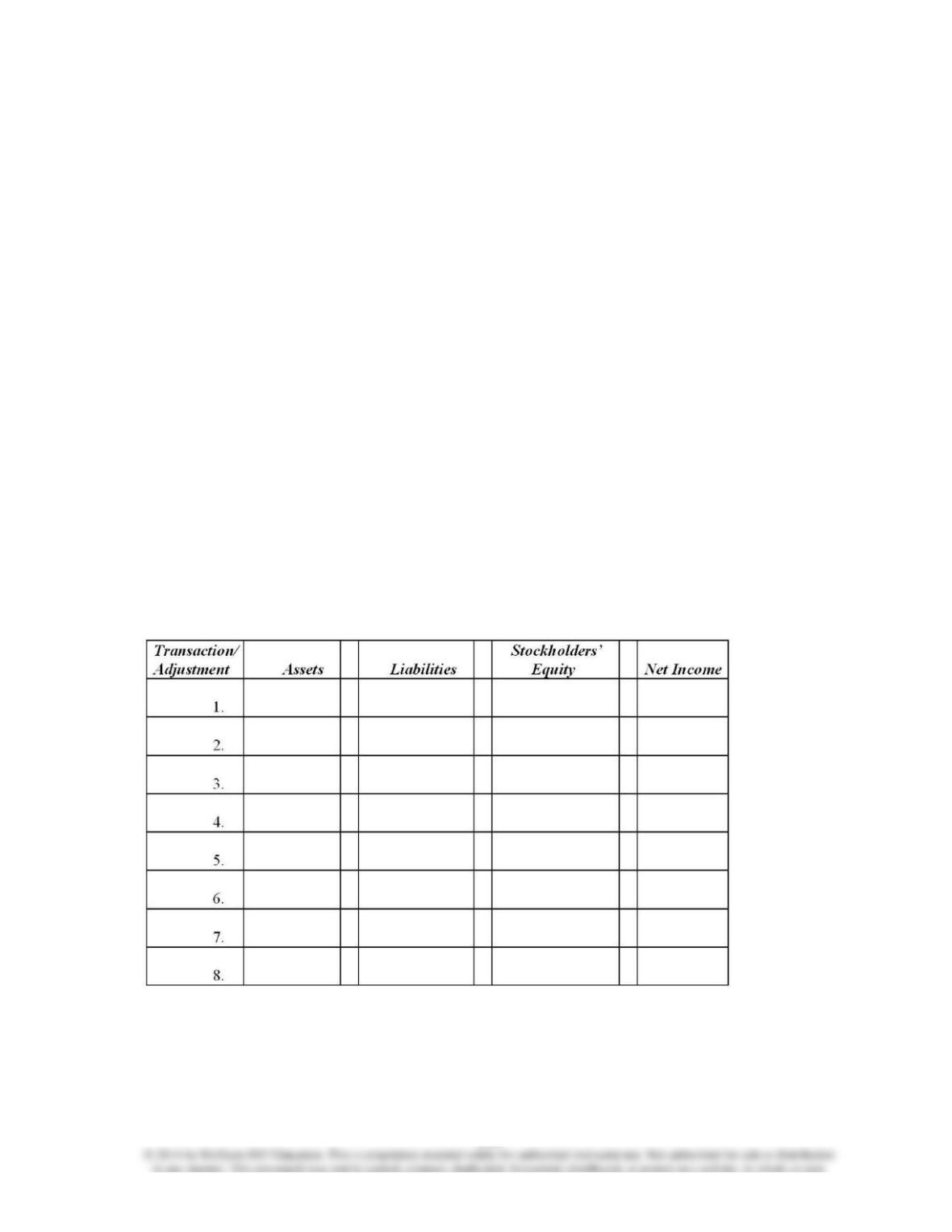

29. Using the column headings provided below, show the effect, if any, of the transaction

entry or adjusting entry on the appropriate balance sheet category or on the income statement by

entering the account name, amount, and indicating whether it is an addition (+) or subtraction (–

). Column headings reflect the expanded balance sheet equation; items that affect net income

should not be shown as affecting stockholders’ equity.

(1.) The firm borrowed $2,000 from the bank; a short-term note was signed.

(2.) Merchandise inventory costing $750 was purchased; cash of $200 was paid and the balance

is due in 30 days.

(3.) Employee wages of $1,000 were accrued at the end of the month.

(4.) Merchandise that cost $350 was sold for $450 in cash.

(5.) This month’s rent of $700 was paid.

(6.) Revenues from services during month totaled $6,500. Of this amount, $2,000 was received in

cash and the balance is expected to be received within 30 days.

(7.) During the month, supplies were purchased on account at a cost of $520, and debited into

the Supplies (asset) account. A total of $400 of supplies were used during the month.

(8.) Interest of $240 has been earned on a note receivable, but has not yet been received.

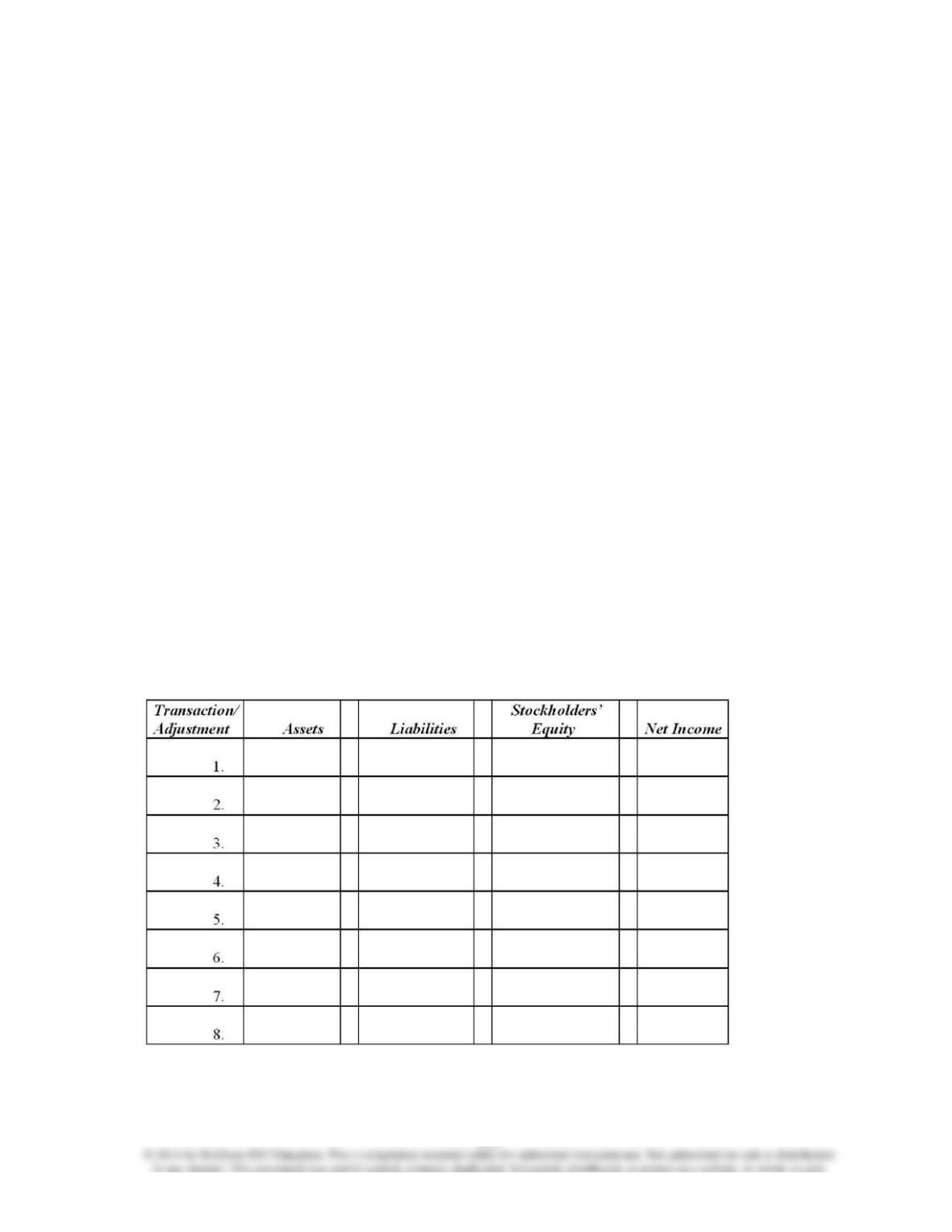

30. Using the column headings provided below, show the effect, if any, of the transaction

entry or adjusting entry on the appropriate balance sheet category or on the income statement by

entering the account name, amount, and indicating whether it is an addition (+) or subtraction (–

). Column headings reflect the expanded balance sheet equation; items that affect net income

should not be shown as affecting stockholders’ equity.

(1.) During the month, the board of directors declared a cash dividend of $1,200, payable next

month.

(2.) Employees were paid $1,900 in wages for their work during the first three weeks of the

month.

(3.) Employee wages of $600 for the last week of the month have not been recorded.

(4.) Merchandise that cost $900 was sold for $1,350. Of this amount, $1,000 was received in cash

and the balance is expected to be received within 30 days.

(5.) A contract was signed with a local radio station for a $100 advertisement; the ad was aired

during this month but will not be paid for until next month.

(6.) Store equipment was purchased at a cash price of $300. The original list price of the

equipment was $400, but a discount was received.

(7.) Received $180 of interest income for the current month.

(8.) Accrued $310 of interest expense at the end of the month.