51. At the time a $400 petty cash fund is being replenished, the company’s accountant finds

vouchers totaling $350 and petty cash of $50. The vouchers include: postage, $100; business

lunches, $150; delivery fees, $75; and office supplies, $25. Which of the following is not

recorded when recognizing expenditures from the petty cash fund?

52. Which of the following is correct regarding a petty cash fund?

53. A company’s cash balance is reported in which two financial statements?

54. The statement of cash flows reports cash flows from the activities of:

55. Operating cash flows would exclude:

56. Cash flows from investing do not include cash flows from:

57. Cash flows from financing activities include:

58. Cash flows from investing activities do not include:

59. Which of the following is NOT correct regarding the reporting of cash?

60. Investing cash flows would include which of the following?

61. Payment of dividends to stockholders is considered a(n):

62. Providing services to customers on account is considered a(n):

63. Issuing common stock for cash is considered a(n):

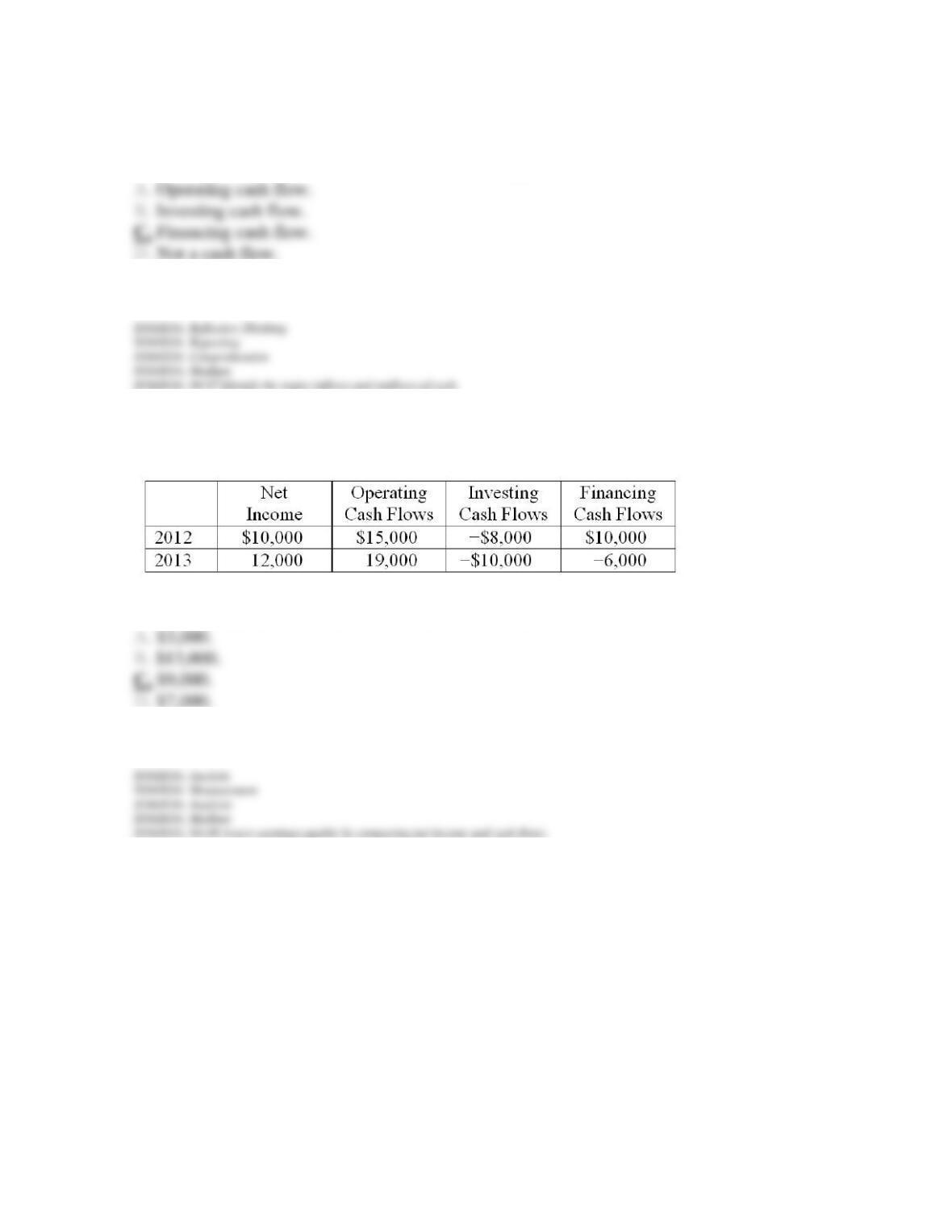

64. Terastar Corp. reports the following amounts for 2012 and 2013:

What is the amount of Terastar’s free cash flows for 2013?

65. Terastar Corp. reports the following amounts for 2012 and 2013.

What is the trend in free cash flows relative to net income?

66. Managers of the company act as stewards or caretakers of the company’s assets.

67. Common types of financial statement fraud include creating fictitious revenues from a

fake customer, improperly valuing assets, and mismatching revenues and expenses.

68. In response to corporate accounting scandals and to public outrage over seemingly

widespread unethical behavior of top executives, Congress passed the Sarbanes-Oxley Act.

69. The Sarbanes-Oxley Act is also known as Generally Accepted Accounting Principles.

70. The Public Company Accounting Oversight Board (PCAOB) has the authority to establish

standards dealing with auditing, quality control, ethics, independence, and other activities

relating to the preparation of audited financial reports.

71. Auditors of public companies can perform the full range of audit and nonaudit consulting

services for their audit clients.

72. Section 404 of the Sarbanes-Oxley Act requires that a company’s management document

and assess the effectiveness of all internal control processes that could affect financial

reporting.

73. Internal control is a company’s plan to (1) improve the accuracy and reliability of

accounting information and (2) safeguard the company’s assets.

74. One benefit of internal control is greater reliance by investors on reported financial

statements.

75. A framework for designing an internal control system is provided by the Financial

Accounting Standards Board (FASB).

76. The control environment refers to the overall top-to-bottom attitude of the company with

respect to internal controls.

77. Risk assessment procedures include periodic reviews of internal controls, assessing

management’s oversight of the internal control, developing solutions to known cases of

internal control failures, and determining whether each division or operation within a

company is meeting its objectives.

78. Separation of duties refers to auditors not being allowed to perform both audit and

nonaudit services for the same client.

79. An example of separation of duties would be not allowing an employee who receives cash

to also be responsible for depositing that cash in the bank account.

80. The internal control component of information and communication relates to the

effectiveness of accurately measuring and communicating business transactions.

81. Management needs to monitor the internal control system, just like any other system. Any

control deficiencies spotted by employees should be reported immediately to management.

82. Separation of duties occurs when two or more people act in coordination to circumvent

internal controls.

83. Effective internal controls ensure a company’s success and survival.

84. The amount of cash reported in a company’s balance sheet includes currency, coins, and

balances in savings and checking accounts, as well as items acceptable for deposit in these

accounts, such as checks received from customers.

85. The amount of cash reported in a company’s balance sheet includes items acceptable for

deposit in bank accounts, such as checks received from customers.

86. The amount of cash reported in a company’s balance sheet includes the balance of

accounts receivable if cash collection is highly likely in the near future.

87. The amount of cash reported in a company’s balance sheet does not include cash

equivalents, defined as short-term investments that have a maturity date no longer than three

months from the date of purchase.

88. Common examples of cash equivalents are money market funds, Treasury bills, and

certificates of deposit.

89. Recording all cash receipts as soon as possible is considered a good internal control.

90. Opening mail and making a list of checks received once per week is considered a good

internal control over cash receipts.

91. Whether a customer uses cash, a check, or a debit card to make a purchase, the company

records the transaction as a cash sale.

92. When customers pay for services with a check, the company should debit Accounts

Receivable and credit Service Revenue.

93. When customers pay for services with a debit card, the company should debit Cash and

credit Service Revenue.

94. When a company pays for services received using a check, it should credit Accounts

Payable until the check is paid by the bank.

95. When a company pays for services received using a credit card, it should credit Accounts

Payable.

96. Allowing the employee who authorizes purchases to also prepare the check is an example

of good internal control.

97. Companies should set maximum purchase limits on debit cards and credit cards as part of

internal controls.

98. A bank reconciliation matches the balance of cash in the bank account with the balance of

cash in the company’s own records.

99. Differences in the company’s cash balance and the bank’s cash balance occur because of

either timing differences or errors.

100. An example of a bank error that causes the company’s balance and bank’s balance of cash

to differ is the purchase of supplies with a check.

101. Cash receipts of the company that have not been added to the bank’s record of the

company’s balance are referred to as checks outstanding.

102. Checks outstanding are checks the company has written that have not been subtracted

from the bank’s record of the company’s balance.

103. A deposit outstanding will cause the bank’s cash balance to be higher than the company’s

cash balance.

104. A check outstanding will cause the bank’s cash balance to be higher than the company’s

cash balance.

105. An NSF check is an example of a cash transaction that is initially recorded by the bank

and later by the company after notification.

106. Interest earned on a bank account is an example of a cash transaction recorded by the

company and then later by the bank after notification.

107. The final step in reconciling the bank’s cash balance and the company’s cash balance is to

update the company’s cash balance for the items used to reconcile the bank’s cash balance.

108. The petty cash fund represents cash on hand and is used to pay for minor purchases.

109. The petty cash fund should have just enough cash to make minor expenditures over a

reasonable period (such as a week or a month).

110. A company’s cash is reported in two financial statements – income statement and

statement of cash flows.

111. Cash is typically reported as a current asset in the balance sheet.

112. The statement of cash flows reports a company’s cash inflows and cash outflows related

to (1) operating activities, (2) investing activities, and (3) financing activities.