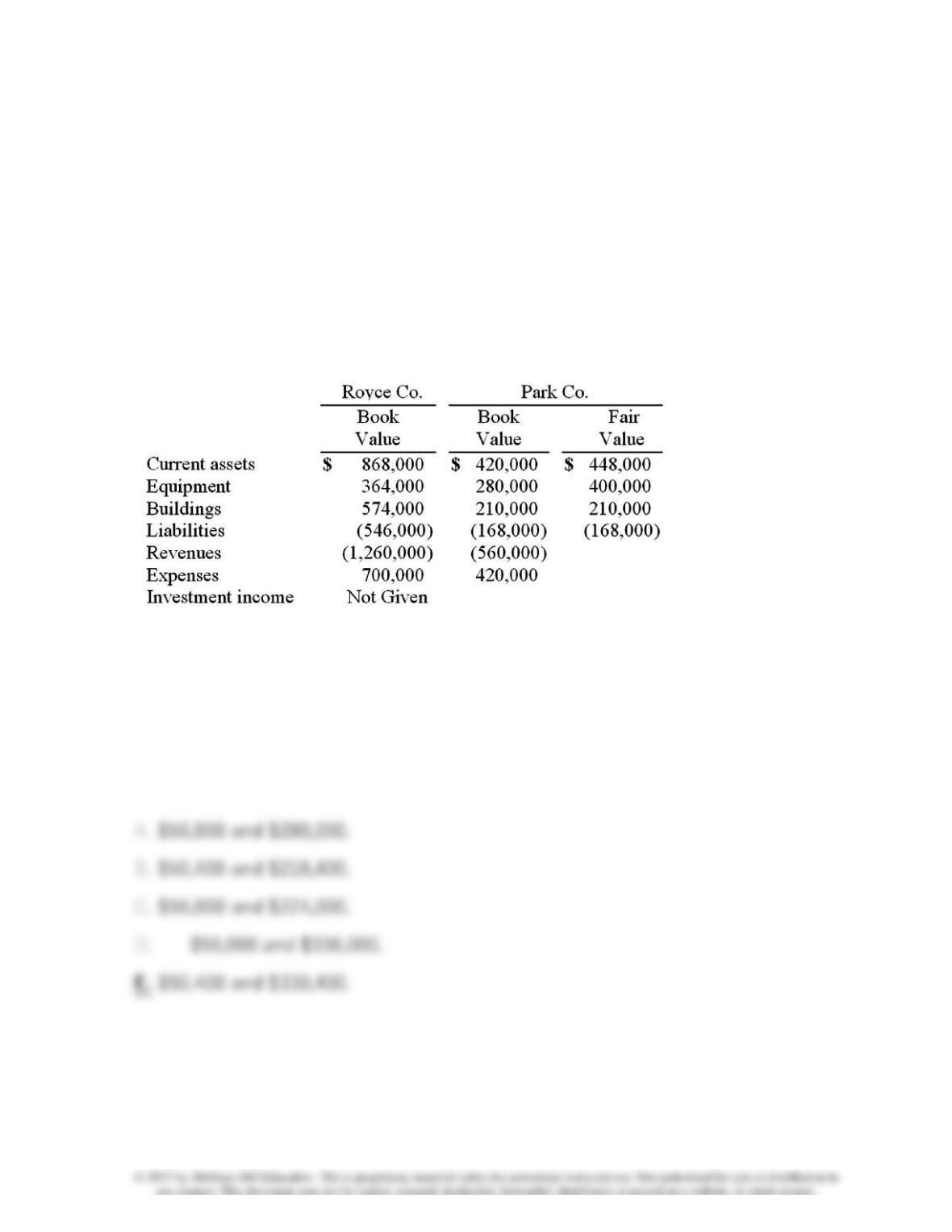

22. Royce Co. acquired 60% of Park Co. for $420,000 on December 31, 2010

when Park’s book value was $560,000. The Royce stock was not actively traded.

On the date of acquisition, Park had equipment (with a ten-year life) that was

undervalued in the financial records by $140,000. One year later, the following

selected figures were reported by the two companies. Additionally, no dividends

have been paid.

What is the non-controlling interest’s share of the subsidiary’s net income for the

year ended December 31, 2011

and

what is the ending balance of the non-

controlling interest in the subsidiary at December 31, 2011?

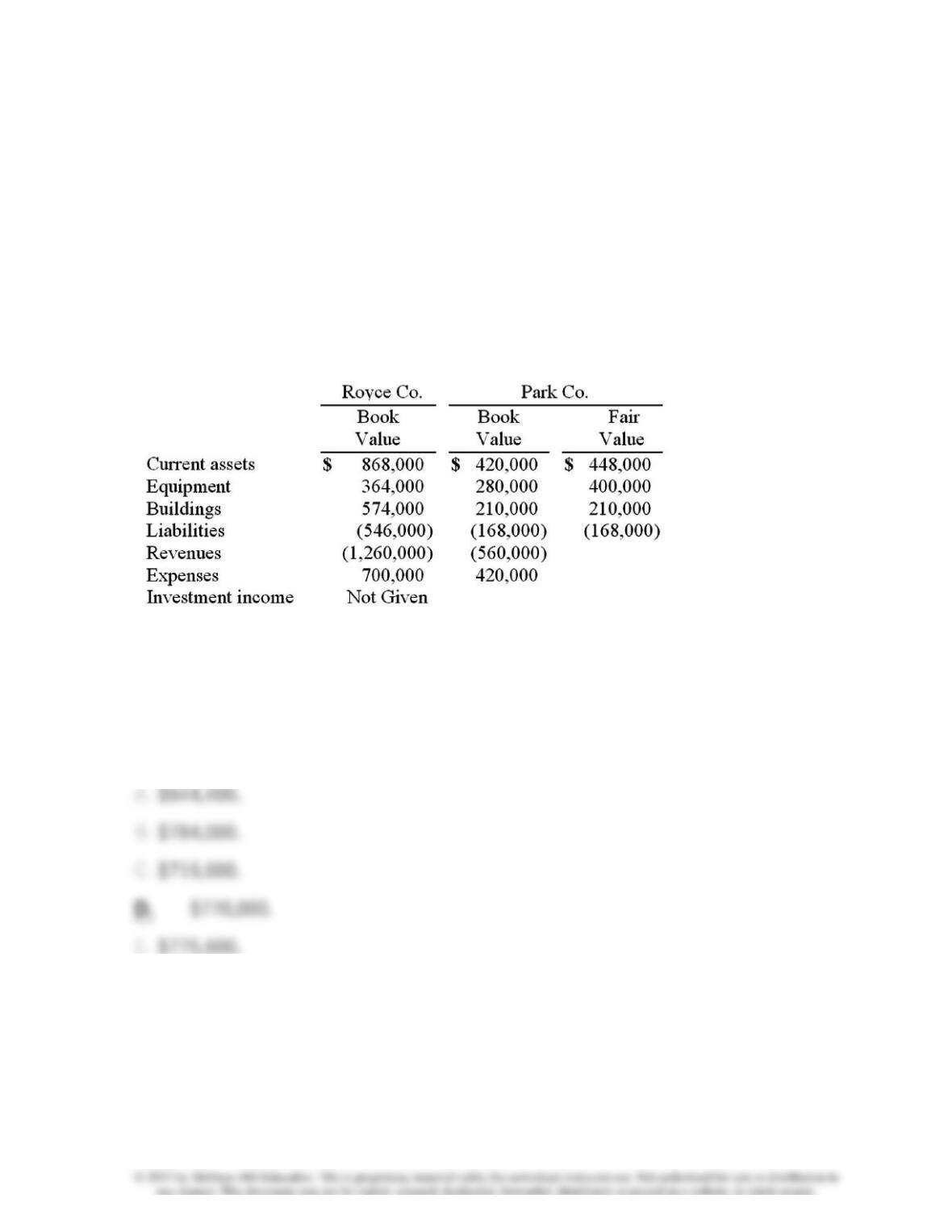

23. Royce Co. acquired 60% of Park Co. for $420,000 on December 31, 2010

when Park’s book value was $560,000. The Royce stock was not actively traded.

On the date of acquisition, Park had equipment (with a ten-year life) that was

undervalued in the financial records by $140,000. One year later, the following

selected figures were reported by the two companies. Additionally, no dividends

have been paid.

What is the consolidated balance of the Equipment account at December 31,

2011?

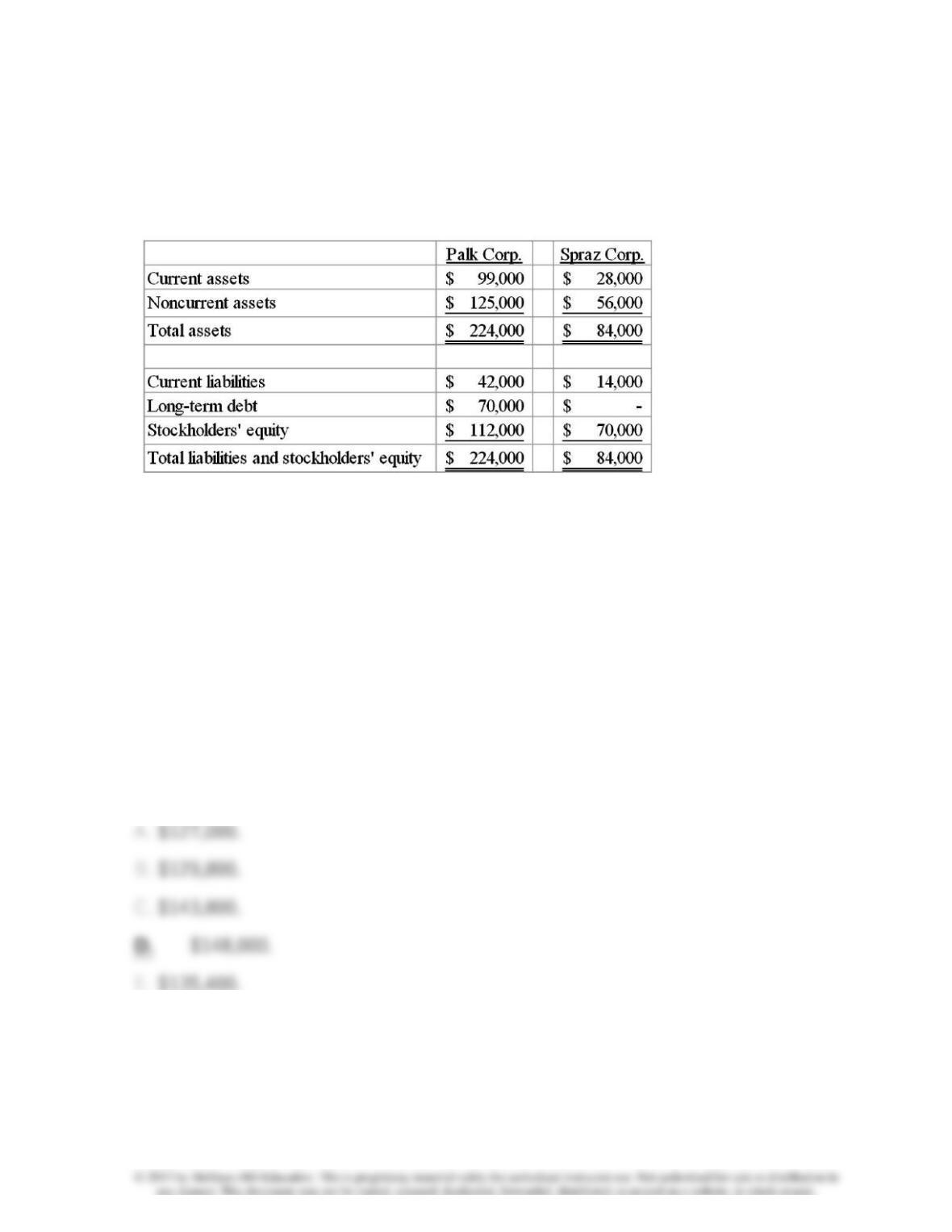

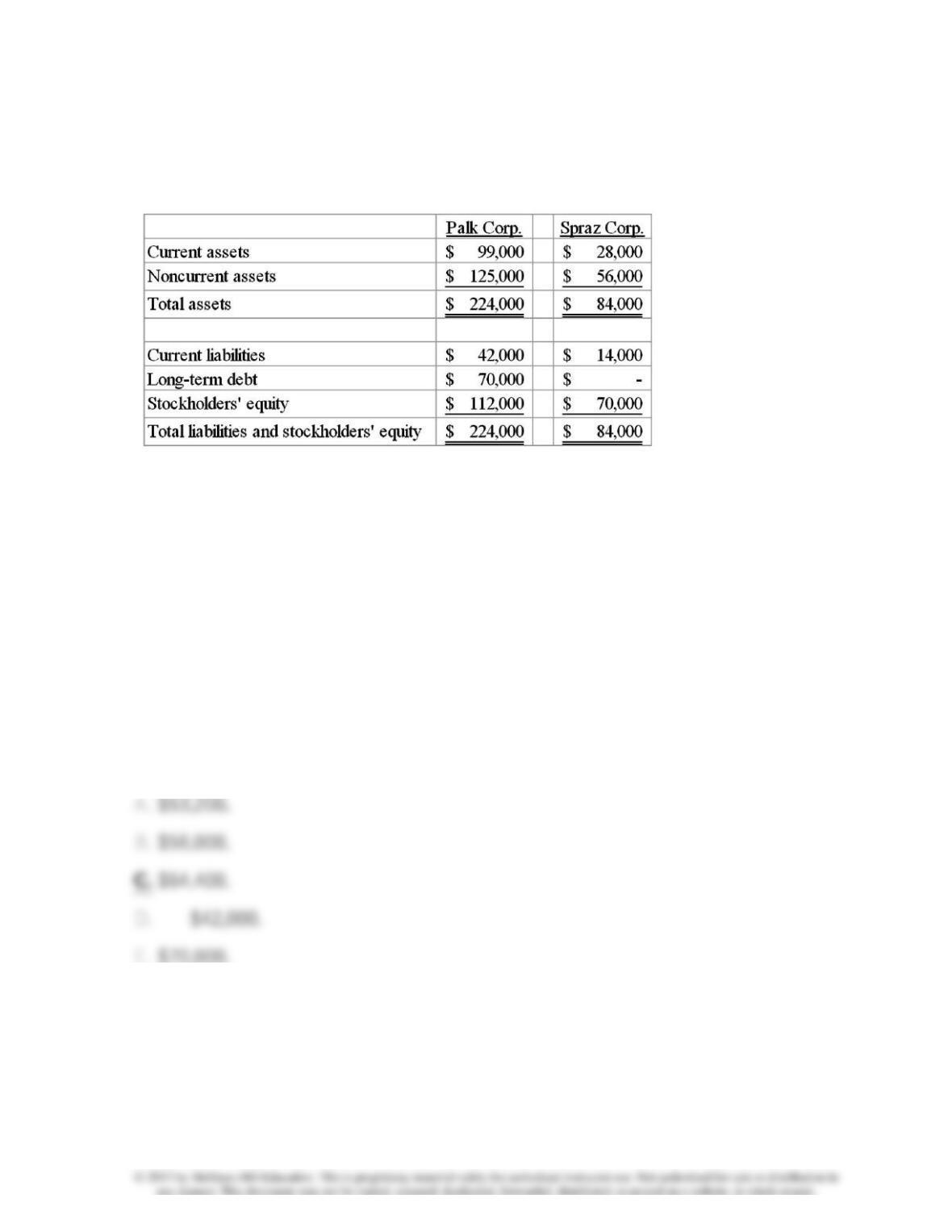

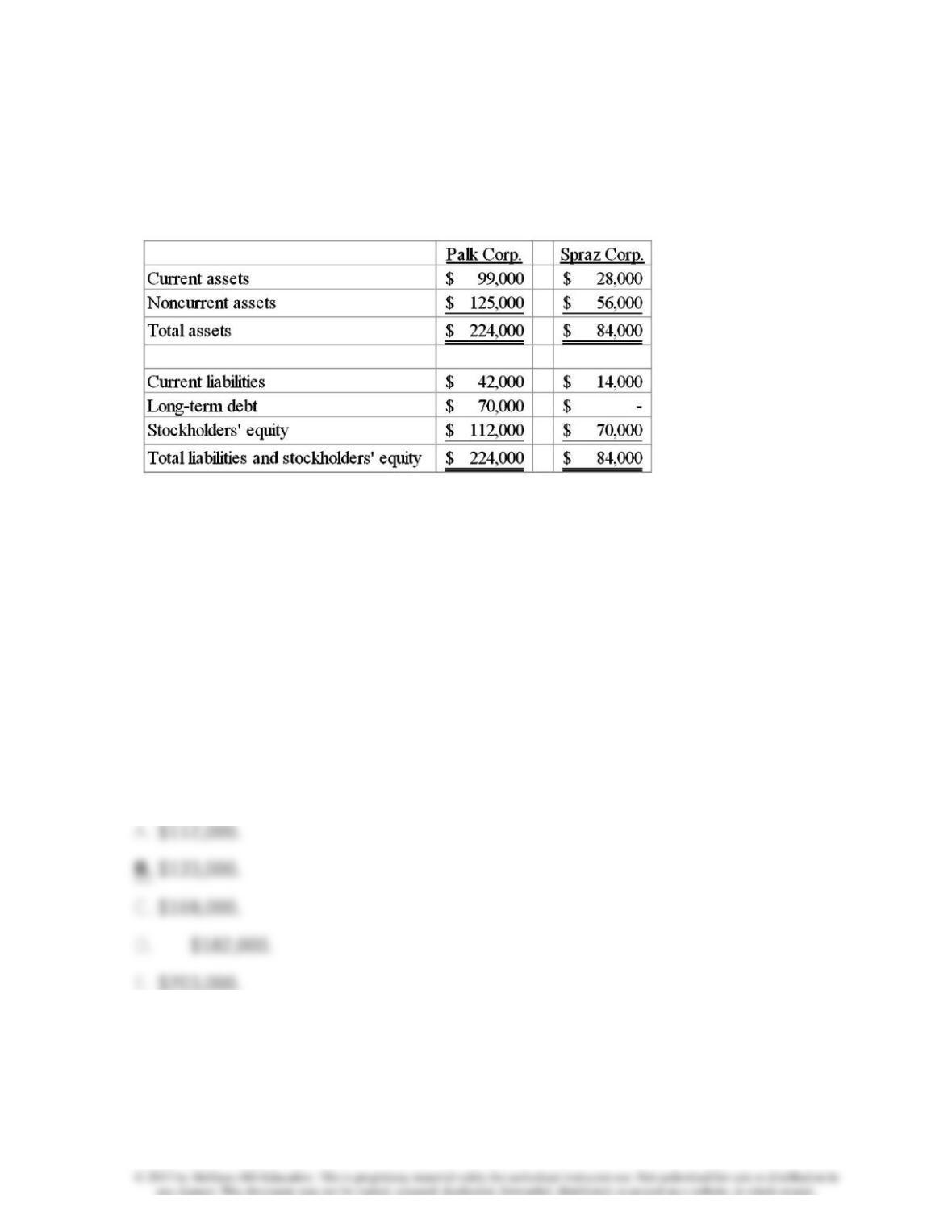

24. On January 1, 2010, Palk Corp. and Spraz Corp. had condensed balance

sheets as follows:

On January 2, 2010, Palk borrowed the entire $84,000 it needed to acquire 80% of

the outstanding common shares of Spraz. The loan was to be paid in ten equal

annual principal payments, plus interest, beginning December 31, 2010. The

excess consideration transferred over the underlying book value of the acquired

net assets was allocated 60% to inventory and 40% to goodwill.

What is

consolidated current assets

at January 2, 2010?

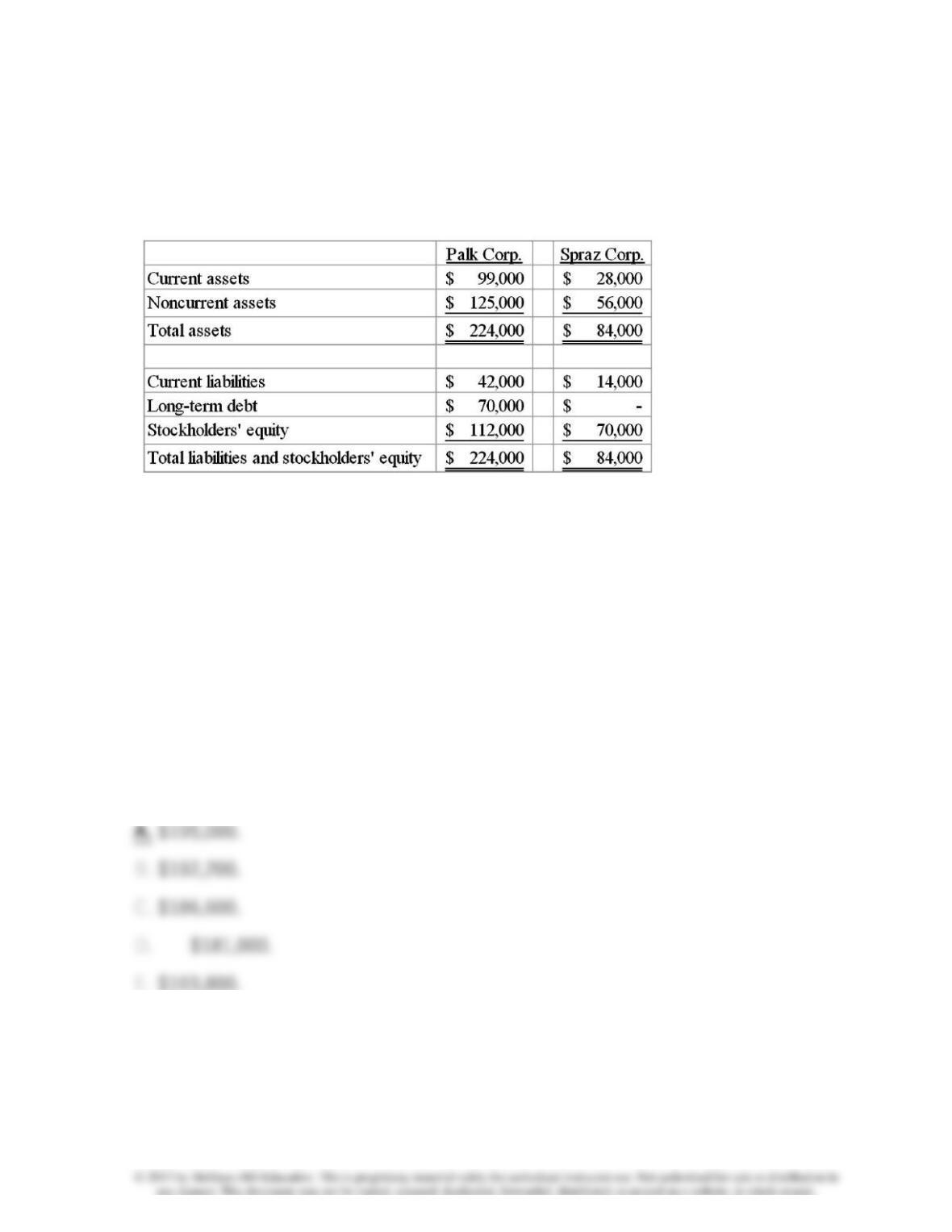

25. On January 1, 2010, Palk Corp. and Spraz Corp. had condensed balance

sheets as follows:

On January 2, 2010, Palk borrowed the entire $84,000 it needed to acquire 80% of

the outstanding common shares of Spraz. The loan was to be paid in ten equal

annual principal payments, plus interest, beginning December 31, 2010. The

excess consideration transferred over the underlying book value of the acquired

net assets was allocated 60% to inventory and 40% to goodwill.

What is

consolidated noncurrent assets

at January 2, 2010?

26. On January 1, 2010, Palk Corp. and Spraz Corp. had condensed balance

sheets as follows:

On January 2, 2010, Palk borrowed the entire $84,000 it needed to acquire 80% of

the outstanding common shares of Spraz. The loan was to be paid in ten equal

annual principal payments, plus interest, beginning December 31, 2010. The

excess consideration transferred over the underlying book value of the acquired

net assets was allocated 60% to inventory and 40% to goodwill.

What are the total

consolidated current liabilities

at January 2, 2010?

27. On January 1, 2010, Palk Corp. and Spraz Corp. had condensed balance

sheets as follows:

On January 2, 2010, Palk borrowed the entire $84,000 it needed to acquire 80% of

the outstanding common shares of Spraz. The loan was to be paid in ten equal

annual principal payments, plus interest, beginning December 31, 2010. The

excess consideration transferred over the underlying book value of the acquired

net assets was allocated 60% to inventory and 40% to goodwill.

What is

consolidated stockholders’ equity

at January 2, 2010?

28. In measuring non-controlling interest at the date of acquisition, which of

the following would

not

be indicative of the value attributed to the non-controlling

interest?

29. When a parent uses the equity method throughout the year to account for

its investment in an acquired subsidiary, which of the following statements is

false

before making adjustments on the consolidated worksheet?

30. When a parent uses the initial value method throughout the year to

account for its investment in an acquired subsidiary, which of the following

statements is

true

before making adjustments on the consolidated worksheet?

31. When a parent uses the partial equity method throughout the year to

account for its investment in an acquired subsidiary, which of the following

statements is

false

before making adjustments on the consolidated worksheet?

32. In a step acquisition, which of the following statements is

false

?

33. Which of the following statements is

false

regarding multiple acquisitions

of a subsidiary’s existing common stock?

34. When a subsidiary is acquired sometime after the first day of the fiscal

year, which of the following statements is true?

35. When consolidating a subsidiary that was acquired on a date other than

the first day of the fiscal year, which of the following statements is

true

in the

presentation of consolidated financial statements?

36. When a parent uses the acquisition method for business combinations and

sells shares of its subsidiary, which of the following statements is

false

?

37. All of the following statements regarding the sale of subsidiary shares are

true except which of the following?

38. Which of the following statements is true regarding the sale of subsidiary

shares when using the acquisition method for accounting for business

combinations?

39. Jax Company uses the acquisition method for accounting for its investment

in Saxton Company. Jax sells some of its shares of Saxton such that neither

control nor significant influence exists. Which of the following statements is

true

?

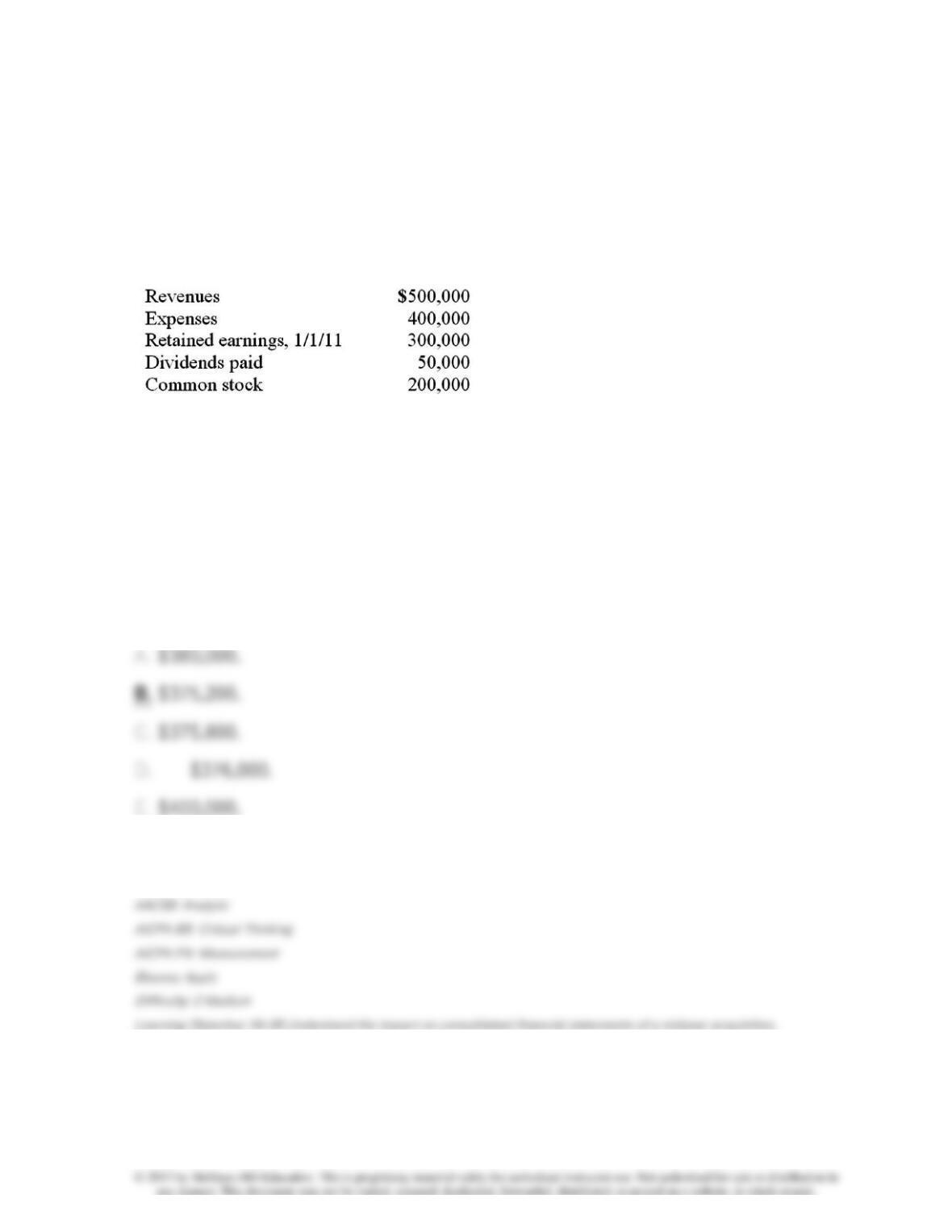

40. Keefe, Inc., a calendar-year corporation, acquires 70% of George Company

on September 1, 2010, and an additional 10% on January 1, 2011.

Total

annual

amortization of $6,000 relates to the first acquisition. George reports the following

figures for 2011:

Without regard for this investment, Keefe independently earns $300,000 in net

income during 2011.

All net income is earned evenly throughout the year.

What is the controlling interest in consolidated net income for 2011?

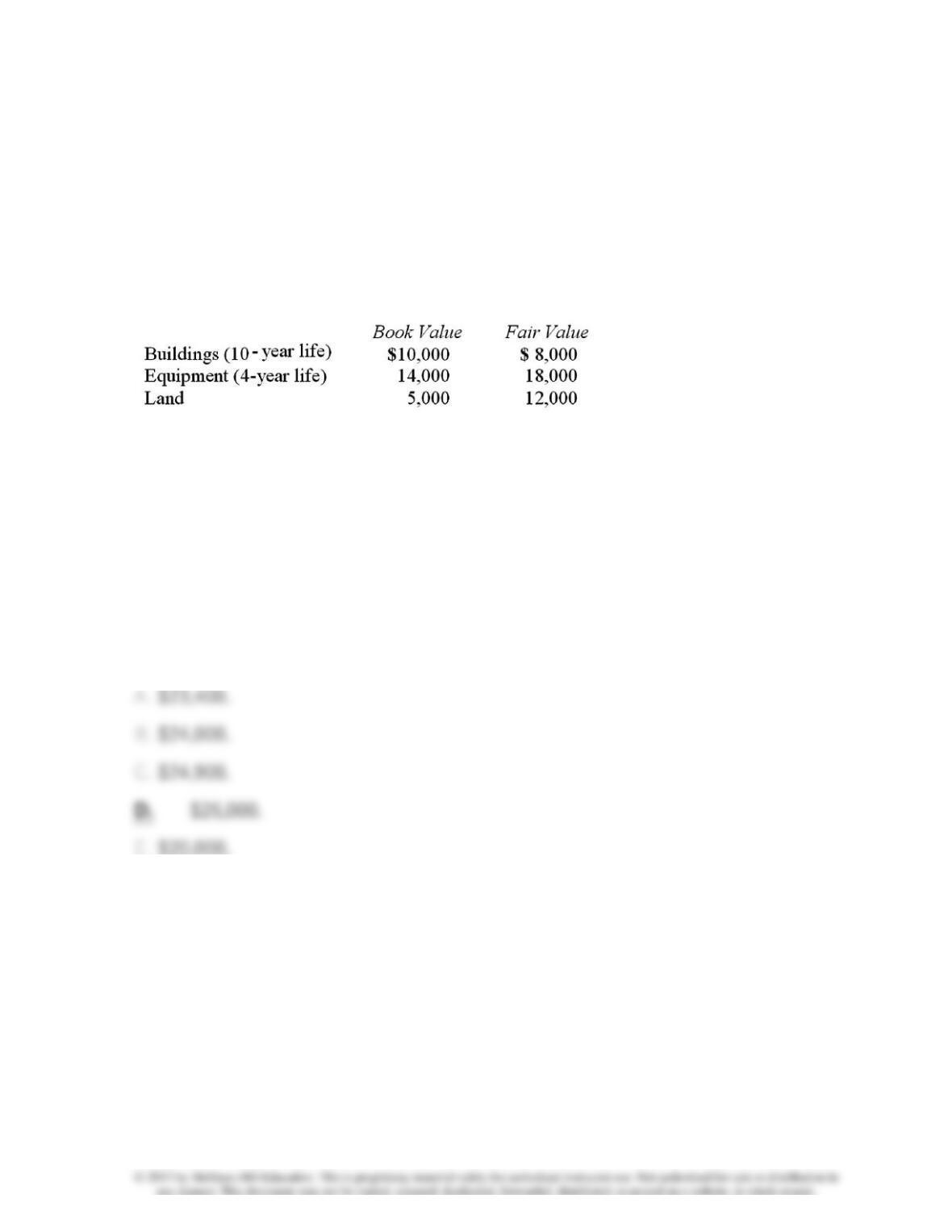

41. McGuire Company acquired 90 percent of Hogan Company on January 1,

2010, for $234,000 cash. This amount is reflective of Hogan’s total fair value.

Hogan’s stockholders’ equity consisted of common stock of $160,000 and

retained earnings of $80,000. An analysis of Hogan’s net assets revealed the

following:

Any excess consideration transferred over fair value is attributable to an

unamortized patent with a useful life of 5 years.

The acquisition value attributable to the non-controlling interest at January 1,

2010 is: