Chapter 3

107. Under the balance sheet classification of property, plant, and equipment, some accounts need adjustment and others

do not. Which do and why? Which do not and why?

108. Why is a physical count of supplies necessary at the end of the accounting period?

Chapter 3

Moderate

Subjective Short Answer

False

SACC.WARR.18.3-3 – LO: 03.03

United States – BUSPROG: Analytic

Bloom’s: Understanding

7/19/2016 9:45 AM

7/19/2016 9:45 AM

JFND-GO3A-EW4R-GPND

4OTI-GO4W-NQNBEE

109. Identify the classification of following items as:

a.

accrued asset

b.

unearned revenue

c.

accrued liability

d.

prepaid expense

(1)

Three months’ interest on notes payable paid in advance

(2)

Subscription fees for six months received in advance

(3)

Services rendered but not yet billed at month-end

(4)

Interest payable accrued on an accounts payable, but not yet paid

(5)

Salaries payable owed but not yet paid

(6)

Two year’s premium on building paid in advance

(1)

(2)

(3)

a

(4)

c

(5)

c

(6)

Moderate

Subjective Short Answer

False

SACC.WARR.18.3-3 – LO: 03.03

United States – BUSPROG: Analytic

Chapter 3

110. Identify the type of adjustment necessary (the type of item involved) and record the transaction for the event. Make

sure to include the ending balances after adjustment.

Assume that on June 1, 2016, Carter Lights Corp. had paid $1,800 in advance for a 6-month insurance policy. The June 30

adjustment is:

Adjustment

End. Bal.

Moderate

Subjective Short Answer

False

SACC.WARR.18.3-3 – LO: 03.03

United States – BUSPROG: Analytic

Bloom’s: Applying

7/19/2016 9:45 AM

Assets =

Liabilities + Stockholders’ Equity

Cash

Prepaid

Insurance

Office

Equipment

Accounts

Payable

Common

Stock

Retained

Earnings

Beg. Bal.

−1,800

1,800

Adjustment

End. Bal.

Bloom’s: Applying

7/19/2016 9:45 AM

10/18/2016 4:45 AM

JFND-GO3A-EW4R-GPBU

Chapter 3

111. Identify the type of adjustment necessary (the type of item involved) and record the transaction for the event. Make

sure to include the ending balances after adjustment.

Assume that on June 1, 2016, Tasty Sausage Corp. has a balance of $100 for supplies. On June 6 it purchased $600 in

supplies for cash. On June 30, at the end of the accounting period, there are $300 of supplies on hand. The June 30

adjustment is:

Beg. Bal.

End. Bal.

Subjective Short Answer

SACC.WARR.18.3-3 – LO: 03.03

United States – BUSPROG: Analytic

United States – DISC: – ACBSP: APC–07 – Adjusting Entries

Bloom’s: Applying

7/19/2016 9:45 AM

11/2/2016 2:32 AM

Assets =

Liabilities + Stockholders’ Equity

Cash

Supplies

Office

Equipment

Accounts

Payable

Common

Stock

Retained

Earnings

Beg. Bal.

−100

100

Supplies

purchased

−600

600

End. Bal.

−700

700

112. Identify the type of adjustment necessary (the type of item involved) and record the transaction for the event. Make

sure to include the ending balances after adjustment.

11/2/2016 2:29 AM

Chapter 3

Assume that on June 1, 2016, Tasty Sausage Corp. received $9,000 in advance to provide sausages over the next three

months. The June 30 adjustment is:

Revenue

Beg. Bal.

Adjustment

End. Bal.

Assets =

Liabilities + Stockholder’s Equity

Cash

Office

Equipment

Accumulated

Depreciation

Unearned

Revenue

Common

Stock

Retained

Earnings

Beg. Bal.

9,000

9,000

Adjustment

End. Bal.

113. Identify the type of adjustment necessary (the type of item involved) and record the transaction for the event. Make

sure to include the ending balances after adjustment.

Assume Mover Lights Corp. pays salaries on the 28th of each month. Light stuffers earn $280/day with a 7-day work

week. June 30th is the end of the accounting period. Light stuffers have worked on the 28th, 29th, and 30th but have not

yet been paid for those days. The June 30 adjustment is:

Assets =

Liabilities + Stockholders’ Equity

Cash

Office

Equipment

Accumulated

Depreciation

Salaries

Payable

Common

Stock

Retained

Earnings

Chapter 3

Adjustment

End. Bal.

114. Identify the type of adjustment necessary (the type of item involved) and record the transaction for the event. Make

sure to include the ending balances after adjustment.

On June 1, Carter Lights Corp. borrowed $38,000 from the bank by signing a promissory note from the bank, with 7%

interest. The note is due in three months. Interest for June has been incurred but not yet recorded. The interest to accrue

for June is $180. The June 30 adjustment is:

Assets =

Liabilities + Stockholders’ Equity

Cash

Office

Equipment

Accumulated

Depreciation

Interest

Payable

Common

Stock

Retained

Earnings

Adjustment

End. Bal.

Chapter 3

115. At the end of the fiscal year, the following adjusting entries were omitted:

(a)

No adjusting entry was made to transfer the $3,000 of prepaid insurance from the

asset account to the expense account.

(b)

No adjusting entry was made to record accrued fees of $500 for services provided

to customers.

Assuming that financial statements are prepared before the errors are discovered, indicate the effect of each error,

considered individually, by inserting the dollar amount in the appropriate spaces. Insert “0” if the error does not affect the

item.

Error (a)

Error (b)

Overstated

Understated

Overstated

Understated

(1)

Assets at December 31

would be

$

$

$

$

(2)

Liabilities at Dec. 31

would be

$

$

$

$

(3)

Net income for the year

would be

$

$

$

$

(4)

Retained earnings at Dec.

31 would be

$

$

$

$

Understated

(2)

United States – DISC: – ACBSP: APC–07 – Adjusting Entries

Chapter 3

31 would be

Subjective Short Answer

SACC.WARR.18.3-3 – LO: 03.03

United States – BUSPROG: Analytic

Bloom’s: Applying

7/19/2016 9:45 AM

11/2/2016 4:09 AM

116. Assume the November transactions for Camindo Co. are as follows:

a.

Received cash of $60,000 from investors in exchange for common stock.

b.

Provided services of $16,300 on account.

c.

Purchased supplies on account $750.

d.

Received cash of $11,800 from clients for services previously billed.

e.

Received $6,250 for services provided from clients who paid cash.

f.

Paid $600 on account for supplies that had been purchased.

g.

Paid $3,380 for a one-year insurance policy.

h.

Paid the following expenses: wages, $7,800; utilities, $1,000; rent, $3,750.

i.

Paid dividends of $2,300 to stockholders.

Record the transactions, using the integrated financial statement framework that follows:

Assets =

Liabilities + Stockholders’ Equity

Cash

Accounts

Receivable

Supplies

Prepaid

Insurance

Accounts

Payable

Common

Stock

Retained

Earnings

a.

b.

c.

d.

e.

f.

g.

h.

Chapter 3

i.

Bal.

Calculate the November 30 cash balance and the amount of net income for November for Hoover Co.

Bal.

Financing

Operating

Operating

Expenses

Operating

Operating

Operating

Financing

Challenging

False

JFND-GO3A-EW4R-GPBA

Chapter 3

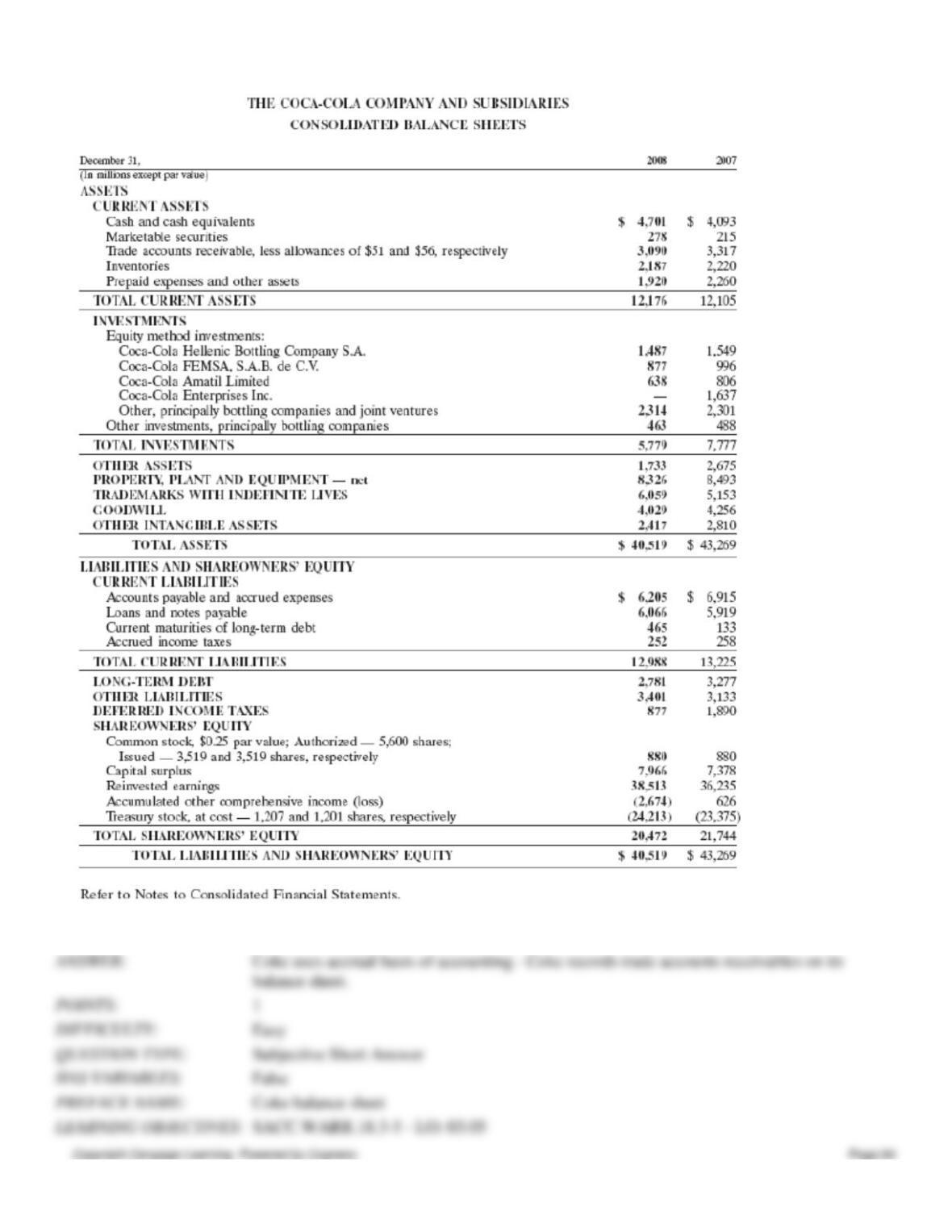

117. Refer to Coke’s balance sheet. Does it appear that Coke uses the cash or accrual basis of accounting?

Chapter 3

118. When are sales recognized under the cash basis of accounting? When are expenses recognized?

119. Describe the differences between the cash and accrual bases of accounting.

Chapter 3

120. BlueInk Corporation’s accumulated depreciation increased by $14,000, while patents decreased by $3,875 between

consecutive balance sheet dates. There were no purchases or sales of depreciable or intangible assets during the year. In

addition, the income statement showed a loss on sale of land of $1,950. Accounts receivable increased $6,320, inventory

decreased $3,125, prepaid expenses decreased $720, and account payable increased $2,760. Reconcile a net income of

$55,000 to net cash flow from operating activities.

Chapter 3

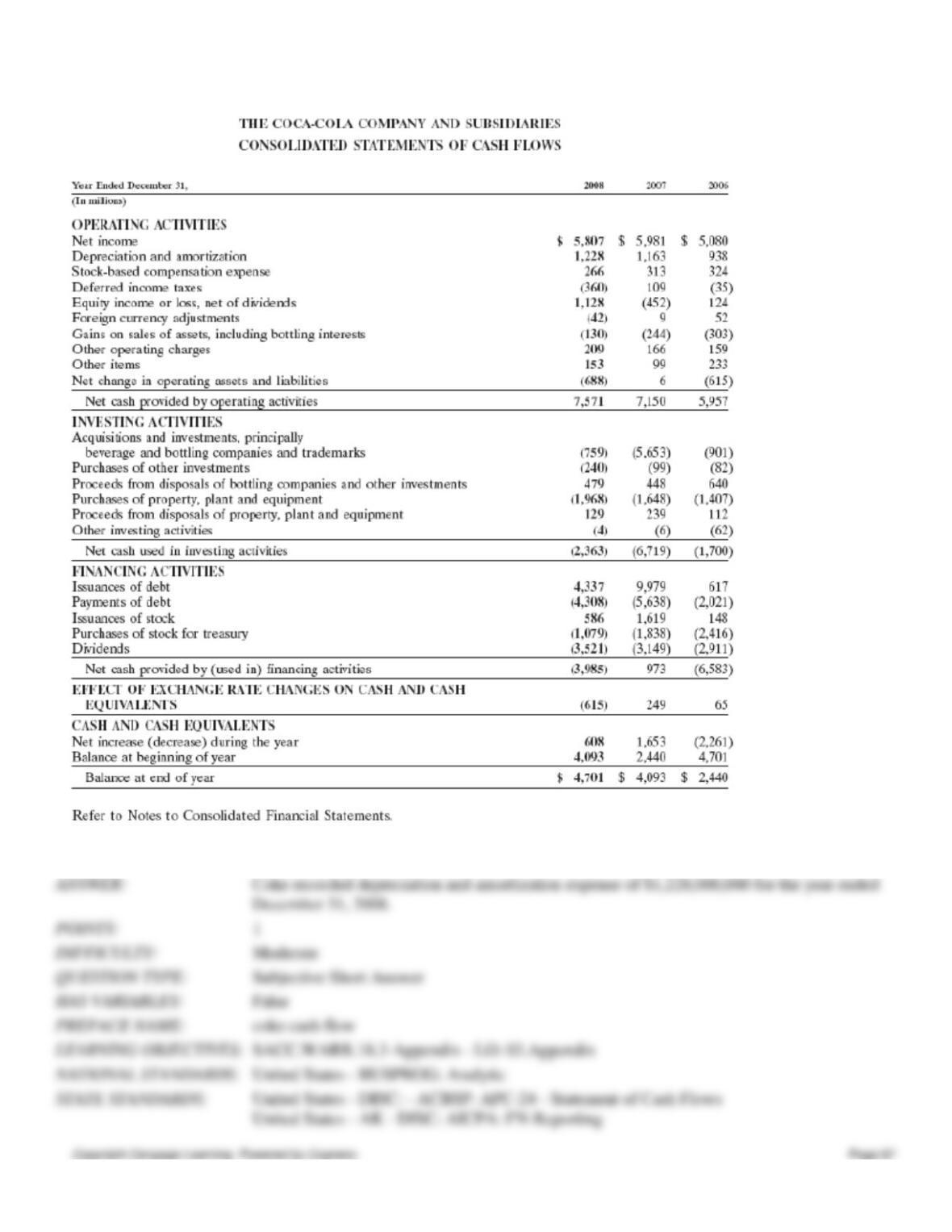

121. Refer to Coke’s Statement of Cash Flows. What amount of depreciation and amortization did Coke record in 2008?

Chapter 3

122. Electroyo Corporation’s accumulated depreciation increased by $8,500, while patents decreased by $2,800 between

consecutive balance sheet dates. There were no purchases or sales of depreciable or intangible assets during the year. In

addition, the income statement showed a gain of $5,350 from sale of land. Reconcile a net income of $68,000 to net cash

flow from operating activities.