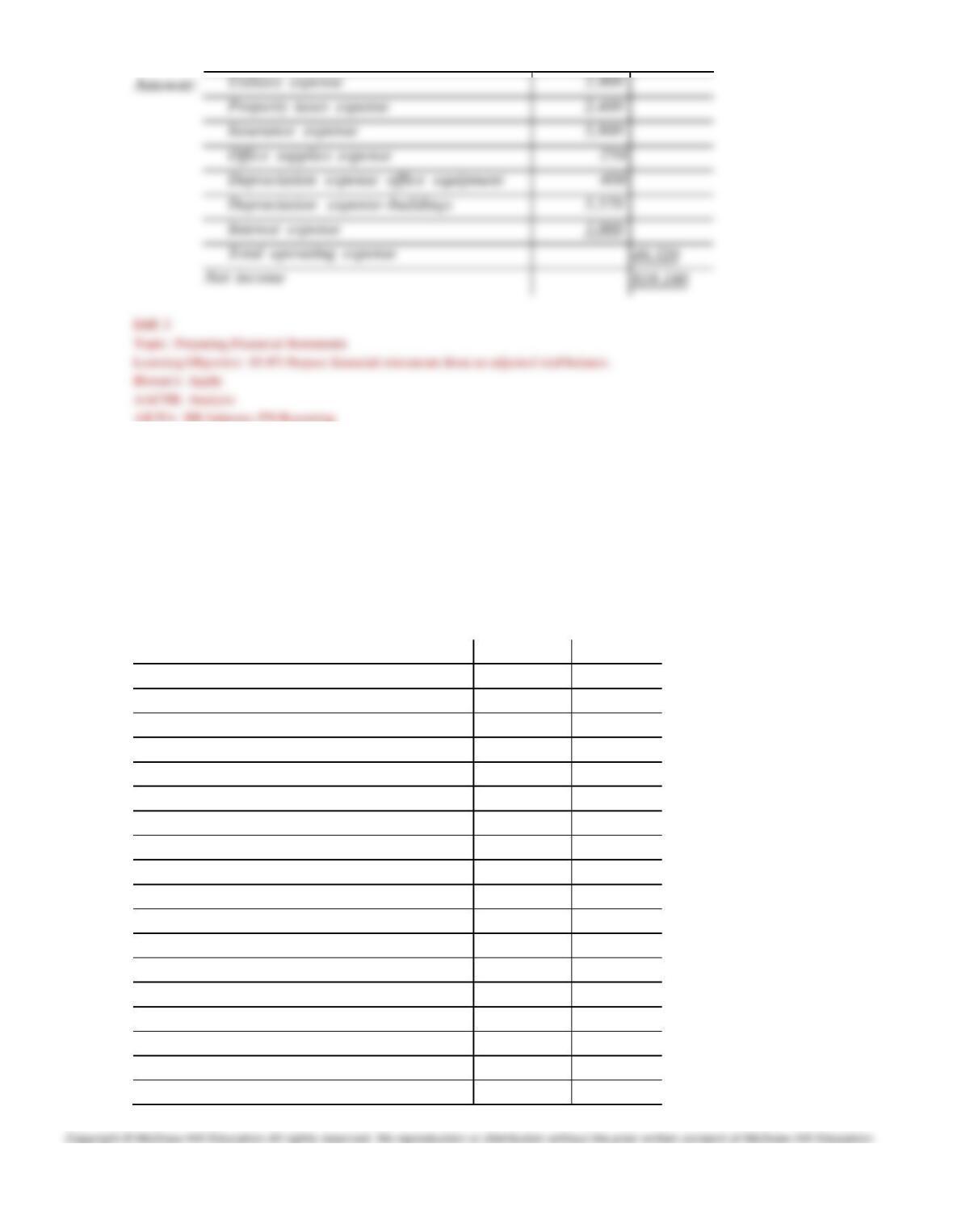

226)

Using the information presented below, prepare a statement of owner’s equity and balance sheet

from the adjusted trial balance of Dodson Containers. Mr. Dodson’s capital account balance of

$40,340 consists of a $30,340 beginning-year balance plus a $10,000 investment during the current

year.

DODSON CONTAINERS

Adjusted Trial Balance

December 31

Cash

$ 3,050

Accounts receivable…

400

Prepaid insurance ..

830

Office supplies ….....…..

80

Office equipment …

4,200

Accumulated depreciation–office equipment

$ 1,100

Buildings…………..

98,000

Accumulated depreciation–buildings..

28,000

Land….

115,000

Wages Payable………

880

Property taxes payable

1,400

Interest payable…..

2,200

Unearned rent…….

460

Long–term notes payable…………….

150,000

Frank Dodson, Capital .

40,340

Frank Dodson, Withdrawals

21,000

Rent earned ………

67,500

Wages expense …..

29,000

Utilities expense … 1

19 2,900

Utilities expense …

2,900

Property taxes expense ……………..

2,400

Insurance expense..

5,800

Office supplies expense

250

Depreciation expense–office equipment

400

Depreciation expense–buildings……..

5,570

Interest expense …

3,000

$291,880

________

$291,880

Totals …………….

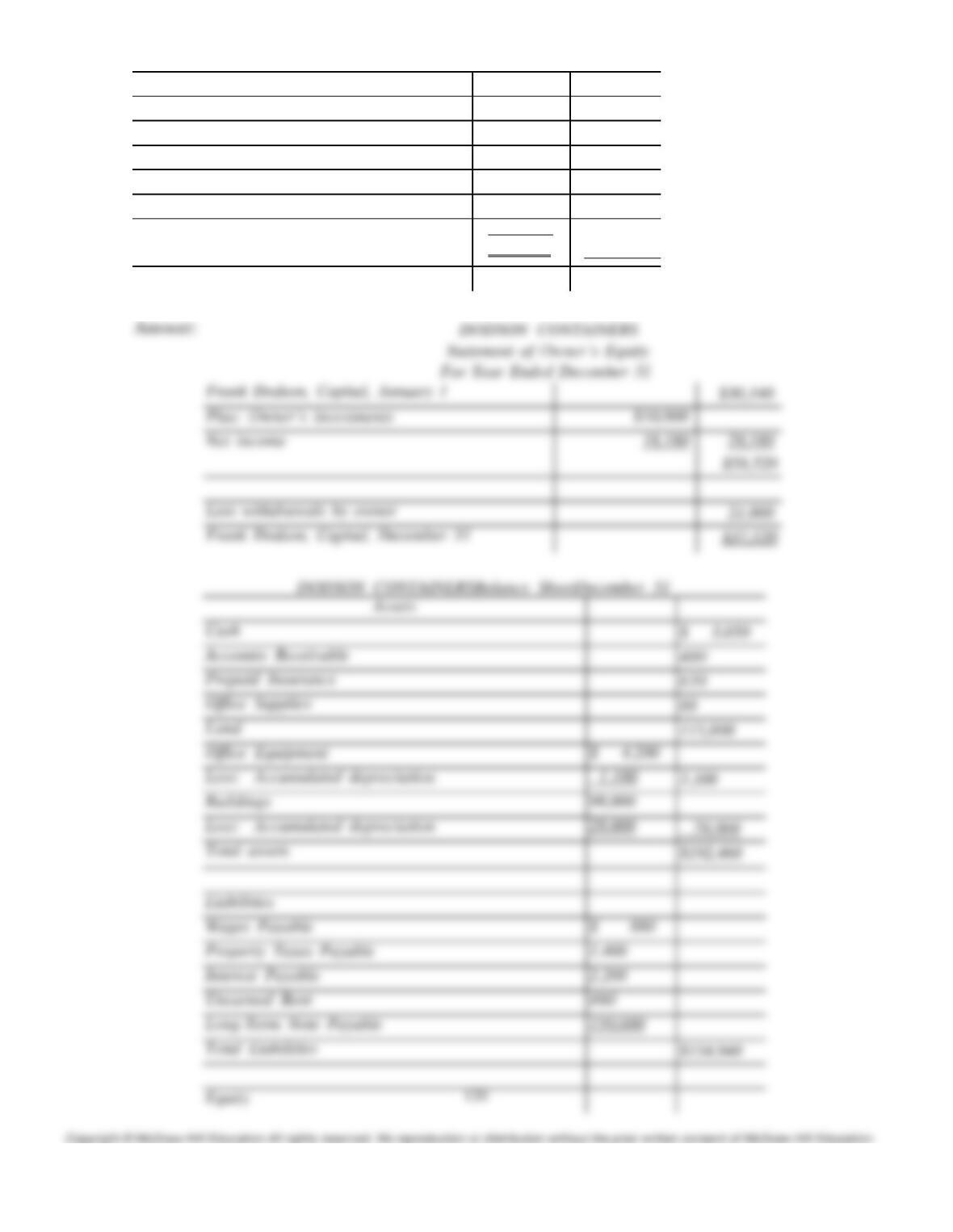

227)

Using the information given below, prepare an income statement and owner’s equity statement for

Rapid Car Services from the adjusted trial balance. Owner Stella Grafton did not make any

additional investments in the company during the year.

Rapid Car Services

Adjusted Trial Balance

For the year ended December 31

Cash

$ 33,000

Accounts receivable

14,200

Office supplies

1,700

Vehicles

100,000

Accumulated depreciation — Vehicles

45,000

Accounts payable

11,500

Stella Grafton, Capital

71,900

Stella Grafton, Withdrawals

40,000

Fees earned

155,000

Rent expense

13,000

Office supplies expense

2,000

Utilities expense

2,500

Depreciation Expense — Vehicles

15,000

Salary expense

50,000

Fuel expense

12,000

________

Totals

$283,400

$283,400

122

228)

Using the information given below, prepare a balance sheet for Rapid Car Services from the adjusted

trial balance. Owner Stella Grafton did not make any additional investments in the company during

the year.

Rapid Car Services

Adjusted Trial Balance

For the year ended December 31

Cash

$ 33,000

Accounts receivable

14,200

Office supplies

1,700

Vehicles

100,000

Accumulated depreciation — Vehicles

45,000

Accounts payable

11,500

Stella Grafton, Capital

71,900

Stella Grafton, Withdrawals

40,000

Fees earned

155,000

Rent expense

13,000

Office supplies expense

2,000

Utilities expense

2,500

Depreciation Expense — Vehicles

15,000

Salary expense

50,000

Fuel expense

12,000

________

Totals $283,400 $283,400

229)

Abdulla, Co. collected 6-months’ rent in advance from a tenant on October 1 of the current year.

When it collected the cash, it recorded the following entry:

Oct. 01 Cash 15,000

Rent Revenue Earned 15,000

Assuming Abdulla only prepares adjustments at year-end, prepare the required adjusting entry at

December 31 of the current year.

230)

On November 1 of the current year, Salinger Company paid $9,600 cash for a one-year insurance

policy that took effect on that day. On the date of the payment, Salinger recorded the following entry:

Nov. 01 Insurance Expense 9,600

Cash 9,600

Assuming Salinger only prepares adjustments at year-end, prepare the required adjusting entry at

December 31 of the current year.

231)

Carroll Co. is a multi-million dollar business. The business results for the year have been impacted

significantly by a slowing economy. The company wants to increase its net income. It has incurred

$2,900,000 in unpaid salaries at the end of the year and wants to leave those amounts unrecorded at

the end of the year. (a) How would this omission affect the financial statements of Carroll? (b)

Which accrual basis of accounting principles does this omission violate? (c) Would this be

considered an ethical problem?

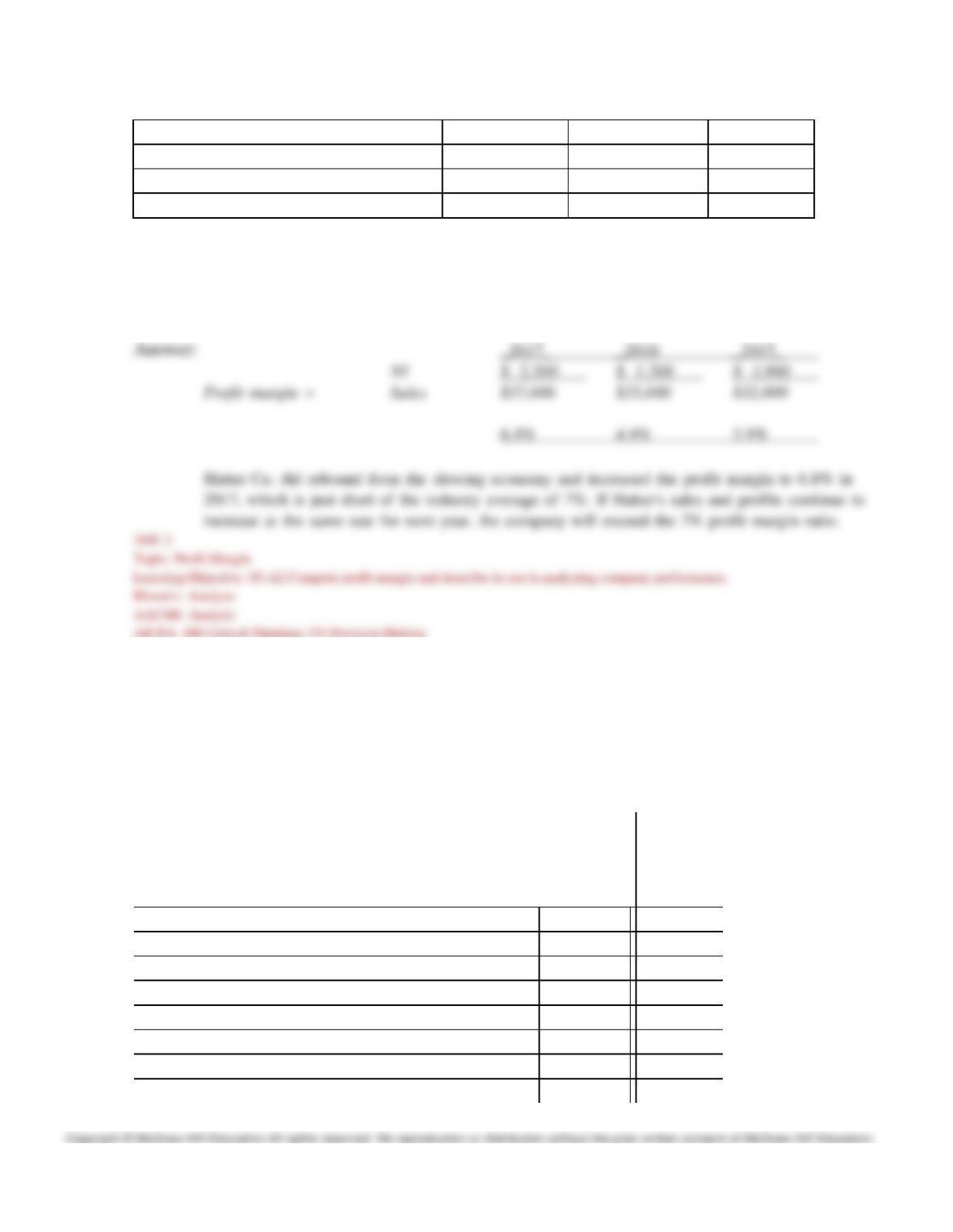

232)

The following information is available for Hatter Co.

2017

2016

2015

Net income

2,500

1,700

1,900

Net sales

37,000

35,000

32,000

Total assets

420,000

395,000

375,000

From the information provided, calculate Hatter’s profit margin ratio for each of the three years. In

2016, economic conditions and a slowing economy impacted the results of operations. Comment on

the results, assuming that the industry average for the profit margin ratio is 7% for each of the three

years.

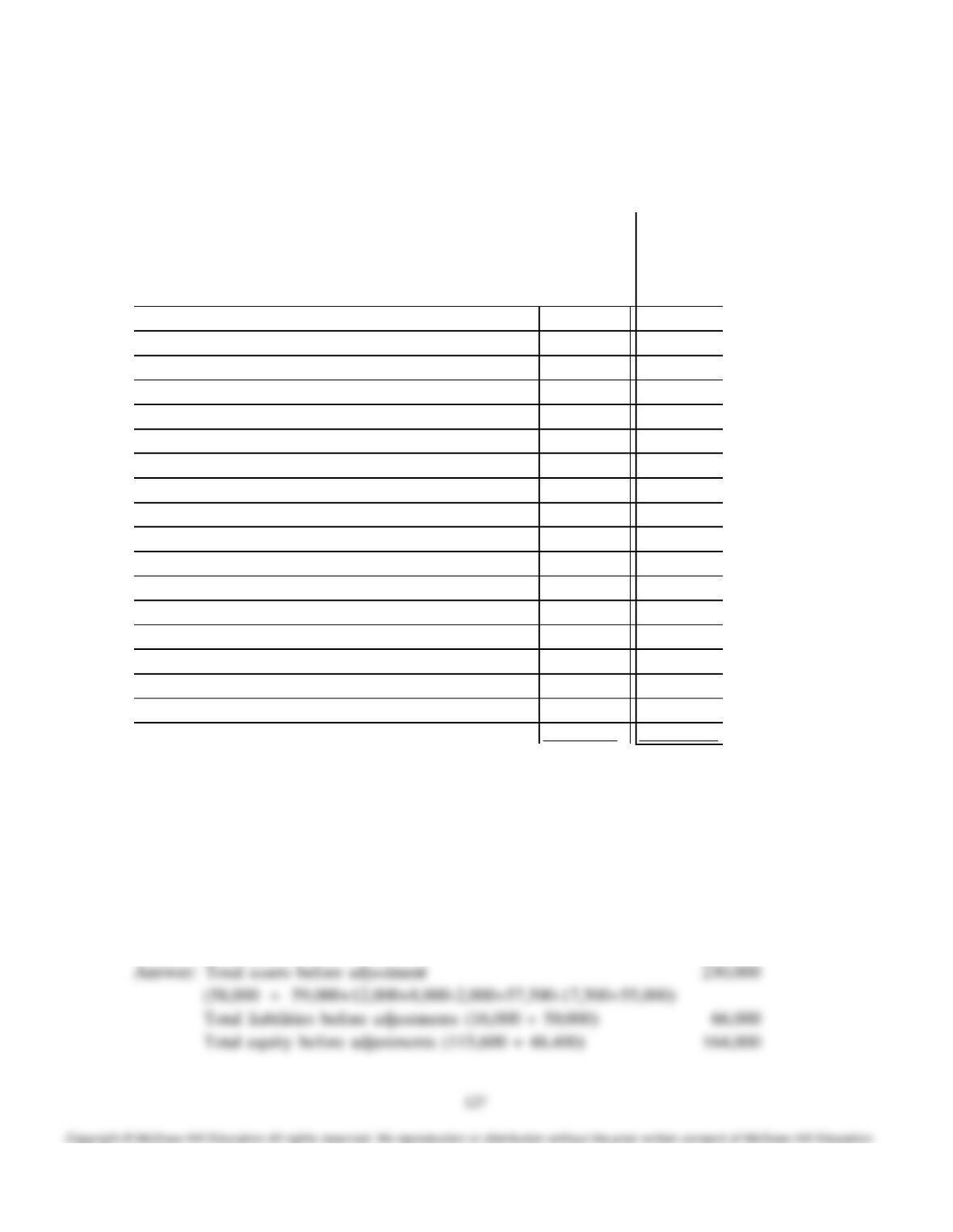

233)

The unadjusted trial balance and the adjustment data for Porter Business Institute are given below

along with adjusting entry information. What is the impact on net income if these adjustments are

not recorded? Show the calculation for net income without the adjustments and net income with

the adjustments. Which one gives the most accurate net income? Which accounting principles are

being violated if the adjustments are not made?

Porter Business Institute

Unadjusted Trial Balance

December 31

(in millions)

Cash………

$ 58,000

Accounts receivable…………..

59,000

Prepaid insurance ……………

12,000

Equipment …

8,000

Accumulated depreciation–equipment ………..

$ 2,000

Buildings……

57,500

Accumulated depreciation–buildings…………..

17,500

Land 125

55,000

Land

55,000

Unearned rent.

16,000

Long-term notes payable……….

50,000

Porter, Capital .

115,600

Tuition fees earned ……….

74,000

Training fees earned …….

23,400

Wages expense ……………

32,000

Utilities expense ………….

8,000

Property taxes expense ……

5,000

Interest expense ……………

4,000

________

Totals …….

$ 298,500

$298,500

Additional information items:

a. The Prepaid Insurance account consists of a payment for a 1 year policy. An analysis of the

insurance invoice indicates that one half of the policy has expired by the end of the December 31

year-end.

b. A cash payment for space sublet for 8 months was received on July 1 and was credited to

Unearned Rent.

c. Accrued interest expense on the note payable of $1,000 has been incurred but not paid.

234)

The unadjusted trial balance and the adjustment data for Porter Business Institute are shown below

along with adjusting entry information. What is the impact of the adjusting entries on the balance

sheet? Show the calculation for total assets, total liabilities, and owner’s equity without the

adjustments; show the calculation for total assets, total liabilities, and owner’s equity with the

adjustments. Which one provides the most accurate presentation of the balance sheet?

Porter Business Institute

Unadjusted Trial Balance

December 31

(in millions)

Cash………

$ 58,000

Accounts receivable…………..

59,000

Prepaid insurance ……………

12,000

Equipment …

8,000

Accumulated depreciation–equipment ………..

$ 2,000

Buildings……

57,500

Accumulated depreciation–buildings…………..

17,500

Land

55,000

Unearned rent.

16,000

Long-term notes payable……….

50,000

Porter, Capital .

115,600

Tuition fees earned ……….

74,000

Training fees earned …….

23,400

Wages expense ……………

32,000

Utilities expense ………….

8,000

Property taxes expense ……

5,000

Interest expense ……………

4,000

________

Totals …….

$ 298,500

$298,500

Additional information items:

a. The Prepaid Insurance account consists of a payment for a 1 year policy. An analysis of the

insurance invoice indicates that one half of the policy has expired by the end of the December 31

year-end.

b. A cash payment for space sublet for 8 months was received on July 1 and was credited to

Unearned Rent.

c. Accrued interest expense on the note payable of $1,000 has been incurred but not paid.

235)

Using the selected information given below for Luk Company, calculate the return on assets, debt

ratio, and profit margin. Comment on the results of operations and the financial position of the

company for the year.

Sales

1,050,000

Expenses

795,000

Assets (beginning of the year)

1,500,000

Assets (end of the year)

1,900,000

Liabilities

850,000

Nov. 1

Paid $11,400 for 12 months of insurance coverage through October 31 of next

year.

5

Received $8,000 cash for future services to be provided to a customer.

7

Paid $10,000 for future advertising.

Dec. 31

A portion of the insurance paid for on November 1 has expired. No adjustment

was made in November to the insurance account.

31

Services of $2,500 are not yet provided to the customer who paid on November

236)

Prepare adjusting entries for the year ended December 31, for each of these separate situations.

Assume that prepaid expenses are initially recorded in asset accounts and that fees collected in

advance are initially recorded as liabilities.

a. The Prepaid Rent account has a debit balance of $8,000 before adjustment, representing a

prepayment for four months’ rent made on December 1 of the current year.

b. One-third of the work related to $18,000 of cash received in advance was performed during this

period.

c. Unpaid accrued salaries at December 31 amounts to $15,000

d. Work was completed for a client on December 31 in the amount of $21,000, but was not

previously billed or recorded.

e. Estimated depreciation on office equipment is $27,000.

237)

Gracio Co. had the following transactions in the last two months of its year ended December 31.

Prepare entries for these transactions under the method that records prepaid expenses as expenses

and records unearned revenues as revenues. Also prepare adjusting entries at the end of the year.

130

31

Services of $2,500 are not yet provided to the customer who paid on November

5.

31

Of the advertising paid for on November 7, $1,500 is not yet used.

238)

For each of the following two separate situations, present both the April 30 adjusting entry and the

subsequent entry during May to record the payment of the accrued expenses or receipt of the accrued

revenue. Assume the company does not prepare reversing entries.

a. Nicolas Company has 5 employees, who earn a total of $2,900 in salaries each working day. They

are paid on Monday for the five-day workweek ending on the previous Friday. Assume that fiscal

year ended April 30, is a Thursday and all employees worked each day and will be paid salaries for

five full days on the following Monday.

b. Services of $3,000 have been performed for Clevenger Company through April 30. The client will

pay the entire amount of the contract when services are completed on May 23.

c. Paid the employees’ salaries on May 4.

d. Received payment from Clevenger Company for services that are now completed on May 23.

SHORT ANSWER QUESTIONS

239)

Companies experiencing seasonal variations in sales often choose a fiscal year corresponding to

their ________ year.

240)

________ are required at the end of the accounting period because certain internal transactions and

events remain unrecorded.

241)

Accrual accounting and the adjusting process rely on two principles: the ________ principle and

the ________ principle.

242)

________ basis accounting means that revenues are recognized when cash is received and that

expenses are recorded when cash is paid. ________ basis accounting means that the financial

effects of revenues and expenses are recorded when earned or incurred.

243) Adjusting is a three-step process (1) ________, (2) ________, and (3) ________.

244)

________ refer to costs incurred in a period that are both unpaid and unrecorded. ________ refer to

revenues earned in a period that are both unrecorded and not yet received in cash (or other assets).

245)

Accrued revenues at the end of one accounting period often result in cash ________ in the next

period.

246)

________ revenues are liabilities requiring delivery of products and for services.

247)

If a prepaid expense account were not adjusted for the amount used, on the balance sheet assets

would be ________ and equity would be ________.

248)

Profit margin = divided by net sales.

249)

The ________ depreciation method allocates equal amounts of an asset’s cost to depreciation

during its useful life.

250)

is the process of allocating the cost of plant assets to the income statement over their

expected useful lives.

251)

A ________ account is an account linked with another account, having an opposite normal

balance, and reported as a subtraction from that other account’s balance.

252)

________ expenses are those costs that are incurred in a period but are both unpaid and

unrecorded.

253)

An is a listing of all of the accounts in the ledger with their account balances before

adjustments are made.

254)

An is a listing of all of the accounts in the ledger with their account balances after

adjustments are made.