Name:

Class:

Date:

chapter 3

Indicate whether the statement is true or false.

1. If the debit portion of an adjusting entry is to an asset account, then the credit portion must be to a liability account.

a.

True

b.

False

2. A company pays $36,000 for 12 months’ rent on October 1, recording the prepayment as an asset. The adjusting entry

on December 31 is a debit to Rent Expense of $9,000, and a credit to Prepaid Rent of $9,000.

a.

True

b.

False

3. Adjusting journal entries are dated on the last day of the period.

a.

True

b.

False

4. A company receives $360 for a 12-month trade magazine subscription on August 1. The adjusting entry on December

31 is a debit to Unearned Subscription Revenue of $150 and a credit to Subscription Revenue of $150.

a.

True

b.

False

5. If the adjustment for accrued salaries at the end of the period is inadvertently omitted, both liabilities and stockholders’

equity will be understated for the period.

a.

True

b.

False

6. The adjustment for accrued fees was debited to Accounts Payable instead of Accounts Receivable. This error will be

detected when the adjusted trial balance is prepared.

a.

True

b.

False

7. The system of accounting where revenues are recorded when they are earned and expenses are recorded when they are

incurred is called the cash basis of accounting.

a.

True

b.

False

8. Generally accepted accounting principles require the accrual basis of accounting.

a.

True

b.

False

9. The revenue recognition principle states that revenue should be recorded in the same period as the cash is received.

a.

True

b.

False

10. When preparing an income statement vertical analysis, each revenue and expense is expressed as a percent of net

income.

a.

True

Name:

Class:

Date:

chapter 3

b.

False

11. An example of deferred revenue is Unearned Rent.

a.

True

b.

False

12. At year-end, the balance in the prepaid insurance account, prior to any adjustments, is $6,000. The amount of the

journal entry required to record insurance expense will be $4,000 if the amount of unexpired insurance applicable to

future periods is $2,000.

a.

True

b.

False

13. Accumulated depreciation accounts are liability accounts.

a.

True

b.

False

14. The adjusted trial balance verifies that total debits equal total credits before the adjusting entries are prepared.

a.

True

b.

False

15. If the adjustment of the unearned rent account at the end of the period to recognize the amount of rent earned is

inadvertently omitted, the net income for the period will be understated.

a.

True

b.

False

16. A fixed asset’s market value is reflected on the balance sheet.

a.

True

b.

False

17. An adjusting entry would adjust an expense account so the expense is reported when incurred.

a.

True

b.

False

18. Accruals are needed when an unrecorded expense has been incurred or an unrecorded revenue has been earned.

a.

True

b.

False

19. Revenues and expenses should be recorded in the same period to which they relate.

a.

True

b.

False

20. A company pays an employee $3,000 for a five-day workweek, Monday–Friday. The adjusting entry on December 31,

which is a Wednesday, is a debit to Wages Expense of $1,800, and a credit to Wages Payable of $1,800.

a.

True

b.

False

Name:

Class:

Date:

chapter 3

21. The matching principle requires expenses be recorded in the same period that the related revenue is recorded.

a.

True

b.

False

22. An adjusting entry would adjust revenue so it is reported when earned and not when cash is received.

a.

True

b.

False

23. By ignoring and not posting the adjusting journal entries to the appropriate accounts, net income will always be

overstated.

a.

True

b.

False

24. A contra asset account for Land will normally appear on the balance sheet.

a.

True

b.

False

25. Accumulated depreciation is reported on the income statement.

a.

True

b.

False

26. Depreciation Expense is reported on the balance sheet as an addition to the related asset.

a.

True

b.

False

27. Vertical analysis is useful for analyzing financial statement changes over time.

a.

True

b.

False

28. The revenue recognition principle requires that the reporting of revenue be included in the period when cash for the

service is received.

a.

True

b.

False

29. The financial statements are prepared from the unadjusted trial balance.

a.

True

b.

False

30. The systematic allocation of land’s cost to expense is called depreciation.

a.

True

b.

False

31. Unearned revenue is a liability.

a.

True

b.

False

Name:

Class:

Date:

chapter 3

32. An adjusting entry to accrue an incurred expense will affect total liabilities.

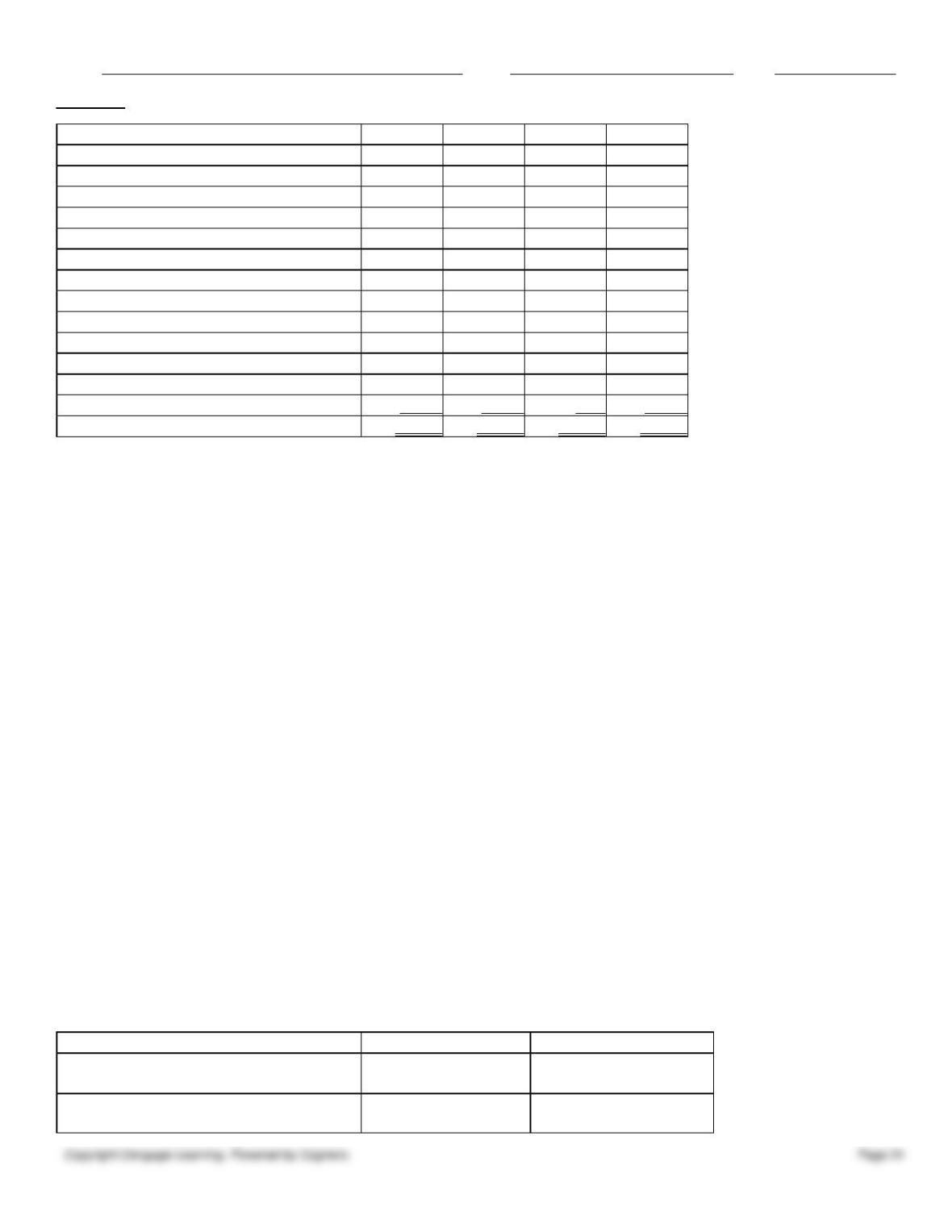

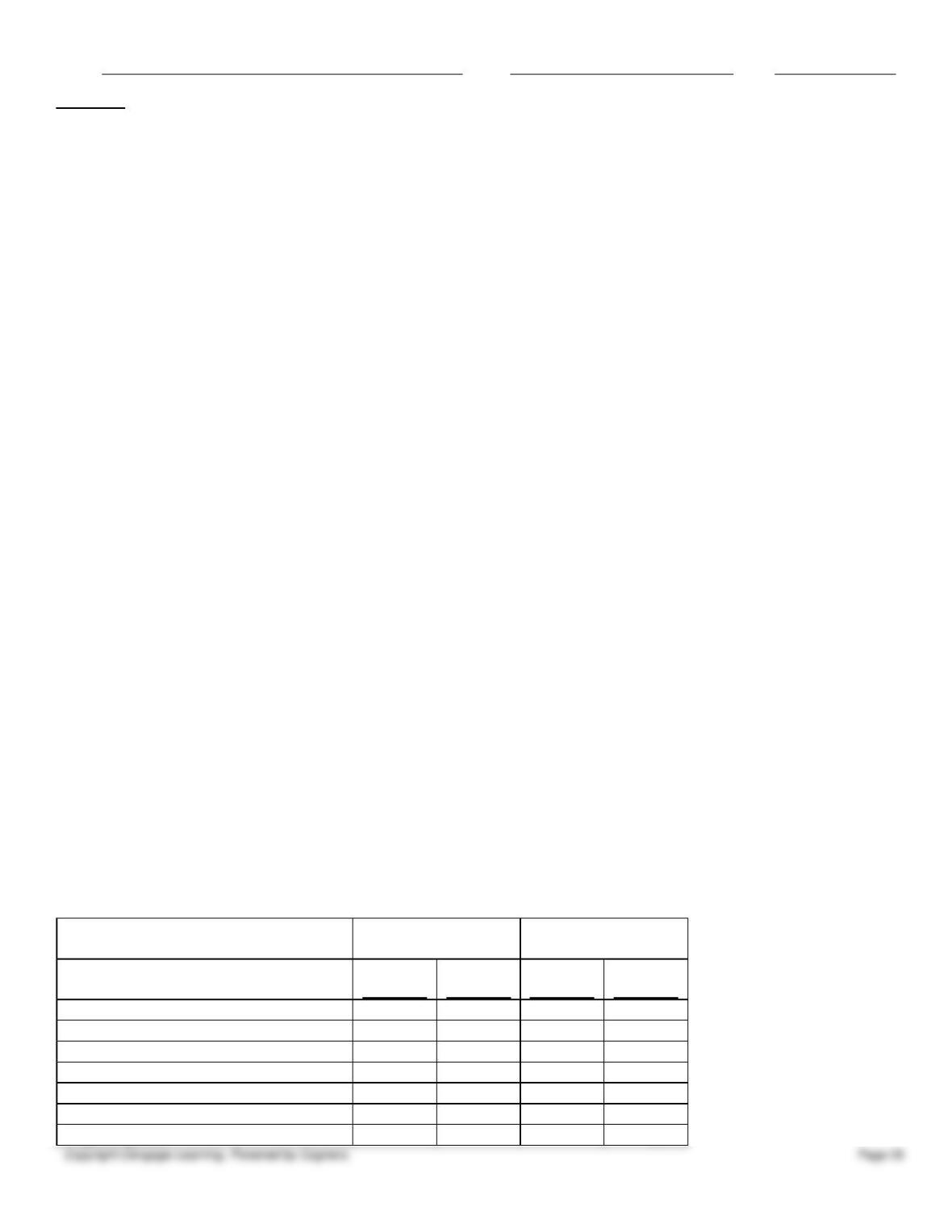

a.

True

b.

False

33. A company realizes that the last two days’ revenue for the month was billed but not recorded. The adjusting entry on

December 31 is a debit to Accounts Receivable and a credit to Fees Earned.

a.

True

b.

False

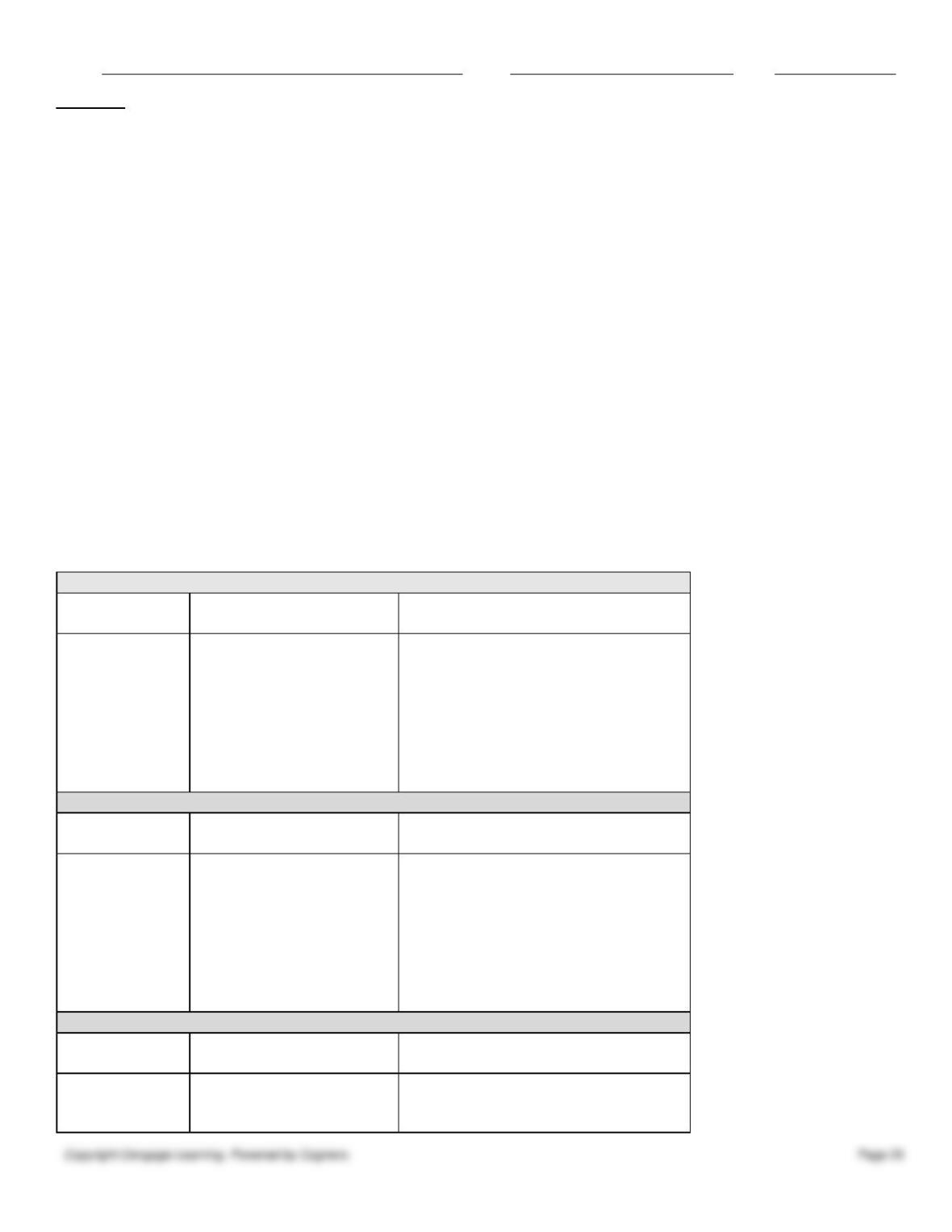

34. The updating of accounts when financial statements are prepared is called the adjusting process.

a.

True

b.

False

35. The matching principle supports matching expenses with the related revenues.

a.

True

b.

False

36. A company depreciates its equipment $500 a year. The adjusting entry on December 31 is a debit to Depreciation

Expense of $500 and a credit to Equipment of $500.

a.

True

b.

False

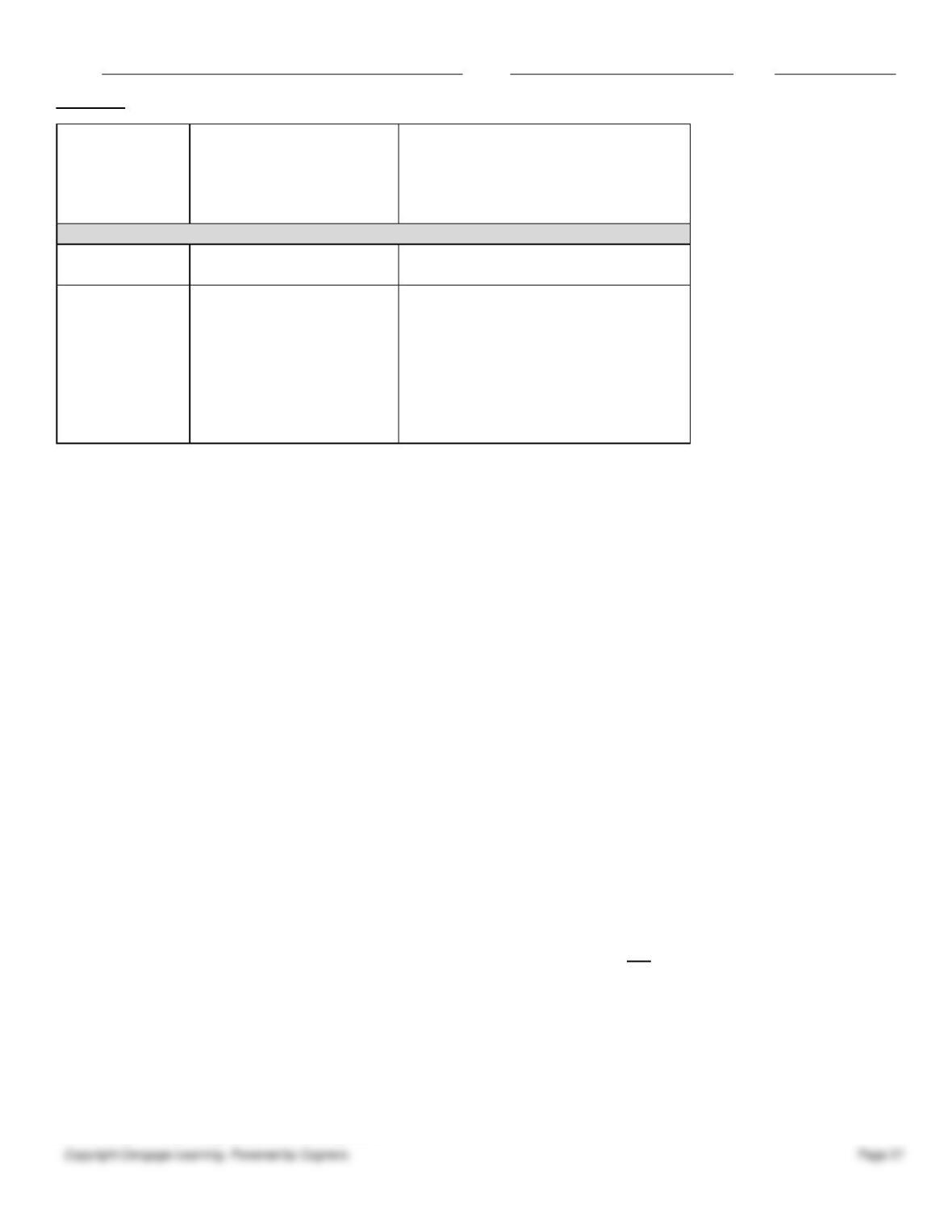

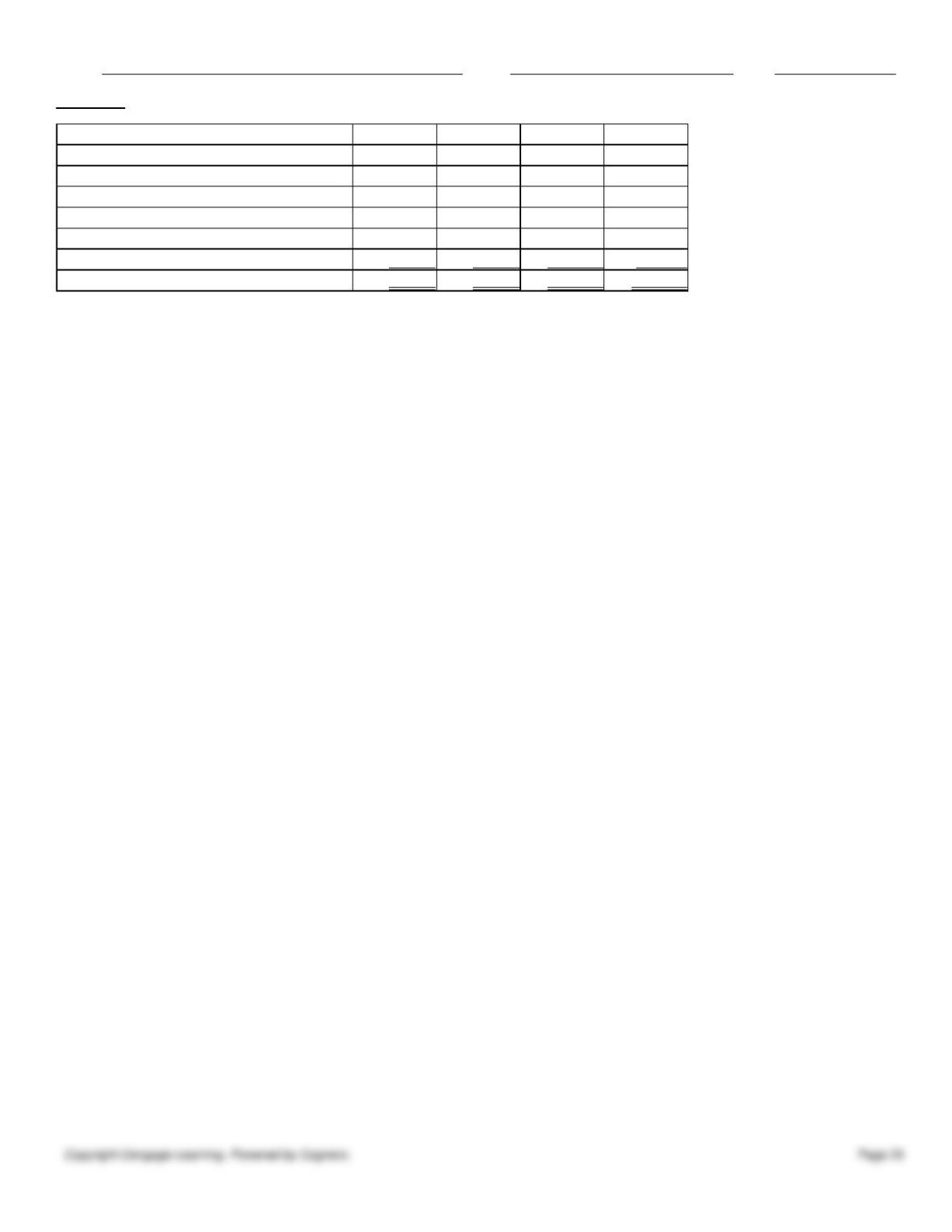

37. If the adjustment to recognize expired insurance at the end of the period is inadvertently omitted, the assets at the end

of the period will be understated.

a.

True

b.

False

38. The difference between the balance of a fixed asset account and the balance of its related accumulated depreciation

account is termed the book value of the asset.

a.

True

b.

False

39. Even though GAAP requires the accrual basis of accounting, some businesses prefer using the cash basis of

accounting.

a.

True

b.

False

40. The balance in the accumulated depreciation account is the sum of the depreciation expense recorded in past periods.

a.

True

b.

False

41. If the adjustment for depreciation for the year is inadvertently omitted, the assets on the balance sheet at the end of the

period will be understated.

a.

True

b.

False

42. For most large businesses, the cash basis of accounting will provide accurate financial statements for user needs.

Name:

Class:

Date:

chapter 3

a.

True

b.

False

43. The difference between deferred revenue and accrued revenue is that accrued revenue has been recorded and

needs adjusting and deferred revenue has never been recorded.

a.

True

b.

False

44. A company receives $6,500 for two season tickets sold on September 1. If $2,500 is earned by December 31, the

adjusting entry made at that time is a debit to Cash of $2,500, and a credit to Ticket Revenue of $2,500.

a.

True

b.

False

45. Adjusting entries affect balance sheet accounts to the exclusion of income statement accounts.

a.

True

b.

False

46. Adjustments for accruals are needed to record a revenue that has been earned or an expense that has been incurred but

not recorded.

a.

True

b.

False

47. Deferrals are recorded transactions that delay the recognition of an expense or revenue.

a.

True

b.

False

48. Vertical analysis compares each item in a financial statement with a total amount from the same statement.

a.

True

b.

False

49. Adjusting entries affect only expense and asset accounts.

a.

True

b.

False

Indicate the answer choice that best completes the statement or answers the question.

50. If the effect of the debit portion of an adjusting entry is to increase the balance of an expense account, which of the

following describes the effect of the credit portion of the entry?

a.

decreases the balance of an owner’s equity account

b.

increases the balance of a liability account

c.

increases the balance of an asset account

d.

decreases the balance of an expense account

51. The term used to describe an expense that has not been paid and has not yet been recognized in the accounts by a

routine entry is

a.

prepaid

Name:

Class:

Date:

chapter 3

b.

deferred

c.

accrued

d.

matched

52. Which of the following is not a characteristic of the accrual basis of accounting?

a.

Revenues and expenses are reported in the period in which cash is received or paid.

b.

Revenues are reported on the income statement in the period in which they are earned.

c.

The accrual basis of accounting supports the matching concept.

d.

Expenses are reported in the same period as the revenues to which they relate.

53. What effect will this adjustment have on the accounting records?

Unearned Fees

6,375

Fees Earned

6,375

a.

increase net income

b.

increase revenues reported for the period

c.

decrease liabilities

d.

All of these choices.

54. Fees payable would appear on the balance sheet as a(n)

a.

asset

b.

liability

c.

fixed asset

d.

unearned revenue

55. At the end of the fiscal year, the usual adjusting entry for depreciation on equipment was omitted. Which of the

following is true?

a.

Total assets will be understated at the end of the current year.

b.

The balance sheet and income statement will be misstated, but the statement of owner’s equity will be correct

for the current year.

c.

Net income will be overstated for the current year.

d.

Total liabilities and total assets will be understated.

56. Which of the following accounts would likely be included in an accrual adjusting entry?

a.

Insurance Expense

b.

Prepaid Rent

c.

Interest Expense

d.

Unearned Rent

57. Using accrual accounting, expenses are recorded and reported only

a.

when they are incurred, whether or not cash is paid

b.

when they are incurred and paid at the same time

c.

if they are paid before they are incurred

d.

if they are paid after they are incurred

Name:

Class:

Date:

chapter 3

58. Gracie Company made a prepaid rent payment of $2,800 on January 1. The company’s monthly rent is $700. The

amount of prepaid rent that would appear on the January 31 balance sheet after adjustment is

a.

$2,100

b.

$700

c.

$2,800

d.

$1,400

59. As time passes, fixed assets other than land lose their capacity to provide useful services. To account for this decrease

in usefulness, the cost of fixed assets is systematically allocated to expense through a process called

a.

equipment allocation

b.

depreciation

c.

accumulation

d.

matching

60. The balance in the office supplies account on January 1 was $7,000, supplies purchased during January were $3,000,

and the supplies on hand on January 31 were $2,000. The amount to be used for the appropriate adjusting entry is

a.

$4,300

b.

$12,000

c.

$5,000

d.

$8,000

61. The adjusting entry to record the depreciation of a building for the fiscal period is

a.

debit Depreciation Expense; credit Building

b.

debit Depreciation Expense; credit Accumulated Depreciation

c.

debit Accumulated Depreciation; credit Depreciation Expense

d.

debit Building; credit Depreciation Expense

62. All of the following statements regarding vertical analysis are true except

a.

vertical analysis may be prepared for several periods to analyze changes in relationships over time

b.

in a vertical analysis of a balance sheet, each asset item is stated as a percent of total assets

c.

in a vertical analysis of an income statement, each item is stated as a percent of total expenses

d.

major differences between a company’s vertical analysis and industry averages should be investigated

63. Adjusting entries affect at least one

a.

income statement account and one balance sheet account

b.

revenue and the dividends account

c.

asset and one owner’s equity account

d.

revenue and one owner’s equity account

64. Deferred revenue is revenue that is

a.

earned and the cash has been received

b.

earned but the cash has not been received

c.

not earned and the cash has not been received

d.

not earned but the cash has been received

Name:

Class:

Date:

chapter 3

65. Prior to the adjusting process, accrued expenses have

a.

not yet been incurred, paid, or recorded

b.

been incurred, have not been paid, but have been recorded

c.

been incurred but not paid and not recorded

d.

been paid but have not yet been incurred

66. The entry to adjust the accounts for salaries accrued at the end of the accounting period is

a.

debit Salaries Payable; credit Cash

b.

debit Cash; credit Salaries Payable

c.

debit Salaries Payable; credit Salaries Expense

d.

debit Salaries Expense; credit Salaries Payable

67. The type of account and normal balance of Prepaid Insurance would be

a.

asset, credit

b.

asset, debit

c.

contra asset, credit

d.

contra asset, debit

68. Which of the following accounts would most likely appear on an adjusted trial balance but probably would not appear

on the unadjusted trial balance?

a.

Fees Earned

b.

Accounts Receivable

c.

Unearned Fees

d.

Depreciation Expense

69. Which of the following is considered to be an accrued expense?

a.

A computer technician installed the latest software updates and was paid on the same day.

b.

A computer technician has been paid in advance to install software updates as they become available.

c.

A computer technician has just signed an agreement with you regarding pricing for future work.

d.

A computer technician has installed the latest software updates, but you have not received an invoice or made

payment.

70. The accounting principle upon which deferrals and accruals are based is

a.

matching

b.

cost

c.

price-level adjustment

d.

conservatism

71. For the year ending December 31, Orion, Inc. mistakenly omitted adjusting entries for $1,500 of supplies that were

used, (2) unearned revenue of $4,200 that was earned, and (3) insurance of $5,000 that expired. For the year ending

December 31, what is the effect of these errors on revenues, expenses, and net income?

a.

Revenues are overstated by $4,200.

b.

Net income is overstated by $2,300.

c.

Expenses are overstated by $6,500.

d.

Expenses are understated by $3,500.

Name:

Class:

Date:

chapter 3

72. Select the best explanation for the following adjusting entry:

Supplies Expense

730

Supplies

730

????????????????

a.

To record supplies used.

b.

To record purchase of supplies.

c.

To reduce supplies expense.

d.

To record sale of supplies.

73. When is the adjusted trial balance prepared?

a.

before adjusting journal entries are posted

b.

after adjusting journal entries are posted

c.

after the adjusting journal entries are journalized

d.

before the adjusting journal entries are journalized

74. The cash basis of accounting records revenues and expenses when the cash is exchanged, while the accrual basis of

accounting

a.

records revenues when they are earned and expenses when they are paid

b.

records revenues and expenses when they are incurred

c.

records revenues when cash is received and expenses when they are incurred

d.

records revenues and expenses when the company needs to apply for a loan

75. Select the best explanation for the following adjusting entry:

Wages Expense

4,500

Wages Payable

4,500

????????????????

a.

To record the payment of wages.

b.

To record wages paid last month.

c.

To record wages paid in advance.

d.

To record accrued wages.

76. Accumulated Depreciation and Depreciation Expense are classified, respectively, as

a.

expense, contra asset

b.

asset, contra liability

c.

revenue, asset

d.

contra asset, expense

77. Which of the following is the proper adjusting entry, based on a prepaid insurance account balance before adjustment

of $14,000 and unexpired insurance of $3,000, for the fiscal year ending on April 30?

a.

debit Insurance Expense, $3,000; credit Prepaid Insurance, $3,000

b.

debit Insurance Expense, $14,000; credit Prepaid Insurance, $14,000

c.

debit Prepaid Insurance, $11,000; credit Insurance Expense, $11,000

d.

debit Insurance Expense, $11,000; credit Prepaid Insurance, $11,000

Name:

Class:

Date:

chapter 3

78. The balance in the supplies account before adjustment at the end of the year is $6,250. The proper adjusting entry if

the amount of supplies on hand at the end of the year is $1,500 would be

a.

debit Supplies, $1,500; credit Supplies Expense, $1,500

b.

debit Supplies Expense, $4,750; credit Supplies, $4,750

c.

debit Supplies Expense, $1,500; credit Supplies, $1,500

d.

debit Supplies, $4,750; credit Supplies Expense, $4,750

79. Prepaid expenses are eventually expected to become

a.

expenses when their future economic value expires or is used up

b.

revenues when services are performed

c.

expenses in the period when they are paid

d.

revenues when the liability is no longer owed

80. A business pays biweekly salaries of $20,000 every other Friday for a 10-day period ending on that day. The last

payday of December is Friday, December 27. Assume the next pay period begins on Monday, December 30, and the

proper adjusting entry is journalized at the end of the fiscal period (December 31). The entry for the payment of the

payroll on Friday, January 10, includes a

a.

debit to Salary Expense of $16,000

b.

debit to Salary Expense of $4,000

c.

credit to Salaries Payable of $16,000

d.

credit to Salaries Payable of $4,000

81. Which of the following is not true regarding depreciation?

a.

Depreciation allocates the cost of a fixed asset over its estimated life.

b.

Depreciation expense reflects the decrease in market value each year.

c.

Depreciation is an allocation not a valuation method.

d.

Depreciation expense does not measure changes in market value.

82. The difference between the balance of a fixed asset account and the related accumulated depreciation account is

termed

a.

historical cost

b.

contra asset

c.

book value

d.

market value

83. Which of the following accounts would likely be included in a deferral adjusting entry?

a.

Interest Revenue

b.

Unearned Revenue

c.

Salaries Payable

d.

Accounts Receivable

84. Data for an adjusting entry described as “accrued wages, $2,020” requires a

a.

debit to Wages Expense and a credit to Wages Payable

b.

debit to Wages Payable and a credit to Wages Expense

Name:

Class:

Date:

chapter 3

c.

debit to Accounts Receivable and a credit to Wages Expense

d.

debit to Dividends and a credit to Wages Payable

85. If the effect of the credit portion of an adjusting entry is to increase the balance of a liability account, which of the

following describes the effect of the debit portion of the entry?

a.

increases the balance of a contra asset account

b.

increases the balance of an asset account

c.

decreases the balance of an owner’s equity account

d.

increases the balance of an expense account

86. Prior to the adjusting process, accrued revenue has

a.

been earned and cash received

b.

been earned and not recorded as revenue

c.

not been earned but recorded as revenue

d.

not been recorded as revenue but cash has been received

87. The adjusting entry for gym memberships earned that were previously recorded in the unearned gym memberships

account is

a.

debit Unearned Gym Memberships; credit Gym Memberships Revenue

b.

debit Gym Memberships Revenue; credit Unearned Gym Memberships

c.

debit Unearned Gym Memberships; credit Prepaid Gym Memberships

d.

debit Gym Memberships Expense; credit Unearned Gym Memberships

88. The general term used to indicate delaying the recognition of an expense already paid or of a revenue already received

is

a.

depreciation

b.

deferral

c.

accrual

d.

inventory

89. Prepaid expenses have

a.

not yet been recorded as expenses but have been paid

b.

been recorded as expenses and paid

c.

been incurred and paid

d.

not yet been recorded as expenses

90. Select the best explanation for the following adjusting entry:

Unearned Revenue

7,500

Fees Earned

7,500

????????????????

a.

To record payment of fees earned.

b.

To record fees earned at the end of the month.

c.

To record fees that have not been earned at the end of the month.

d.

To record payment of fees to be earned.

Name:

Class:

Date:

chapter 3

91. Smokey Company purchases a one-year insurance policy on July 1 for $3,600. The adjusting entry on December 31 is

a.

debit Insurance Expense, $1,800; credit Prepaid Insurance, $1,800

b.

debit Insurance Expense, $1,500; credit Prepaid Insurance, $1,500

c.

debit Insurance Expense, $2,100; credit Prepaid Insurance, $2,100

d.

debit Prepaid Insurance, $1,800; credit Cash, $1,800

92. Buster Industries pays weekly salaries of $30,000 on Friday for a five-day week ending on that day. The adjusting

entry necessary at the end of the fiscal period ending on Tuesday is

a.

debit Salaries Payable, $12,000; credit Cash, $12,000

b.

debit Salary Expense, $12,000; credit Dividends, $12,000

c.

debit Salary Expense, $12,000; credit Salaries Payable, $12,000

d.

debit Dividends, $12,000; credit Cash, $12,000

93. If there is a balance in the unearned subscriptions account after adjusting entries are made, it represents a(n)

a.

deferral

b.

accrual

c.

dividend

d.

revenue

94. By matching revenue earned during the accounting period to related incurred expenses,

a.

net income or loss will always be underestimated

b.

net income or loss will always be overestimated

c.

net income or loss will be properly reported on the income statement

d.

net income or loss will not be determined

95. Services were performed but not billed. What effect will this have on the income statement if an adjusting entry is not

made?

a.

Revenues will be overstated.

b.

Expenses will be overstated.

c.

Net income will be understated.

d.

Liabilities will be understated.

96. Which of the following is an example of an accrued expense?

a.

salary owed but not yet paid

b.

fees received but not yet earned

c.

supplies on hand

d.

a two-year premium paid on a fire insurance policy

97. Accrued revenues affect _____ on the balance sheet.

a.

assets

b.

liabilities

c.

owner’s capital

d.

prepaid expenses

98. Using accrual accounting, revenue is recorded and reported only

Name:

Class:

Date:

chapter 3

a.

when cash is received without regard to when the services are rendered

b.

when the services are rendered without regard to when cash is received

c.

when cash is received at the time services are rendered

d.

if cash is received after the services are rendered

99. The type of account and normal balance of Unearned Consulting Fees would be

a.

revenue, credit

b.

expense, debit

c.

liability, credit

d.

liability, debit

100. The revenue recognition principle

a.

is not in conflict with the cash method of accounting

b.

determines when revenue is credited to a revenue account

c.

states that revenue is not recorded until the cash is received

d.

controls all revenue reporting for the cash basis of accounting

101. How will the following adjusting journal entry affect the accounting equation?

Unearned Subscription Revenue

11,500

Subscription Revenue

11,500

a.

increase assets, increase revenues

b.

increase liabilities, increase revenues

c.

decrease liabilities, increase revenues

d.

decrease liabilities, decrease revenues

102. Supplies are recorded as assets when purchased. Therefore, the credit to Supplies in the adjusting entry is for the

amount of supplies

a.

still on hand

b.

purchased

c.

used

d.

required for the next accounting period

103. The unexpired insurance at the end of the fiscal period represents a(n)

a.

accrued asset

b.

accrued liability

c.

accrued expense

d.

deferred expense

104. The cost of office supplies to be used in future periods is ordinarily shown on the balance sheet as

a.

stockholders’ equity

b.

an asset

c.

a contra asset

d.

a liability

Name:

Class:

Date:

chapter 3

105. The account type and normal balance of Unearned Revenue are

a.

revenue, credit

b.

expense, debit

c.

liability, credit

d.

asset, debit

106. Which account would normally not require an adjusting entry?

a.

Wages Expense

b.

Accounts Receivable

c.

Accumulated Depreciation

d.

Cash

107. If there is a balance in the prepaid rent account after adjusting entries are made, it represents a(n)

a.

deferral

b.

accrual

c.

revenue

d.

liability

108. What effect will this adjusting journal entry have on the accounting records?

Supplies Expense

760

Supplies

760

a.

increase income

b.

decrease net income

c.

decrease expenses

d.

increase assets

109. The supplies account had a balance of $4,400 at the beginning of the year and was debited during the year for

$2,400, representing the total of supplies purchased during the year. If $400 of supplies are on hand at the end of the year,

the supplies expense to be reported on the income statement for the year is

a.

$400

b.

$2,000

c.

$6,800

d.

$6,400

110. At the end of the fiscal year, the usual adjusting entry to account for the expired portion of prepaid insurance was

omitted. Which of the following statements is true?

a.

Total assets at the end of the year will be understated.

b.

Owner’s equity at the end of the year will be understated.

c.

Net income for the year will be overstated.

d.

Insurance expense will be overstated.

111. Which of the following pairs of accounts could not appear in the same adjusting entry?

a.

Fees Earned and Unearned Fees

b.

Interest Income and Interest Expense

Name:

Class:

Date:

chapter 3

c.

Rent Expense and Prepaid Rent

d.

Salaries Payable and Salaries Expense

112. Which of the following steps in the accounting process would be completed last?

a.

preparing the adjusted trial balance

b.

posting

c.

preparing the financial statements

d.

journalizing

113. The adjusting entry to account for supplies used was omitted at the end of the year. This would affect the income

statement by having

a.

expenses understated and therefore net income overstated

b.

revenues understated and therefore net income understated

c.

expenses understated and therefore net income understated

d.

expenses overstated and therefore net income understated

114. Prepaid rent, representing rent for the next six months’ occupancy, would be reported on the tenant’s balance sheet as

a(n)

a.

asset

b.

liability

c.

owner’s equity account

d.

contra liability

115. The matching principle

a.

addresses the relationship between the journal and the balance sheet

b.

determines whether the normal balance of an account is a debit or credit

c.

requires that the dollar amount of debits equal the dollar amount of credits on a trial balance

d.

states that the revenues and related expenses should be reported in the same period

116. Adjusting entries always include

a.

only income statement accounts

b.

only balance sheet accounts

c.

the cash account

d.

at least one income statement account and one balance sheet account

117. Accrued expenses affect _____ on the balance sheet.

a.

assets

b.

liabilities

c.

fixed assets

d.

prepaid expenses

118. The account type and normal balance of Prepaid Expense are

a.

revenue, credit

b.

expense, debit

c.

liability, credit

Name:

Class:

Date:

chapter 3

d.

asset, debit

119. Which of the following is considered to be unearned revenue?

a.

theater tickets sold last month for yesterday’s performance

b.

theater tickets sold yesterday on credit for yesterday’s performance

c.

theater tickets that were not sold for the current performance

d.

theater tickets sold for next month’s performance

120. Prepaid advertising, representing payment for the next quarter, would be reported on the balance sheet as

a.

an asset

b.

a liability

c.

a contra asset

d.

owner’s equity

121. The unearned rent account has a balance of $72,000. If $18,000 of the $72,000 remains unearned at the end of the

accounting period, the amount of the adjusting entry is

a.

$18,000

b.

$90,000

c.

$54,000

d.

$36,000

122. What is the purpose of the adjusted trial balance?

a.

to verify that all of the adjusting entries have been posted

b.

to verify that the net income (loss) is correctly reported

c.

to verify that no adjusting journal entry has been omitted

d.

to verify that the debits and credits balance

123. Which of the following is an example of a prepaid expense?

a.

Supplies

b.

Accounts Receivable

c.

Unearned Subscription Revenue

d.

Unearned Fees

124. Two income statements for Toby Sam Enterprises follow:

Toby Sam Enterprises

Income Statement

For the Years Ended December 31

Year 2

Year 1

Fees earned

$674,350

$520,600

Operating expenses

472,045

338,390

Income from operations

$202,305

$182,210

Based on a vertical analysis of Toby Sam Enterprises’ income statements, has income from operations increased or

decreased as a percentage of revenue?

Name:

Class:

Date:

chapter 3

a.

increased by 5%

b.

increased by 111%

c.

decreased by 5%

d.

decreased by 111%

125. Generally accepted accounting principles require that companies use the _____ of accounting.

a.

cash basis

b.

deferral basis

c.

accrual basis

d.

account basis

126. The balance in the prepaid rent account before adjustment at the end of the year is $32,000, which represents four

months’ rent paid on December 1. The adjusting entry required on December 31 is

a.

debit Rent Expense, $8,000; credit Prepaid Rent, $8,000

b.

debit Prepaid Rent, $24,000; credit Rent Expense, $8,000

c.

debit Rent Expense, $24,000; credit Prepaid Rent, $8,000

d.

debit Prepaid Rent, $8,000; credit Rent Expense, $8,000

127. The net income reported on the income statement is $58,000. However, adjusting entries have not been made at the

end of the period for supplies expense of $2,200 and accrued salaries of $1,300. Net income, as corrected, is

a.

$56,700

b.

$58,000

c.

$55,800

d.

$54,500

128. Adjusting entries are

a.

the same as correcting entries

b.

needed to bring accounts up to date and match revenue and expense

c.

optional under generally accepted accounting principles

d.

rarely needed in large companies

129. The entry to adjust for the cost of supplies used during the accounting period is

a.

debit Supplies Expense; credit Supplies

b.

debit Owner’s Equity; credit Supplies

c.

debit Accounts Payable; credit Supplies

d.

debit Supplies; credit Owner’s Equity

130. The net book value of a fixed asset is determined by the original cost

a.

less accumulated depreciation

b.

less market value

c.

less accumulated depreciation plus depreciation expense

d.

plus accumulated depreciation

131. The omission of an adjusting entry for the depreciation of equipment will have what effect on the financial

statements?

Name:

Class:

Date:

chapter 3

a.

Net income will be overstated on the income statement.

b.

Expenses will be understated on the income statement.

c.

Assets will be overstated on the balance sheet.

d.

All of these choices.

132. Which of the following is an example of accrued revenue?

a.

snow removal services that have been paid for three months in advance

b.

snow removal services that have been provided but have not been billed or paid

c.

an agreement that has been signed for snow removal services for the next three months

d.

snow removal services that have been provided and paid on the same day

133. What effect will the following adjusting entry have on the accounting records?

Depreciation Expense

2,150

Accumulated Depreciation

2,150

a.

increase net income

b.

increase revenues

c.

decrease expenses

d.

decrease net book value

134. A business pays biweekly salaries of $20,000 every other Friday for a 10-day period ending on that day. The

adjusting entry necessary at the end of the fiscal period ending on the second Wednesday of the pay period includes a

a.

debit to Salary Expense of $8,000

b.

debit to Salaries Payable of $8,000

c.

credit to Salary Expense of $16,000

d.

credit to Salaries Payable of $16,000

Match each of the following omissions to the effect (a through h) it would have on the balance sheet.

a.

Assets and owner’s equity overstated

b.

Assets and owner’s equity understated

c.

Assets overstated and owner’s equity understated

d.

Assets understated and owner’s equity overstated

e.

Liabilities and owner’s equity overstated

f.

Liabilities and owner’s equity understated

g.

Liabilities overstated and owner’s equity understated

h.

Liabilities understated and owner’s equity overstated

135. No adjustment was made for supplies used up during the month.

136. Wages are paid every Friday for the five-day workweek. The month ended on Monday and no adjustment was

recorded.

137. Interest earned on a note receivable was not recorded.

Name:

Class:

Date:

chapter 3

138. Services provided to customers on the last day of the month were not billed.

139. An attorney has earned half of a retainer fee that was received and recorded last month. No adjustment was

recorded for the amount earned.

140. Property taxes are paid annually. The estimated monthly amount for the taxes was not recorded.

141. Depreciation on equipment was not recorded.

142. A tenant paid six months’ rent in advance when he moved in on the first day of the month. No entry was made on the

last day of the month.

Match each of the following examples to the type of account (a through e) it represents. Letters may be used more than

once.

a.

Prepaid expense

b.

Accrued expense

c.

Unearned revenue

d.

Accrued revenue

e.

None of these choices

143. Services provided that have not been recorded.

144. Paid for a one-year insurance policy.

145. Retainer fee received from a client for future legal representation.

146. Annual property taxes owed that are to be paid at the beginning of next year.

147. Wages owed that will be paid next month.

148. Paid for a six-month magazine subscription.

149. Received payment covering a six-month magazine subscription.

150. Provided tutoring for a student that will be invoiced next month.

151. Received six months of rental payments from a tenant.

152. Paid six months of rental payments to the landlord.

153. Annual depreciation on equipment, recorded on a monthly basis.

154. A contract to provide tutoring services beginning next month was signed.

155. At the end of April, the first month of the company’s year, the usual adjusting entry transferring rent earned to a

revenue account from the unearned rent account was omitted. Indicate which items will be incorrectly stated, because of

the error, on (a) the income statement for April and (b) the balance sheet as of April 30. Also indicate whether the items in

error will be overstated or understated.

Name:

Class:

Date:

chapter 3

156. Journalize the adjusting entries necessary on December 31 for the following items. Omit explanations.

1. Fees accrued but not billed, $6,300.

2. The supplies account balance on December 31, $4,750; supplies on hand, $960.

3. Wages accrued but not paid, $2,700.

4. Depreciation of office equipment, $1,650.

5. Rent expired during year, $10,800.

157. What is the purpose of an adjusted trial balance? What type(s) of error does it detect? What type(s) of error does it

not detect?

158. Two income statements for Midnight Enterprises are as follows:

Midnight Enterprises

Income Statements

For the Years Ended December 31

Year 2

Year 1

Fees earned

$674,350

$520,600

Operating expenses

472,045

338,390

Income from operations

$202,305

$182,210

(a) Prepare a vertical analysis of Midnight Enterprises’ income statements.

(b) Does the vertical analysis indicate a favorable or unfavorable change?

159. On January 1, Power House Co. prepaid the annual rent of $10,140. Journalize this transaction.

160. Salaries of $6,400 are paid for a five-day week on Friday. Journalize the necessary adjusting entry if the month ends

on Thursday.

161. For the year ending December 31, Beard Clinical Supplies Co. mistakenly omitted adjusting entries for (1) $9,800 of

unearned revenue that was earned, (2) earned revenue that was not billed of $10,200, and (3) accrued wages of $7,000.

Indicate the combined effect of the errors on (a) revenues, (b) expenses, and (c) net income.

162. On January 2, Safe Motorcycling Monthly received a check for $72 from a subscriber for a 12-month subscription.

The January issue was mailed on January 15. Prepare the necessary entries for the month of January.

163. Gizmo Company purchased a one-year insurance policy on October 1 for $1,800. Journalize the adjusting entry

required on December 31.

164. On November 1, clients of Great Designs Company prepaid $4,250 for services to be provided in the future at a rate

of $85 per hour.

(a) Journalize the receipt of cash.

(b) As of November 30, Great Designs shows that 15 hours of services have been provided on this agreement. Journalize

the necessary adjusting entry.

(c) Determine the total unearned fees in hours and dollars at November 30.

165. Depreciation on equipment for the year is $6,300.

(a) Journalize the transaction if the company prepares adjustments once a year.

(b) Journalize the transaction if the company prepares adjustments on a monthly basis.

166. Using the following account balances for Garry’s Tree Service, prepare a trial balance.

Name:

Class:

Date:

chapter 3

Accounts Payable

$ 7,000

Accumulated Depreciation—Machinery

7,340

Cash

25,000

Garry Mauss, Capital

32,910

Garry Mauss, Drawing

3,300

Machinery

18,350

Prepaid Rent

12,200

Rent Expense

11,500

Service Revenue

21,000

Supplies

1,000

Wages Expense

2,000

Wages Payable

3,600

Unearned Revenue

1,500

167. The prepaid insurance account had a beginning balance of $6,600 and was debited for $2,300 for premiums paid

during the year. Journalize the adjusting entry required at the end of the year, assuming the amount of unexpired insurance

related to future periods is $4,100.

168. Explain the difference between accrued revenues and unearned revenues. Provide an example of each.

169. A one-year insurance policy was purchased on June 1 for $2,400. Journalize the adjusting entry required on

December 31.

170. On January 1, DogMart Company purchased a two-year liability insurance policy for $22,800 cash. The purchase

was recorded to Prepaid Insurance. Journalize the January 31 adjusting entry.

171. Two income statements for Danielle’s Design Services are as follows:

Danielle’s Design Services

Income Statements

For the Years Ended December 31

Year 2

Year 1

Fees earned

$765,340

$696,520

Expenses:

Wages expense

$254,000

$214,600

Rent expense

120,000

108,000

Supplies expense

76,500

98,715

Miscellaneous expense

11,680

16,420

Total expenses

$462,180

$437,735

Income from operations

$303,160

$258,785

(a) Prepare a vertical analysis of Danielle’s Design Services income statements.

(b) What types of changes are indicated: favorable or unfavorable?

(c) What other information would enhance the analysis?

172. Ski Master Company pays weekly salaries of $18,000 on Friday for a five-day week ending on that day. Journalize

the necessary adjusting entry at the end of the accounting period, assuming that the period ends on Wednesday.

Name:

Class:

Date:

chapter 3

173. At the end of the current year, fees of $3,700 have been earned but have not been billed to clients. Journalize the

adjusting entry to record the accrued fees.

174. For each of the following, journalize the necessary adjusting entry. Omit explanations.

(a)

A business pays weekly salaries of $22,000 on Friday for a five-day week ending on

that day. Journalize the necessary adjusting entry at the end of the fiscal period,

assuming that the fiscal period ends (1) on Tuesday or (2) on Wednesday.

(b)

The balance in the prepaid insurance account before adjustment at the end of the year

is $18,000. Journalize the adjusting entry required under each of the following

alternatives: (1) the amount of insurance expired during the year is $5,300 or (2) the

amount of unexpired insurance applicable to a future period is $2,700.

(c)

On July 1 of the current year, a business pays $54,000 to the city for taxes (license

fees) for the coming fiscal year. Journalize the adjusting entry required to bring the

accounts affected by the taxes up to date as of July 31.

(d)

The estimated depreciation on equipment for the year is $32,000.

175. Indicate whether the following error would cause the adjusted trial balance totals to be unequal. If the error would

cause the adjusted trial balance totals to be unequal, indicate whether the debit or credit total is higher and by how much.

The entry for $975 of supplies used during the period was journalized as a debit to Supplies Expense for $795 and credit

to Supplies for $975.

176. A business pays biweekly salaries of $20,000 every other Friday for a 10-day period ending on that day. The last

payday of December is Friday, December 27. Assume the next pay period begins on Monday, December 30 and the

proper adjusting entry is journalized at the end of the fiscal period (December 31). Journalize the entry for the payment of

the payroll on Friday, January 10.

177. Depreciation on an office building is $2,800. Journalize the adjusting entry required on December 31.

178. DogMart Company records depreciation for equipment. Depreciation for the period ending December 31 is $1,400

for office equipment and $2,650 for production equipment. Journalize the two entries to record the depreciation.

179. At the end of the fiscal year, the following adjusting entries were omitted:

(a)

No adjusting entry was made to transfer the $1,750 of prepaid insurance from the

asset account to the expense account.

(b)

No adjusting entry was made to record accrued fees of $525 for services provided

to customers.

Assuming that financial statements are prepared before the errors are discovered, indicate the effect of each error,

considered individually, on the following items. Specify whether each item would be overstated or understated and by

how much. If no effect, insert a zero.

Error (a) Error (b)

Over- Under- Over- Under-

stated stated stated stated

(1) Assets at Dec. 31 $ $ $ $

(2) Liabilities at Dec. 31 $ $ $ $

(3) Net income for the year $ $ $ $

Name:

Class:

Date:

chapter 3

(4) Owner’s equity at Dec. 31 $ $ $ $

180. Indicate whether the following error would cause the adjusted trial balance totals to be unequal. If the error would

cause the adjusted trial balance totals to be unequal, indicate whether the debit or credit total is higher and by how much.

The adjustment for accrued fees of $1,170 was journalized as a debit to Accounts Receivable for $1,170 and a credit to

Fees Earned for $1,107.

181. The supplies account had a beginning balance of $1,750. Supplies purchased during the period totaled $3,500. At the

end of the period before adjustment, $350 of supplies was on hand. Journalize the adjusting entry for supplies.

182. For the year ending June 30, Island Clinical Services mistakenly omitted adjusting entries for (1) $1,500 of supplies

that were used, (2) unearned revenue of $4,200 that was earned, and (3) insurance of $5,000 that expired. What is the

combined effect of these errors on (a) revenues, (b) expenses, and (c) net income for the year ending June 30?

183. Jordon J. James started JJJ Consulting on January 1. The following are the account balances at the end of the first

month of business, before adjusting entries were recorded:

Accounts Payable

$ 300

Accounts Receivable

750

Cash

6,300

Consulting Revenue

4,925

Equipment

7,000

Jordon J. James, Capital

15,000

Jordon J. James, Drawing

1,375

Prepaid Rent

4,000

Supplies

800

Adjustment data:

Supplies on hand at the end of the month, $200

Unbilled consulting revenue, $700

Rent expense for the month, $1,000

Depreciation on equipment, $90

(a) Prepare the required adjusting entries, adding accounts as needed. Omit explanations.

(b) Prepare an adjusted trial balance for JJJ Consulting as of January 31.

184. On January 1, Newman Company estimated its property tax to be $5,100 for the year.

(a)

How much should the company accrue each month for property taxes?

(b)

Determine the balance in Property Tax Payable as of August 31.

(c)

Journalize the property tax accrual for September.

185. REM Consulting is completing the accounting information processing at the end of the fiscal year, December 31. The

following trial balances are available.

Accounts

Unadjusted

Trial Balance

Adjusted

Trial Balance

Debit

Credit

Debit

Credit

Cash

13,000

13,000

Name:

Class:

Date:

chapter 3

Accounts Receivable

1,500

1,800

Prepaid Insurance

600

200

Supplies

3,800

3,000

Machines

30,000

30,000

Accumulated Depreciation

12,000

17,500

Wages Payable

900

Unearned Fees

6,700

6,500

Randall E. Moore, Capital

24,000

24,000

Randall E. Moore, Drawing

4,800

4,800

Fees Earned

25,000

25,500

Wages Expense

14,000

14,900

Depreciation Expense

5,500

Supplies Expense

800

Insurance Expense

400

67,700

67,700

74,400

74,400

(a) Reconstruct the adjusting entries and give a brief explanation of each.

(b) Determine the amount of REM’s net income or loss.

186. Accounts to use for transactions (a) through (j), each identified by a number, are listed. Following this list are the

transactions. For each transaction, indicate the accounts that should be debited and credited by their account number(s).

21

Accounts Payable

12

Accounts Receivable

19

Accumulated Depreciation

16

Building

31

Myra May, Capital

11

Cash

56

Depreciation Expense

32

Myra May, Drawing

41

Fees Earned

55

Insurance Expense

24

Insurance Payable

57

Interest Expense

25

Interest Payable

13

Interest Receivable

17

Land

18

Office Equipment

26

Notes Payable

14

Office Supplies

18

Office Supplies Expense

15

Prepaid Insurance

23

Unearned Fees

54

Wages Expense

22

Wages Payable

Transactions

Account(s) Debited

Account(s) Credited

a. Accrued wages as of the last day of

month; payment will be made in three days.

b. Paid the wages previously recorded in

transaction (a) plus the wages earned in the

Name:

Class:

Date:

chapter 3

first three days of the month.

c. Bought a three-year insurance policy and

paid in full.

d. Made an entry to adjust for the expired

portion of the insurance premium.

e. Received $7,000 from a contract to

perform accounting services over the next

two years.

f. Made an entry to adjust for half of the

services performed in (e).

g. Purchased office supplies, paying part

cash and charging the balance on account.

h. Borrowed money from a bank and signed

a note payable due in six months.

i. Recorded one month’s accrued interest

on the note payable.

j. Recorded depreciation on the office

equipment.

187. Bloom’s Company pays biweekly salaries of $40,000 every other Friday for a 10-day period ending on that day. The

last payday of December is Friday, December 27. Assuming the next pay period begins on Monday, December 30,

journalize the adjusting entry necessary at the end of the fiscal period (December 31).

188. At January 31, the end of the first month of the year, the usual adjusting entry transferring expired insurance to an

expense account is omitted. Which items will be incorrectly stated, because of the error, on (a) the income statement for

January and (b) the balance sheet as of January 31? Also indicate whether the items in error will be overstated or

understated.

189. On December 15, Great Designs Company hired an independent contractor for a project. The contractor completed

the project on December 29 and submitted an invoice for $2,425 which was due on January 15. The amount was duly paid

on January 15.

(a) Journalize the entry or entries necessary to record these transactions.

(b) Discuss how the accrual basis of accounting affects this(these) journal entry(ies).

190. Journalize the following transactions.

(a) On December 1, $18,000 was received for a service contract to be performed from December 1 through April 30.

(b) Assuming the work is performed evenly throughout the contract period, journalize the adjusting entry required on

December 31.

191. On January 1, Great Designs Company had a debit balance of $1,450 in the office supplies account. During the

month, Great Designs purchased $115 and $160 of office supplies and journalized them to the asset account upon

purchasing. On January 31, an inspection of the office supplies cabinet shows that only $350 of office supplies remains.

Journalize the January 31 adjusting entry for office supplies.

192. Zoey Bella Company has a payroll of $10,000 for a five-day workweek. Its employees are paid each Friday for the

five-day workweek. Journalize the adjusting entry required on December 31, assuming the year ends on a Thursday.

193. Journalize the required entries for the following items:

Name:

Class:

Date:

chapter 3

(a)

Austin Company pays daily wages of $645 (Monday–Friday). Paydays are every other

Friday. Journalize the Monday, January 31 adjusting entry, assuming that the previous

payday was Friday, January 21.

(b)

Journalize the transaction to record Austin Company’s payroll on Friday, February 4.

(c)

Annual depreciation expense on the company’s fixed assets is $39,600. Journalize the

adjusting entry to recognize depreciation for the month of January.

(d)

The company’s office supplies account shows a debit balance of $3,755. A count of

office supplies on hand on January 31 shows $635 worth of supplies on hand. Journalize

the January 31 adjusting entry for Office Supplies.

194. For each of the following errors, considered individually, indicate whether the error would cause the adjusted trial

balance totals to be unequal. If the error would cause the adjusted trial balance total to be unequal, indicate whether the

debit or credit total is higher and by how much.

a)

The adjustment for unearned fees of $3,260 was journalized as a debit to Accounts

Payable for $3,260 and a credit to Fees Earned of $3,260.

b)

The adjustment for supplies expense of $425 was journalized as a debit to Supplies

Expense for $542 and a credit to Supplies for $425.

195. Complete the missing items in this summary of adjustments chart:

PREPAID EXPENSES

Examples

Adjusting Entry

Financial Statement Impact

if Adjusting Entry Is Omitted

Supplies,

(a)

Dr. Expense

Cr. Asset

Income Statement:

Revenues: No effect

Expenses: Understated

Net income: (b)

Balance Sheet:

Assets: (c)

Liabilities: (d)

Owner’s equity: Overstated

UNEARNED REVENUES

Examples

Adjusting Entry

Financial Statement Impact if

Adjusting Entry is Omitted

Unearned rent,

(e)

(f)

Income Statement:

Revenues: (g)

Expenses: No effect

Net income: (h)

Balance Sheet:

Assets: (i)

Liabilities: Overstated

Owner’s equity: (j)

ACCRUED REVENUES

Examples

Adjusting Entry

Financial Statement Impact if

Adjusting Entry Is Omitted

Interest income

due on a note,

(k)

Dr. Asset

Cr. Revenue

Income Statement:

Revenues: (l)

Expenses: (m)

Name:

Class:

Date:

chapter 3

Net income: Understated

Balance Sheet:

Assets: (n)

Liabilities: (o)

Owner’s equity: Understated

ACCRUED EXPENSES

Examples

Adjusting Entry

Financial Statement Impact if

Adjusting Entry Is Omitted

Interest due on a

note payable,

(p)

(q)

Income Statement:

Revenues: No effect

Expenses: (r)

Net income: (s)

Balance Sheet:

Assets: (t)

Liabilities: Understated

Owner’s equity: (u)

196. On November 15, Great Designs Company purchased an advertising campaign for the month of December. Great

Designs paid cash of $2,700 in advance. The advertising campaign ran in December and was completed on December 31.

(a) Journalize all necessary entries for the advertising campaign for November and December.

(b) Discuss how the matching principle applies to this(these) journal entry(ies).

197. Under the accrual basis, some accounts in the ledger require updating at the end of the period. Discuss the three main

reasons for this updating and give an example of each.

198. Indicate which of the following accounts would, under normal circumstances, require an adjusting entry.

a. Cash

b. Prepaid Insurance

c. Depreciation Expense

d. Wages Payable

e. Accumulated Depreciation

f. Equipment

199. Explain the difference between the accrual basis of accounting and the cash basis of accounting.

200. On December 31, a business estimates depreciation on equipment used during the first year of operations to be

$2,900. (a) Journalize the adjusting entry required on December 31. (b) If the adjusting entry in (a) were omitted, which

items would be erroneously stated on (1) the income statement for the year and (2) the balance sheet as of December 31?

201. Accrued salaries of $600 owed to employees for December 29, 30, and 31 are not taken into consideration in

preparing the financial statements for the year ended December 31. Indicate which items will be erroneously stated,

because of the error, on (a) the income statement for the year and (b) the balance sheet as of December 31. Also indicate

whether the items in error will be overstated or understated

202. The estimated amount of depreciation on equipment for the current year is $5,300. Journalize the adjusting entry to

record the depreciation.

203. On January 2, Dog Mart prepaid $30,000 rent for the year and recorded the prepayment in an asset account. Prepare

the January 31 adjusting entry for rent expense.

Name:

Class:

Date:

chapter 3

204. On March 1, a business paid $3,600 for a 12-month liability insurance policy. On April 1, the business entered into a

two-year rental contract for equipment at a total cost of $18,000. Determine the following amounts:

(a) Insurance expense for the month of March

(b) Balance in Prepaid Insurance as of March 31

(c) Equipment rent expense for the month of April

(d) Balance in Prepaid Equipment Rental as of April 30

205. Journalize the adjusting entries necessary at the end of the month for the following items:

(a)

The beginning balance of the supplies account was $245. During the month the

company bought additional supplies in the amount of $735. At the end of the month a

physical inventory showed $343 of unused supplies.

(b)

The company has a 12% note payable in the amount of $17,000 due in six months. The

interest expense of $170 for the month has not been recorded.

(c)

The company has two employees. The manager is paid on the fifteenth of every month

for work performed during the first half of the month and on the first of the following

month for the work performed during the second half of the month. His monthly salary

is $5,500. The other employee is paid $650 for each five-day work week (Monday–

Friday). The last day of the month fell on Thursday.

(d)

The unearned fees account shows a balance of $46,000. According to the manager 60%

of that amount has been earned.

(e)

At the end of the month, $5,700 of services had been performed but not yet billed.

206. On December 31, the balance in the office supplies account is $1,385. A physical count shows $435 worth of

supplies on hand. Journalize the adjusting entry for supplies.

207. The balance in the unearned fees account, before adjustment at the end of the year, is $10,250. Journalize the

adjusting entry required if the amount of unearned fees at the end of the year is $3,125.

208. Explain the difference between accrued expenses and prepaid expenses. Provide an example of each.

209. List the four basic types of accounts that require adjusting entries and give an example of each.

210. The company determines that the interest expense on a note payable for the period ending December 31 is $775. This

amount is payable on January 1. Journalize these transactions for December 31 and January 1.

211. Journalize the six entries to adjust the accounts at December 31. Omit explanations. (Hint: One of the accounts was

affected by two different adjusting entries.)

Accounts

Unadjusted

Trial Balance

Adjusted

Trial Balance

Debit

Balances

Credit

Balances

Debit

Balances

Credit

Balances

Cash

5,000

5,000

Accounts Receivable

32,000

32,600

Supplies

3,600

100

Prepaid Insurance

4,000

1,400

Equipment

11,000

11,000

Accumulated Depreciation

1,700

Wages Payable

2,000

Name:

Class:

Date:

chapter 3

Unearned Fees

8,900

3,500

Jose Mendez, Capital

22,000

22,000

Fees Earned

69,000

75,000

Wages Expense

44,300

46,300

Supplies Expense

3,500

Insurance Expense

2,600

Depreciation Expense

1,700

99,900

99,900

104,200

104,200

Name:

Class:

Date:

chapter 3

Answer Key

Name:

Class:

Date:

chapter 3

Name:

Class:

Date:

chapter 3

Name:

Class:

Date:

chapter 3

Name:

Class:

Date:

chapter 3

Name:

Class:

Date:

chapter 3

Name:

Class:

Date:

chapter 3

Name:

Class:

Date:

chapter 3

Name:

Class:

Date:

chapter 3

Name:

Class:

Date:

chapter 3

Name:

Class:

Date:

chapter 3

Name:

Class:

Date:

chapter 3

Name:

Class:

Date:

chapter 3

Name:

Class:

Date:

chapter 3

Name:

Class:

Date:

chapter 3

Name:

Class:

Date:

chapter 3

Name:

Class:

Date:

chapter 3