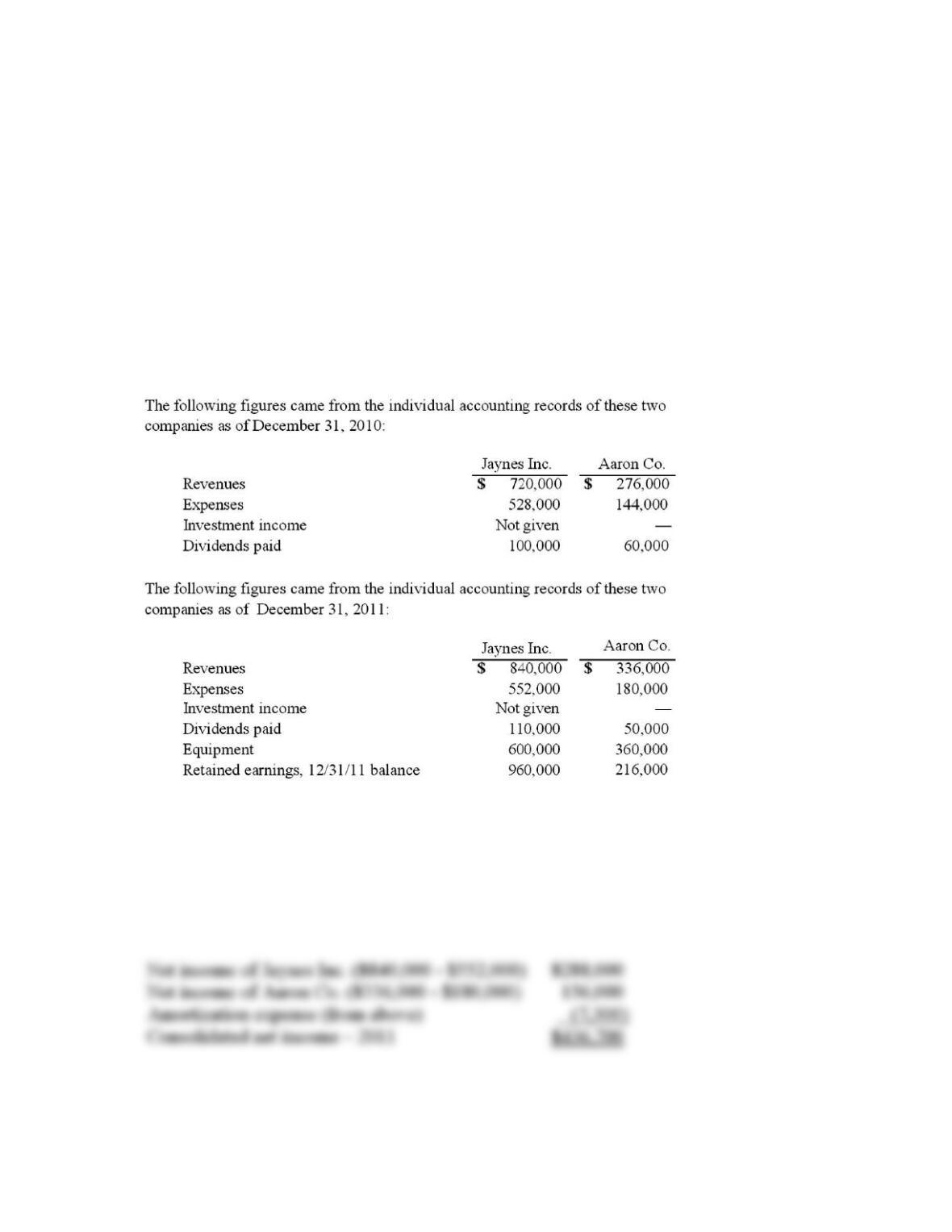

112. Jaynes Inc. acquired all of Aaron Co.’s common stock on January 1, 2010,

by issuing 11,000 shares of $1 par value common stock. Jaynes’ shares had a $17

per share fair value. On that date, Aaron reported a net book value of $120,000.

However, its equipment (with a five-year remaining life) was undervalued by

$6,000 in the company’s accounting records. Any excess of consideration

transferred over fair value of assets and liabilities is assigned to an unrecorded

patent to be amortized over ten years.

What was consolidated net income for the year ended December 31, 2011?

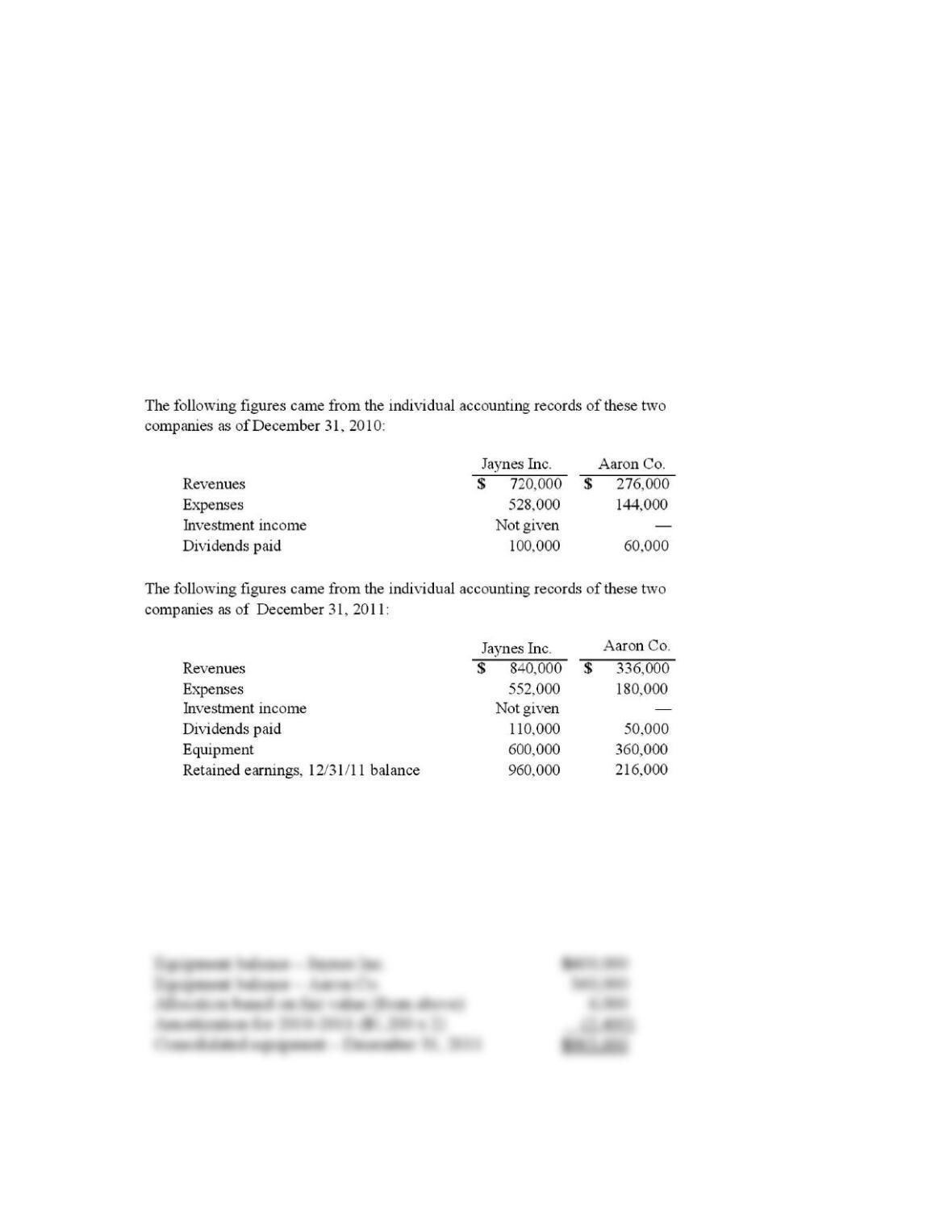

113. Jaynes Inc. acquired all of Aaron Co.’s common stock on January 1, 2010,

by issuing 11,000 shares of $1 par value common stock. Jaynes’ shares had a $17

per share fair value. On that date, Aaron reported a net book value of $120,000.

However, its equipment (with a five-year remaining life) was undervalued by

$6,000 in the company’s accounting records. Any excess of consideration

transferred over fair value of assets and liabilities is assigned to an unrecorded

patent to be amortized over ten years.

What was consolidated equipment as of December 31, 2011?

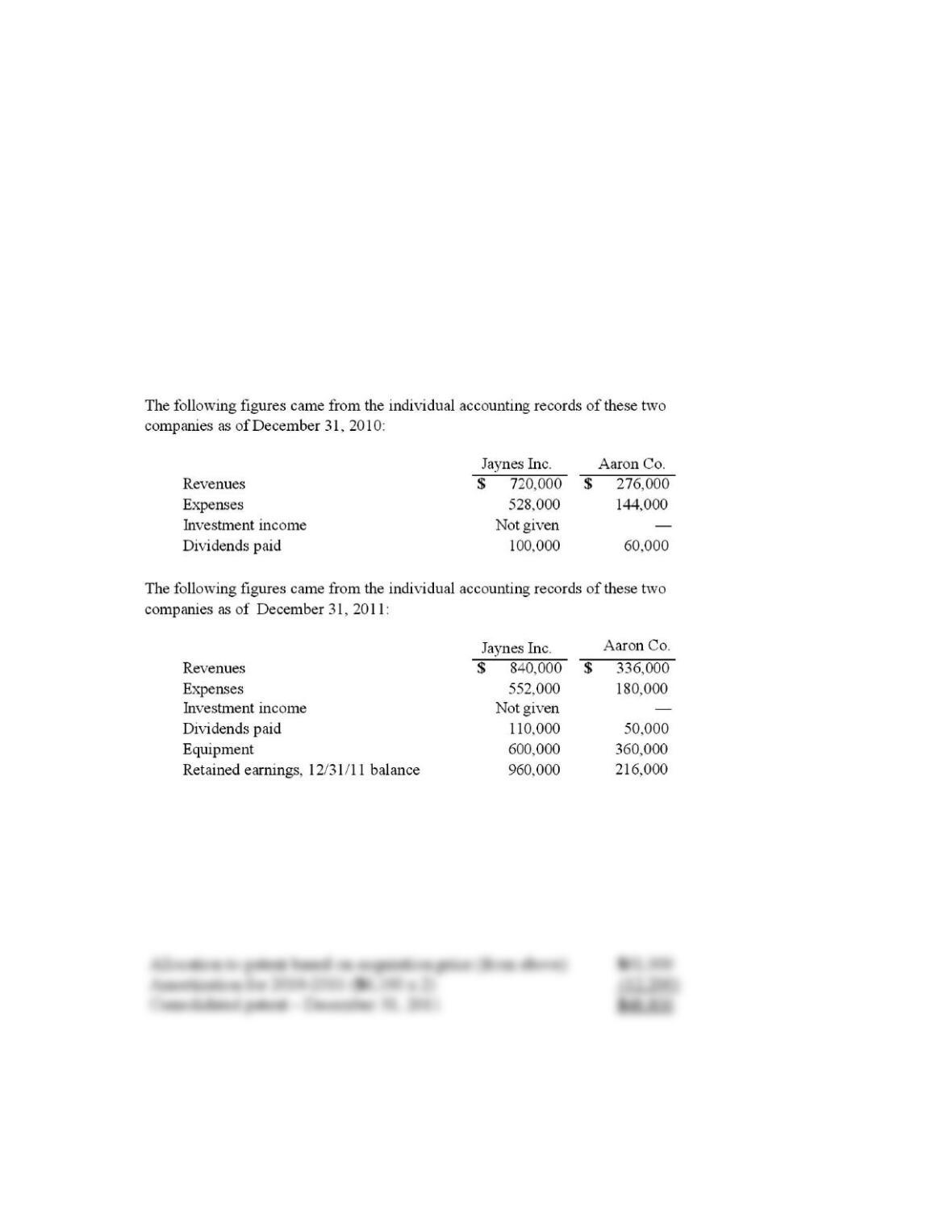

114. Jaynes Inc. acquired all of Aaron Co.’s common stock on January 1, 2010,

by issuing 11,000 shares of $1 par value common stock. Jaynes’ shares had a $17

per share fair value. On that date, Aaron reported a net book value of $120,000.

However, its equipment (with a five-year remaining life) was undervalued by

$6,000 in the company’s accounting records. Any excess of consideration

transferred over fair value of assets and liabilities is assigned to an unrecorded

patent to be amortized over ten years.

What was the total for consolidated patents as of December 31, 2011?

115. Utah Inc. acquired all of the outstanding common stock of Trimmer Corp.

on January 1, 2009. At that date, Trimmer owned only three assets and had no

liabilities:

If Utah paid $300,000 in cash for Trimmer, what allocation should have been

assigned to the subsidiary’s Building account and its Equipment account in a

December 31, 2011 consolidation?

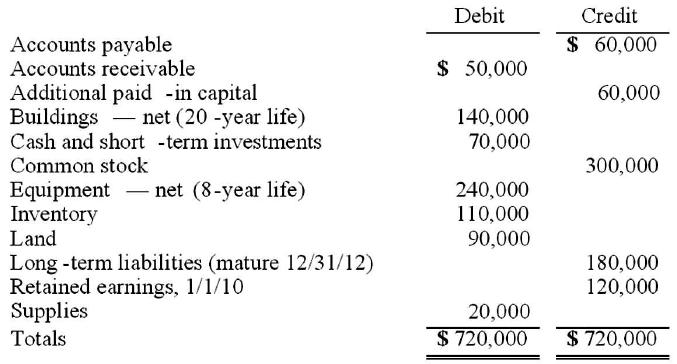

116. Matthews Co. acquired all of the common stock of Jackson Co. on January

1, 2010. As of that date, Jackson had the following trial balance:

During 2010, Jackson reported net income of $96,000 while paying dividends of

$12,000. During 2011, Jackson reported net income of $132,000 while paying

dividends of $36,000.

Assume that Matthews Co. acquired the common stock of Jackson Co. for

$588,000 in cash. As of January 1, 2010, Jackson’s land had a fair value of

$102,000, its buildings were valued at $188,000, and its equipment was appraised

at $216,000. Any excess of consideration transferred over fair value of assets and

liabilities acquired is due to an unamortized patent to be amortized over 10 years.

Matthews decided to use the equity method for this investment.

Required:

(A.) Prepare consolidation worksheet entries for December 31, 2010.

(B.) Prepare consolidation worksheet entries for December 31, 2011.

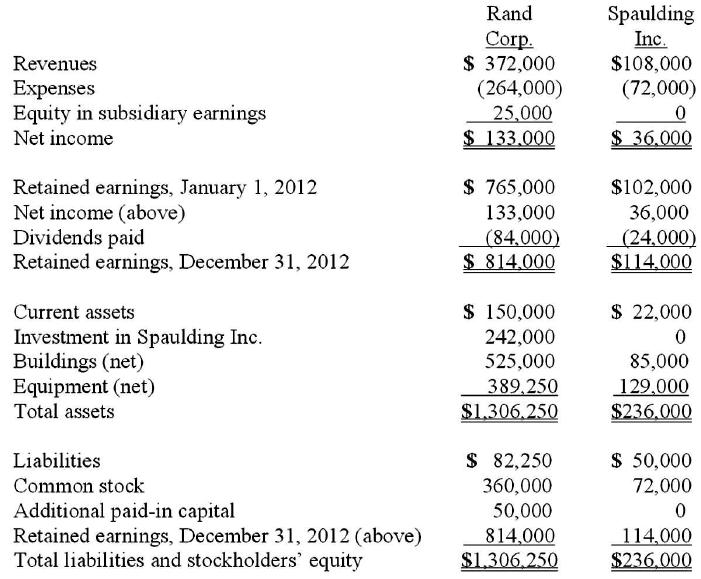

117. On January 1, 2009, Rand Corp. issued shares of its common stock to

acquire all of the outstanding common stock of Spaulding Inc. Spaulding’s book

value was only $140,000 at the time, but Rand issued 12,000 shares having a par

value of $1 per share and a fair value of $20 per share. Rand was willing to

convey these shares because it felt that buildings (ten-year life) were

undervalued on Spaulding’s records by $60,000 while equipment (five-year life)

was undervalued by $25,000. Any consideration transferred over fair value of

identified net assets acquired is assigned to goodwill.

Following are the individual financial records for these two companies for the

year ended December 31, 2012.

Required:

Prepare a consolidation worksheet for this business combination.

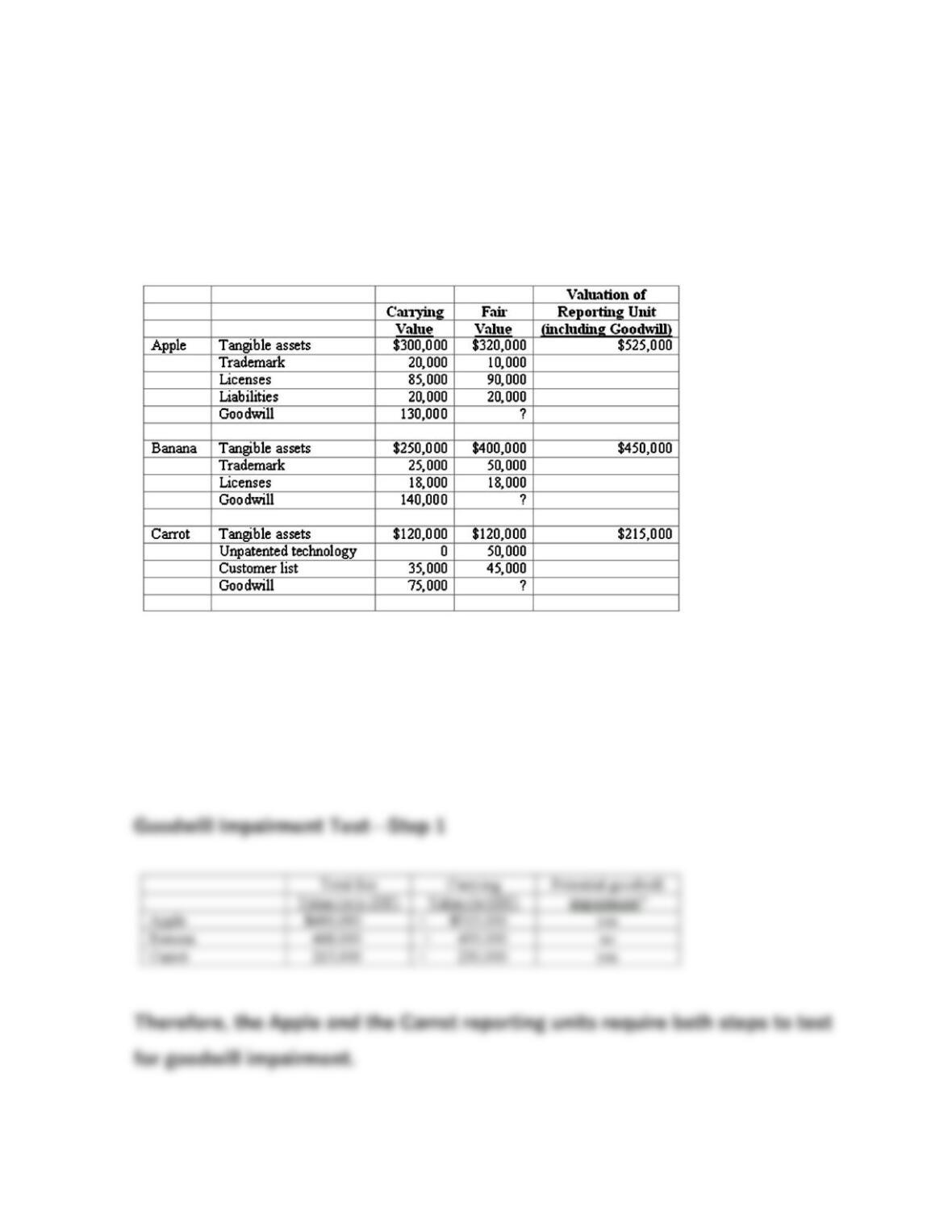

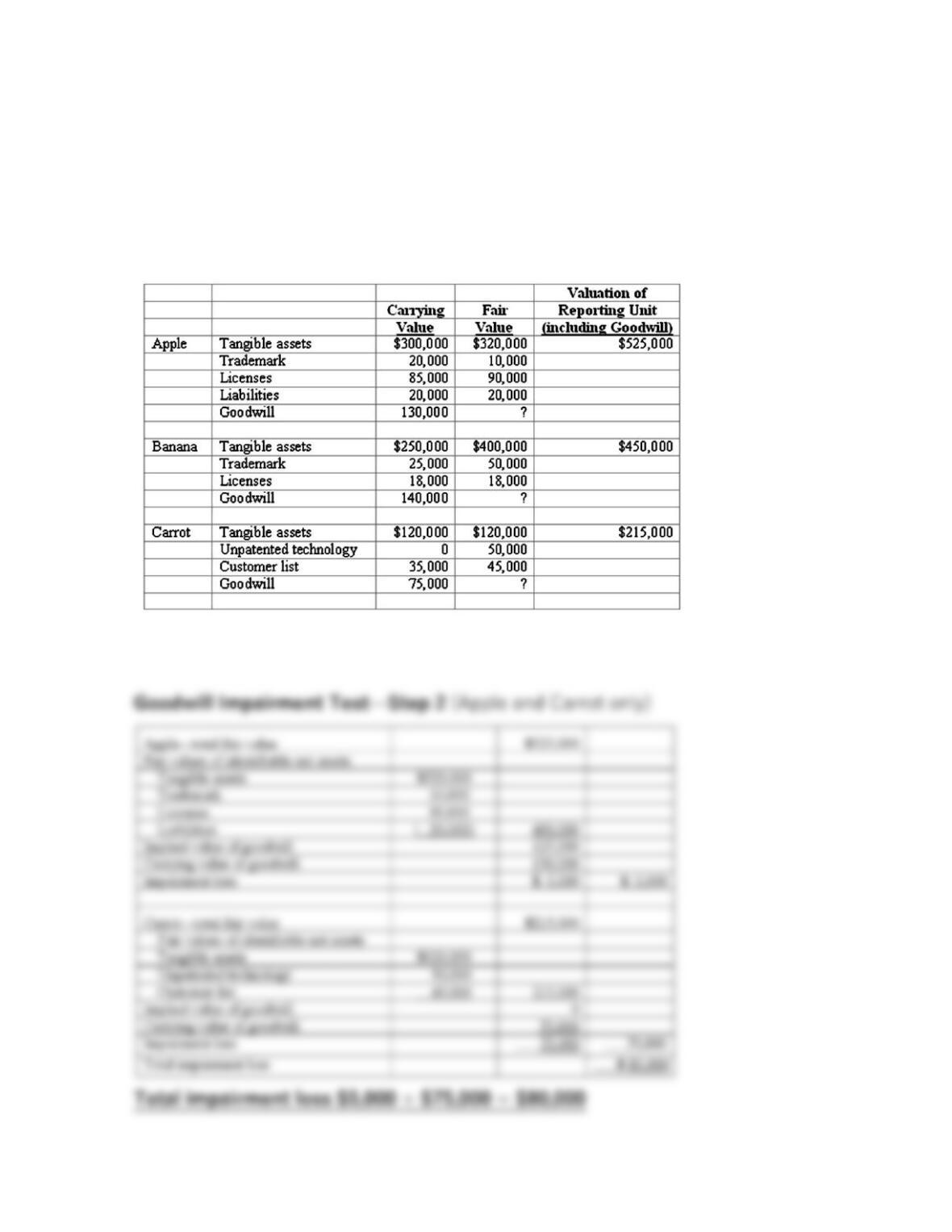

118. Pritchett Company recently acquired three businesses, recognizing

goodwill in each acquisition. Destin has allocated its acquired goodwill to its

three reporting units: Apple, Banana, and Carrot. Pritchett provides the following

information in performing the 2011 annual review for impairment:

Which of Pritchett’s reporting units require both steps to test for goodwill

impairment?

119. Pritchett Company recently acquired three businesses, recognizing

goodwill in each acquisition. Destin has allocated its acquired goodwill to its

three reporting units: Apple, Banana, and Carrot. Pritchett provides the following

information in performing the 2011 annual review for impairment:

How much goodwill impairment should Pritchett report for 2011?

120. On 4/1/09, Sey Mold Corporation acquired 100% of DotDot.Com for

$2,000,000 cash. On the date of acquisition, DotDot’s net book value was

$900,000. DotDot’s assets included land that was undervalued by $300,000, a

building that was undervalued by $400,000, and equipment that was overvalued

by $50,000. The building had a remaining useful life of 8 years and the equipment

had a remaining useful life of 4 years. Any excess fair value over consideration

transferred is allocated to an undervalued patent and is amortized over 5 years.

121. On 4/1/09, Sey Mold Corporation acquired 100% of DotDot.Com for

$2,000,000 cash. On the date of acquisition, DotDot’s net book value was

$900,000. DotDot’s assets included land that was undervalued by $300,000, a

building that was undervalued by $400,000, and equipment that was overvalued

by $50,000. The building had a remaining useful life of 8 years and the equipment

had a remaining useful life of 4 years. Any excess fair value over consideration

transferred is allocated to an undervalued patent and is amortized over 5 years.

122. On 4/1/09, Sey Mold Corporation acquired 100% of DotDot.Com for

$2,000,000 cash. On the date of acquisition, DotDot’s net book value was

$900,000. DotDot’s assets included land that was undervalued by $300,000, a

building that was undervalued by $400,000, and equipment that was overvalued

by $50,000. The building had a remaining useful life of 8 years and the equipment

had a remaining useful life of 4 years. Any excess fair value over consideration

transferred is allocated to an undervalued patent and is amortized over 5 years.

123. For each of the following situations, select the best answer that applies to

consolidating financial information subsequent to the acquisition date:

(A) Initial value method.

(B) Partial equity method.

(C) Equity method.

(D) Initial value method and partial equity method but not equity method.

(E) Partial equity method and equity method but not initial value method.

(F) Initial value method, partial equity method, and equity method.

_____1. Method(s) available to the parent for internal record-keeping.

_____2. Easiest internal record-keeping method to apply.

_____3. Income of the subsidiary is recorded by the parent when earned.

_____4. Designed to create a parallel between the parent’s investment accounts

and changes in the underlying equity of the acquired company.

_____5. For years subsequent to acquisition, requires the *C entry.

_____6. Uses the cash basis for income recognition.

_____7. Investment account remains at initially recorded amount.

_____8. Dividends received by the parent from the subsidiary reduce the parent’s

investment account.

_____9. Often referred to in accounting as a

single-line consolidation

.

_____10. Increases the investment account for subsidiary earnings, but does not

decrease the subsidiary account for equity adjustments such as amortizations.