73. How is the fair value allocation of an intangible asset allocated to expense

when the asset has no legal, regulatory, contractual, competitive, economic, or

other factors that limit its life?

74. Harrison, Inc. acquires 100% of the voting stock of Rhine Company on

January 1, 2010 for $400,000 cash. A contingent payment of $16,500 will be paid

on April 15, 2011 if Rhine generates cash flows from operations of $27,000 or

more in the next year. Harrison estimates that there is a 20% probability that

Rhine will generate at least $27,000 next year, and uses an interest rate of 5% to

incorporate the time value of money. The fair value of $16,500 at 5%, using a

probability weighted approach, is $3,142.

What will Harrison record as its Investment in Rhine on January 1, 2010?

75. Harrison, Inc. acquires 100% of the voting stock of Rhine Company on

January 1, 2010 for $400,000 cash. A contingent payment of $16,500 will be paid

on April 15, 2011 if Rhine generates cash flows from operations of $27,000 or

more in the next year. Harrison estimates that there is a 20% probability that

Rhine will generate at least $27,000 next year, and uses an interest rate of 5% to

incorporate the time value of money. The fair value of $16,500 at 5%, using a

probability weighted approach, is $3,142.

Assuming Rhine generates cash flow from operations of $27,200 in 2010, how will

Harrison record the $16,500 payment of cash on April 15, 2011 in satisfaction of

its contingent obligation?

76. Harrison, Inc. acquires 100% of the voting stock of Rhine Company on

January 1, 2010 for $400,000 cash. A contingent payment of $16,500 will be paid

on April 15, 2011 if Rhine generates cash flows from operations of $27,000 or

more in the next year. Harrison estimates that there is a 20% probability that

Rhine will generate at least $27,000 next year, and uses an interest rate of 5% to

incorporate the time value of money. The fair value of $16,500 at 5%, using a

probability weighted approach, is $3,142.

When recording consideration transferred for the acquisition of Rhine on January

1, 2010, Harrison will record a contingent performance obligation in the amount

of:

77. Beatty, Inc. acquires 100% of the voting stock of Gataux Company on

January 1, 2010 for $500,000 cash. A contingent payment of $12,000 will be paid

on April 1, 2011 if Gataux generates cash flows from operations of $26,500 or

more in the next year. Beatty estimates that there is a 30% probability that

Gataux will generate at least $26,500 next year, and uses an interest rate of 4% to

incorporate the time value of money. The fair value of $12,000 at 4%, using a

probability weighted approach, is $3,461.

What will Beatty record as its Investment in Gataux on January 1, 2010?

78. Beatty, Inc. acquires 100% of the voting stock of Gataux Company on

January 1, 2010 for $500,000 cash. A contingent payment of $12,000 will be paid

on April 1, 2011 if Gataux generates cash flows from operations of $26,500 or

more in the next year. Beatty estimates that there is a 30% probability that

Gataux will generate at least $26,500 next year, and uses an interest rate of 4% to

incorporate the time value of money. The fair value of $12,000 at 4%, using a

probability weighted approach, is $3,461.

Assuming Gataux generates cash flow from operations of $27,200 in 2010, how

will Beatty record the $12,000 payment of cash on April 1, 2011 in satisfaction of

its contingent obligation?

79. Beatty, Inc. acquires 100% of the voting stock of Gataux Company on

January 1, 2010 for $500,000 cash. A contingent payment of $12,000 will be paid

on April 1, 2011 if Gataux generates cash flows from operations of $26,500 or

more in the next year. Beatty estimates that there is a 30% probability that

Gataux will generate at least $26,500 next year, and uses an interest rate of 4% to

incorporate the time value of money. The fair value of $12,000 at 4%, using a

probability weighted approach, is $3,461.

Beatty, Inc. acquires 100% of the voting stock of Gataux Company on January 1,

2010 for $500,000 cash. A contingent payment of $12,000 will be paid on April 1,

2011 if Gataux generates cash flows from operations of $26,500 or more in the

next year. Beatty estimates that there is a 30% probability that Gataux will

generate at least $26,500 next year, and uses an interest rate of 4% to

incorporate the time value of money. The fair value of $12,000 at 4%, using a

probability weighted approach, is $3,461.

When recording consideration transferred for the acquisition of Gataux on

January 1, 2010, Beatty will record a contingent performance obligation in the

amount of:

80. Prince Company acquires Duchess, Inc. on January 1, 2009. The

consideration transferred exceeds the fair value of Duchess’ net assets. On that

date, Prince has a building with a book value of $1,200,000 and a fair value of

$1,500,000. Duchess has a building with a book value of $400,000 and fair value

of $500,000.

If push-down accounting is used, what amounts in the Building account appear in

Duchess’ separate balance sheet and in the consolidated balance sheet

immediately after acquisition?

81. Prince Company acquires Duchess, Inc. on January 1, 2009. The

consideration transferred exceeds the fair value of Duchess’ net assets. On that

date, Prince has a building with a book value of $1,200,000 and a fair value of

$1,500,000. Duchess has a building with a book value of $400,000 and fair value

of $500,000.

If push-down accounting is not used, what amounts in the Building account

appear on Duchess’ separate balance sheet and on the consolidated balance

sheet immediately after acquisition?

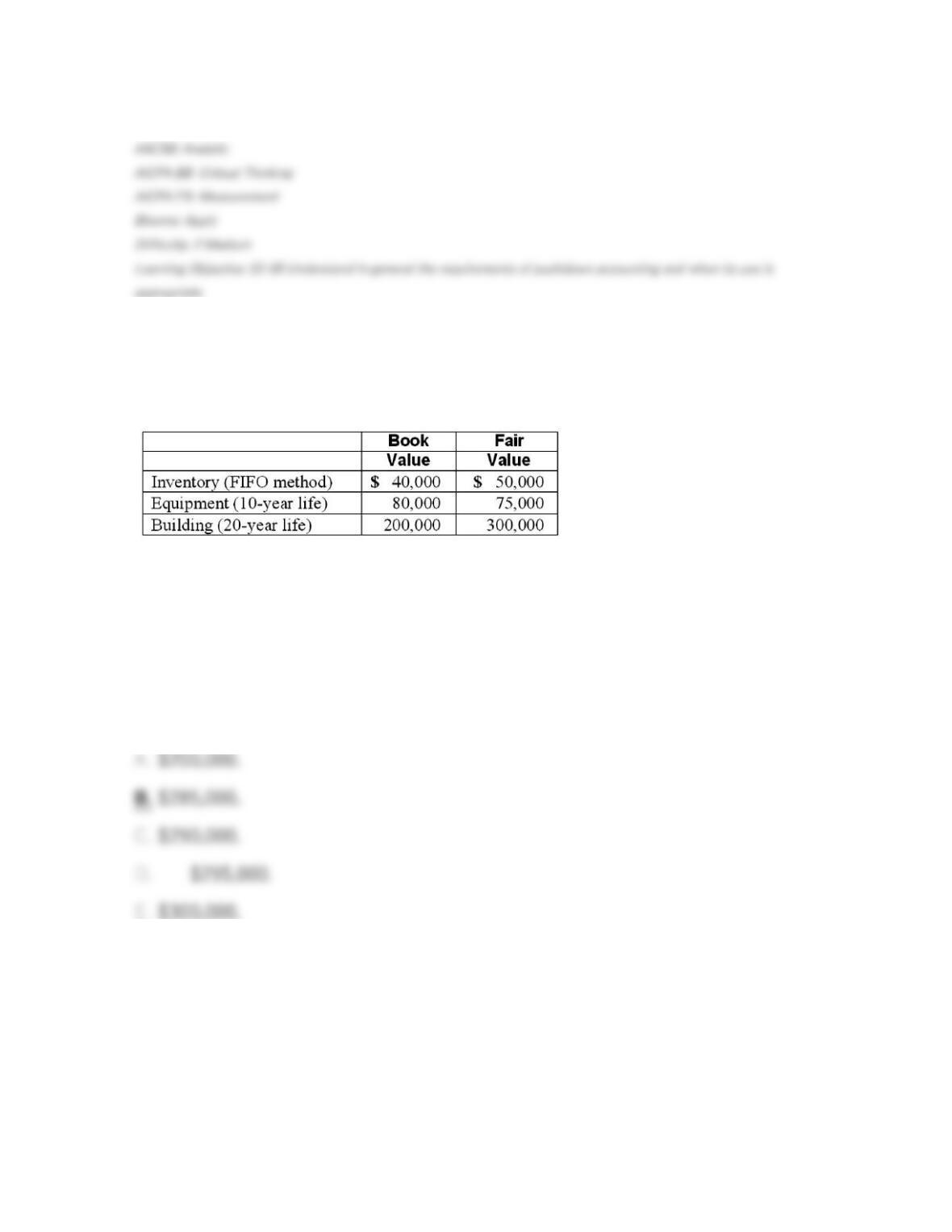

82. Watkins, Inc. acquires all of the outstanding stock of Glen Corporation on

January 1, 2010. At that date, Glen owns only three assets and has no liabilities:

If Watkins pays $450,000 in cash for Glen, what amount would be represented as

the subsidiary’s Building in a consolidation at December 31, 2012, assuming the

book value of the building at that date is still $200,000?

83. Watkins, Inc. acquires all of the outstanding stock of Glen Corporation on

January 1, 2010. At that date, Glen owns only three assets and has no liabilities:

If Watkins pays $400,000 in cash for Glen, what amount would be represented as

the subsidiary’s Building in a consolidation at December 31, 2012, assuming the

book value of the building at that date is still $200,000?

84. Watkins, Inc. acquires all of the outstanding stock of Glen Corporation on

January 1, 2010. At that date, Glen owns only three assets and has no liabilities:

If Watkins pays $450,000 in cash for Glen, what amount would be represented as

the subsidiary’s Equipment in a consolidation at December 31, 2012, assuming

the book value of the equipment at that date is still $80,000?

85. Watkins, Inc. acquires all of the outstanding stock of Glen Corporation on

January 1, 2010. At that date, Glen owns only three assets and has no liabilities:

If Watkins pays $450,000 in cash for Glen, what acquisition-date fair value

allocation, net of amortization, should be attributed to the subsidiary’s Equipment

in consolidation at December 31, 2012?

86. Watkins, Inc. acquires all of the outstanding stock of Glen Corporation on

January 1, 2010. At that date, Glen owns only three assets and has no liabilities:

If Watkins pays $300,000 in cash for Glen, at what amount would the subsidiary’s

Building be represented in a January 2, 2010 consolidation?

87. Watkins, Inc. acquires all of the outstanding stock of Glen Corporation on

January 1, 2010. At that date, Glen owns only three assets and has no liabilities:

If Watkins pays $450,000 in cash for Glen, at what amount would Glen’s Inventory

acquired be represented in a December 31, 2010 consolidated balance sheet?

88. Watkins, Inc. acquires all of the outstanding stock of Glen Corporation on

January 1, 2010. At that date, Glen owns only three assets and has no liabilities:

If Watkins pays $450,000 in cash for Glen, and Glen earns $50,000 in net income

and pays $20,000 in dividends during 2010, what amount would be reflected in

consolidated net income for 2010 as a result of the acquisition?

89. According to the FASB ASC regarding the testing procedures for Goodwill

Impairment, the proper procedure for conducting impairment testing is:

90. When is a goodwill impairment loss recognized?

91. For an acquisition when the subsidiary retains its incorporation, which

method of internal recordkeeping is the easiest for the parent to use?

92. For an acquisition when the subsidiary retains its incorporation, which

method of internal recordkeeping gives the most accurate portrayal of the

accounting results for the entire business combination?

93. For an acquisition when the subsidiary maintains its incorporation, under

the partial equity method, what adjustments are made to the balance of the

investment account?