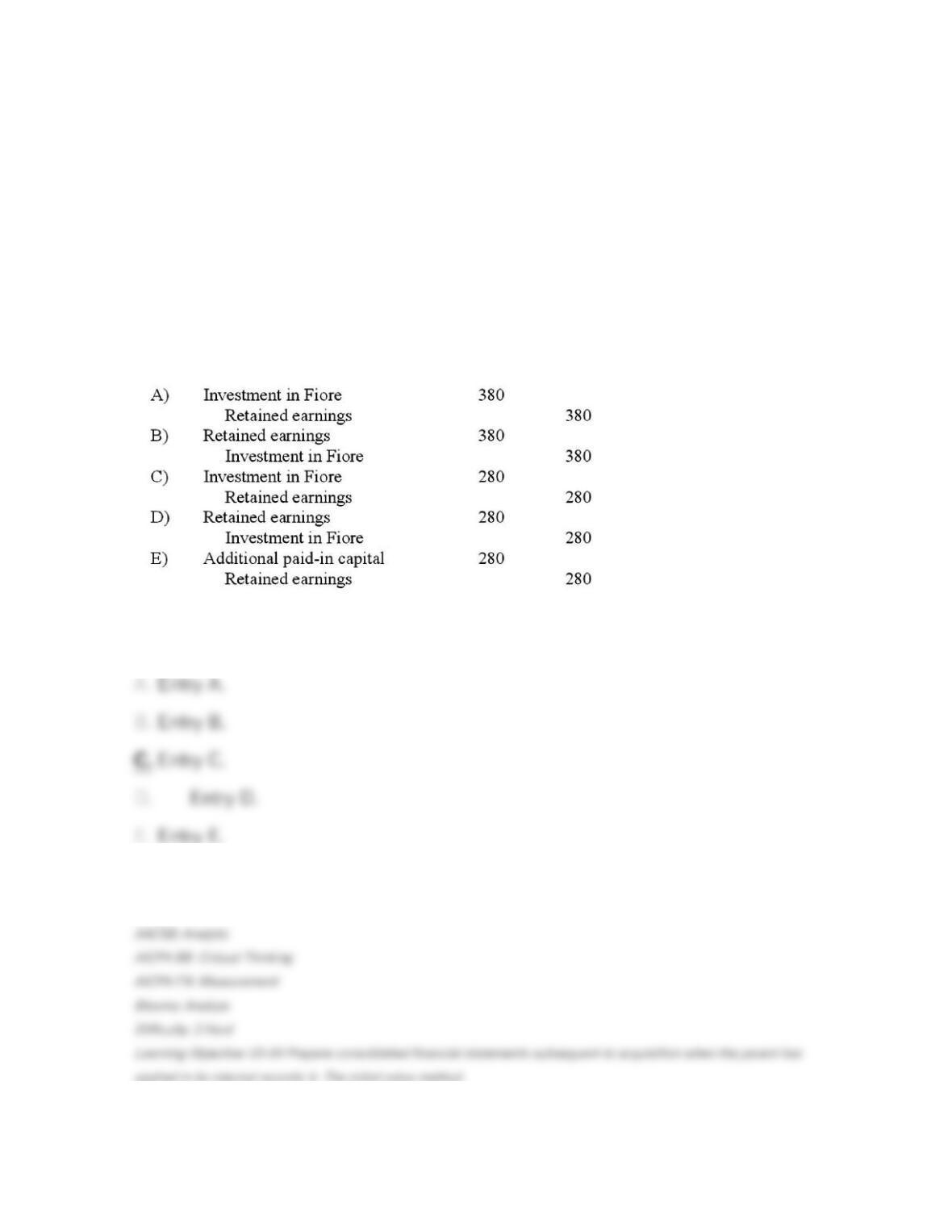

53. Kaye Company acquired 100% of Fiore Company on January 1, 2011. Kaye

paid $1,000 excess consideration over book value which is being amortized at $20

per year. Fiore reported net income of $400 in 2011 and paid dividends of $100.

Assume the initial value method is used. In the year subsequent to acquisition,

what additional worksheet entry must be made for consolidation purposes that is

not required for the equity method?

54. Hoyt Corporation agreed to the following terms in order to acquire the net

assets of Brown Company on January 1, 2011:

(1.) To issue 400 shares of common stock ($10 par) with a fair value of $45 per

share.

(2.) To assume Brown’s liabilities which have a fair value of $1,500.

On the date of acquisition, the consideration transferred for Hoyt’s acquisition of

Brown would be

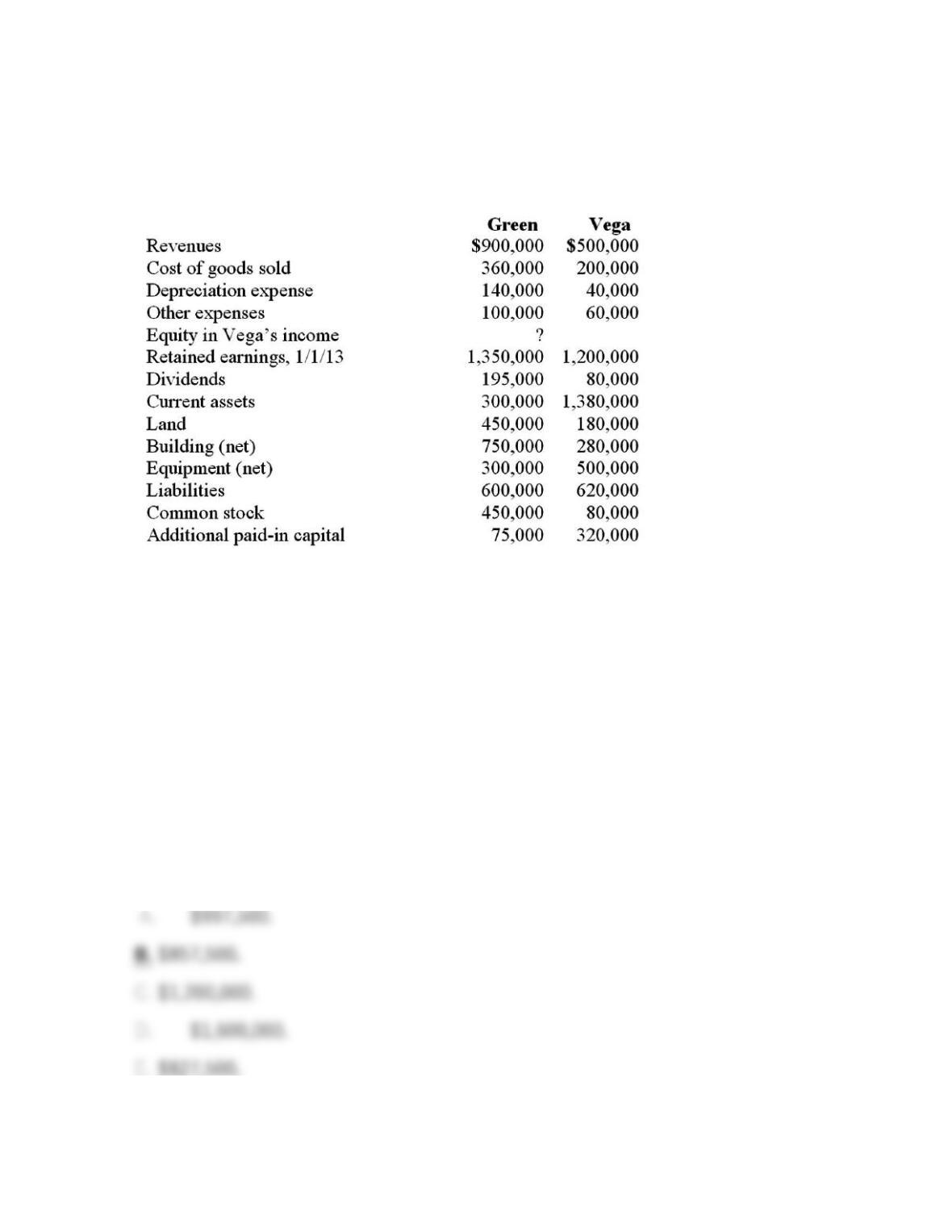

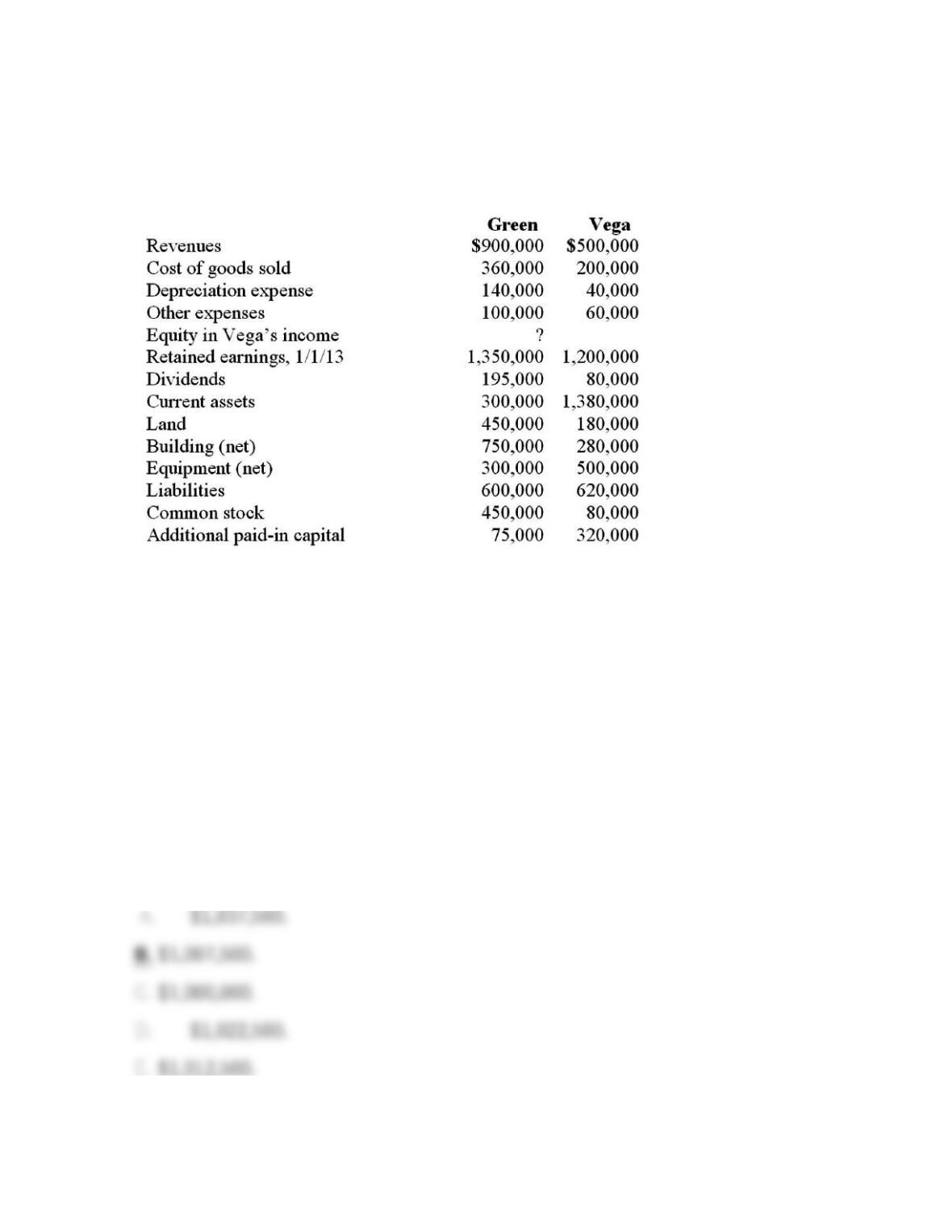

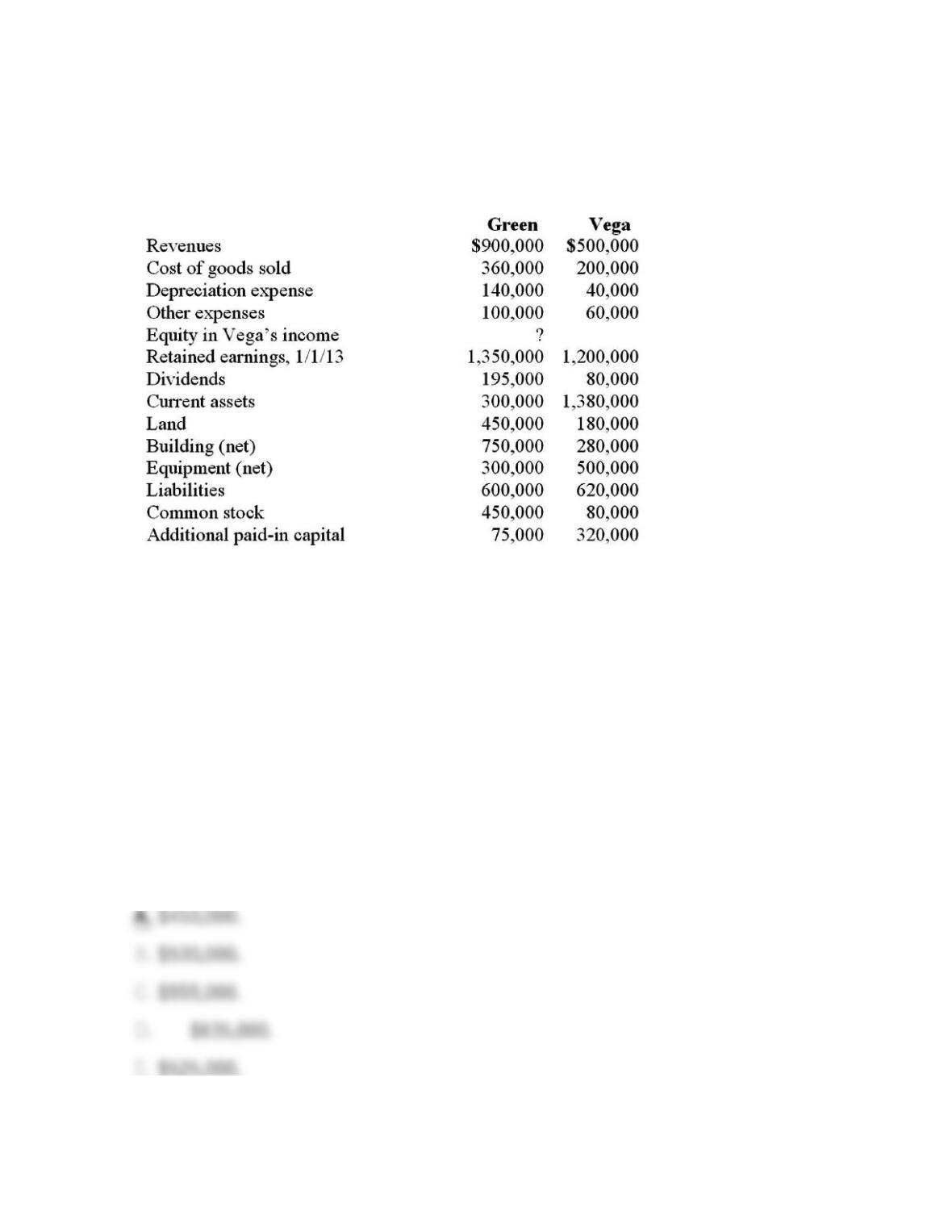

55. Following are selected accounts for Green Corporation and Vega Company

as of December 31, 2013. Several of Green’s accounts have been omitted.

Green acquired 100% of Vega on January 1, 2009, by issuing 10,500 shares of its

$10 par value common stock with a fair value of $95 per share. On January 1,

2009, Vega’s land was undervalued by $40,000, its buildings were overvalued by

$30,000, and equipment was undervalued by $80,000. The buildings have a 20–

year life and the equipment has a 10-year life. $50,000 was attributed to an

unrecorded trademark with a 16-year remaining life. There was no goodwill

associated with this investment.

Compute the book value of Vega at January 1, 2009.

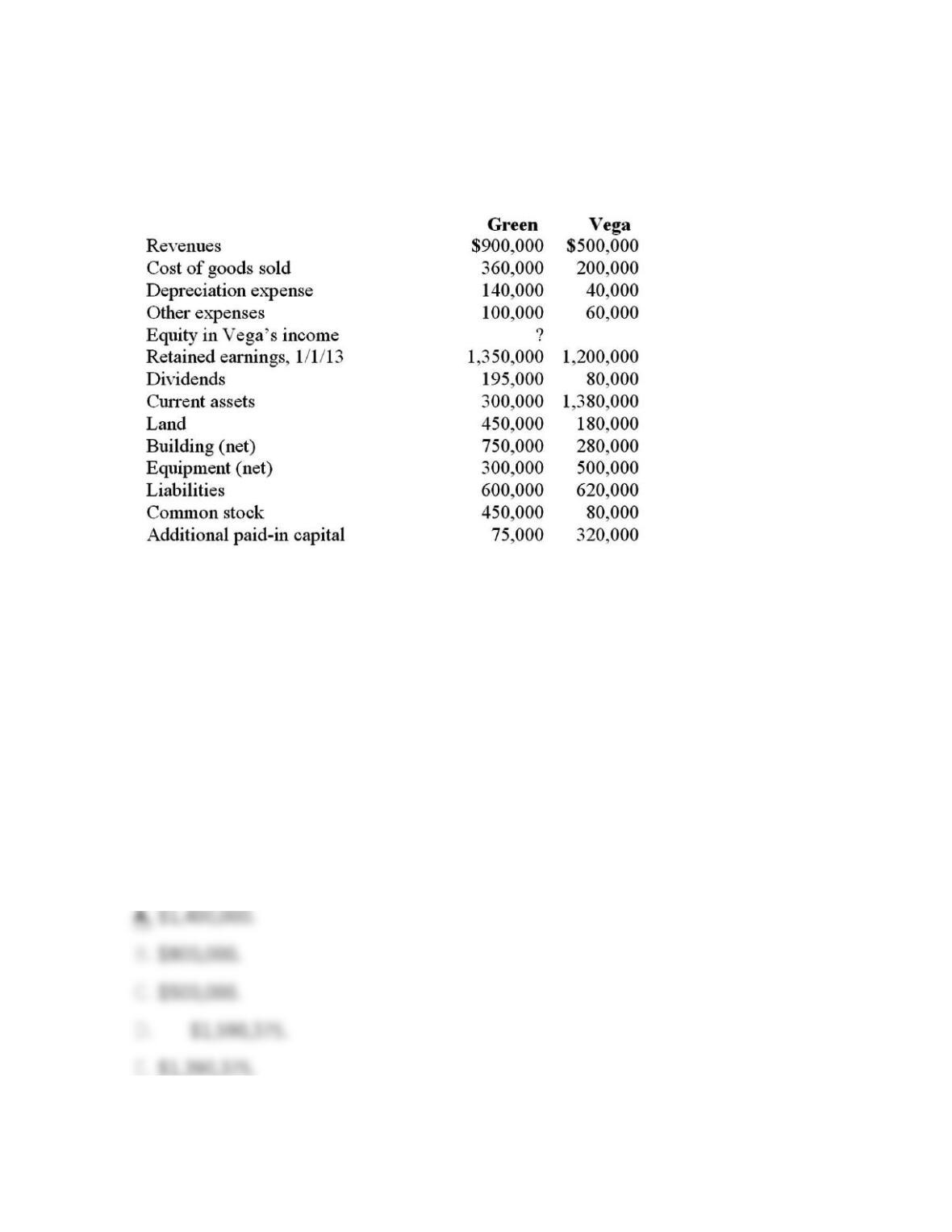

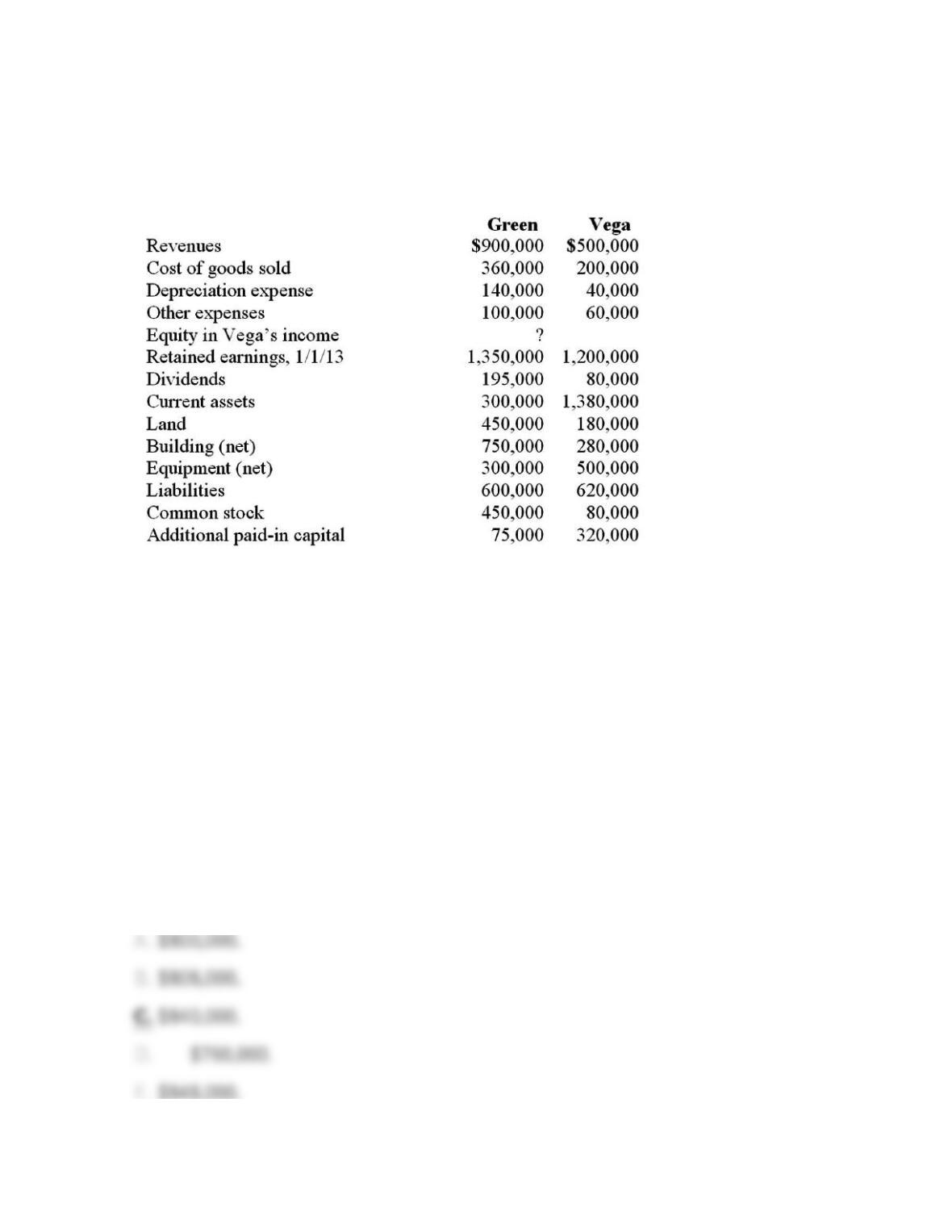

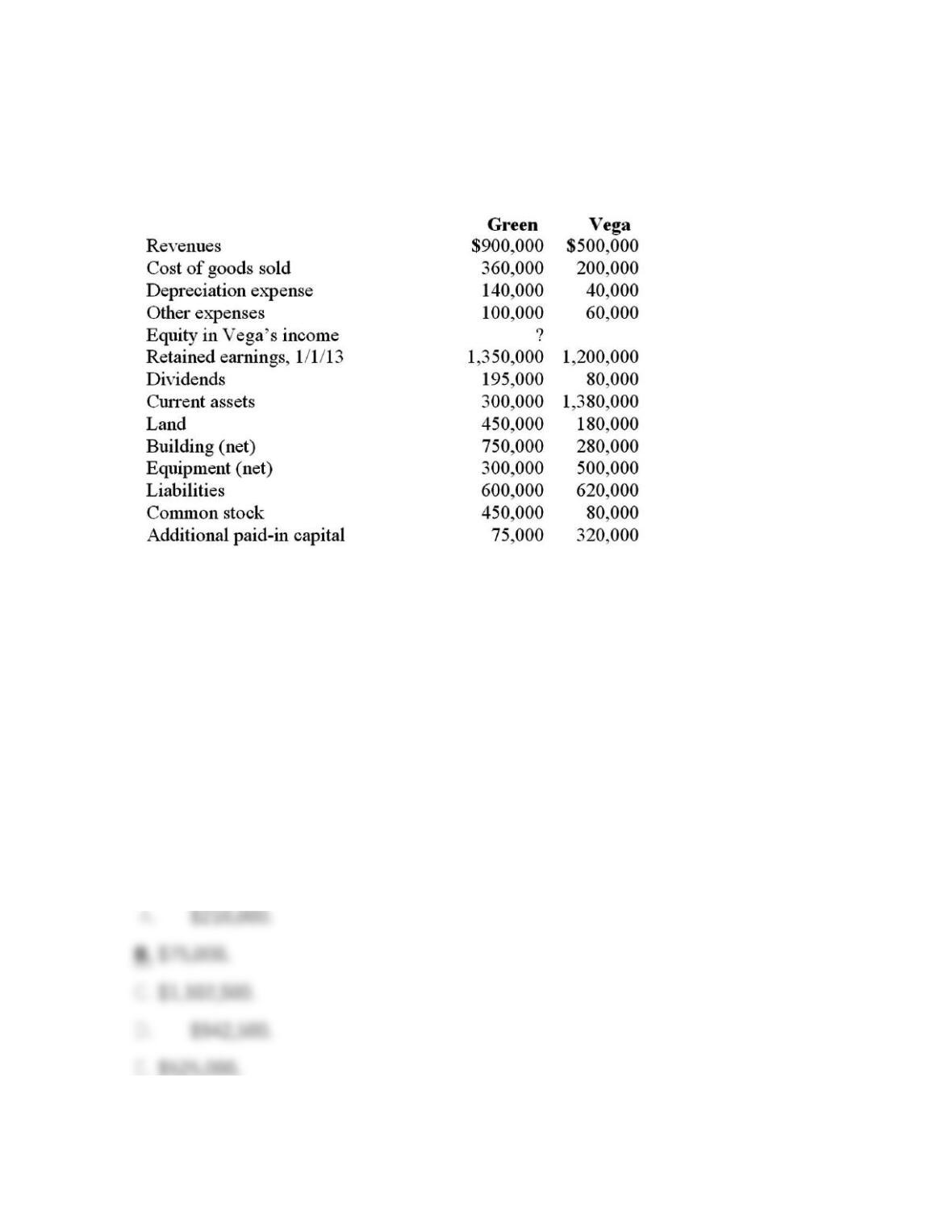

56. Following are selected accounts for Green Corporation and Vega Company

as of December 31, 2013. Several of Green’s accounts have been omitted.

Green acquired 100% of Vega on January 1, 2009, by issuing 10,500 shares of its

$10 par value common stock with a fair value of $95 per share. On January 1,

2009, Vega’s land was undervalued by $40,000, its buildings were overvalued by

$30,000, and equipment was undervalued by $80,000. The buildings have a 20–

year life and the equipment has a 10-year life. $50,000 was attributed to an

unrecorded trademark with a 16-year remaining life. There was no goodwill

associated with this investment.

Compute the December 31, 2013, consolidated revenues.

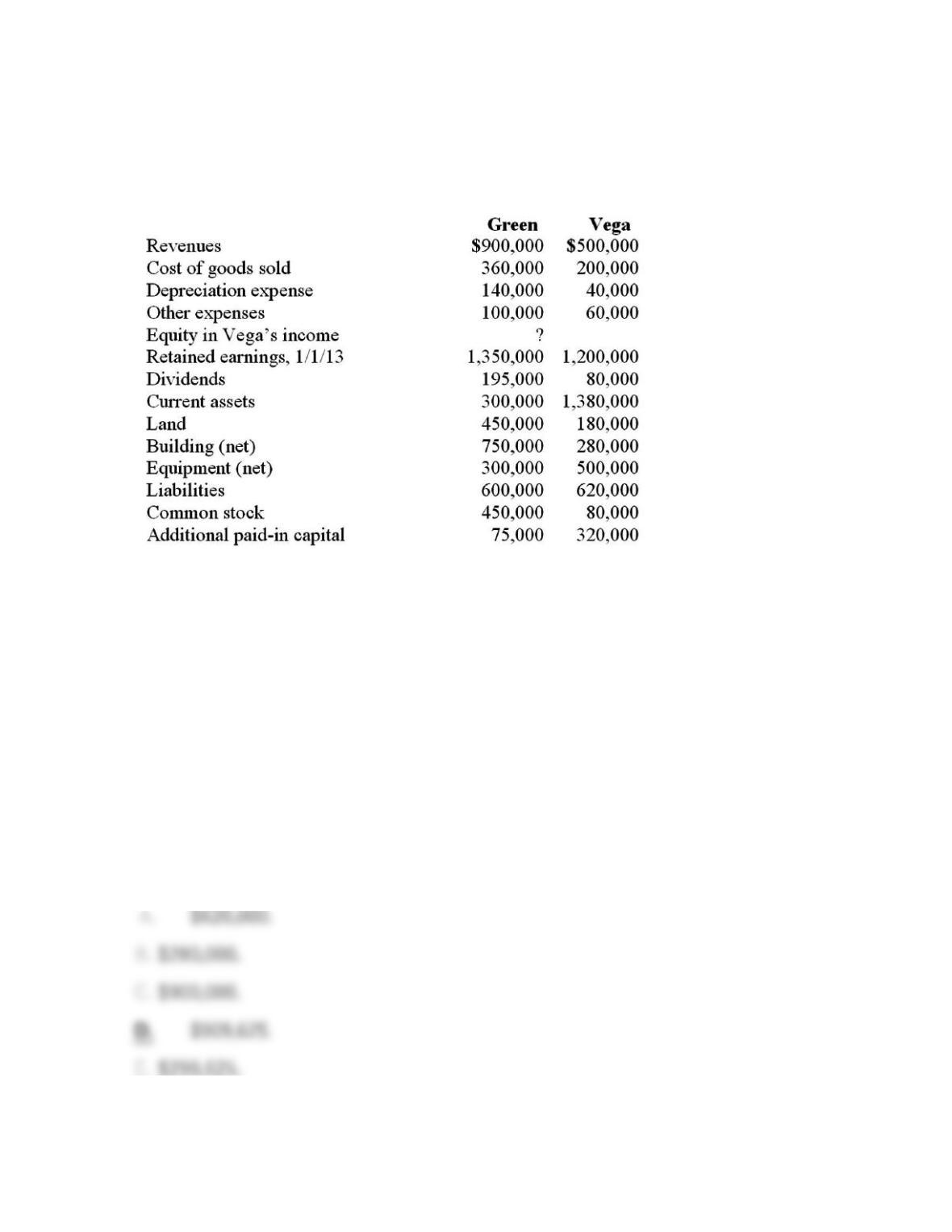

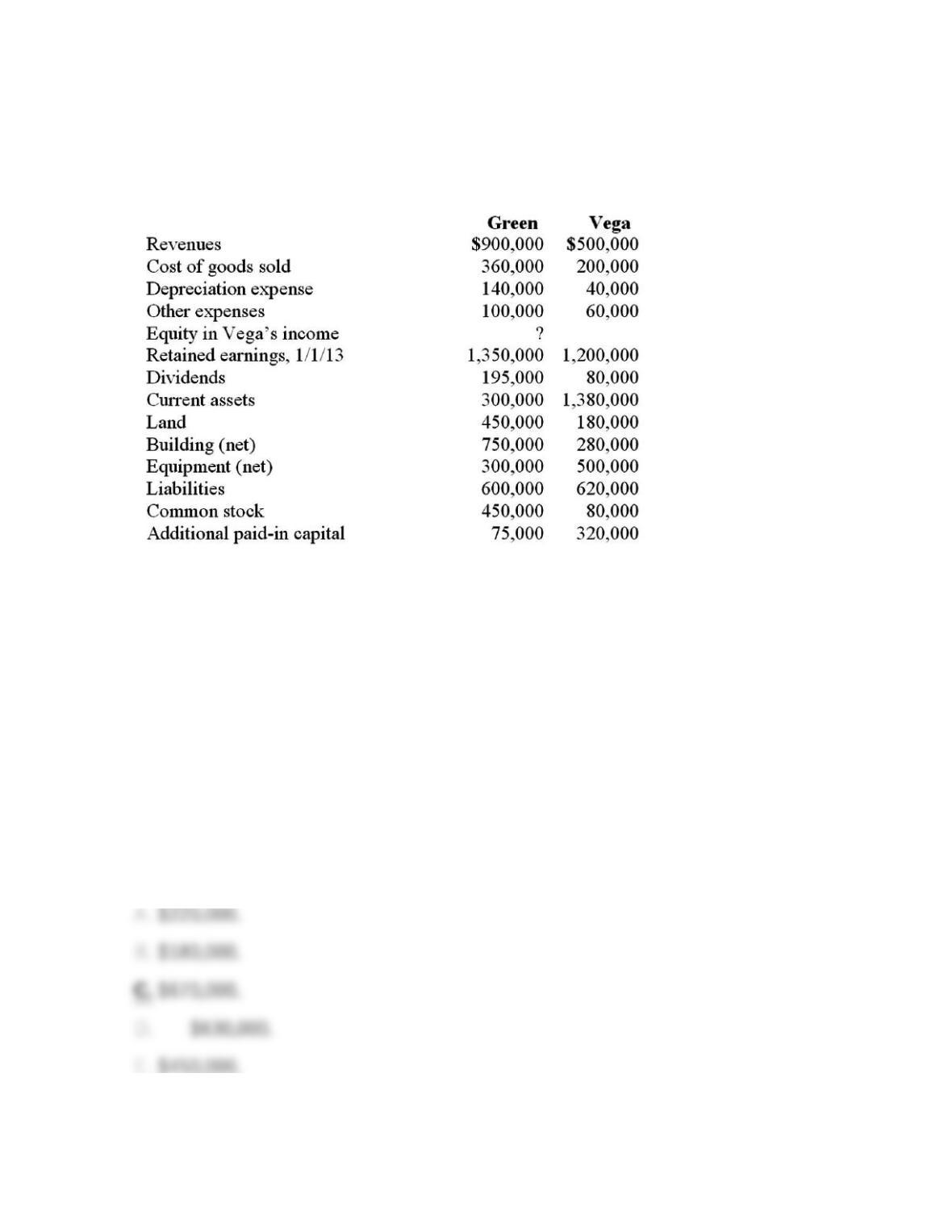

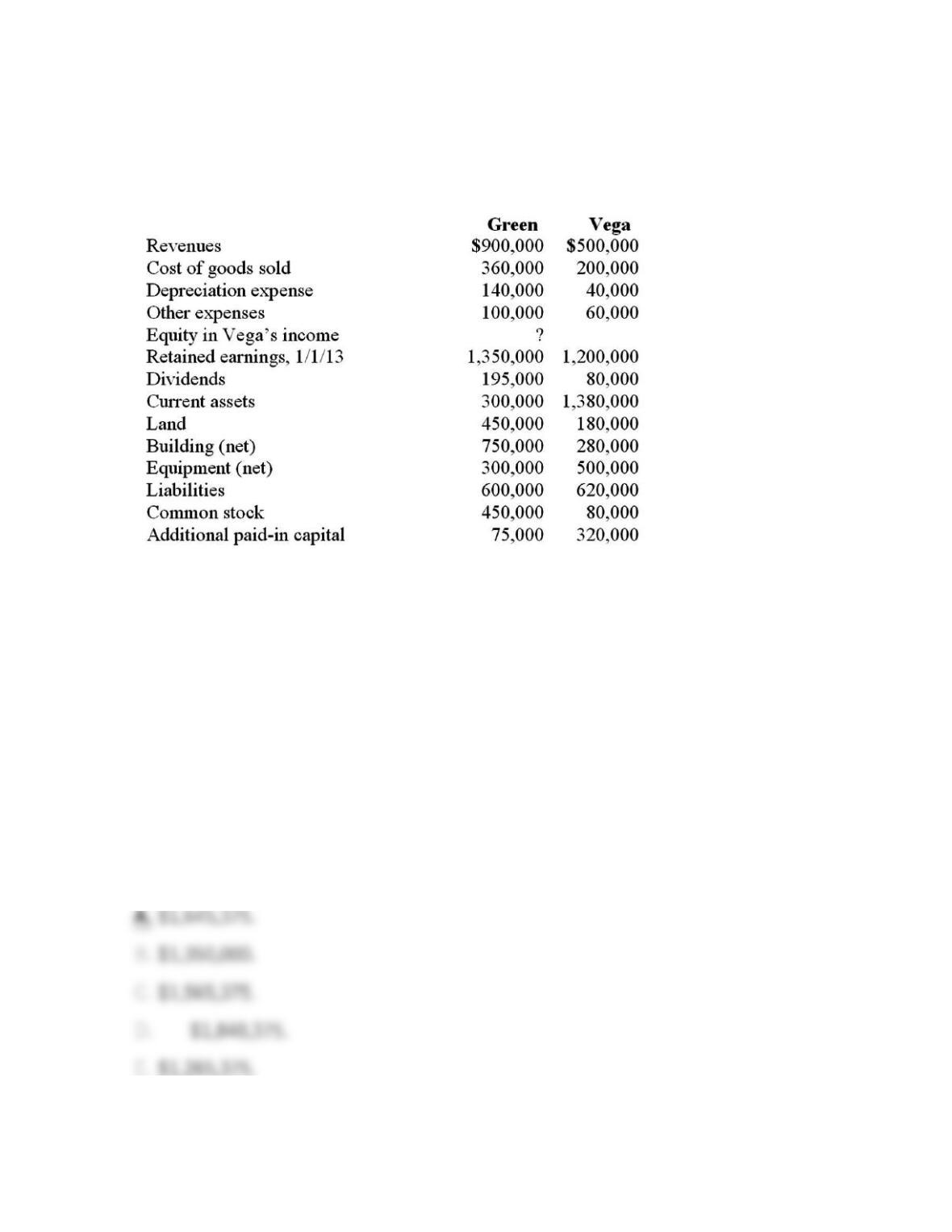

57. Following are selected accounts for Green Corporation and Vega Company

as of December 31, 2013. Several of Green’s accounts have been omitted.

Green acquired 100% of Vega on January 1, 2009, by issuing 10,500 shares of its

$10 par value common stock with a fair value of $95 per share. On January 1,

2009, Vega’s land was undervalued by $40,000, its buildings were overvalued by

$30,000, and equipment was undervalued by $80,000. The buildings have a 20–

year life and the equipment has a 10-year life. $50,000 was attributed to an

unrecorded trademark with a 16-year remaining life. There was no goodwill

associated with this investment.

Compute the December 31, 2013, consolidated total expenses.

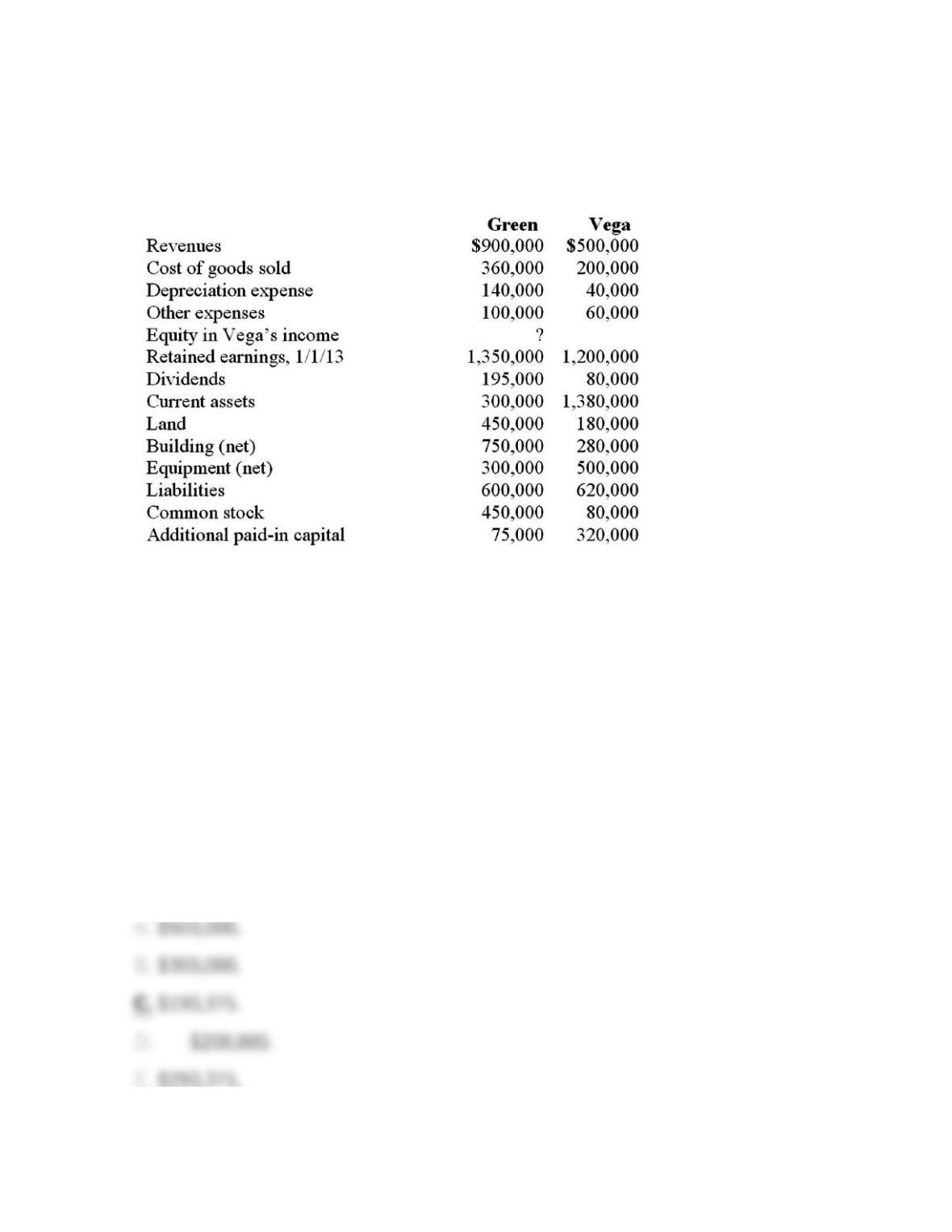

58. Following are selected accounts for Green Corporation and Vega Company

as of December 31, 2013. Several of Green’s accounts have been omitted.

Green acquired 100% of Vega on January 1, 2009, by issuing 10,500 shares of its

$10 par value common stock with a fair value of $95 per share. On January 1,

2009, Vega’s land was undervalued by $40,000, its buildings were overvalued by

$30,000, and equipment was undervalued by $80,000. The buildings have a 20–

year life and the equipment has a 10-year life. $50,000 was attributed to an

unrecorded trademark with a 16-year remaining life. There was no goodwill

associated with this investment.

Compute the December 31, 2013, consolidated buildings.

59. Following are selected accounts for Green Corporation and Vega Company

as of December 31, 2013. Several of Green’s accounts have been omitted.

Green acquired 100% of Vega on January 1, 2009, by issuing 10,500 shares of its

$10 par value common stock with a fair value of $95 per share. On January 1,

2009, Vega’s land was undervalued by $40,000, its buildings were overvalued by

$30,000, and equipment was undervalued by $80,000. The buildings have a 20-

year life and the equipment has a 10-year life. $50,000 was attributed to an

unrecorded trademark with a 16-year remaining life. There was no goodwill

associated with this investment.

Compute the December 31, 2013, consolidated equipment.

60. Following are selected accounts for Green Corporation and Vega Company

as of December 31, 2013. Several of Green’s accounts have been omitted.

Green acquired 100% of Vega on January 1, 2009, by issuing 10,500 shares of its

$10 par value common stock with a fair value of $95 per share. On January 1,

2009, Vega’s land was undervalued by $40,000, its buildings were overvalued by

$30,000, and equipment was undervalued by $80,000. The buildings have a 20–

year life and the equipment has a 10-year life. $50,000 was attributed to an

unrecorded trademark with a 16-year remaining life. There was no goodwill

associated with this investment.

Compute the December 31, 2013, consolidated land.

61. Following are selected accounts for Green Corporation and Vega Company

as of December 31, 2013. Several of Green’s accounts have been omitted.

Green acquired 100% of Vega on January 1, 2009, by issuing 10,500 shares of its

$10 par value common stock with a fair value of $95 per share. On January 1,

2009, Vega’s land was undervalued by $40,000, its buildings were overvalued by

$30,000, and equipment was undervalued by $80,000. The buildings have a 20–

year life and the equipment has a 10-year life. $50,000 was attributed to an

unrecorded trademark with a 16-year remaining life. There was no goodwill

associated with this investment.

Compute the December 31, 2013, consolidated trademark.

62. Following are selected accounts for Green Corporation and Vega Company

as of December 31, 2013. Several of Green’s accounts have been omitted.

Green acquired 100% of Vega on January 1, 2009, by issuing 10,500 shares of its

$10 par value common stock with a fair value of $95 per share. On January 1,

2009, Vega’s land was undervalued by $40,000, its buildings were overvalued by

$30,000, and equipment was undervalued by $80,000. The buildings have a 20-

year life and the equipment has a 10-year life. $50,000 was attributed to an

unrecorded trademark with a 16-year remaining life. There was no goodwill

associated with this investment.

Compute the December 31, 2013, consolidated common stock.

63. Following are selected accounts for Green Corporation and Vega Company

as of December 31, 2013. Several of Green’s accounts have been omitted.

Green acquired 100% of Vega on January 1, 2009, by issuing 10,500 shares of its

$10 par value common stock with a fair value of $95 per share. On January 1,

2009, Vega’s land was undervalued by $40,000, its buildings were overvalued by

$30,000, and equipment was undervalued by $80,000. The buildings have a 20–

year life and the equipment has a 10-year life. $50,000 was attributed to an

unrecorded trademark with a 16-year remaining life. There was no goodwill

associated with this investment.

Compute the December 31, 2013, consolidated additional paid-in capital.

64. Following are selected accounts for Green Corporation and Vega Company

as of December 31, 2013. Several of Green’s accounts have been omitted.

Green acquired 100% of Vega on January 1, 2009, by issuing 10,500 shares of its

$10 par value common stock with a fair value of $95 per share. On January 1,

2009, Vega’s land was undervalued by $40,000, its buildings were overvalued by

$30,000, and equipment was undervalued by $80,000. The buildings have a 20–

year life and the equipment has a 10-year life. $50,000 was attributed to an

unrecorded trademark with a 16-year remaining life. There was no goodwill

associated with this investment.

Compute the December 31, 2013 consolidated retained earnings.

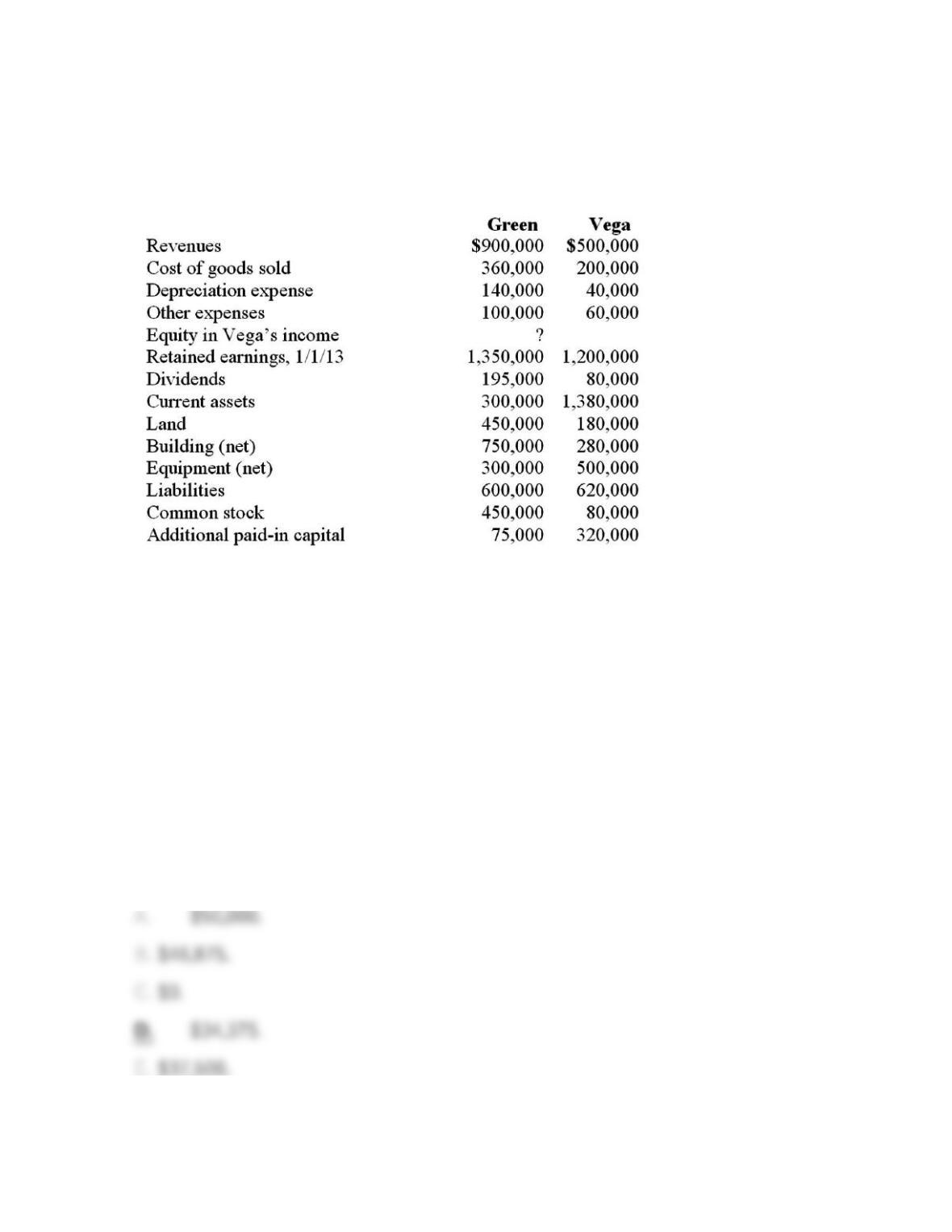

65. Following are selected accounts for Green Corporation and Vega Company

as of December 31, 2013. Several of Green’s accounts have been omitted.

Green acquired 100% of Vega on January 1, 2009, by issuing 10,500 shares of its

$10 par value common stock with a fair value of $95 per share. On January 1,

2009, Vega’s land was undervalued by $40,000, its buildings were overvalued by

$30,000, and equipment was undervalued by $80,000. The buildings have a 20-

year life and the equipment has a 10-year life. $50,000 was attributed to an

unrecorded trademark with a 16-year remaining life. There was no goodwill

associated with this investment.

Compute the equity in Vega’s income to be included in Green’s consolidated

income statement for 2013.

66. One company acquires another company in a combination accounted for as

an acquisition. The acquiring company decides to apply the initial value method in

accounting for the combination. What is one reason the acquiring company might

have made this decision?

67. One company acquires another company in a combination accounted for as

an acquisition. The acquiring company decides to apply the equity method in

accounting for the combination. What is one reason the acquiring company might

have made this decision?

68. When is a goodwill impairment loss recognized?

69. Which of the following will result in the recognition of an impairment loss

on goodwill?

70. Goehler, Inc. acquires all of the voting stock of Kenneth, Inc. on January 4,

2010, at an amount in excess of Kenneth’s fair value. On that date, Kenneth has

equipment with a book value of $90,000 and a fair value of $120,000 (10-year

remaining life). Goehler has equipment with a book value of $800,000 and a fair

value of $1,200,000 (10-year remaining life). On December 31, 2011, Goehler has

equipment with a book value of $975,000 but a fair value of $1,350,000 and

Kenneth has equipment with a book value of $105,000 but a fair value of

$125,000.

If Goehler applies the

equity method

in accounting for Kenneth, what is the

consolidated balance for the Equipment account as of December 31, 2011?

71. Goehler, Inc. acquires all of the voting stock of Kenneth, Inc. on January 4,

2010, at an amount in excess of Kenneth’s fair value. On that date, Kenneth has

equipment with a book value of $90,000 and a fair value of $120,000 (10-year

remaining life). Goehler has equipment with a book value of $800,000 and a fair

value of $1,200,000 (10-year remaining life). On December 31, 2011, Goehler has

equipment with a book value of $975,000 but a fair value of $1,350,000 and

Kenneth has equipment with a book value of $105,000 but a fair value of

$125,000.

If Goehler applies the

partial equity method

in accounting for Kenneth, what is

the consolidated balance for the Equipment account as of December 31, 2011?

72. Goehler, Inc. acquires all of the voting stock of Kenneth, Inc. on January 4,

2010, at an amount in excess of Kenneth’s fair value. On that date, Kenneth has

equipment with a book value of $90,000 and a fair value of $120,000 (10-year

remaining life). Goehler has equipment with a book value of $800,000 and a fair

value of $1,200,000 (10-year remaining life). On December 31, 2011, Goehler has

equipment with a book value of $975,000 but a fair value of $1,350,000 and

Kenneth has equipment with a book value of $105,000 but a fair value of

$125,000.

If Goehler applies the

initial value method

in accounting for Kenneth, what is the

consolidated balance for the Equipment account as of December 31, 2011?