71. Of the following six accounts, which ones have temporary balances?

(1) Service Revenue

(2) Dividends

(3) Salaries Expense

(4) Common Stock

(5) Retained Earnings

(6) Cash

72. The ending Retained Earnings balance of Juan’s Mexican Restaurant chain increased by

$3.2 million from the beginning of the year. The company declared a dividend of $1.3 million

during the year. What was the net income earned during the year?

73. The Retained Earnings account had a beginning credit balance of $26,000. During the

period, the business had a net loss $12,000, and the company paid dividends of $8,000. The

ending balance in the Retained Earnings account is:

74. Which of the following describes the purpose(s) of closing entries?

75. Which of the following is a permanent account?

76. Which of the following accounts will NOT be involved in closing entries?

77. When a company prepares closing entries, which one of the following is NOT a correct

closing entry?

78. In the first three years of operations, Lindsey Corporation earned net income/loss of –

$150,000, $100,000, and $250,000. At the end of the third year, Lindsey Corporation has a

balance of $120,000 for its Retained Earnings account. What is the total amount of dividends

Lindsey Corporation paid over the three years?

79. For the first three years of operations, the company reports net income of $1,000, $2,000,

and $3,000, and pays dividends of $500, $1,000, and $1,000. What is the balance of retained

earnings at the end of the third year?

80. Which of the following is true concerning temporary and permanent accounts?

81. The closing process includes which of the following?

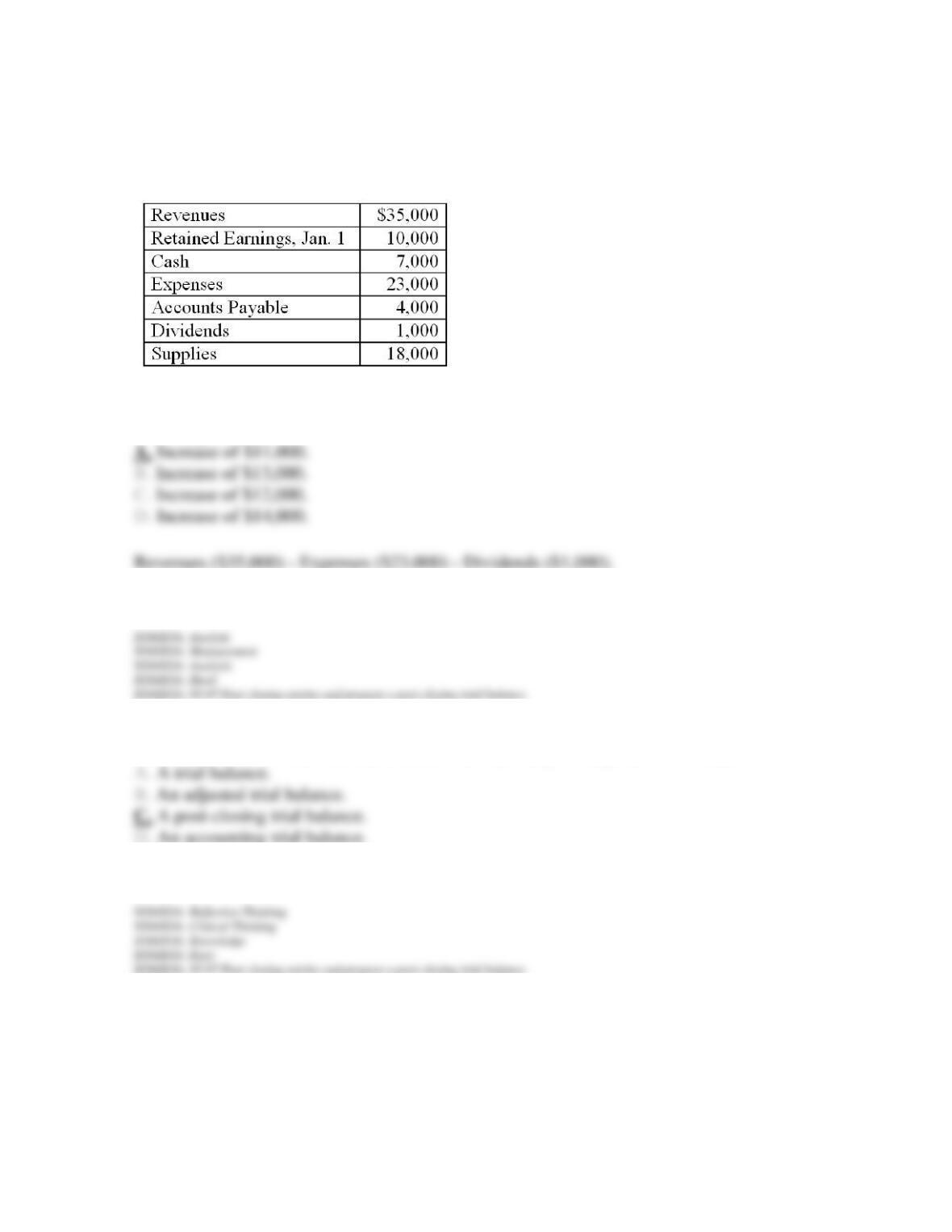

82. Frosty Inc. has the following balances on December 31 prior to closing entries:

Based upon the balances above, what net adjustment would be made to Retained Earnings due

to closing entries?

83. A list of all accounts and their balances after posting closing entries is referred to as:

84. A post-closing trial balance:

85. Which of the following accounts is(are) listed in a post-closing trial balance?

86. Which one of the following accounts would NOT have a balance after closing entries?

87. Accrual-basis accounting involves recording revenues when earned and recording

expenses with their related revenues.

88. The revenue recognition principle states that we record revenue in the period in which we

collect cash.

89. According to the revenue recognition principle, if a company provides services to a

customer in the current year but does not collect cash until the following year, the company

should report the revenue in the current year.

90. Jones Corporation provides services to a customer on June 17, but the customer does not

pay for the services until August 12. According to the revenue recognition principle, Jones

Corporation should record the revenue on August 12.

91. The matching principle states that we recognize expenses in the same period as the

revenues they help to generate.

92. According to the matching principle, if costs associated with producing revenue in the

current year are not paid in cash until the following year, the costs should be expensed in the

current year.

93. Under cash-basis accounting, we record revenues at the time we receive cash and

expenses at the time we pay cash.

94. Under cash-basis accounting, the timing of cash inflows and outflows exactly matches the

reporting of revenues and expenses in the income statement.

95. Under cash-basis accounting, if a company provides services to a customer in the current

year but does not collect cash until the following year, the company should report the revenue

in the current year.

96. Under cash-basis accounting, if costs associated with producing revenue in the current

year are not paid in cash until the following year, the costs should be expensed in the

following year.

97. Because cash-basis accounting violates both the revenue recognition principle and the

matching principle, it is generally not accepted in preparing financial statements.

98. Adjusting entries involve recording events that have occurred but that have not yet been

recorded by the end of the period.

99. Adjusting entries should be prepared after financial statements are prepared.

100. Because adjusting entries allow the proper application of the revenue recognition

principle or the matching principle, they are a necessary part of cash-basis accounting.

101. Prepaid expenses involve payment of cash (or an obligation to pay cash) for the purchase

of an asset before the expense is incurred.

102. Unearned revenues occur when cash is received after the revenue is earned.

103. Accrued expenses involve the payment of cash before recording an expense and a

liability.

104. Accrued revenues involve the receipt of cash after the revenue has been earned and an

asset has been recorded.

105. The adjusting entry for a prepaid expense always includes a debit to an expense account

and a credit to a liability account.

106. The adjusting entry for a prepaid expense has the effect of reducing total assets and

reducing net income.

107. The Supplies account is an example of an accrued expense.

108. Suppose Simeon Company begins the year with $1,000 in supplies, purchases an

additional $5,500 of supplies during the year, and ends the year with $700 in supplies. The

year-end adjusting entry includes Supplies Expense of $7,200.

109. The adjusting entry for an unearned revenue always includes a debit to an asset account

and a credit to a revenue account.

110. The adjusting entry for an unearned revenue has the effects of reducing liabilities and

increasing net income.

111. On November 1, 2012, a company receives $1,800 for services to be provided evenly

over the next six months. The December 31, 2012, adjusting entry for the company would

include a credit to Unearned Revenue for $600.

112. The adjusting entry for an accrued expense always includes a debit to an expense

account and a credit to a liability account.

113. The adjusting entry for an accrued expense has the effects of decreasing net income and

decreasing liabilities.

114. On December 31, 2012, employees who earn $500 per day have worked eight days and

will be paid on January 6, 2013. The adjusting entry on December 31, 2012, includes a debit

to Salaries Expense for $4,000.

115. At December 31, 2012, a company has received, but not paid, a utility bill for $250. The

amount of utility expense for the current period equals $250.

116. The adjusting entry for an accrued revenue always includes a debit to a liability account

and a credit to a revenue account.

117. The adjusting entry for an accrued revenue has the effects of increasing assets and

increasing net income.

118. Adjusting entries are unnecessary for transactions that do not involve revenue or expense

activities, such as selling common stock or paying dividends.

119. Adjusting entries are not necessary when cash is received at the same time revenues are

earned.

120. Adjusting entries are not necessary when cash is paid at the same time expenses are

incurred.

121. A post-closing trial balance is a list of all accounts and their balances after we have

updated account balances for adjusting entries.

122. Once the adjusted trial balance is complete, financial statements are prepared.

123. A classified balance sheet separates assets into current and long-term, and separates

liabilities into current and long-term.

124. Current assets are assets that provide a benefit to a company over more than one year.

125. Long-term assets are assets that provide a benefit to a company for more than one year.

126. Current liabilities are liabilities due within one year.

127. Long-term liabilities are liabilities due in more than one year.

128. Long-term asset categories include investments; property, plant, and equipment; and

intangible assets.

129. The components of retained earnings include assets, expenses, and dividends.

130. Closing entries transfer the balances of all temporary accounts (revenues, expenses, and

dividends) to the balance of the Common Stock account.

131. The closing entry for revenue accounts includes a debit to Retained Earnings and a credit

to all revenue accounts.

132. The closing entry for expense accounts includes a debit to Retained Earnings and a credit

to all expense accounts.

133. The closing entry for dividends includes a debit to the Dividends account and a credit to

Retained Earnings.