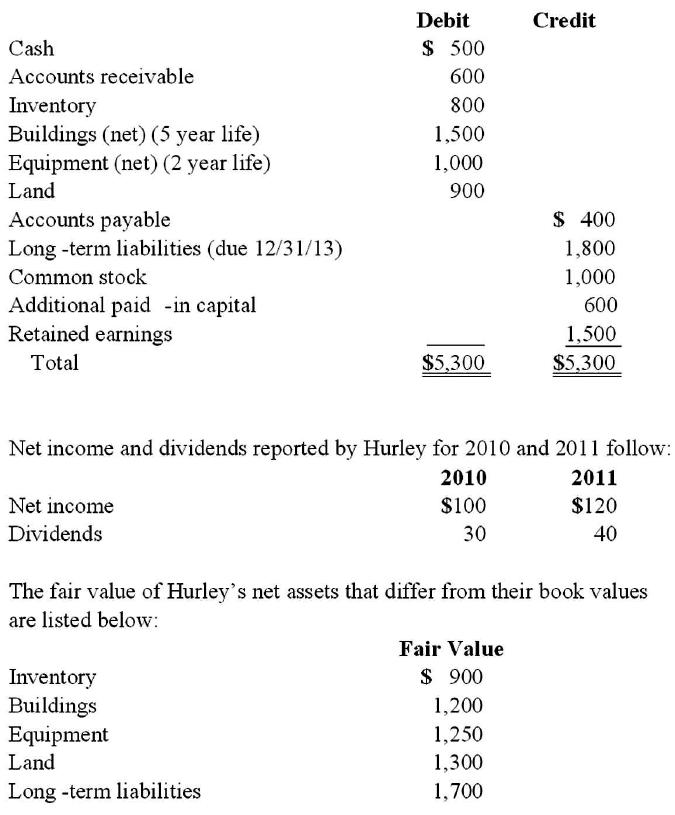

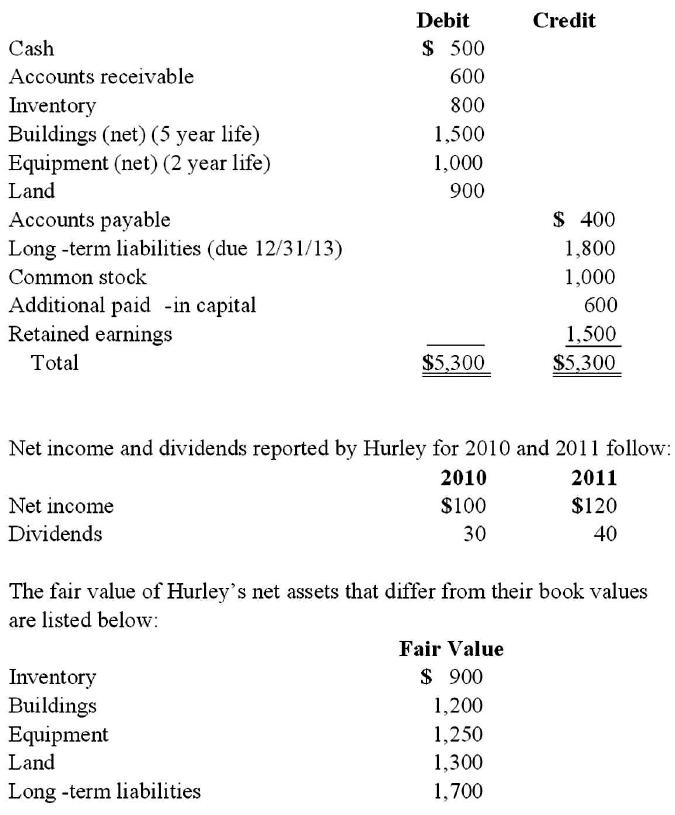

41. Perry Company acquires 100% of the stock of Hurley Corporation on

January 1, 2010, for $3,800 cash. As of that date Hurley has the following trial

balance;

Any excess of consideration transferred over fair value of net assets acquired is

considered goodwill with an indefinite life. FIFO inventory valuation method is

used.

Compute the amount of Hurley’s buildings that would be reported in a December

31, 2010, consolidated balance sheet.

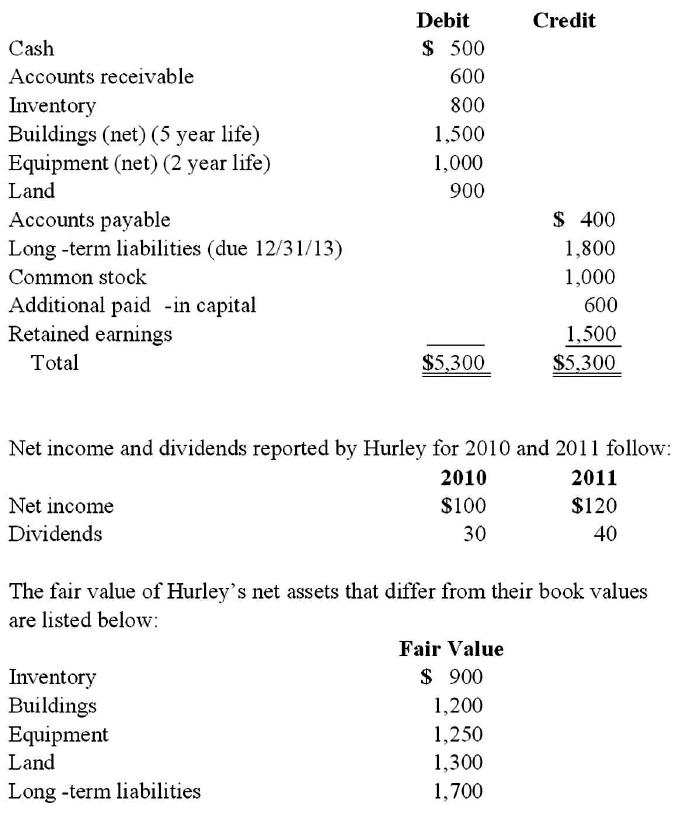

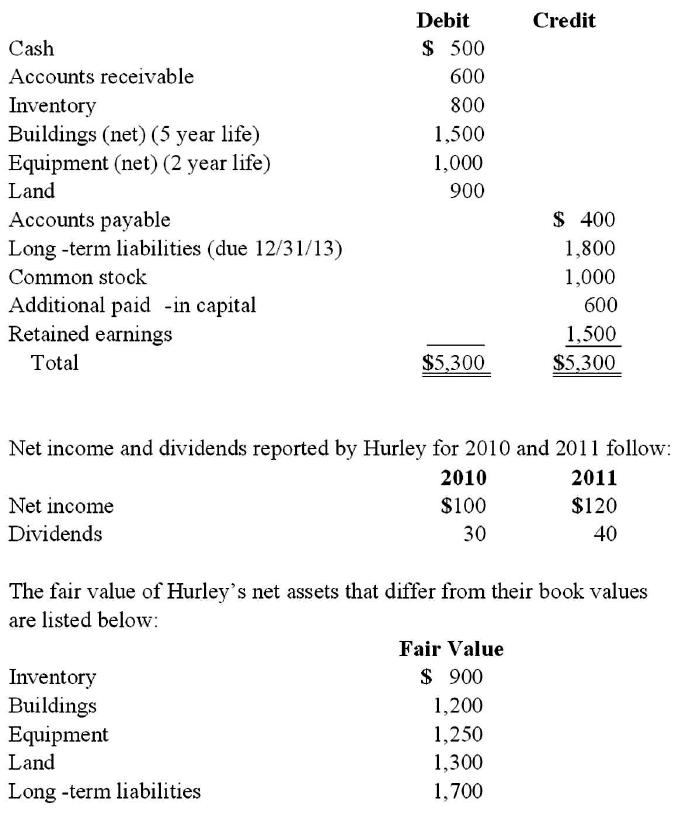

42. Perry Company acquires 100% of the stock of Hurley Corporation on

January 1, 2010, for $3,800 cash. As of that date Hurley has the following trial

balance;

Any excess of consideration transferred over fair value of net assets acquired is

considered goodwill with an indefinite life. FIFO inventory valuation method is

used.

Compute the amount of Hurley’s equipment that would be reported in a

December 31, 2010, consolidated balance sheet.

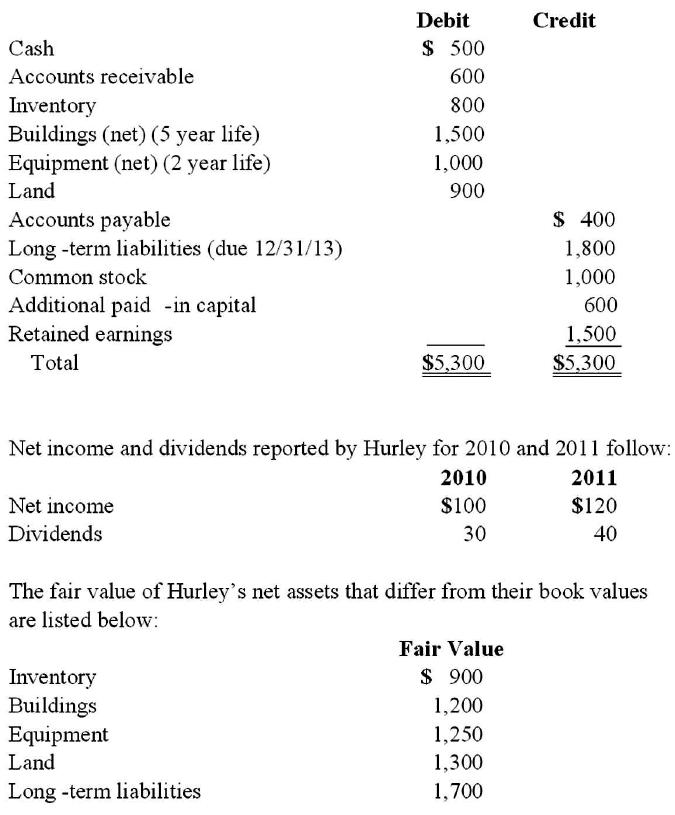

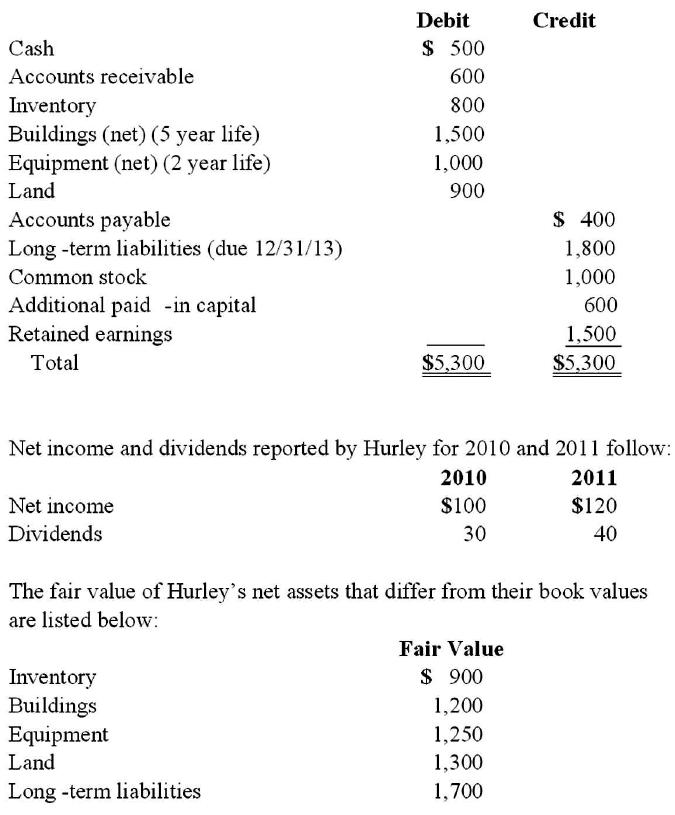

43. Perry Company acquires 100% of the stock of Hurley Corporation on

January 1, 2010, for $3,800 cash. As of that date Hurley has the following trial

balance;

Any excess of consideration transferred over fair value of net assets acquired is

considered goodwill with an indefinite life. FIFO inventory valuation method is

used.

Compute the amount of total expenses reported in an income statement for the

year ended December 31, 2010, in order to recognize acquisition-date allocations

of fair value and book value differences,

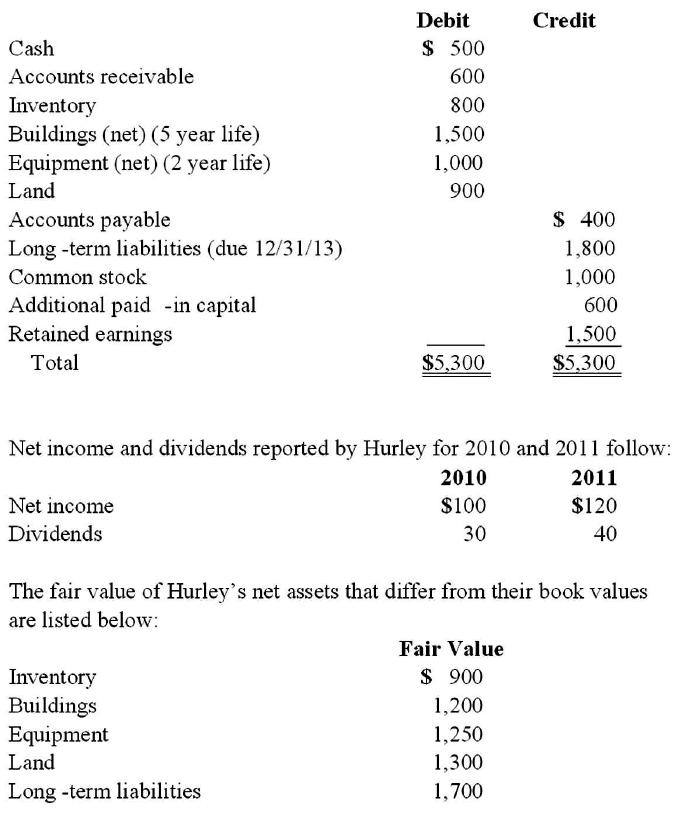

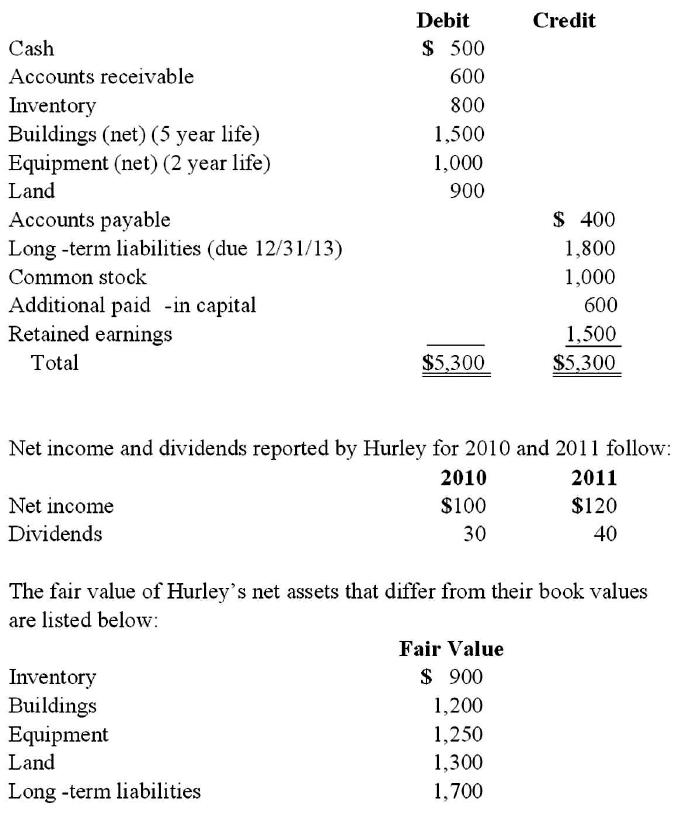

44. Perry Company acquires 100% of the stock of Hurley Corporation on

January 1, 2010, for $3,800 cash. As of that date Hurley has the following trial

balance;

Any excess of consideration transferred over fair value of net assets acquired is

considered goodwill with an indefinite life. FIFO inventory valuation method is

used.

Compute the amount of Hurley’s long-term liabilities that would be reported in a

December 31, 2010, consolidated balance sheet.

45. Perry Company acquires 100% of the stock of Hurley Corporation on

January 1, 2010, for $3,800 cash. As of that date Hurley has the following trial

balance;

Any excess of consideration transferred over fair value of net assets acquired is

considered goodwill with an indefinite life. FIFO inventory valuation method is

used.

Compute the amount of Hurley’s buildings that would be reported in a December

31, 2011, consolidated balance sheet.

46. Perry Company acquires 100% of the stock of Hurley Corporation on

January 1, 2010, for $3,800 cash. As of that date Hurley has the following trial

balance;

Any excess of consideration transferred over fair value of net assets acquired is

considered goodwill with an indefinite life. FIFO inventory valuation method is

used.

Compute the amount of Hurley’s equipment that would be reported in a

December 31, 2011, consolidated balance sheet.

47. Perry Company acquires 100% of the stock of Hurley Corporation on

January 1, 2010, for $3,800 cash. As of that date Hurley has the following trial

balance;

Any excess of consideration transferred over fair value of net assets acquired is

considered goodwill with an indefinite life. FIFO inventory valuation method is

used.

Compute the amount of Hurley’s land that would be reported in a December 31,

2011, consolidated balance sheet.

48. Perry Company acquires 100% of the stock of Hurley Corporation on

January 1, 2010, for $3,800 cash. As of that date Hurley has the following trial

balance;

Any excess of consideration transferred over fair value of net assets acquired is

considered goodwill with an indefinite life. FIFO inventory valuation method is

used.

Compute the amount of Hurley’s long-term liabilities that would be reported in a

December 31, 2011, consolidated balance sheet.

49. Kaye Company acquired 100% of Fiore Company on January 1, 2011. Kaye

paid $1,000 excess consideration over book value which is being amortized at $20

per year. Fiore reported net income of $400 in 2011 and paid dividends of $100.

Assume the equity method is applied. How much will Kaye’s income increase or

decrease as a result of Fiore’s operations?

50. Kaye Company acquired 100% of Fiore Company on January 1, 2011. Kaye

paid $1,000 excess consideration over book value which is being amortized at $20

per year. Fiore reported net income of $400 in 2011 and paid dividends of $100.

Assume the partial equity method is applied. How much will Kaye’s income

increase or decrease as a result of Fiore’s operations?

51. Kaye Company acquired 100% of Fiore Company on January 1, 2011. Kaye

paid $1,000 excess consideration over book value which is being amortized at $20

per year. Fiore reported net income of $400 in 2011 and paid dividends of $100.

Assume the initial value method is applied. How much will Kaye’s income

increase or decrease as a result of Fiore’s operations?

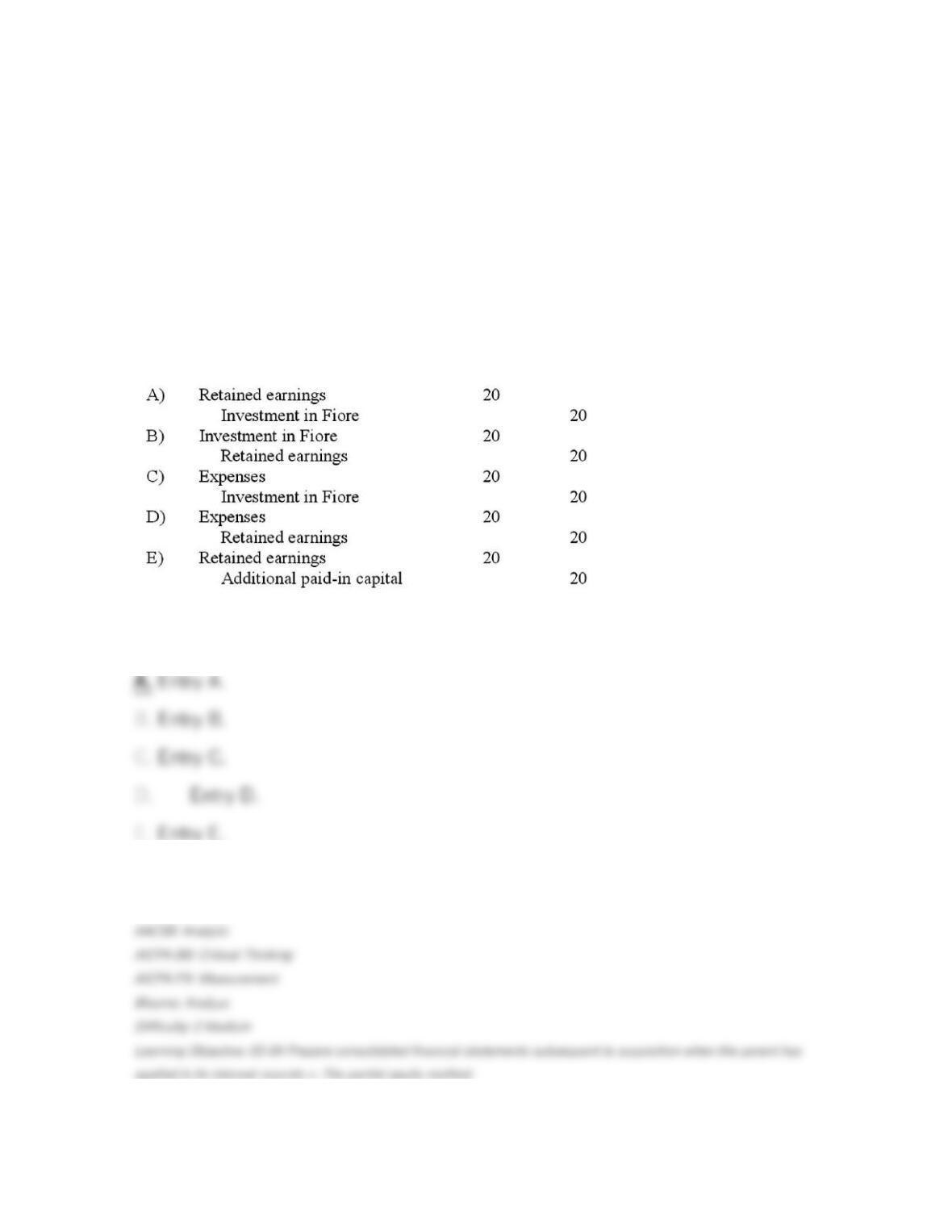

52. Kaye Company acquired 100% of Fiore Company on January 1, 2011. Kaye

paid $1,000 excess consideration over book value which is being amortized at $20

per year. Fiore reported net income of $400 in 2011 and paid dividends of $100.

Assume the partial equity method is used. In the years following acquisition, what

additional worksheet entry must be made for consolidation purposes that is not

required for the equity method?