3-202

212. Almo company manufactures and sells adjustable canopies that attach to motor homes

and trailers. Almo developed its budget for the current year assuming that the canopies would

sell at a price of $400 each. The variable expenses for each canopy were forecasted to be $200

and the annual fixed expenses were forecasted to be $100,000. Almo had targeted a profit of

$400,000.

While Almo’s sales usually rise during the second quarter, the May financial statements reported

that sales were not meeting expectations. For the first five months of the year, only 350 units had

been sold at the established price, with variable expense as planned, and it was clear that the

target profit for the year would not be reached unless some actions were taken. Almo’s president

assigned a management committee to analyze the situation and develop several alternative

courses of action. The following three alternatives were presented to the president, only one of

which can be selected.

1. Reduce the selling price by $40. The marketing department forecasts that with the lower price,

2,700 units could be sold during the remainder of the year.

2. Lower variable expenses per unit by $25 through the use of less expensive materials. Because

of the difference in materials, the selling price would have to be lowered by $30 and sales of

2,200 units for the remainder of the year are forecast.

3. Cut fixed expenses by $10,000 and lower the selling price by 5 percent. Sales of 2,000 units

would be expected for the remainder of the year.

Required:

a. If no changes are made to the selling price or cost structure, estimate the number of units that

must be sold during the year to break even.

b. If no changes are made to the selling price or cost structure, estimate the number of units that

must be sold during the year to attain the target profit of $400,000.

c. Determine which of the alternatives Almo’s president should select to maximize profit.

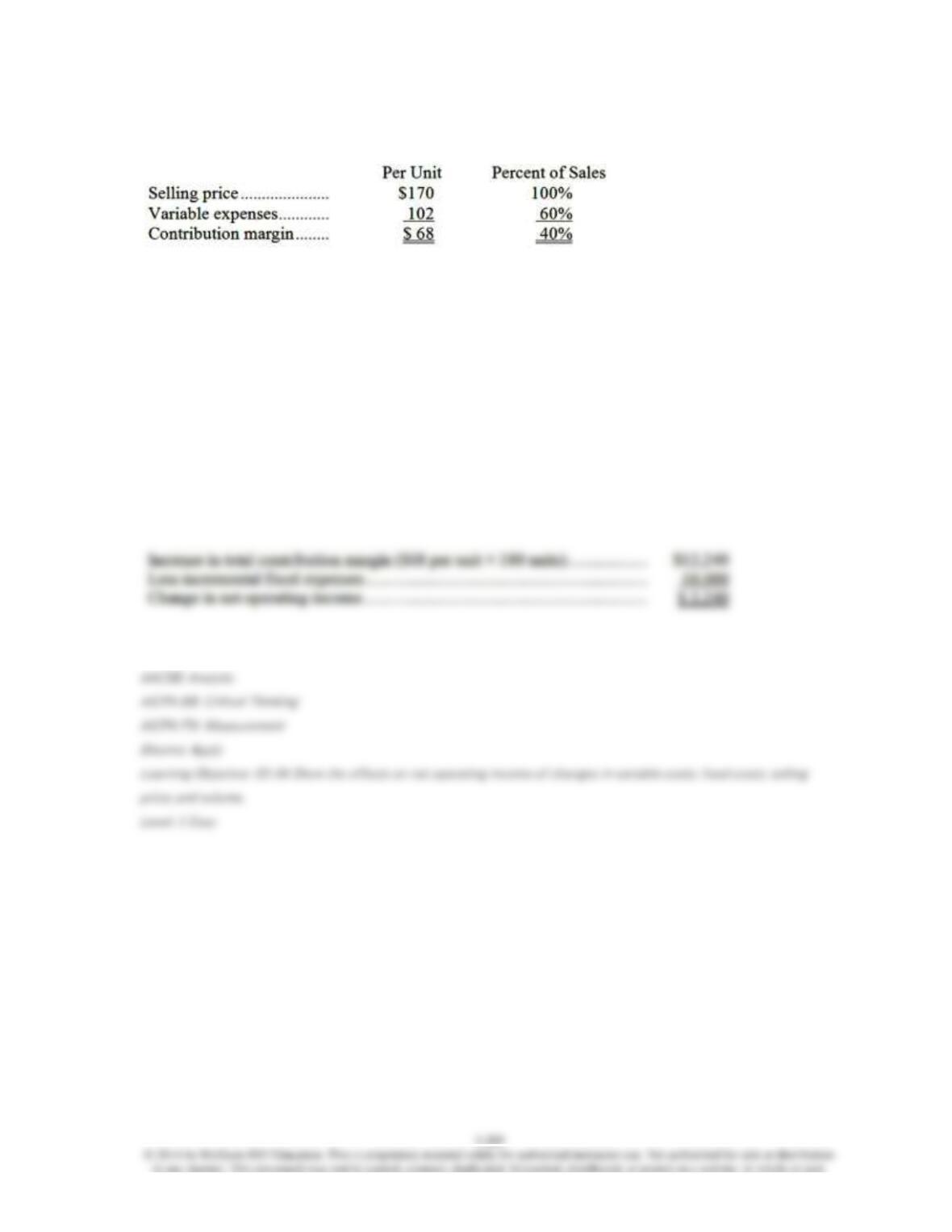

213. Zeeb Corporation produces and sells a single product. Data concerning that product

appear below:

Fixed expenses are $355,000 per month. The company is currently selling 5,000 units per month.

Required:

The marketing manager believes that a $12,000 increase in the monthly advertising budget would

result in a 160 unit increase in monthly sales. What should be the overall effect on the company’s

monthly net operating income of this change? Show your work!

214. Data concerning Lantieri Corporation’s single product appear below:

Fixed expenses are $162,000 per month. The company is currently selling 3,000 units per month.

Required:

The marketing manager believes that a $10,000 increase in the monthly advertising budget would

result in a 180 unit increase in monthly sales. What should be the overall effect on the company’s

monthly net operating income of this change? Show your work!

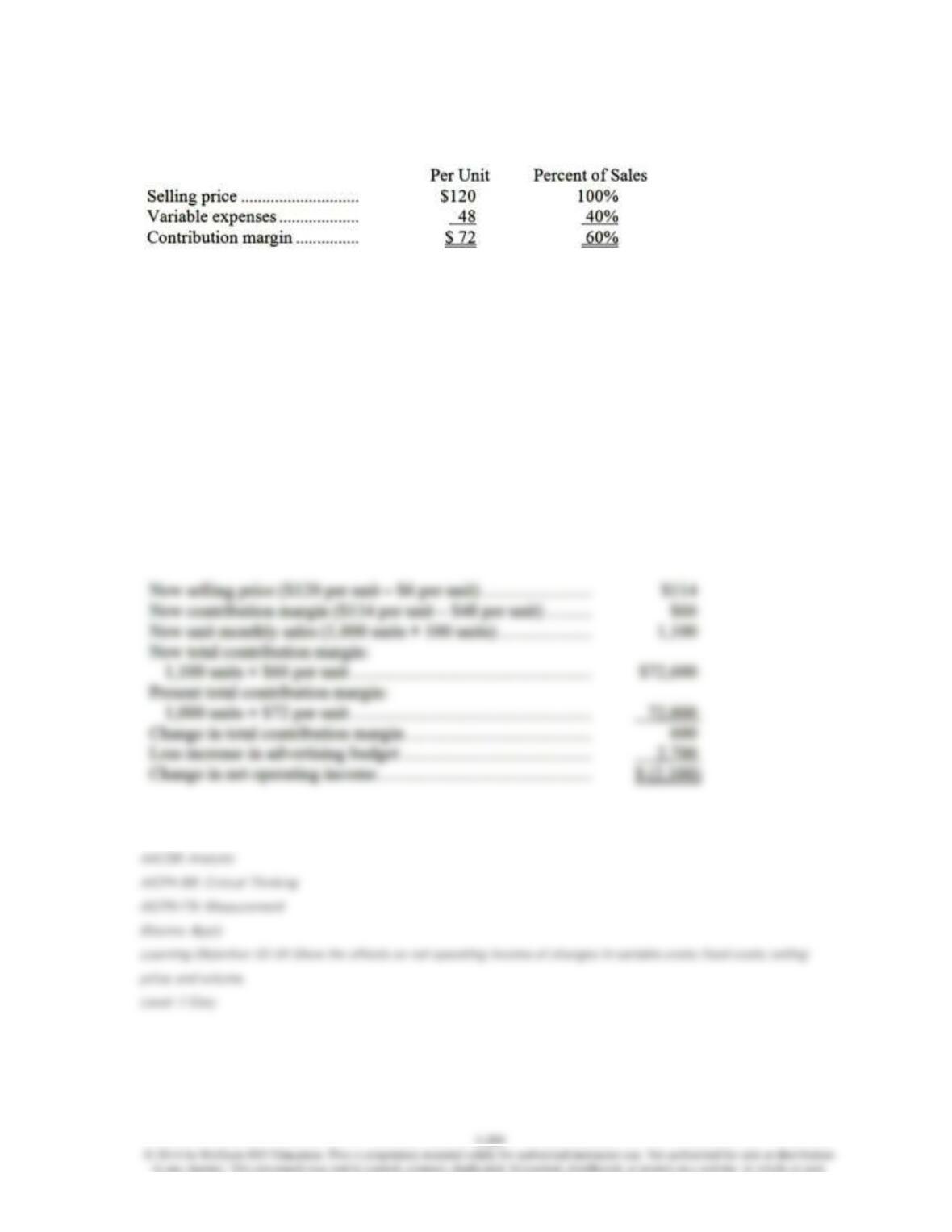

215. Calderon Corporation produces and sells a single product. Data concerning that product

appear below:

Fixed expenses are $110,000 per month. The company is currently selling 1,000 units per month.

Required:

Management is considering using a new component that would increase the unit variable cost by

$56. Since the new component would improve the company’s product, the marketing manager

predicts that monthly sales would increase by 500 units. What should be the overall effect on the

company’s monthly net operating income of this change if fixed expenses are unaffected? Show

your work!

216. Data concerning Goulbourne Corporation’s single product appear below:

Fixed expenses are $444,000 per month. The company is currently selling 7,000 units per month.

Required:

Management is considering using a new component that would increase the unit variable cost by

$2. Since the new component would improve the company’s product, the marketing manager

predicts that monthly sales would increase by 200 units. What should be the overall effect on the

company’s monthly net operating income of this change if fixed expenses are unaffected? Show

your work!

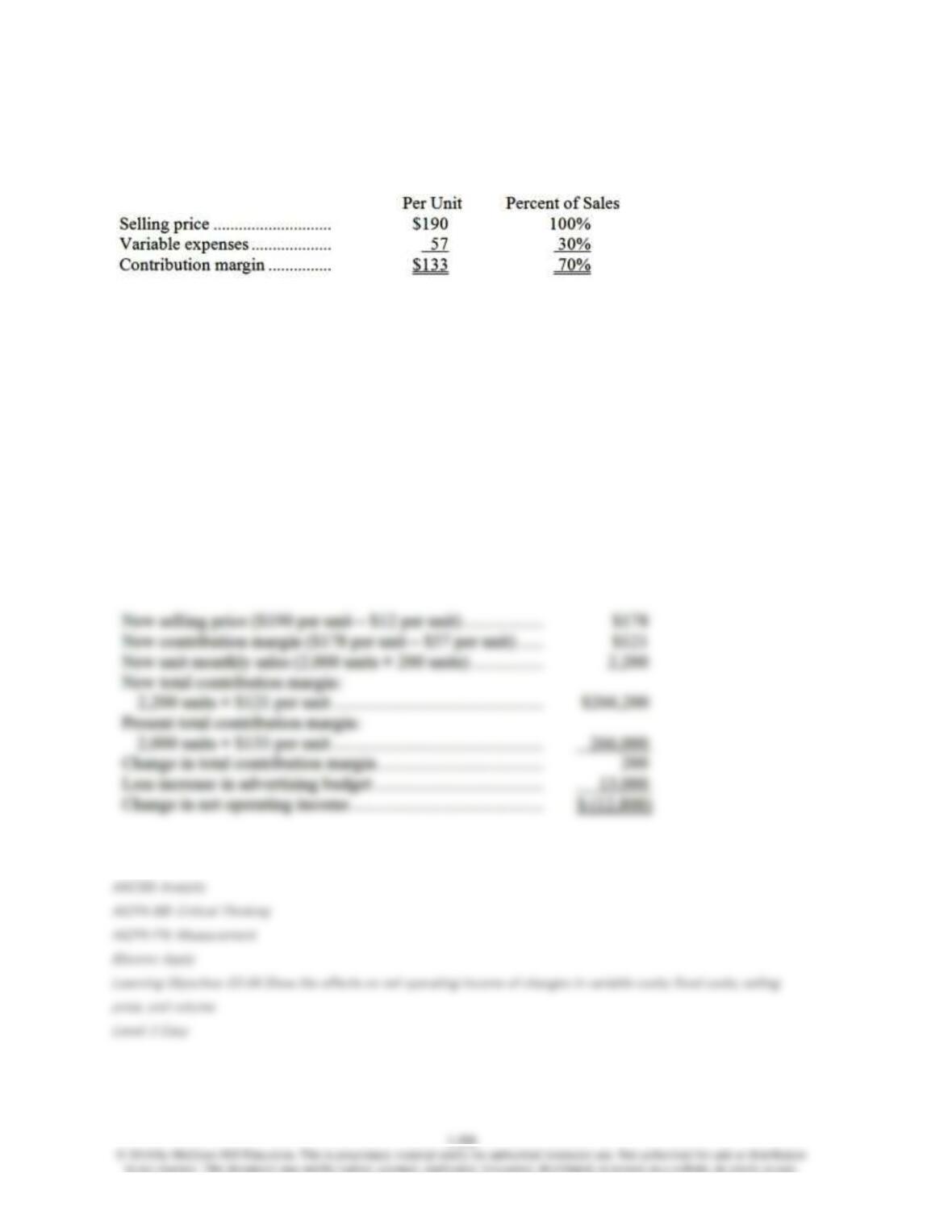

217. Tapp Corporation produces and sells a single product. Data concerning that product

appear below:

Fixed expenses are $226,000 per month. The company is currently selling 2,000 units per month.

Required:

The marketing manager would like to cut the selling price by $12 and increase the advertising

budget by $13,000 per month. The marketing manager predicts that these two changes would

increase monthly sales by 200 units. What should be the overall effect on the company’s monthly

net operating income of this change? Show your work!

218. Data concerning Maline Corporation’s single product appear below:

Fixed expenses are $55,000 per month. The company is currently selling 1,000 units per month.

Required:

The marketing manager would like to cut the selling price by $6 and increase the advertising

budget by $2,700 per month. The marketing manager predicts that these two changes would

increase monthly sales by 100 units. What should be the overall effect on the company’s monthly

net operating income of this change? Show your work!

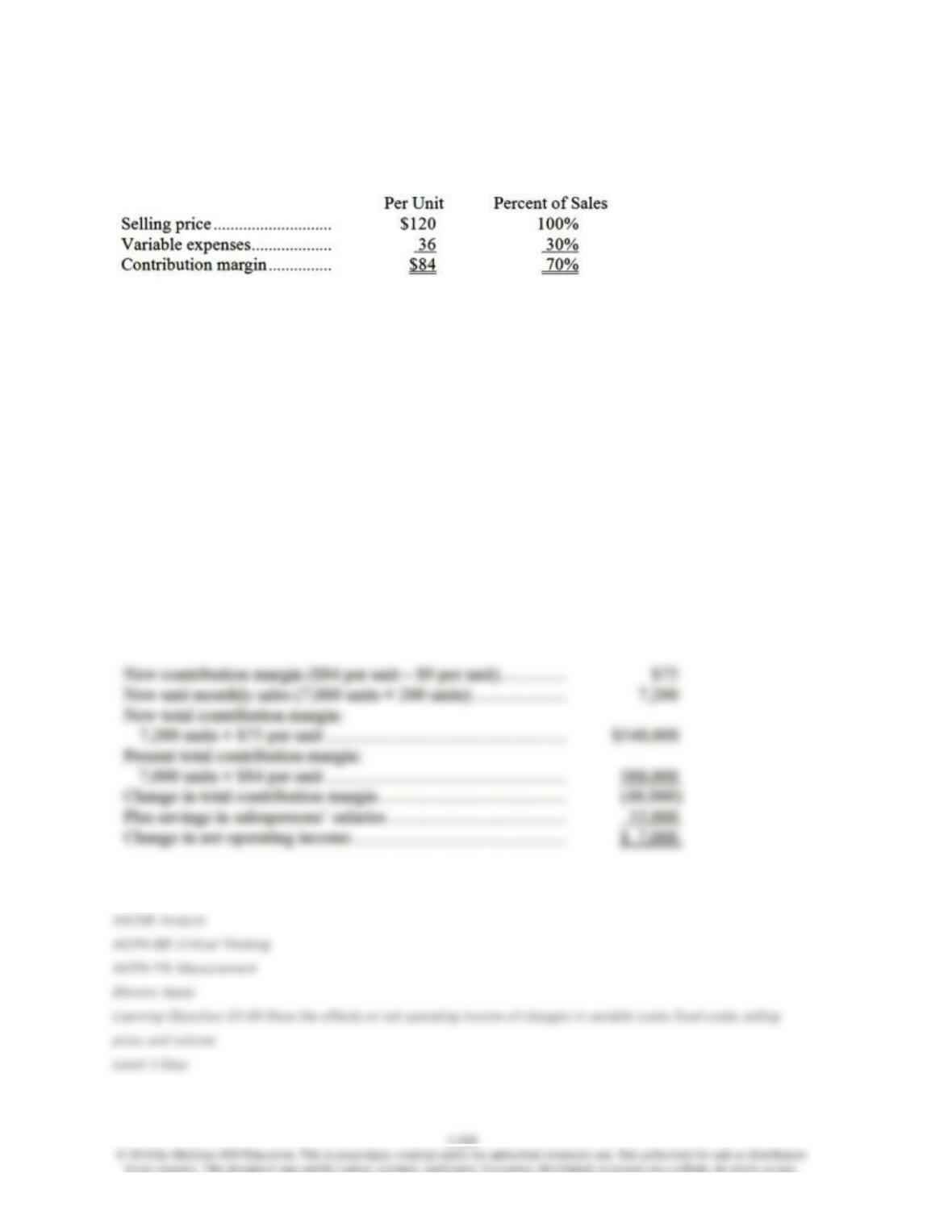

219. Dubitsky Corporation produces and sells a single product. Data concerning that product

appear below:

Fixed expenses are $516,000 per month. The company is currently selling 7,000 units per month.

Required:

The marketing manager would like to introduce sales commissions as an incentive for the sales

staff. The marketing manager has proposed a commission of $9 per unit. In exchange, the sales

staff would accept an overall decrease in their salaries of $55,000 per month. The marketing

manager predicts that introducing this sales incentive would increase monthly sales by 200 units.

What should be the overall effect on the company’s monthly net operating income of this change?

Show your work!

220. Data concerning Tietz Corporation’s single product appear below:

Fixed expenses are $1,044,000 per month. The company is currently selling 9,000 units per

month.

Required:

The marketing manager would like to introduce sales commissions as an incentive for the sales

staff. The marketing manager has proposed a commission of $14 per unit. In exchange, the sales

staff would accept an overall decrease in their salaries of $110,000 per month. The marketing

manager predicts that introducing this sales incentive would increase monthly sales by 400 units.

What should be the overall effect on the company’s monthly net operating income of this change?

Show your work!

221. Churchwell Corporation produces and sells a single product. Data concerning that

product appear below:

Required:

a. Assume the company’s monthly target profit is $69,000. Determine the unit sales to attain that

target profit. Show your work!

b. Assume the company’s monthly target profit is $41,400. Determine the dollar sales to attain

that target profit. Show your work!

222. Guagliano Corporation produces and sells a single product whose selling price is $110.00

per unit and whose variable expense is $29.70 per unit. The company’s monthly fixed expense is

$345,290.

Required:

a. Assume the company’s monthly target profit is $16,060. Determine the unit sales to attain that

target profit. Show your work!

b. Assume the company’s monthly target profit is $40,150. Determine the dollar sales to attain

that target profit. Show your work!

223. Arzola Corporation produces and sells a single product. Data concerning that product

appear below:

Required:

Assume the company’s monthly target profit is $17,080. Determine the unit sales to attain that

target profit. Show your work!

224. The selling price of Bayard Corporation’s only product is $230.00 per unit and its variable

expense is $80.50 per unit. The company’s monthly fixed expense is $792,350.

Required:

Assume the company’s monthly target profit is $29,900. Determine the unit sales to attain that

target profit. Show your work!

3-216

225. Dagnan Corporation produces and sells a single product whose contribution margin ratio

is 66%. The company’s monthly fixed expense is $667,920 and the company’s monthly target

profit is $72,600.

Required:

Determine the dollar sales to attain the company’s target profit. Show your work!

226. The contribution margin ratio of Thronson Corporation’s only product is 69%. The

company’s monthly fixed expense is $455,400 and the company’s monthly target profit is $41,400.

Required:

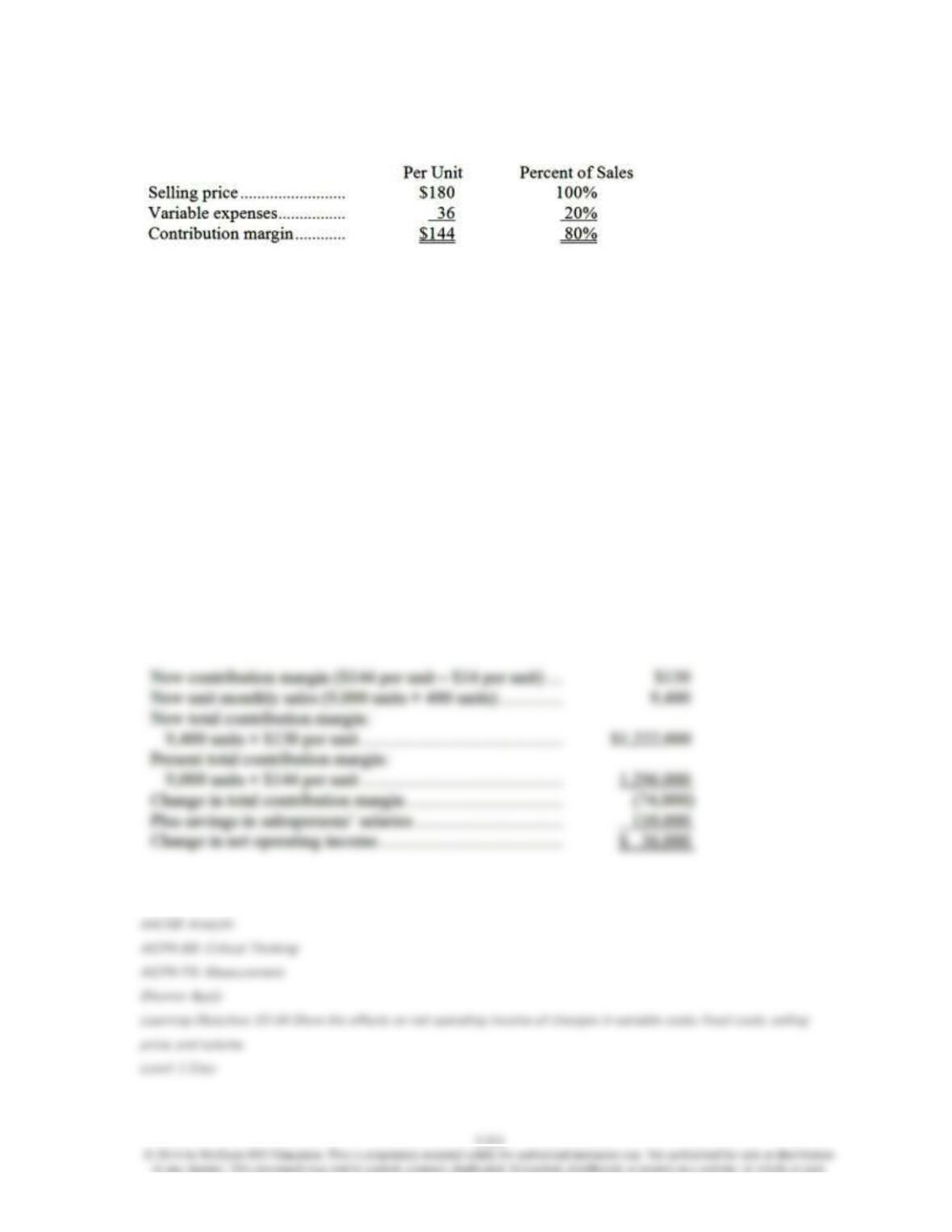

Determine the dollar sales to attain the company’s target profit. Show your work!