135) Presented below are terms preceded by letters a through f and followed by a list of definitions 1

through 6. Match the letter of the terms with the definitions. Use the space provided preceding each

definition.

(a) Sunk cost

(b) Opportunity cost

(c) Out-of-pocket cost

(d) Net present value

(e) Incremental cost

(f) Annuity

________ (1) A cost that requires a future outlay of cash and is relevant for current and future

decision making.

(2) A series of cash flows of equal dollar amount over equal time periods.

________ (3) An estimate of an asset’s value to the company; computed by discounting the future net

cash flows from the investment the project’s required rate of return and then subtracting the initial

amount invested.

(4) A cost that cannot be avoided or changed because it arises from past decision;

irrelevant to future decisions.

(5) An additional cost incurred if a company pursues a certain course of action.

________ (6) The potential benefits lost by taking a specific action when two or more alternative

choices are available.

ESSAY QUESTIONS

136) What is capital budgeting? Why are capital budgeting decisions often difficult and risky?

137) Briefly describe the time value of money. Why is the time value of money important in capital

budgeting?

138) In using a capital budgeting method that takes the time value of money into consideration,

management must consider a hurdle rate in making its decisions. What is a hurdle rate? What

factors does management have to consider in selecting a hurdle rate?

139) Identify the five steps involved in managerial decision making.

140) Good management accounting indicates that projects be evaluated using relevant data. In choosing

among alternatives, what factors (considerations) are relevant?

141) How does the calculation of break-even time (BET) differ from the calculation of payback period

(PBP)?

142) Briefly describe both the payback period method and the net present value method of comparing

investment alternatives.

143) When making capital budgeting decisions, companies usually prefer shorter payback periods.

Explain why shorter payback periods are desirable.

144) What is one advantage and one disadvantage of using the accounting rate of return to evaluate

investment alternatives?

145) You have evaluated three projects of similar investment amount and risk using the net present

value (NPV) method. How would you decide which one of the projects to select?

146) When the amount invested differs substantially across projects, NPV is of limited value for

comparison purposes. You have evaluated three projects of substantially different investment

amounts using the net present value (NPV) method. How would you decide which one of the

projects to select?

147) Identify at least three reasons for managers to favor the internal rate of return (IRR) over other

capital budgeting approaches.

148) For each of the capital budgeting methods listed below, place an X in the correct column,

indicating the measurement basis of each, the ability to make comparison among projects, and

whether each method reflects or ignores the time value of money.

Measurement Basis

Comparison among

projects

Time value of money

Cash

flows

Accrual

income

Allows

comparison

Difficult

to

compare

Reflects

time value

of money

Ignores

time value

of money

Payback period

Accounting rate of

return

Net present value

_

Internal rate of

return

149) A company inadvertently produced 6,000 defective portable radios. The radios cost $10 each to be

manufactured. A salvage company will purchase the defective units as they are for $8 each. The

production manager reports that the defects can be corrected for $4.50 per unit, enabling the

company to sell them at the regular price of $15.00. The repair operations would not affect other

production operations. Prepare an analysis that shows which action should be taken.

150) A company manufactures two products. Each unit of product X requires 10 machine hours and

each unit of product Y requires 4 machine hours. The company’s productive capacity is limited to

180,000 machine hours. Each unit of product X sells for $15 and has variable costs of $7. Each

unit of product Y sells for $8 and has variable costs of $3. If the company can sell all that it

produces of both products, what should the sales mix be?

151) Goodfellow Company had the following results of operations for the past year:

Sales (8,000 units at $6.80)

$ 54,400

Materials and direct labor

(20,000)

Overhead (40% variable)

(10,000)

Selling and administrative expenses (all fixed)

(6,000)

Operating income

$ 18,400

A foreign company (whose sales will not affect Goodfellow’s regular sales) offers to buy 2,000 units

at $5.00 per unit. In addition to variable manufacturing costs, there would be shipping costs of

$1,200 in total on these units. Prepare an analysis of this additional business to show whether

Goodfellow should take this order.

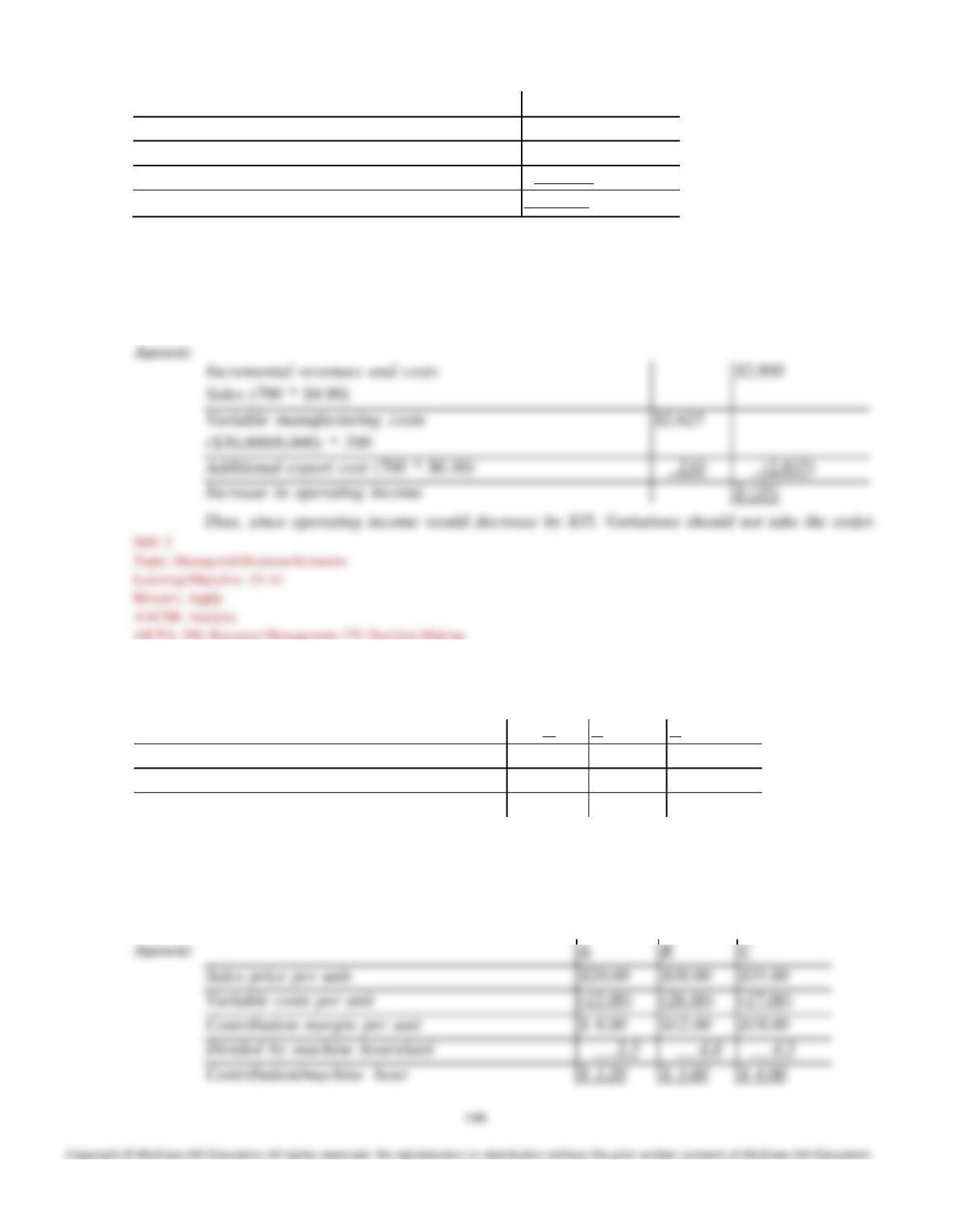

152) Variations Company had the following results of operations for the past year:

Sales (8,000 units at $7.00)

$ 56,000

Variable manufacturing costs

(30,000)

Fixed manufacturing costs

(6,000)

Fixed selling and administrative expenses

(4,500)

Operating income

$ 15,500

A foreign company (whose sales will not affect Variations’ regular sales) offers to buy 700 units at

$4.00 per unit. In addition to variable manufacturing costs, there would be an export cost of $0.30

per unit. Prepare an analysis of this additional business to show whether Variations should take this

order.

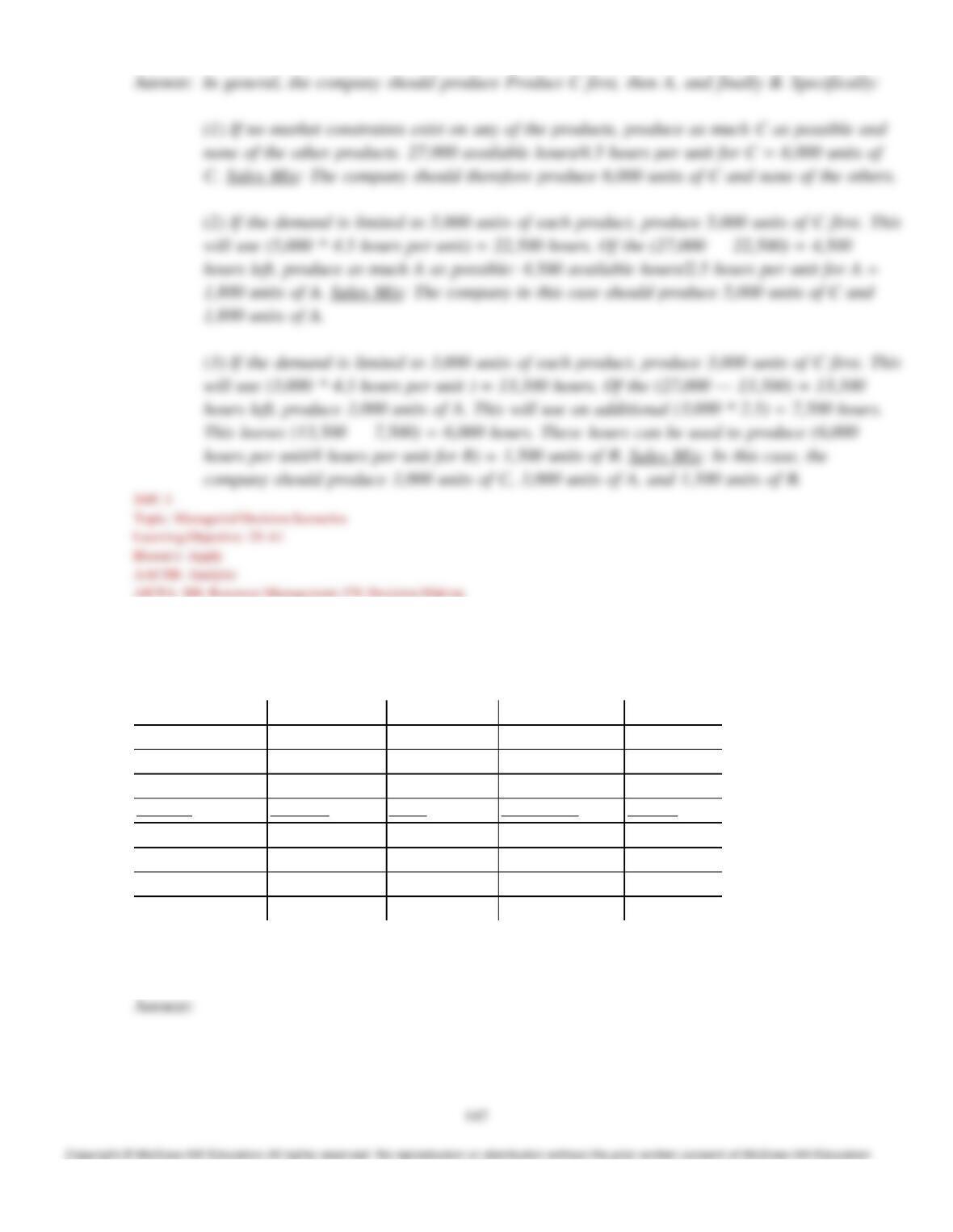

153) A company produces three different products that all require processing on the same machines. There

are only 27,000 machine hours available in each year. Production information for each product is:

A

B

C

Sales price per unit

$20.00

$38.00

$35.00

Variable costs per unit

$12.00

$26.00

$17.00

Machine hours necessary to produce one unit

2.5

4.0

4.50

Required:

(1) Determine the preferred sales mix if there are no market constraints on any of the products.

(2) Determine the preferred sales mix if the demand is limited to 5,000 units for each product.

(3) Determine the preferred sales mix if the demand is limited to 3,000 units for each product.

154) A company puts four products through a common production process. This process costs $100,000

each year. The four products can be sold when they emerge from this process at the “split-off point”,

or processed further and then sold. Data about the four products for the coming period are:

Unit Sales

Unit Sales

Price per

Price per

unit at

unit after

Additional

Split-Off

Further

Processing

Product

Volume

Point

Processing

Costs

Stroller

20,000 lb.

$28.00

$42.00

$400,000

Walker

10,000 lb.

7.00

28.00

144,000

Jogger

5,000 lb.

36.00

58.00

120,000

Runner

5,000 lb.

18.00

22.00

40,000

Determine which products should be sold at the split-off point and which should be processed

further.

155) A company has just received a special, one-time order for 1,000 units. Producing the order will have

no effect on the production and sales of other units. The buyer’s name will be stamped on each unit,

at a cost of $1.50 per unit. Normal cost data, excluding stamping, follows:

Direct materials…………………………… $ 10 per unit

Direct labor……………………………….. 16 per unit

Variable overhead………………………… 4 per unit

Allocated fixed overhead…………………. 12 per unit

Allocated fixed selling expense…………… 8 per unit

Prepare an analysis that indicates the selling price per unit this company will require to earn $3,000

on the order.

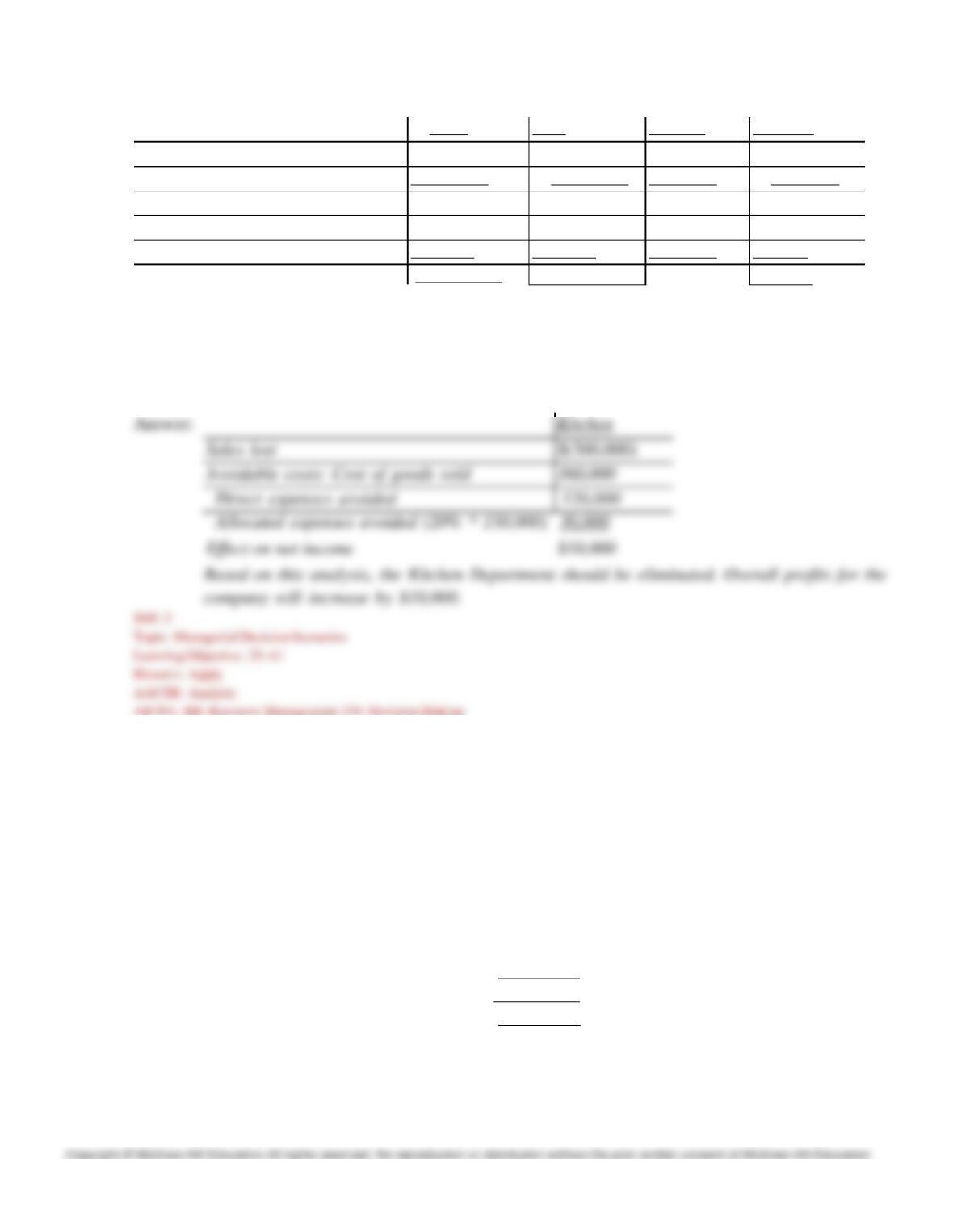

156) Spilker Linens Store has three departments: Bath, Kitchen, and Bedding. The most recent income

statement, showing the total operating profit and departmental results is shown below:

Total

Bath

Kitchen

Bedding

Sales

$2,100,000

$1,000,000

$600,000

$500,000

Cost of goods sold

(1,260,000)

(500,000)

(400,000)

(360,000)

Gross profit

840,000

500,000

200,000

140,000

Direct expenses

(420,000)

(200,000)

(100,000)

(120,000)

Allocated expenses

(350,000)

(100,000)

(75,000)

(175,000)

Net income (loss)

$ 70,000

$ 200,000

$ 25,000

$(155,000)

Based on this income statement, management is planning on eliminating the Bedding department, as

it is generating a net loss. If the Bedding department is eliminated, the Kitchen department will

expand to fill the space, but sales will not change in total, nor will direct expenses. None of

Bedding’s allocated expenses will be avoided, but they will be reallocated to Bath and Kitchen. Bath

will be allocated $100,000 additional expenses, and Kitchen will be allocated $75,000 additional

expenses. Prepare a new income statement for Spilker Linens Store, showing the results if the

Bedding Department is eliminated and indicate whether eliminating the department is advisable.

151

157) Luxury Linens has three departments: Bath, Kitchen, and Bedding. The most recent income

statement, showing the total operating profit and departmental results is shown below:

Total

Bath

Kitchen

Bedding

Sales

$2,100,000

$1,000,000

$500,000

$600,000

Cost of goods sold

(1,260,000)

(500,000)

(360,000)

(400,000)

Gross profit

840,000

500,000

140,000

200,000

Direct expenses

(420,000)

(200,000)

(120,000)

(100,000)

Allocated expenses

(325,000)

(100,000)

(150,000)

(75,000)

Net income (loss)

$ 95,000

$ 200,000

$(130,000)

$25,000

Based on this income statement, management is considering eliminating the Kitchen department. If

the Kitchen department is eliminated, the other departments will expand to fill the space but sales are

not expected to change. Twenty percent of Kitchen’s allocated expenses will be avoided due to

restructuring and the remainder reallocated equally to Bath and Bedding. Show an analysis

indicating whether the Kitchen department should be eliminated.

158) Generalware, Inc. sells a single product and reports the following results from sales of 100,000 units:

Sales ($45 unit) …………..…………….…

Less costs and expenses:

$4,500,000

Direct materials ($16/unit)………….…

$1,600,000

Direct labor ($9/unit)…………….….…

900,000

Variable overhead ($3/unit)…….……..

300,000

Fixed overhead ($8.10/unit)…………….

810,000

Variable administrative ($4.50/unit)….

450,000

Fixed administrative ($4/unit)…………

400,000

Total costs and expenses………………

$(4,460,000)

Operating income…………………………

$ 40,000

A foreign company wants to purchase 15,000 units. However, they are willing to pay only $36 per

unit for this one-time order. They also agree to pay all freight costs. To fill the order, Generalware

will incur normal production costs. Total fixed overhead will have to be increased by $60,000 to pay

for equipment rentals and insurance. No additional administrative costs (variable or fixed) will be

incurred in association with this special order.

Required:

(1) Should Generalware accept the order if it does not affect regular sales? Explain.

(2) Assume that Generalware can accept the special order only by giving up 5,000 units of its normal

sales. Should the company accept the special order under these circumstances?

159) A company is planning to introduce a new portable computer to its existing product line.

Management must decide whether to make the computer case or buy it from an outside supplier.

The lowest outside price is $90. If the case is produced internally, the company will have to

purchase new equipment that will yield annual depreciation of $130,000. The company will also

need to rent a new production facility at $200,000 a year. At 20,000 cases per year, a preliminary

analysis of production costs shows the following:

Per Case

Direct materials

$ 40.00

Direct labor

32.00

Variable overhead

10.00

Equipment depreciation 6.50

Building rental 10.00

Allocated fixed overhead 7.50

Total cost $106.00

Required:

(1) Determine whether the company should make the cases or buy them from the outside supplier.

(2) What other factors, besides cost, should the company consider?

Periods

of $1 at 12%

1……

0.8929

2……

0.7972

3……

0.7118

160) A company must decide between scrapping or rebuilding units that do not pass inspection. The

company has 15,000 such units that cost $6 per unit to manufacture. The units were built to satisfy

a special order, which must still be satisfied if the defective units are scrapped. The units can be

sold as scrap for $2.50 each or they can be reworked for $4.50 each and sold for the full price of

$9.00 each. If the units are sold as scrap, the company will have to build 15,000 replacement units

and sell them at the full price.

Required:

(1) What is the net return from selling the units as scrap?

(2) What is the net return from reworking and selling the units?

(3) Should the company sell the units as scrap or rework them?

161) Nebraska Co. is reviewing a capital investment of $100,000. This project’s projected cash flows over

a five-year period are estimated at $35,000 each year.

Required:

(a) Calculate the payback period.

(b) Calculate the break-even time. Assume a 12% hurdle rate and use the table below:

Present Value

154

4…… 0.6355

5…… 0.5674

(c) Using the results in (a) and (b), make a recommendation for the project.

162) A company is considering purchasing a machine for $85,000. The machine is expected to generate

a net after-tax income of $11,250 per year. Depreciation expense would be $8,500. What is the

payback period for this machine?

163) A company is trying to decide which of two new product lines to introduce in the coming year. The

predicted revenue and cost data for each product line follows:

Product A

Product B

Sales

$80,000

$96,000

Direct materials

3,000

6,000

Direct labor

30,000

45,000

Other cash operating expenses

7,500

9,000

New equipment costs 155

75,000

100,000