55) A challenge in calculating the total costs and expenses of a department is:

A) Assigning direct costs to the department.

B) Allocating indirect expenses to the department.

C) Determining the direct expenses of the department.

D) Determining the amount of sales of the department.

E) Determining the gross profit ratio.

56) A company has two departments, Y and Z that incur delivery expenses. An analysis of the total

delivery expense of $9,000 indicates that Dept. Y had a direct expense of $1,000 for deliveries and

Dept. Z had no direct expense. The indirect expenses are $8,000. The analysis also indicates that

40% of regular delivery requests originate in Dept. Y and 60% originate in Dept. Z. Departmental

delivery expenses for Dept. Y and Dept. Z, respectively, are:

A) $5,500; $3,500.

B) $4,500; $4,500.

C) $4,200; $4,800.

D) $5,400; $3,600.

E) $4,800; $4,200.

57) A company has two departments, Y and Z that incur wage expenses. An analysis of the total wage

expense of $19,000 indicates that Dept. Y had a direct wage expense of $2,000 and Dept. Z had a

direct wage expense of $3,500. The remaining expenses are indirect and analysis indicates they

should be allocated evenly between the two departments. Departmental wage expenses for Dept. Y

and Dept. Z, respectively, are:

A) $9,500; $9,500.

B) $6,750; $6,750.

C) $8,750; $10,250.

D) $10,250; $8,750.

E) $2,000; $3,500.

58) Which of the following is not a step in creating operating department income statements?

A) Allocate indirect expenses across departments.

B) Allocate service department expenses to operating departments.

C) Prepare the departmental income statements.

D) Accumulate revenues and direct expenses by department.

E) Eliminate the uncontrollable costs for each department.

59) The most useful allocation basis for the departmental costs of an advertising campaign for a

storewide sale is likely to be:

A) An equal amount of cost for each department.

B) Relative number of items each department had on sale.

C) Proportion of sales of each department.

D) Floor space of each department.

E) Number of customers to enter each department.

60) Costs that the manager has the power to determine or at least significantly affect are called:

A) Direct costs.

B) Joint costs.

C) Controllable costs.

D) Uncontrollable costs.

E) Indirect costs.

61) A report that accumulates the actual expenses that a manager is responsible for and their budgeted

amounts is a:

A) Departmental accounting report.

B) Managerial cost report.

C) Controllable expense report.

D) Responsibility accounting performance report.

E) Segmental accounting report.

62) An accounting system that is set up to control costs and evaluate managers’ performance by

assigning costs to the managers responsible for controlling them is called a(n):

A) Responsibility accounting system.

B) Cost accounting system.

C) Activity-based accounting system.

D) Financial accounting system.

E) Managerial accounting system.

63) Costs that the manager does not have the power to determine or at least significantly affect are:

A) Uncontrollable costs.

B) Direct costs.

C) Joint costs.

D) Variable costs.

E) Indirect costs.

64) Plans that identify costs and expenses under each manager’s control prior to the reporting period,

typically based on the flexible budget approach, are called:

A) Managerial accounting systems.

B) Responsibility accounting systems.

C) Cost accounting systems.

D) Activity-based accounting systems.

E) Responsibility accounting budgets.

65) Within an organizational structure, the person most likely to be evaluated in terms of controllable

costs would be:

A) A sales representative.

B) A maintenance worker.

C) A production line worker.

D) A cost center manager.

E) A payroll clerk.

66) The most useful data for evaluation of a manager’s cost performance is based on:

A) Controllable costs.

B) Contribution percentages.

C) Uncontrollable expenses.

D) Direct costs.

E) Departmental contributions to overhead.

67) In a responsibility accounting system:

A) Outputs of the departments are not part of the evaluation process.

B) All managers at a given level have equal authority and responsibility.

C) Each accounting report contains all items allocated to a responsibility center.

D) Managers are responsible for their departments’ controllable costs.

E) Organized and clear lines of authority and responsibility are only incidental.

68) Responsibility accounting performance reports:

A) Are equally detailed at all levels of management.

B) Are useful in any format.

C) Are usually summarized at higher levels of management.

D) Become more detailed at higher levels of management.

E) Are irrelevant at the highest level of management.

69) A responsibility accounting performance report displays:

A) Only indirect costs.

B) Only direct costs.

C) Both actual costs and budgeted costs.

D) Only actual costs.

E) Only budgeted costs.

70) Which of the following is not true regarding a responsibility accounting system?

A) It can be applied at any level of an organization.

B) It should not hold a manager responsible for costs over which the manager has no influence.

C) It is designed to measure the performance of managers in terms of controllable costs.

D) It is only relevant in manufacturing companies.

E) It assigns responsibility for costs to the appropriate managerial level that controls those costs.

71) A cost incurred to produce or purchase two or more products at the same time is a(n):

A) Differential cost.

B) Fixed cost.

C) Joint cost.

D) Product cost.

E) Incremental cost.

72) In regard to joint cost allocation, the “split-off point” is:

A) Not acceptable when using the value basis for allocating joint costs.

B) The point at which some products are sold and some remain in inventory.

C) The point at which separate products can be identified.

D) A physical basis method to allocate costs based on ratio of some physical characteristic.

E) The difference between the actual and market value of joint costs.

73) Allocating joint costs to products using a value basis method is based on their relative:

A) Direct costs.

B) Variable costs.

C) Total costs.

D) Sales values.

E) Gross margins.

74) Differential Chemical produced 10,000 gallons of Preon and 20,000 gallons of Paron. Joint costs

incurred in producing the two products totaled $7,500. At the split-off point, Preon has a market

value of $6.00 per gallon and Paron $2.00 per gallon. Compute the portion of the joint costs to be

allocated to Preon if the value basis is used.

A) $1,500. B) $3,000. C) $2,500 D) $4,500. E) $5,625.

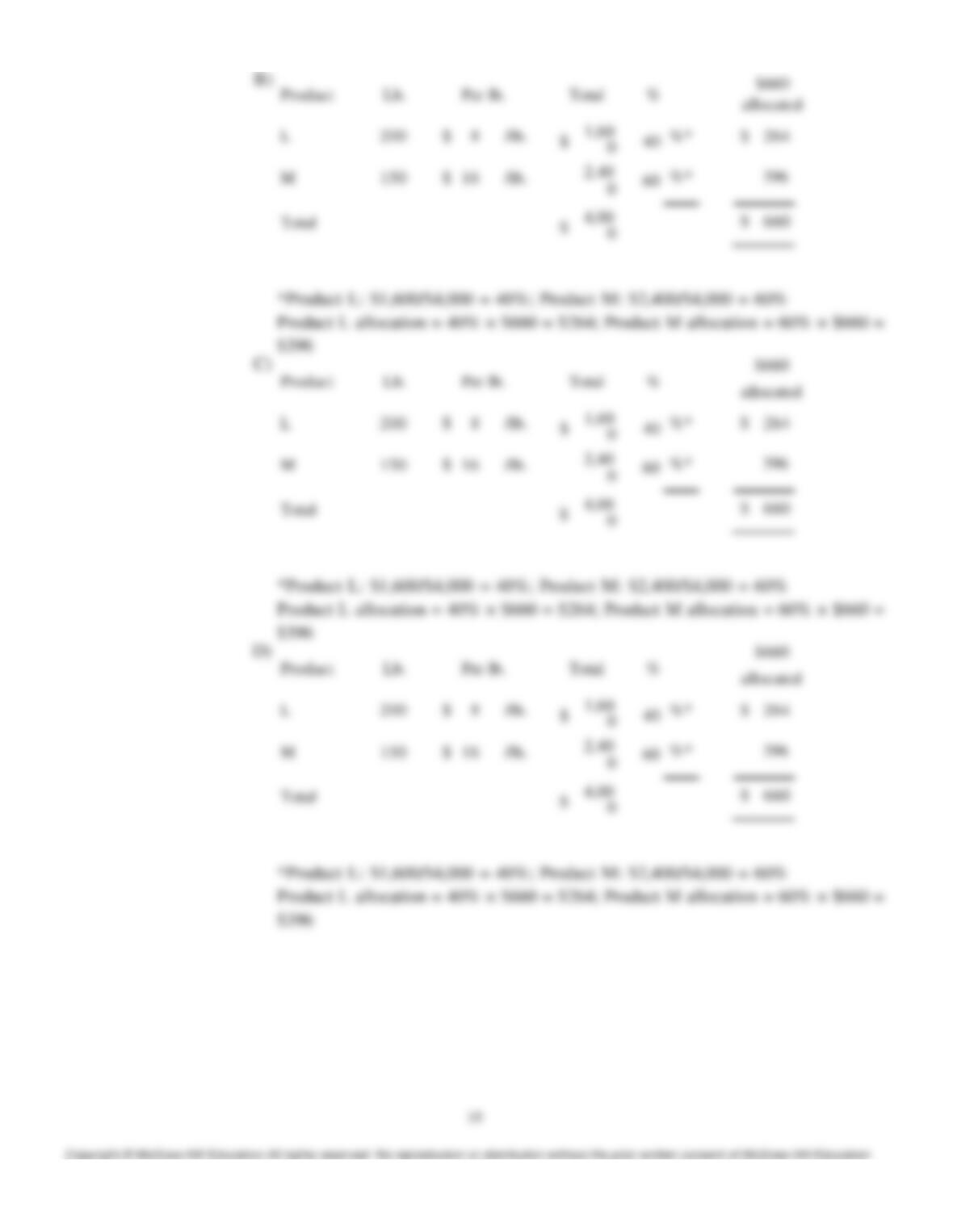

75) Data pertaining to a company’s joint production for the current period follows:

L

M

Quantities produced

200 lbs.

150 lbs.

Market value at split-off point

$ 8 /lb.

$ 16 /lb.

Compute the cost to be allocated to Product L for this period’s $660 of joint costs if the value basis is

used. (Do not round your intermediate calculations.)

A) $796. B) $1,364. C) $264. D) $396. E) $330.

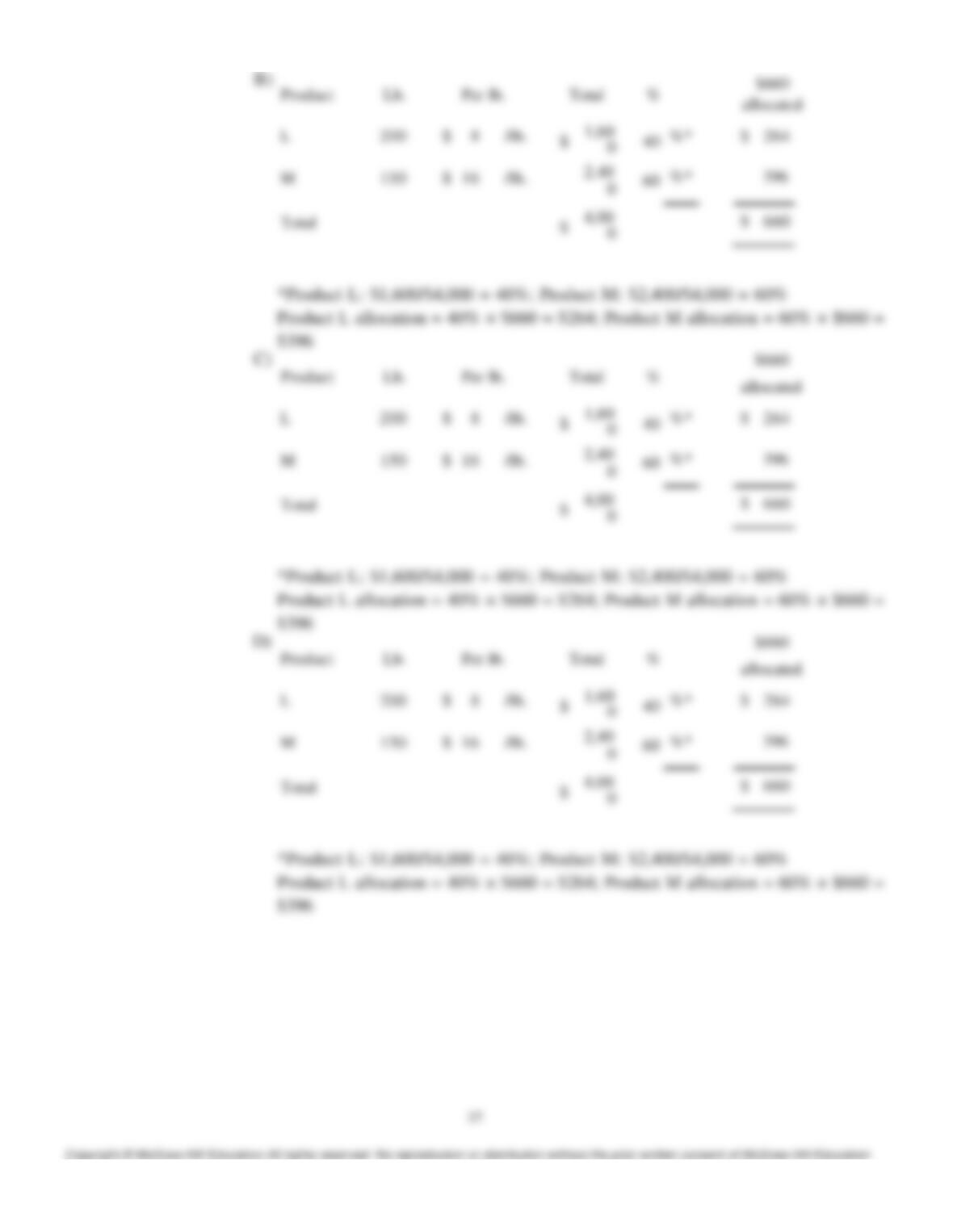

76) Data pertaining to a company’s joint production for the current period follows:

L

M

Quantities produced

Market value at split-off point

200 lbs.

$ 8 /lb.

150 lbs.

$ 16 /lb.

Compute the cost to be allocated to Product M for this period’s $660 of joint costs if the value basis is

used.

A) $330. B) $396. C) $1,364. D) $264. E) $796.

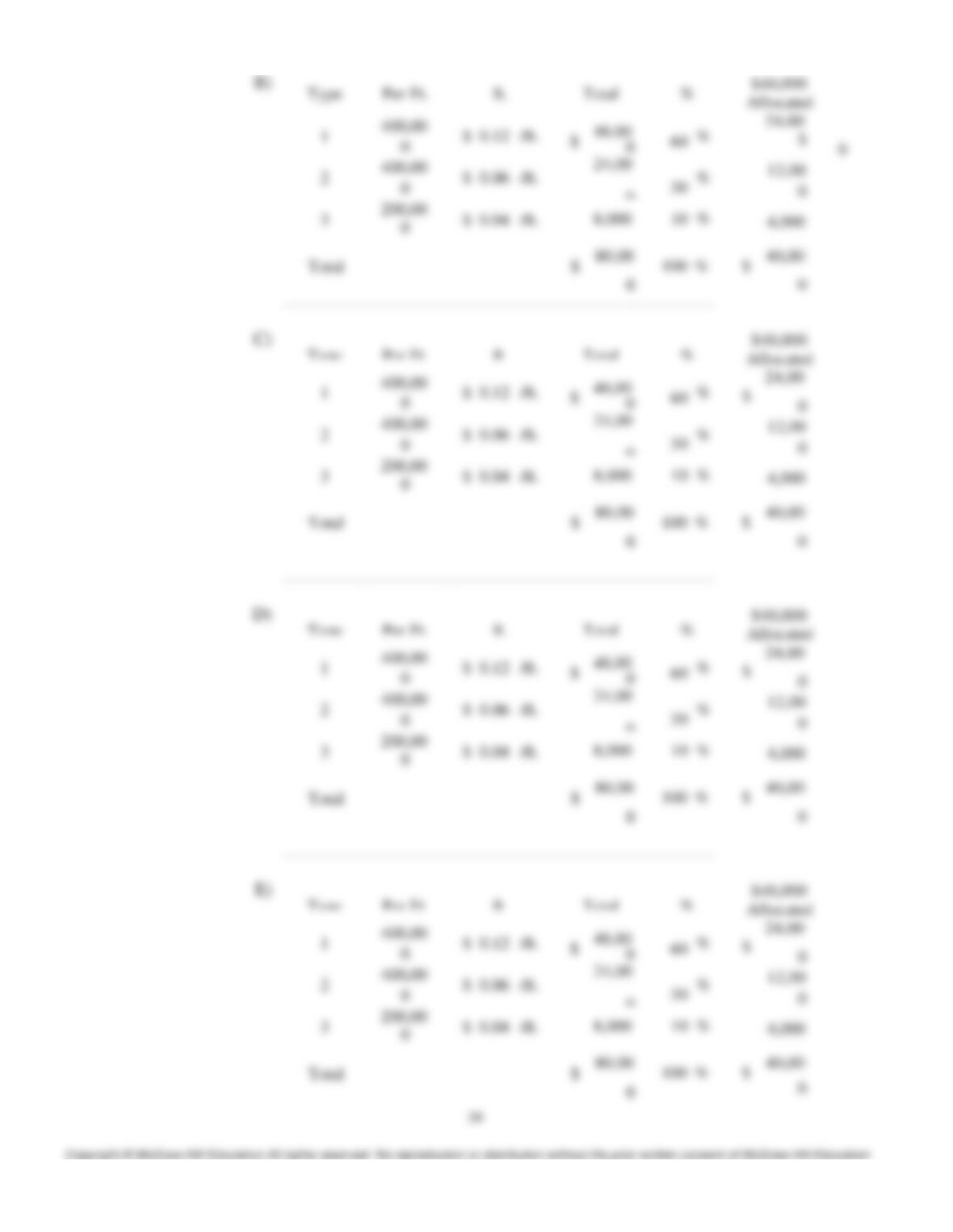

77) A lumber mill bought a shipment of logs for $40,000. When cut, the logs produced a million board

feet of lumber in the following grades. Compute the cost to be allocated to Type 1 and Type 2

lumber, respectively, if the value basis is used.

Type 1—400,000 bd. ft. priced to sell at $0.12 per bd. ft.

Type 2— 400,000 bd. ft. priced to sell at $0.06 per bd. ft.

Type 3— 200,000 bd. ft. priced to sell at $0.04 per bd. ft.

A) $40,000; $24,000.

B) $24,000; $8,000.

C) $13,333; $4,444.

D) $24,000; $12,000.

E) $16,000; $16,000.

78) A lumber mill paid $70,000 for logs that produced 200,000 board feet of lumber in 3 different grades

and amounts as follows:

Grade

Production

Market Price

Structural

25,000 board feet

$ 1,350/1,000 bd. ft.

No. 1 Common

No. 2 Common

75,000 board feet

100,000 board feet

$ 750/1,000 bd. ft.

$ 300/1,000 bd. ft.

Compute the portion of the $70,000 joint cost to be allocated to No. 2 Common if the value basis is

used.

A) $35,000. B) $70,000. C) $17,500. D) $23,333. E) $0.