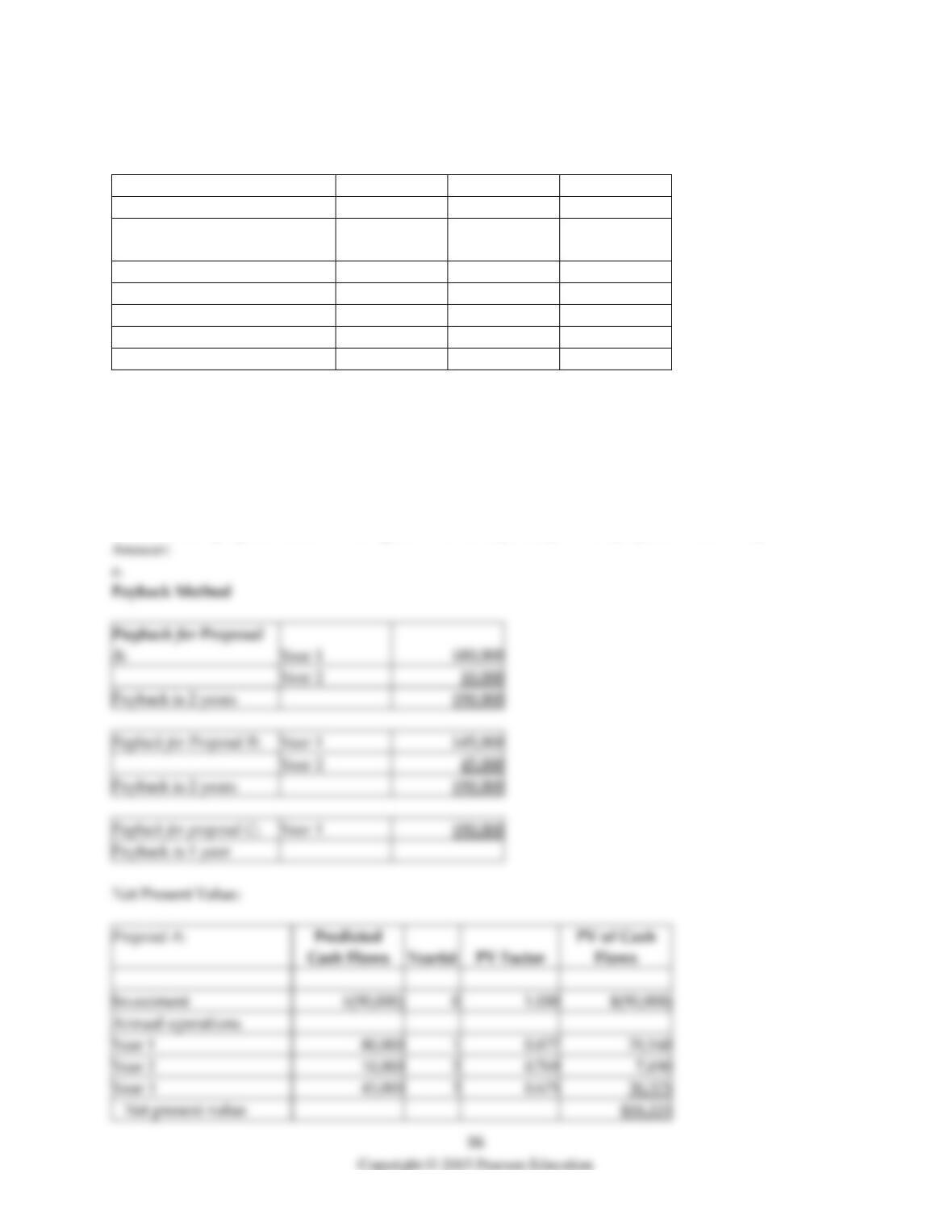

14) Gavin and Alex, baseball consultants, are in need of a microcomputer network for their staff. They

have received three proposals, with related facts as follows:

Proposal A

Proposal B

Proposal C

Initial investment in equipment

$90,000

$90,000

$90,000

Annual cash increase in

operations:

Year 1

80,000

45,000

90,000

Year 2

10,000

45,000

0

Year 3

45,000

45,000

0

Salvage value

0

0

0

Estimated life

3 yrs

3 yrs

1 yr

The company uses straight-line depreciation for all capital assets.

Required:

a. Compute the payback period, net present value, and accrual accounting rate of return with initial

investment, for each proposal. Use a required rate of return of 14%.

b. Rank each proposal 1, 2, and 3 using each method separately. Which proposal is best? Why?

10,000

45,000

Flows

Investment

Annual operations

Year 1

80,000

70,160

Year 3

45,000

30,375

Net present value

15) Gibson Manufacturing is considering buying an automated machine that costs $600,000. It requires

working capital of $60,000. Annual cash savings are anticipated to be $280,200 for five years. The

company uses straight-line depreciation. The salvage value at the end of five years is expected to be

$24,000. The working capital will be recovered at the end of the machine’s life.

Required:

Compute the accrual accounting rate of return based on the initial investment.

16) What are the four alternative methods for evaluating capital budgeting projects? What is an

advantage and disadvantage of each method?

17) Bock Construction Company is considering four proposals for the construction of new loading

facilities that will include the latest in ship loading/unloading equipment. After careful analysis, the

company’s accountant has developed the following information about the four proposals:

Proposal 1

Proposal 2

Proposal 3

Proposal 4

Payback period

4 years

4.5 years

6 years

7 years

Net present value

$80,000

$178,000

$166,000

$308,000

Internal rate of return

12%

14%

11%

13%

Accrual accounting rate of

return

8%

6%

4%

7%

Required:

How can this information be used in the decision-making process for the new loading facilities? Does it

cause any confusion?

18) What are the strengths and weaknesses of the accrual accounting rate-of-return (AARR) method for

evaluating long-term projects?

Objective 21.5

1) Which of the following is a component of net-initial-investment cash flows?

A) original cost of an old equipment

B) cash outflow to purchase a new equipment

C) depreciation cost

D) after-tax cash flow from operations

2) The Fortive Corporation disposes a capital asset with an original cost of $180,000 and accumulated

depreciation of $111,000 for $56,000. Alpha betas tax rate is 40%. Calculate the after-tax cash inflow from

the disposal of the capital asset.

A) $5,200

B) ($5,200)

C) $61,200

D) $69,000

3) The Golden Shades Corporation disposes a capital asset with an original cost of $280,000 and

accumulated depreciation of $160,000 for a salvage price of $50,000. Silver Shades’s tax rate is 40%.

Calculate the after-tax cash inflow from the disposal of the capital asset.

A) $28,000

B) $70,000

C) $50,000

D) $78,000

4) The Ambitz Corporation has an annual cash inflow from operations from its investment in a capital

asset of $35,000 each year for four years. The corporation’s income tax rate is 40%. Calculate the total

after-tax cash inflow from operations for four years.

A) $ 140,000

B) $ 150,000

C) $ 84,000

D) $35,000

5) The Venoid Corporation has an annual cash inflow from operations from its investment in a capital

asset of $16,000 each year for six years. The corporation’s income tax rate is 30%. Calculate the total after-

tax cash inflow from operations for six years.

A) $96,000

B) $67,200

C) $28,800

D) $16,000

6) A capital budgeting tool that management can use to summarize the difference in the future net cash

inflows from an intangible asset at two different points in time is referred to as:

A) the accrual accounting rate-of-return method

B) the net present value method

C) sensitivity analysis

D) the payback method

7) The focus in capital budgeting should be on ________.

A) favorable and unfavorable variance

B) expenses under accrual accounting

C) expected future cash flows that differ between alternatives

D) allocation of overheads

8) An example of a sunk cost in a capital budgeting decision for new equipment is ________.

A) the initial investment in working capital

B) the original price of an old equipment

C) the necessary transportation costs on a new equipment

D) the initial investment in a new equipment

9) Depreciation is usually NOT considered an operating cash flow in capital budgeting because ________.

A) depreciation is usually a constant amount each year over the life of the capital investment

B) deducting depreciation from operating cash flows would be counting the lump-sum amount twice

C) depreciation usually does not result in an increase in working capital

D) depreciation usually has no effect on the disposal price of the machine

10) The relevant terminal disposal price of a machine equals the ________.

A) difference between the salvage value of the old machine and the ultimate salvage value of the new

machine

B) total of the salvage values of the old machine and the new machine

C) salvage value of the old machine

D) salvage value of the new machine

11) Net initial investment includes ________.

A) depreciation on new equipment, cash outflow for working capital, and after-tax cash inflow from

disposal of the old equipment

B) cash outflow to purchase new equipment, depreciation on new equipment, and after-tax cash inflow

from disposal of the old equipment

C) cash outflow to purchase new equipment, cash outflow for working capital, and after-tax cash inflow

from disposal of the old equipment

D) cash outflow to purchase new equipment, cash outflow for working capital, and depreciation on new

equipment

12) The income taxes saved as a result of depreciation deductions are irrelevant because they decrease

cash outflows.

13) Tax deductions for depreciation result in tax savings that partially offset the cost of acquiring the

capital asset.

14) The use of an accelerated method of depreciation for tax purposes would usually decrease the present

value of the investment.

15) Net initial investment in the project includes the acquisition of assets and any associated additions to

working capital, minus the after-tax cash flow from the disposal of existing assets.

16) Relevant cash flows are expected future cash flows that differ among the alternative uses of

investment funds.

17) Deducting depreciation from operating cash flows would result in counting the initial investment

twice in a discounted cash flow analysis.

18) In determining whether to keep a machine or replace it, the original cost of the machine is a sunk cost

and is NOT a relevant factor.

19) In the net present value (NPV) method, pre-tax cash flows should be used instead of after-tax cash

flows when taxes are a consideration.

20) In calculating the net initial investment cash flows, any increase in working capital required for the

project should be included.

21) Cash received from the disposal of old equipment is NOT relevant to a decision to buy a replacement.

22) A increase in the tax rate will increase the net present value (NPV) for a given capital budgeting

project.

23) While calculating terminal recovery of working capital there are no tax consequences as there is no

gain or loss on working capital.

24) Depreciation results in income tax cash savings which are not relevant in capital budgeting decisions.

25) Explain why the term tax shield is used in conjunction with depreciation.

26) What are the relevant cash inflows and outflows for capital budgeting decisions?

Objective 21.6

1) Which of the following statements is true of a post-investment audit?

A) It encourages managers to overstate the expected cash inflows from projects and accept projects they

should reject.

B) It helps managers avoid optimistic estimate errors.

C) It does not help senior management to recognize problems in the implementation of the project.

D) It provides managers with feedback about the performance of a project so they can compare the actual

results to the costs and benefits expected at the time the project was selected.

2) Comparison of the actual results for a project to the costs and benefits expected at the time the project

was selected is referred to as ________.

A) the audit trail

B) management control

C) a post-investment audit

D) a cost-benefit analysis

3) Post-investment audits ________.

A) result in managers to overstate the expected cash inflows from projects and accept projects they

should reject

B) provide management with feedback about the performance of a project

C) include obtaining appropriation requests so that the funding will be authorized to purchase the

equipment

D) are usually not feasible in a large project because the cost accounting system does not collect actual

costs at the same level of detail as the initial plans had

4) The reason to have a post-investment audit is ________.

A) they encourage mid-level managers to make overly optimistic estimates during the early stages of the

capital budgeting process

B) they help alert senior management to problems in the implementation of projects

C) they analyze by calculating contribution-margin

D) they help in calculating present value

5) As a discounted cash flow method does not report good operating income results in the project’s early

years, managers are tempted to not use discounted cash flow methods even though the decisions based

on them would be in the best interests of the company as a whole over the long run.

6) Post-investment audits prevent managers from overstating the expected cash inflows from projects and

accepting projects they should reject.

7) What conflicts can arise between using discounted cash flow methods for capital budgeting decisions

and accrual accounting for performance evaluation? How can these conflicts be reduced?

1) Using capital budgeting techniques to track and (based on success to date) modify resource levels

committed to staged R&D investments is called timed options.

2) Discuss a range of factors that managers may have to consider when making capital budgeting

decisions that are strategic in nature.

Objective 21.A

1) The nominal approach to incorporating inflation into the net present value method predicts ________.

A) cash inflows and outflows in nominal monetary units and uses a real rate as the required rate of return

B) cash inflows and outflows in real monetary units and uses a nominal rate as the required rate of return

C) cash inflows and outflows in real monetary units and uses a real rate as the required rate of return

D) cash inflows and outflows in nominal monetary units and uses a nominal rate as the required rate of

return

2) The nominal approach to incorporating inflation into the net present value method predicts cash

inflows in real monetary units and uses a real rate as the required rate of return.

3) In nominal rate of return, the inflation element is the premium above the real rate.

4) The nominal rate of return is made up of a risk-free element when there is no expected inflation, a

business-risk element, and an inflation element.

5) What is the difference between nominal approach and real approach to incorporating inflation into the

net present value method?

6) How is inflation related to capital budgeting? Discuss.