Accounting for Pensions and Postretirement Benefits

20–21

82. The unexpected gain or loss on plan assets in 2015 is

a. $45,920 loss.

b. $26,320 gain.

c. $22,400 gain.

d. $250,320 gain.

83. The corridor for 2015 is

a. $722,400.

b. $728,000.

c. $791,000.

d. $933,800.

84. The amount of AOCI (net gain) amortized in 2015 is

a. $17,850.

b. $17,500.

c. $13,563.

d. $11,638.

85. Presented below is information related to Decker Manufacturing Company as of

December 31, 2015:

Projected benefit obligation $850,000

Accumulated OCI -net gain 300,000

Accumulated OCI (PSC) 405,000

The amount for the prior service cost is related to an increase in benefits. The fair value of

the pension plan assets is $600,000.

The pension asset / liability reported on the balance sheet at December 31, 2015 is

a. Pension liability of $250,000

b. Pension liability of $600,000

c. Pension liability of $850,000

d. Pension liability of $1,255,000

Use the following information for questions 86 and 87.

Foster Corporation received the following report from its actuary at the end of the year:

December 31, 2014 December 31, 2015

Projected benefit obligation $2,000,000 $2,200,000

Accumulated benefit obligation 1,300,000 1,480,000

Fair value of pension plan assets 1,380,000 1,440,000

86. The amount reported as the pension liability at December 31, 2014 is

a. $ -0-.

b. $80,000.

c. $620,000.

d. $700,000.

Test Bank for Intermediate Accounting, Fifteenth Edition

20–22

87. The amount reported as the pension liability at December 31, 2015 is

a. $2,200,000

b. $1,480,000

c. $720,000

d. $760,000

Use the following information for questions 88 and 89.

The following information relates to Jackson, Inc.:

For the Year Ended December 31,

2014 2015

Plan assets (at fair value) $1,360,000 $1,824,000

Pension expense 570,000 450,000

Projected benefit obligation 1,620,000 1,934,000

Annual contribution to plan 600,000 450,000

Accumulated OCI (PSC) 480,000 420,000

88. The amount reported as the liability for pensions on the December 31, 2014 balance

sheet is

a. $ -0-.

b. $30,000.

c. $260,000.

d. $230,000.

89. The amount reported as the liability for pensions on the December 31, 2015 balance

sheet is

a. $ -0-.

b. $110,000.

c. $1,934,000.

d. $420,000.

90. Presented below is information related to Noble Inc. as of December 31, 2015.

Accumulated OCI (G/L) $ 90,000

Projected benefit obligation 3,650,000

Accumulated benefit obligation 3,420,000

Vested benefits 1,620,000

Plan assets (at fair value) 3,354,000

Accumulated OCI (PSC) -0-

The amount reported as the pension liability on Noble’s balance sheet at December 31,

2015 is as follows:

a. $ -0-.

b. $66,000.

c. $230,000.

d. $296,000.

Accounting for Pensions and Postretirement Benefits

20–23

91. Rossi Company has a defined-benefit plan. At the end of 2015, it has determined the

following information related to its pension plan:

Projected benefit obligation $730,000

Accumulated benefit obligation 660,000

Fair value of pension plan assets 610,000

The amount of pension liability that is reported in Rossi‘s balance sheet at the end of 2015 is

a. $150,000.

b. $120,000.

c. $70,000.

d. $50,000.

92. Presented below is pension information related to Waters Company as of December 31,

2015:

Accumulated benefit obligation $3,000,000

Projected benefit obligation 3,500,000

Plan assets (at fair value) 3,750,000

Accumulated OCI (G / L) 100,000

The amount to be reported as Pension Asset / Liability as of December 31, 2015 is

a. Pension Liability of $500,000.

b. Pension Asset of $750,000.

c. Pension Liability of $250,000.

d. Pension Asset of $250,000.

Use the following information for questions 93 and 94.

On January 1, 2015, Parks Co. has the following balances:

Projected benefit obligation $4,200,000

Fair value of plan assets 3,750,000

The settlement rate is 10%. Other data related to the pension plan for 2015 are:

Service cost $240,000

Amortization of prior service costs 54,000

Contributions 270,000

Benefits paid 250,000

Actual return on plan assets 264,000

Amortization of net gain 18,000

93. The balance of the projected benefit obligation at December 31, 2015 is

a. $4,494,000.

b. $4,596,000.

c. $4,860,000.

d. $4,610,000.

94. The fair value of plan assets at December 31, 2015 is

a. $3,506,000.

b. $3,764,000.

c. $4,034,000.

d. $4,284,000.

Test Bank for Intermediate Accounting, Fifteenth Edition

20–24

95. Huggins Company has the following information at December 31, 2015 related to its

pension plan:

Projected benefit obligation $4,000,000

Accumulated benefit obligation 3,200,000

Plan assets (fair value) 4,350,000

Accumulated OCI (PSC) 300,000

The amount of pension asset / liability Huggins Company would recognize at December 31,

2015 is

a. Pension liability of $300,000.

b. Pension asset of $1,150,000.

c. Pension liability of $800,000.

d. Pension asset of $350,000.

96. The following pension plan information is for Farr Company at December 31, 2015.

Projected benefit obligation $8,500,000

Accumulated benefit obligation 7,500,000

Plan assets (at fair value) 6,150,000

Accumulated OCI (PSC) 540,000

Pension expense for 2015 3,000,000

Contribution for 2015 2,400,000

The amount to be reported as the liability for pensions on the December 31, 2015 balance

sheet is

a. $2,350,000.

b. $2,150,000.

c. $1,600,000.

d. $1,350,000.

*97. The following facts relate to the Patton Co. postretirement benefits plan for 2015:

Service cost $180,000

Discount rate 9%

APBO, January 1, 2015 $1,500,000

EPBO, January 1, 2015 $2,000,000

Benefit payments to employees $115,000

The amount of postretirement expense for 2015 is

a. $180,000.

b. $315,000.

c. $360,000.

d. $430,000.

Accounting for Pensions and Postretirement Benefits

20–25

*98. The following facts relate to the postretirement benefits plan of Keller, Inc. for 2015:

Service cost $730,000

Discount rate 8%

APBO, January 1, 2015 $4,000,000

EPBO, January 1, 2015 $4,800,000

Average remaining service to full eligibility 20 years

Average remaining service to expected retirement 25 years

The amount of postretirement expense for 2015 is

a. $1,050,000.

b. $1,210,000.

c. $1,250,000.

d. $1,114,000.

*99. The following facts relate to the Gamble Co. postretirement benefits plan for 2015:

Service cost $136,000

Discount rate 10%

EPBO, January 1, 2015 $1,095,000

APBO, January 1, 2015 $900,000

Actual return on plan assets in 2015 $31,500

Expected return on plan assets in 2015 $24,000

The amount of postretirement expense for 2015 is

a. $194,500.

b. $202,000.

c. $221,500.

d. $226,000.

Test Bank for Intermediate Accounting, Fifteenth Edition

20–26

MULTIPLE CHOICE—CPA Adapted

100. The following information pertains to Hopson Co.’s pension plan:

Actuarial estimate of projected benefit obligation at 1/1/15 $72,000

Assumed discount rate 10%

Service costs for 2015 $28,000

Pension benefits paid during 2015 $15,000

If no change in actuarial estimates occurred during 2015, Hopson‘s projected benefit

obligation at December 31, 2015 was

a. $79,200.

b. $80,000.

c. $102,200.

d. $87,200.

101. Interest cost included in pension expense recognized for a period by an employer

sponsoring a defined-benefit pension plan represents the

a. shortage between the expected and actual returns on plan assets.

b. increase in the projected benefit obligation due to the passage of time.

c. increase in the fair value of plan assets due to the passage of time.

d. amortization of the discount on accumulated OCI (PSC).

102. Logan Corp., a company whose stock is publicly traded, provides a noncontributory

defined-benefit pension plan for its employees. The company’s actuary has provided the

following information for the year ended December 31, 2015:

Projected benefit obligation $700,000

Accumulated benefit obligation 525,000

Fair value of plan assets 825,000

Service cost 240,000

Interest on projected benefit obligation 24,000

Amortization of prior service cost 60,000

Expected and actual return on plan assets 82,500

The market-related asset value equals the fair value of plan assets. No contributions have

been made for 2015 pension cost. In its December 31, 2015 balance sheet, Logan should

report a pension asset / liability of

a. Pension liability of $700,000

b. Pension asset of $825,000

c. Pension asset of $125,000

d. Pension liability of $525,000

103. Seigel Co. maintains a defined-benefit pension plan for its employees. At each balance

sheet date, Yeager should report a pension asset / liability equal to the

a. accumulated benefit obligation.

b. projected benefit obligation.

c. accumulated benefit obligation.

d. funded status relative to the projected benefit obligation.

Accounting for Pensions and Postretirement Benefits

20–27

104. Ohlman, Inc. maintains a defined-benefit pension plan for its employees. As of December

31, 2015, the market value of the plan assets is less than the accumulated benefit

obligation. The projected benefit obligation exceeds the accumulated benefit obligation. In

its balance sheet as of December 31, 2015, Ohlman should report a liability in the amount

of the

a. excess of the projected benefit obligation over the fair value of the plan assets.

b. excess of the accumulated benefit obligation over the fair value of the plan assets.

c. projected benefit obligation.

d. accumulated benefit obligation.

105. At December 31, 2015, the following information was provided by the Vargas Corp.

pension plan administrator:

Fair value of plan assets $4,500,000

Accumulated benefit obligation 5,580,000

Projected benefit obligation 7,400,000

What is the amount of the pension liability that should be shown on Vargas’ December 31,

2013 balance sheet?

a. $7,400,000

b. $2,900,000

c. $1,820,000

d. $1,080,000

DERIVATIONS — Computational

No. Answer Derivation

Test Bank for Intermediate Accounting, Fifteenth Edition

20–28

DERIVATIONS — Computational (cont.)

No. Answer Derivation

Accounting for Pensions and Postretirement Benefits

20–29

DERIVATIONS — Computational (cont.)

DERIVATIONS — CPA Adapted

No. Answer Derivation

BRIEF EXERCISES

BE. 20-106—Pension accounting terminology.

Briefly explain the following terms:

(a) Service cost

(b) Interest cost

(c) Prior service cost

(d) Vested benefits

Solution 20-106

Test Bank for Intermediate Accounting, Fifteenth Edition

20–30

BE. 20-107—Pension assets.

Discuss the following ideas related to pension assets:

(a) Market-related asset value.

(b) Actual return on plan assets.

(c) Expected return on plan assets.

(d) Unexpected gains and losses on plan assets.

Solution 20-107

BE. 20-108—Measuring and recording pension expense.

Kessler, Inc. received the following information from its pension plan trustee concerning the

operation of the company’s defined-benefit pension plan for the year ended December 31, 2015:

January 1, 2015 December 31, 2015

Projected benefit obligation $2,500,000 $2,850,000

Fair value of plan assets 1,250,000 1,600,000

Accumulated benefit obligation 1,930,000 2,620,000

Accumulated OCI – (PSC) 540,000 300,000

The service cost component for 2015 is $140,000 and the amortization of prior service cost is

$240,000. The company’s actual funding of the plan in 2015 amounted to $500,000. The

expected return on plan assets and the settlement rate were both 8%.

Instructions

(a) Determine the pension expense to be reported in 2015.

(b) Prepare the journal entry to record pension expense and the employers’ contribution to the

pension plan in 2015.

Accounting for Pensions and Postretirement Benefits

20–31

Solution 20-108

BE. 20-109—Measuring and recording pension expense.

Presented below is information related to Jones Department Stores, Inc. pension plan for 2015.

Accumulated benefit obligation (at year-end) $600,000

Service cost 540,000

Funding contribution for 2015 480,000

Settlement rate used in actuarial computation 10%

Expected return on plan assets 9%

Amortization of PSC (due to benefit increase) 100,000

Amortization of net gains 48,000

Projected benefit obligation (at beginning of period) 470,000

Fair value of plan assets (at beginning of period) 360,000

Instructions

(a) Compute the amount of pension expense to be reported for 2015. (Show computations.)

(b) Prepare the journal entry to record pension expense and the employer’s contribution for

2015.

Solution 20-109

Test Bank for Intermediate Accounting, Fifteenth Edition

20–32

BE. 20-110— Recording pension asset / liability.

Miles Co. had the following selected balances at December 31, 2015:

Projected benefit obligation $4,650,000

Accumulated benefit obligation 4,550,000

Fair value of plan assets 4,340,000

Accumulated OCI (PSC) 170,000

Instructions

Calculate the pension asset / liability to be recorded at December 31, 2015.

Solution 20-110

EXERCISES

Ex. 20-111—Pension calculations.

Montoya Company has available the following information about its defined-benefit pension plan

for the year ending December 31, 2015:

Service cost for 2015 $ 25,000

Accumulated benefit obligation 683,000

Plan assets at fair value 630,000

Accumulated OCI (PSC) 300,000

Vested benefit obligation 505,000

Market-related asset value 725,000

Projected benefit obligation 845,000

Accumulated OCI net gain 90,000

Interest on projected benefit obligation 64,000

Instructions

(a) Calculate the pension asset / liability to be recorded at December 31, 2015.

(b) Calculate the 2016 amortization of the net gain. The average remaining service life of

employees is 10 years.

Solution 20-111

Ex. 20-112—Pension plan calculations.

The following information is for the pension plan for the employees of Payne, Inc.

12/31/14 12/31/15

Accumulated benefit obligation $2,800,000 $3,760,000

Projected benefit obligation 3,100,000 4,000,000

Fair value of plan assets 3,130,000 3,630,000

AOCI – Net (gain) or loss (425,000) (480,000)

Accounting for Pensions and Postretirement Benefits

20–33

Settlement rate 8% 8%

Expected rate of return 7% 6%

Payne estimates that the average remaining service life is 15 years. Payne’s contribution was

$520,000 in 2015 and benefits paid were $260,000.

Instructions

(a) Calculate the interest cost for 2015.

(b) Calculate the actual return on plan assets in 2015.

(c) Calculate the unexpected gain or loss in 2015.

(d) Calculate the corridor for 2015 and the amortization of the net gain for 2015.

Solution 20-112

Ex. 20-113—Pension plan calculations and entries.

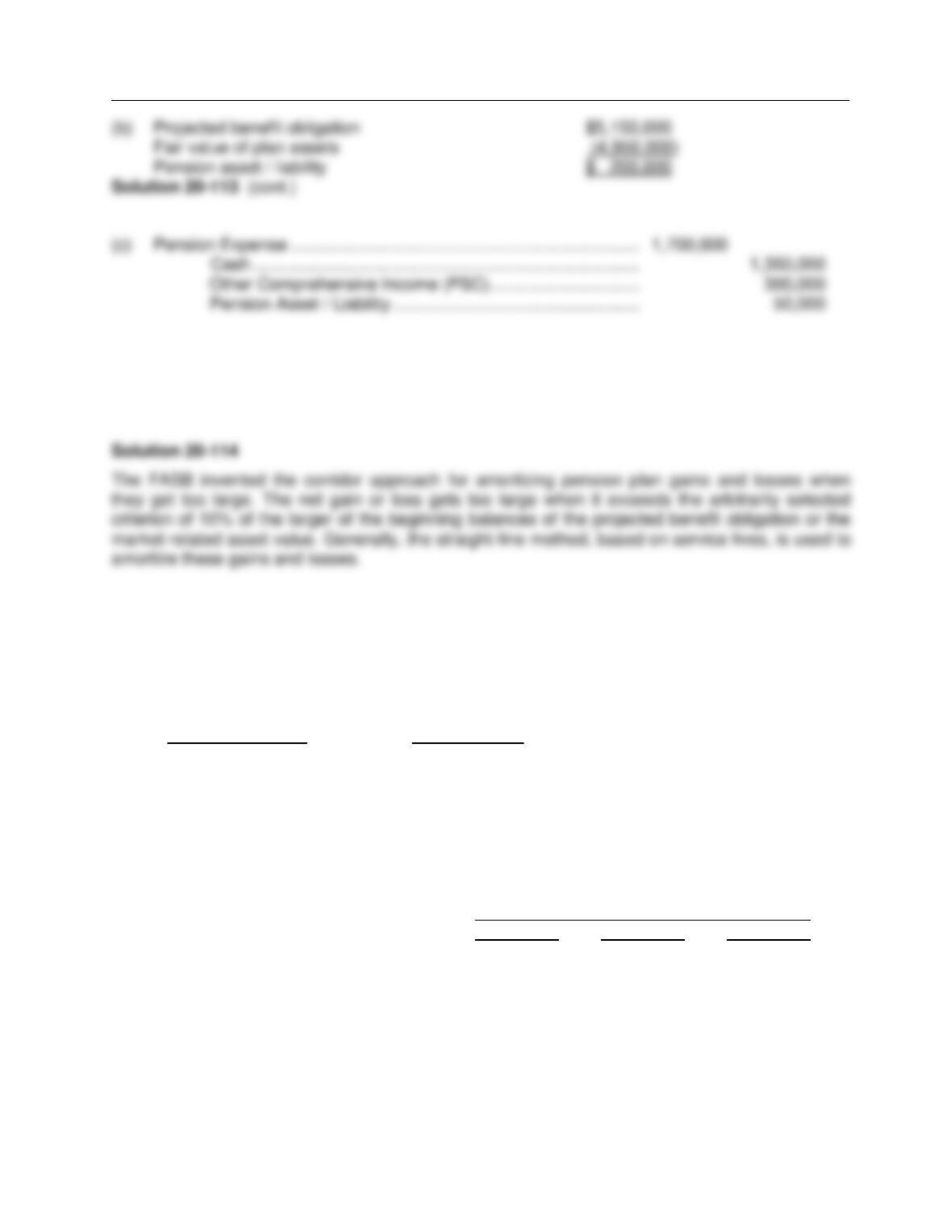

Selected Information about the pension plan of Roman Co. is as follows:

12/31/14 12/31/15

Accumulated benefit obligation $4,700,000 $4,930,000

Projected benefit obligation 4,950,000 5,150,000

Accumulated OCI (PSC) 1,800,000 1,500,000

Fair value of plan assets 4,750,000 4,950,000

Pension expense 1,000,000 1,700,000

Contribution 985,000 1,350,000

Discount rate (for year) 9% 8%

Instructions

(a) What is the corridor for 2015?

(b) Calculate the pension asset / liability at December 31, 2015.

(c) Prepare the entry for 2015 to record the pension expense and contribution.

Solution 20-113

Test Bank for Intermediate Accounting, Fifteenth Edition

20–34

Ex. 20-114—Corridor amortization.

Explain corridor amortization.

Ex. 20-115—Corridor approach (amortization of net gains and losses.)

Gibbs Company has 200 employees who are expected to receive benefits under the company‘s

defined-benefit pension plan. The total number of service-years of these employees is 2,000. The

actuary for the company’s pension plan calculated the following net gains and losses:

For the Year Ended

December 31 (Gain) Or Loss

2014 $640,000

2015 (554,000)

2016 990,000

Prior to 2014, there was no unrecognized net gain or loss.

Information about the company’s projected benefit obligation and market-related (and fair) value

of plan assets follows:

As of January 1

2014 2015 2016

Projected benefit obligation $2,100,000 $2,340,000 $2,940,000

Fair value of plan assets 1,680,000 2,460,000 2,550,000

Instructions

Based on the above information about Gibbs Company, prepare a schedule which reflects the

amount of net gain or loss to be amortized by the company as a component of pension expense

for the years 2014, 2015, and 2016. The company amortizes net gains or losses using the

straight-line method over the average service life of participating employees.

Accounting for Pensions and Postretirement Benefits

20–35

Ex. 20-116—Pension plan calculations and journal entry.

On January 1, 2015, McGee Co. had the following balances:

Projected benefit obligation $7,400,000

Fair value of plan assets 7,400,000

Other data related to the pension plan for 2015:

Service cost 315,000

Contributions to the plan 459,000

Benefits paid 450,000

Actual return on plan assets 444,000

Settlement rate 9%

Expected rate of return 6%

Instructions

(a) Determine the projected benefit obligation at December 31, 2015. There are no net gains or

losses.

(b) Determine the fair value of plan assets at December 31, 2015.

(c) Calculate pension expense for 2015.

(d) Prepare the journal entry to record pension expense and the contributions for 2015.

Test Bank for Intermediate Accounting, Fifteenth Edition

20–36

*Ex. 20-117—Computing and recording postretirement expense.

The following information is related to the Stone Co. postretirement benefits plan for 2015:

Service cost $163,000

Discount rate 10%

EPBO, January 1, 2015 820,000

APBO, January 1, 2015 660,000

Actual return on plan assets in 2015 22,400

Expected return on plan assets in 2015 29,000

Contributions (funding) 224,000

Instructions

(a) Compute the amount of postretirement expense for 2015. (Show computations.)

(b) Prepare the journal entry to record postretirement expense and Stone‘s contributions for

2015.

*Ex. 20-118—Computing postretirement expense and APBO.

The following information is related to the postretirement benefits plan of Heerey, Inc. for 2015:

Service cost $ 280,000

Discount rate 8%

APBO, January 1, 2015 2,250,000

EPBO, January 1, 2015 2,400,000

Actual return on plan assets in 2015 104,000

Expected return on plan assets in 2015 95,600

Amortization of PSC, due to benefit increase 107,200

Contributions (funding) 400,000

Benefit payments 208,000