Cost Accounting, 15e Global Edition (Horngren/Datar/Rajan)

Chapter 2 An Introduction to Cost Terms and Purposes

Objective 2.1

1) An actual cost is ________.

A) is the cost incurred

B) is a predicted or forecasted cost

C) is anything for which a cost measurement is desired

D) is the collection of cost data in some organized way by means of an accounting system

2) Comparing budgeted costs to actual costs helps managers to improve ________.

A) coordination

B) control

C) implementation

D) planning

3) Budgeted costs are ________.

A) the costs incurred this year

B) the costs incurred last year

C) planned or forecasted costs

D) competitor’s costs

4) Cost assignment ________.

A) includes future and arbitrary costs

B) encompasses allocating indirect costs to a cost object

C) is the same as cost accumulation

D) is the difference between budgeted and actual costs

5) A cost system determines the cost of a cost object by ________.

A) accumulating and then assigning costs

B) accumulating costs

C) assigning and then accumulating costs

D) assigning costs

6) A cost object is anything for which a cost measurement is desired.

7) Costs are accounted for in two basic stages: assignment followed by accumulation.

8) An actual cost is the cost incurred–a historical or past cost.

9) Accountants define a cost as a resource to be sacrificed to achieve a specific objective.

10) A cost is a resource sacrificed or forgone to achieve a specific objective.

11) Managers use cost accumulation data to make decisions and implement them.

12) Lucas Manufacturing has three cost objects that it uses to accumulate costs for its manufacturing

plants. They are:

Cost object #1: The physical buildings and equipment

Cost object #2: The use of buildings and equipment

Cost object #3: The availability and use of manufacturing labor

The following manufacturing overhead cost categories are found in the accounting records:

a. Depreciation on buildings and equipment

b. Lubricants for machines

c. Property insurance

d. Supervisors salaries

e. Fringe benefits

f. Property taxes

g. Utilities

Required:

Assign each of the above costs to the most appropriate cost object.

Objective 2.2

1) Which of the following factors affect the direct/indirect classification of a cost?

A) the level of budgeted profit for the next year

B) the estimation of time required to complete the order

C) the ability to execute an order in the most cost-efficient manner

D) the design of the operation

2) The general term used to identify both the tracing and the allocation of accumulated costs to a cost

object is ________.

A) cost accumulation

B) cost assignment

C) cost tracing

D) conversion costing

3) Cost accumulation is ________.

A) the collection of cost data in some organized way by means of an accounting system

B) anything for which a cost measurement is desired

C) anything for which a profit measurement is desired

D) the collection of profit data in some organized way by means of an accounting system

4) Which of the following statements about the direct/indirect cost classification is true?

A) Indirect costs are always traced.

B) Indirect costs are always allocated.

C) The design of sales target affects the direct/indirect classification.

D) The direct/indirect classification depends on the cost control measures.

5) Cost tracing is ________.

A) the assignment of direct costs to the chosen cost object

B) a function of cost allocation

C) the process of tracking both direct and indirect costs associated with a cost object

D) the process of determining the actual cost of the cost object

6) Cost allocation is ________.

A) the process of tracking both direct and indirect costs associated with a cost object

B) the process of determining the opportunity cost of a cost object chosen

C) the assignment of indirect costs to the chosen cost object

D) made based on material acquisition document

7) The determination of a cost as either direct or indirect depends upon the ________.

A) accounting standards

B) tax system chosen

C) inventory valuation

D) cost object chosen

8) Classifying a cost as either direct or indirect depends upon ________.

A) the behavior of the cost in response to volume changes

B) whether the cost is expensed in the period in which it is incurred

C) whether the cost can be easily traced with the cost object

D) whether a cost is fixed or variable

9) A manufacturing plant produces two product lines: golf equipment and soccer equipment. An example

of direct costs for the golf equipment line is ________.

A) beverages provided daily in the plant break room

B) monthly lease payments for a specialized piece of equipment needed to manufacture the golf driver

C) salaries of the clerical staff that work in the company administrative offices

D) overheads incurred in producing both golf and soccer equipment

10) A manufacturing plant produces two product lines: golf equipment and soccer equipment. An

example of indirect cost for the soccer equipment line is the ________.

A) material used to make the soccer balls

B) labor to shape the leather used to make the soccer ball

C) material used to manufacture the soccer studs

D) salary paid to plant supervisor

11) Which one of the following items is a direct cost?

A) Customer-service costs of a multiproduct firm; Product A is the cost object.

B) Printing costs incurred for payroll check processing; payroll check processing is the cost object.

C) The salary of a maintenance supervisor in a multiproduct manufacturing plant; Product B is the cost

object.

D) Utility costs of the administrative offices; the accounting department is the cost object.

12) Indirect manufacturing costs ________.

A) can be traced to the product that created the costs

B) can be easily identified with the cost object

C) generally include the cost of material and the cost of labor

D) may include both variable and fixed costs

13) Which of the following is true of indirect costs?

A) Indirect costs are always considered sunk costs.

B) All indirect costs are included in cost of goods sold.

C) Indirect costs always vary in direct proportion to the level of production.

D) Indirect costs cannot be traced to a particular cost object in an economically feasible way.

14) Which of the following statements is true?

A) A direct cost of one cost object will always be a direct cost of another cost object.

B) Because of a cost-benefit tradeoff, some direct costs may be treated as indirect costs.

C) All fixed costs are indirect costs.

D) All direct costs are variable costs.

15) Which of the following statements is true of direct costs?

A) A direct cost of one cost object is a true sense of the budgeted costs.

B) All variable costs are direct costs.

C) A direct cost of one cost object can be an indirect cost of another cost object.

D) All fixed costs are direct costs.

16) A cost may be direct for one cost object and indirect for another cost object.

17) Assigning indirect costs is easier than assigning direct costs.

18) Improvements in information-gathering technologies are making it possible to trace more costs as

direct.

19) The smaller the amount of a cost the more likely it is economically feasible to trace it to a particular

cost object.

20) A direct cost of one cost object can be an indirect cost of another cost object.

21) The cost of electricity used in the production of multiple products would be classified as a indirect

cost.

22) The broader the cost object definition, higher the proportion of direct costs are of total costs.

23) The distinction between direct and indirect costs is clearly set forth in Generally Accepted Accounting

Principles (GAAP).

24) Archambeau Products Company manufactures office furniture. Recently, the company decided to

develop a formal cost accounting system and classify all costs into three categories. Categorize each of the

following items as being appropriate for (1) cost tracing to the finished furniture, (2) cost allocation of an

indirect manufacturing cost to the finished furniture, or (3) as a nonmanufacturing item.

Cost Cost Nonmanu-

Item Tracing Allocation facturing

Carpenter wages ________ ________ ________

Depreciation – office building ________ ________ ________

Glue for assembly ________ ________ ________

Lathe department supervisor ________ ________ ________

Lathe depreciation ________ ________ ________

Lathe maintenance ________ ________ ________

Lathe operator wages ________ ________ ________

Lumber ________ ________ ________

Samples for trade shows ________ ________ ________

Metal brackets for drawers ________ ________ ________

Factory washroom supplies ________ ________ ________

25) What are the factors that affect the classification of a cost as direct or indirect?

26) What are the differences between direct costs and indirect costs? Give an example of each.

1) Which of the following is true if the volume of sales increases?

A) fixed cost increases

B) variable cost decreases

C) variable cost increases

D) fixed cost decreases

2) Which of the following is a fixed cost?

A) monthly rent payment

B) electricity expenses

C) travel expenses

D) direct material costs

3) Cost behavior refers to ________.

A) how costs react to a change in the level of activity

B) whether a cost is incurred in a manufacturing, merchandising, or service company

C) classifying costs as either perpetual or period costs

D) whether a particular expense is expensed in the same or the following period

4) Which of the following is true if the production volume decreases?

A) fixed cost per unit increases

B) average cost per unit decreases

C) variable cost per unit increases

D) variable cost per unit decreases

5) At a plant where a union agreement sets annual salaries and conditions, annual labor costs usually

________.

A) are considered a variable cost

B) are considered a fixed cost

C) depend on the scheduling of floor workers

D) depend on the scheduling of production runs

6) Variable costs ________.

A) are always indirect costs

B) increase in total when the actual level of activity increases

C) include most personnel costs and depreciation on machinery

D) are never considered a part of prime cost

7) Maize Plastics manufactures and sells 50 bottles per day. Fixed costs are $30,000 and the variable costs

for manufacturing 50 bottles are $10,000. Each bottle is sold for $1,000. How would the daily profit be

affected if the daily volume of sales drop by 10%?

A) profits are reduced by $4,000

B) profits are reduced by $1,000

C) profits are reduced by $5,000

D) profits are reduced by $6,000

8) Fixed costs depend on the ________.

A) amount of resources used

B) amount of resources acquired

C) volume of production

D) total number of units sold

9) Which one of the following is a variable cost for an insurance company?

A) rent of the building

B) CEO’s salary

C) electricity expenses

D) property taxes

10) Which of the following is a fixed cost for an automobile manufacturing plant?

A) administrative salaries

B) electricity used by assembly-line machines

C) sales commissions

D) tires

11) If each motorcycle requires a belt that costs $20 and 2,000 motorcycles are produced for the month, the

total cost for belts is ________.

A) considered to be a direct fixed cost

B) considered to be a direct variable cost

C) considered to be an indirect fixed cost

D) considered to be an indirect variable cost

12) The most likely cost driver of distribution costs is the ________.

A) number of parts within the product

B) number of miles driven

C) number of products manufactured

D) number of production hours

13) The most likely cost driver of direct labor costs is the ________.

A) number of machine setups for the product

B) number of miles driven

C) number of production hours

D) number of machine hours

14) Which of the following statements is true?

A) There is a cause-and-effect relationship between the cost driver and the amount of cost.

B) Fixed costs have cost drivers over the short run.

C) Over the short run all costs have cost drivers.

D) Volume of production is a cost driver of distribution costs.

15) A band of normal activity or volume in which specific cost-volume relationships are maintained is

referred to as the ________.

A) average range

B) cost-allocation range

C) cost driver range

D) relevant range

16) Within the relevant range, if there is a change in the level of the cost driver, then ________.

A) total fixed costs and total variable costs will change

B) total fixed costs and total variable costs will remain the same

C) total fixed costs will remain the same and total variable costs will change

D) total fixed costs will change and total variable costs will remain the same

17) Outside the relevant range, variable costs, such as direct material costs ________.

A) will decrease proportionately with changes in sales volumes

B) will remain the same with changes in production volumes

C) will not change proportionately with changes in production volumes

D) will increase proportionately with changes in sales volumes

18) Which of the following is a cost driver for a company’s human resource costs?

A) the number of employees in the company

B) the number of job applications processed

C) the number of units sold

D) the square footage of the office space used by the human resource department

Answer the following questions using the information below:

Zephyr Apparels is a clothing retailer. Unit costs associated with one of its products, Product DCT121, are

as follows:

Direct materials $ 70

Direct manufacturing labor 20

Variable manufacturing overhead 15

Fixed manufacturing overhead 32

Sales commissions (2% of sales) 5

Administrative salaries 16

Total $158

19) What are the direct variable manufacturing costs per unit associated with Product DCT121?

A) $142

B) $90

C) $105

D) $110

20) What are the indirect nonmanufacturing variable costs per unit associated with Product DCT121?

A) $5

B) $21

C) $90

D) $142

Answer the following questions using the information below:

The East Company manufactures several different products. Unit costs associated with Product ORD210

are as follows:

Direct materials $54

Direct manufacturing labor 8

Variable manufacturing overhead 11

Fixed manufacturing overhead 25

Sales commissions (2% of sales) 5

Administrative salaries 12

Total $115

21) What is the percentage of the total variable costs per unit associated with Product ORD105 with

respect to total cost?

A) 72%

B) 68%

C) 75%

D) 70%

22) What is the percentage of the total fixed costs per unit associated with Product ORD105 with respect

to total cost?

A) 32%

B) 28%

C) 26%

D) 20%

23) A fixed cost is fixed only in relation to a given wide range of total activity or volume and only for a

given

time span, usually a particular budget period.

24) A cost driver is a variable, such as the level of activity or volume that causally affects costs over a

given time span.

25) Fixed cost per unit reduces with an increase in production volume.

26) Variable costs per unit vary with the level of production or sales volume.

27) Wood used to manufacture chairs is considered a direct variable cost.

28) Variable costs depend on the resources used.

29) A fixed cost remains unchanged in total for a given time period, despite wide changes in the related

level

of total activity or volume of output produced.

30) An appropriate cost driver for shipping costs might be the number of units shipped.

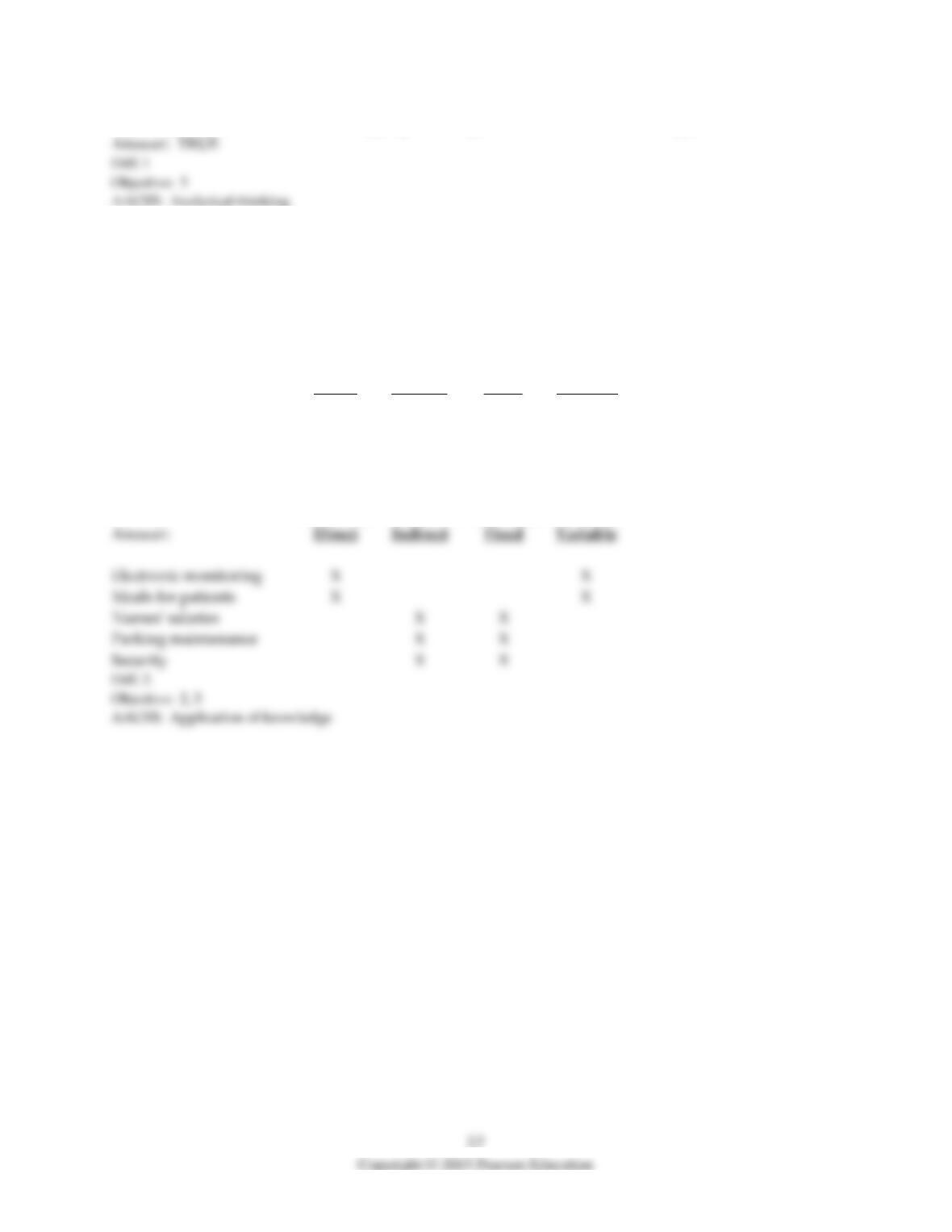

31) Butler Hospital wants to estimate the cost for each patient stay. It is a general health care facility

offering only basic services and not specialized services such as organ transplants.

Required:

a. Classify each of the following costs as either direct or indirect with respect to each patient.

b. Classify each of the following costs as either fixed or variable with respect to hospital costs per day.

Direct Indirect Fixed Variable

Electronic monitoring ________ ________ ________ ________

Meals for patients ________ ________ ________ ________

Nurses’ salaries ________ ________ ________ ________

Parking maintenance ________ ________ ________ ________

Security ________ ________ ________ ________

32) The list of representative cost drivers in the right column below are randomized with respect to the

list of functions in the left column. That is, they do not match.

Function

Representative Cost Driver

1.

Purchasing

A.

Number of employees

2.

Billing

B.

Number of shipments

3.

Shipping

C.

Number of customers

4.

Computer Support

D.

Number of invoices

5.

Personnel

E.

Number of desktop computers

6.

Customer Service

F.

Number of purchase orders

Required:

Match each business function with its representative cost driver.

Function

Insert letter of appropriate driver (A through F)

1.

Purchasing

2.

Billing

3.

Shipping

4.

Computer Support

5.

Personnel

6.

Customer Service

Function

Insert letter of appropriate driver (A through F)

1.

Purchasing

2.

Billing

3.

Shipping

4.

Computer Support

5.

Personnel

6.

Customer Service

33) Describe a variable cost. Describe a fixed cost. Explain why the distinction between variable and fixed

costs is important in cost accounting.

Objective 2.4

1) A unit cost is computed by ________.

A) multiplying total cost by the number of units produced

B) dividing total cost by the number of units produced

C) dividing variable cost by the number of units produced

D) dividing fixed cost by the number of units produced

2) In making product mix and pricing decisions, managers should focus on ________.

A) total costs

B) unit costs

C) variable costs

D) manufacturing costs

3) When 20,000 units are produced, fixed costs are $16 per unit. Therefore, when 16,000 units are

produced, fixed costs will ________.

A) increase to $20 per unit

B) remain at $16 per unit

C) decrease to $10 per unit

D) total $160,000

4) When 20,000 units are produced, variable costs are $8 per unit. Therefore, when 10,000 units are

produced ________.

A) variable costs will remain at $8 per unit

B) variable costs will total $60,000

C) variable unit costs will increase to $12 per unit

D) variable unit costs will decrease to $3 per unit

5) Eigen Manufacturing Corp. provided the following information for last month:

Sales $40,000

Variable costs 14,000

Fixed costs 10,000

Operating income $16,000

If sales reduce to half of the amount in the next month, what is the projected operating income?

A) $15,000

B) $6,000

C) $16,000

D) $3,000

6) Genosis Metals provided the following information for last month:

Sales $20,000

Variable costs 8,000

Fixed costs 4,000

Operating income $8,000

If sales reduce to half the amount in the next month, what is the projected operating income?

A) $0

B) $4,000

C) $2,000

D) $6,000