26. Which of the following statements is true regarding a statutory

consolidation?

27. In a transaction accounted for using the acquisition method where

consideration transferred exceeds book value of the acquired company, which

statement is true for the acquiring company with regard to its investment?

28. In a transaction accounted for using the acquisition method where

consideration transferred is less than fair value of net assets acquired, which

statement is true?

29. Which of the following statements is true regarding the acquisition method

of accounting for a business combination?

30. Which of the following statements is true?

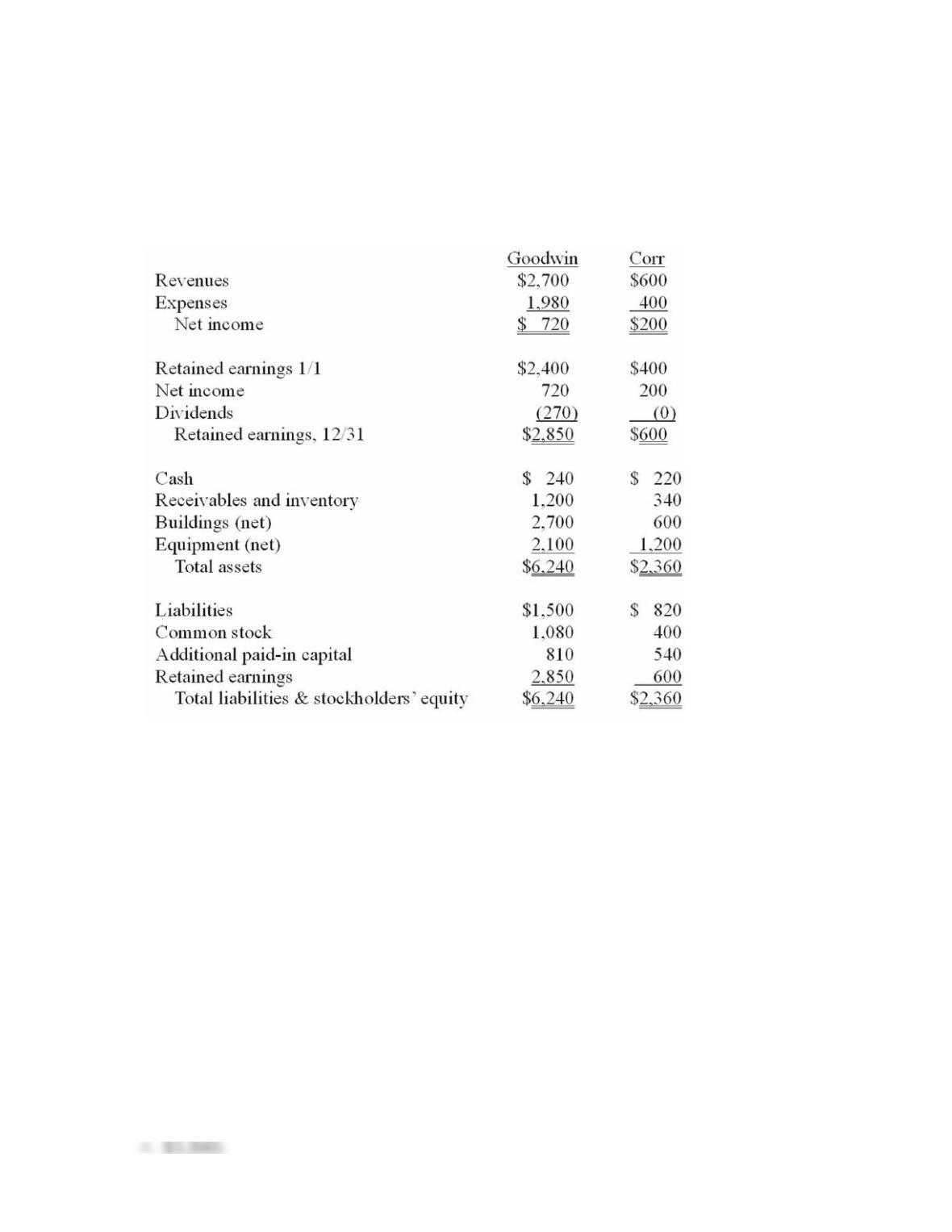

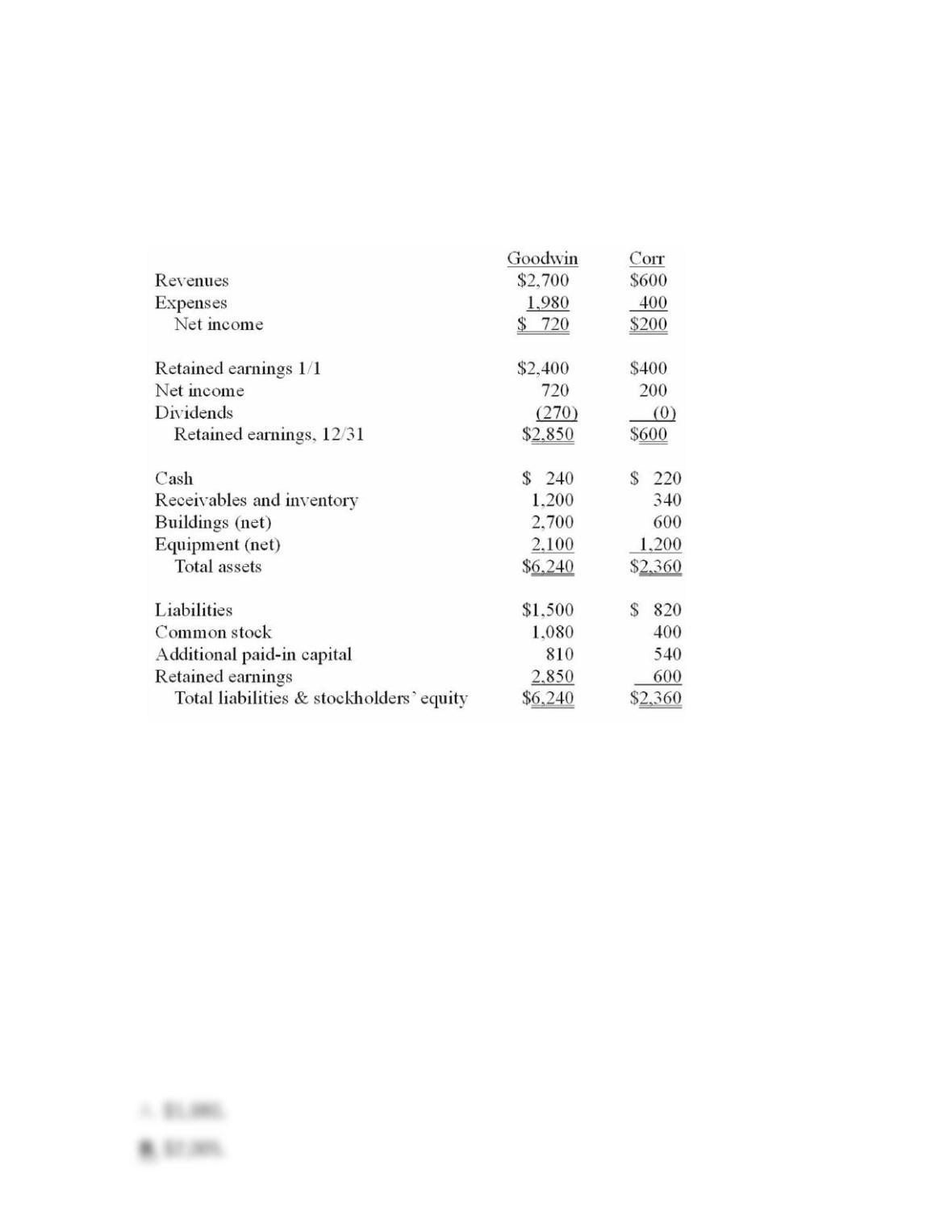

31. The financial statements for Goodwin, Inc., and Corr Company for the year

ended December 31, 20X1, prior to Goodwin’s acquisition business combination

transaction regarding Corr, follow (in thousands):

On December 31, 20X1, Goodwin issued $600 in debt and 30 shares of its $10

par value common stock to the owners of Corr to acquire all of the outstanding

shares of that company. Goodwin shares had a fair value of $40 per share.

Goodwin paid $25 to a broker for arranging the transaction. Goodwin paid $35 in

stock issuance costs. Corr’s equipment was actually worth $1,400 but its

buildings were only valued at $560.

In this acquisition business combination, at what amount is the investment

recorded on Goodwin’s books?

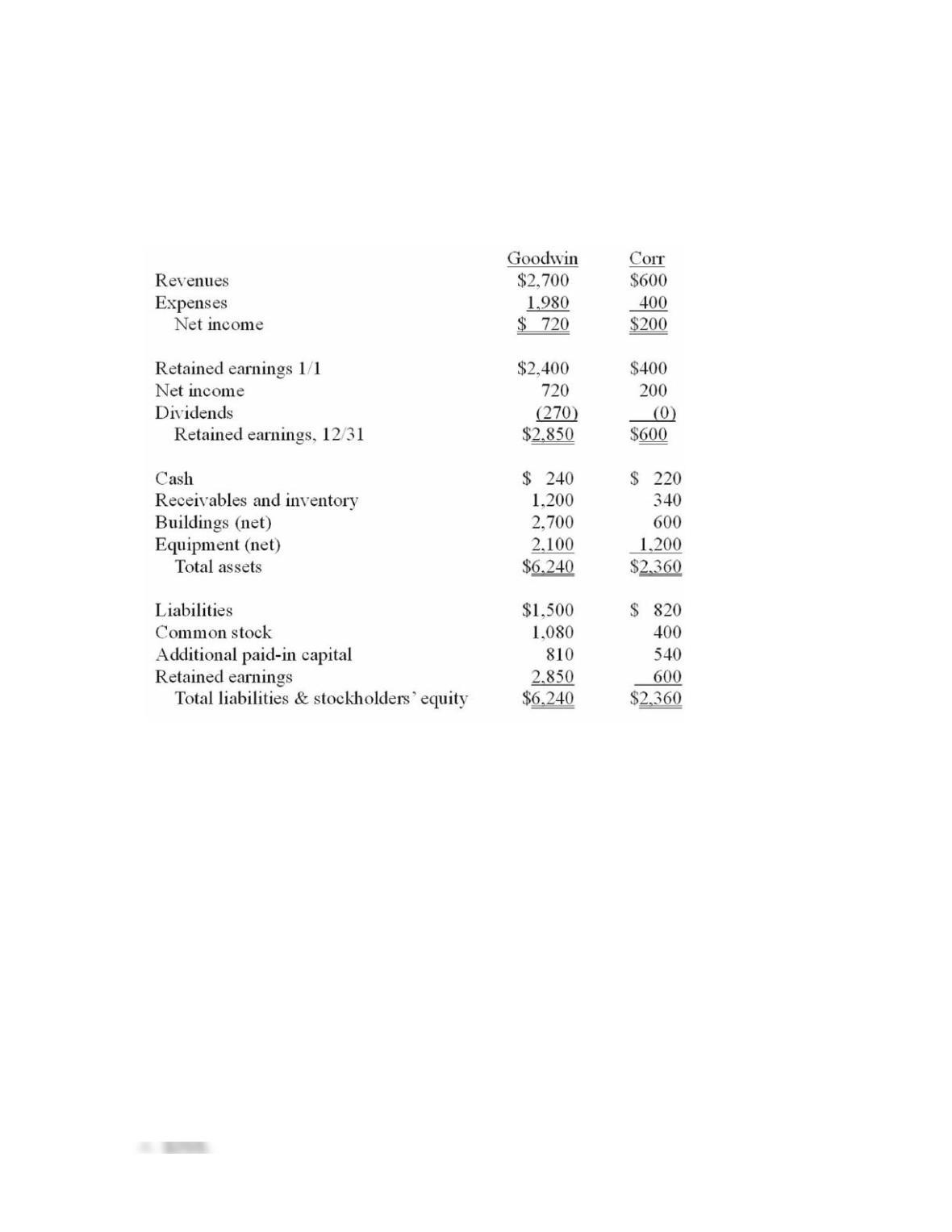

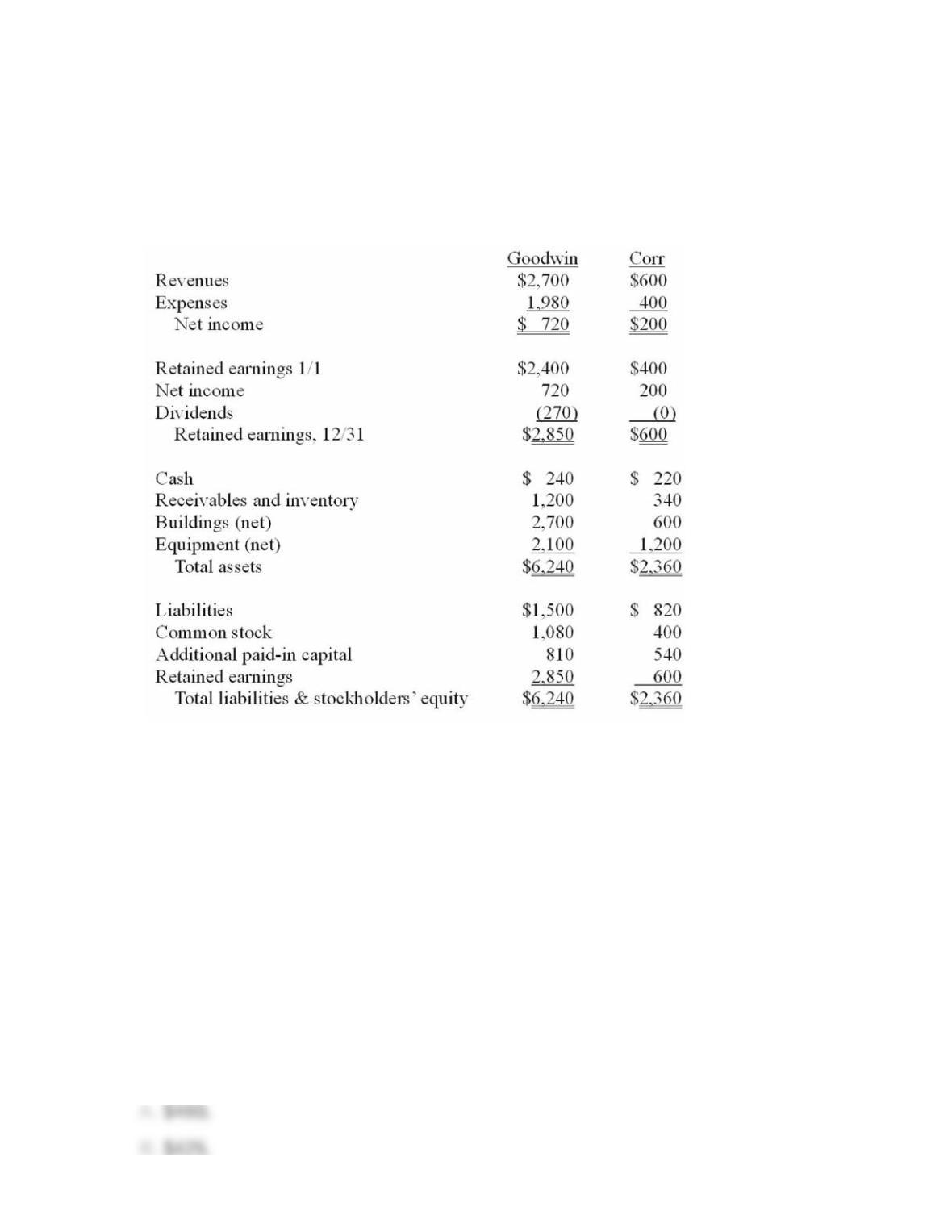

32. The financial statements for Goodwin, Inc., and Corr Company for the year

ended December 31, 20X1, prior to Goodwin’s acquisition business combination

transaction regarding Corr, follow (in thousands):

On December 31, 20X1, Goodwin issued $600 in debt and 30 shares of its $10

par value common stock to the owners of Corr to acquire all of the outstanding

shares of that company. Goodwin shares had a fair value of $40 per share.

Goodwin paid $25 to a broker for arranging the transaction. Goodwin paid $35 in

stock issuance costs. Corr’s equipment was actually worth $1,400 but its

buildings were only valued at $560.

In this acquisition business combination, what total amount of common stock

and additional paid-in capital is recorded on Goodwin’s books?

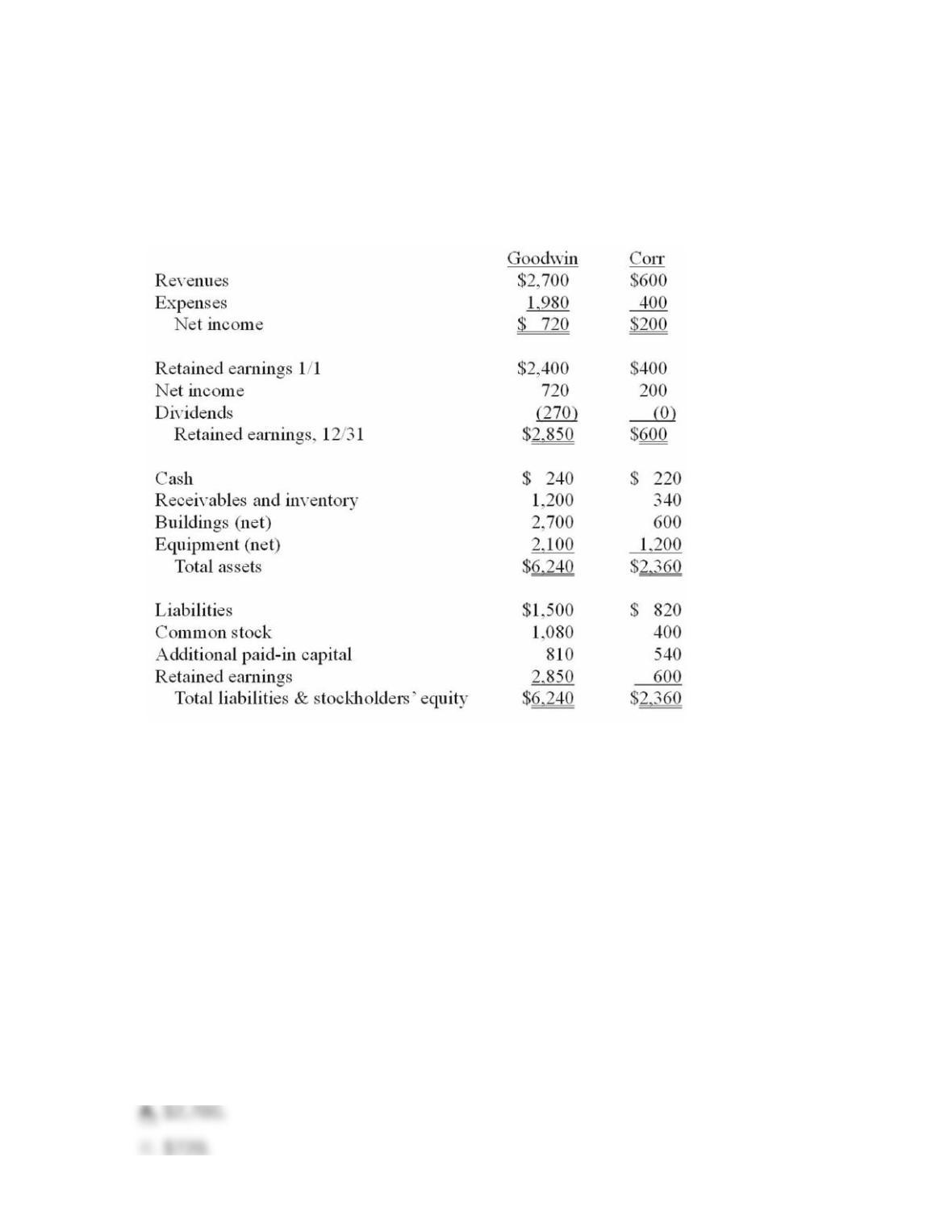

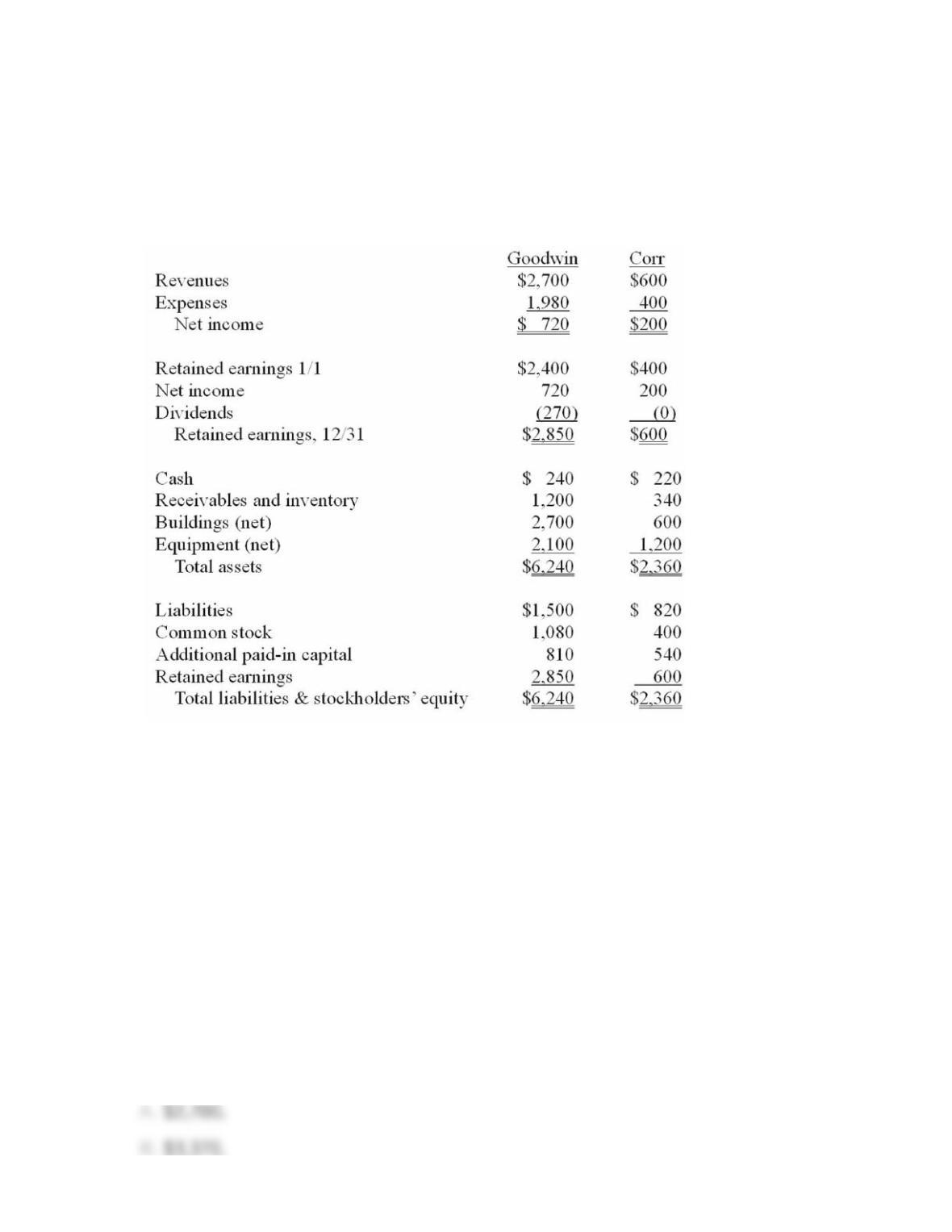

33. The financial statements for Goodwin, Inc., and Corr Company for the year

ended December 31, 20X1, prior to Goodwin’s acquisition business combination

transaction regarding Corr, follow (in thousands):

On December 31, 20X1, Goodwin issued $600 in debt and 30 shares of its $10

par value common stock to the owners of Corr to acquire all of the outstanding

shares of that company. Goodwin shares had a fair value of $40 per share.

Goodwin paid $25 to a broker for arranging the transaction. Goodwin paid $35 in

stock issuance costs. Corr’s equipment was actually worth $1,400 but its

buildings were only valued at $560.

Compute the consolidated revenues for 20X1.

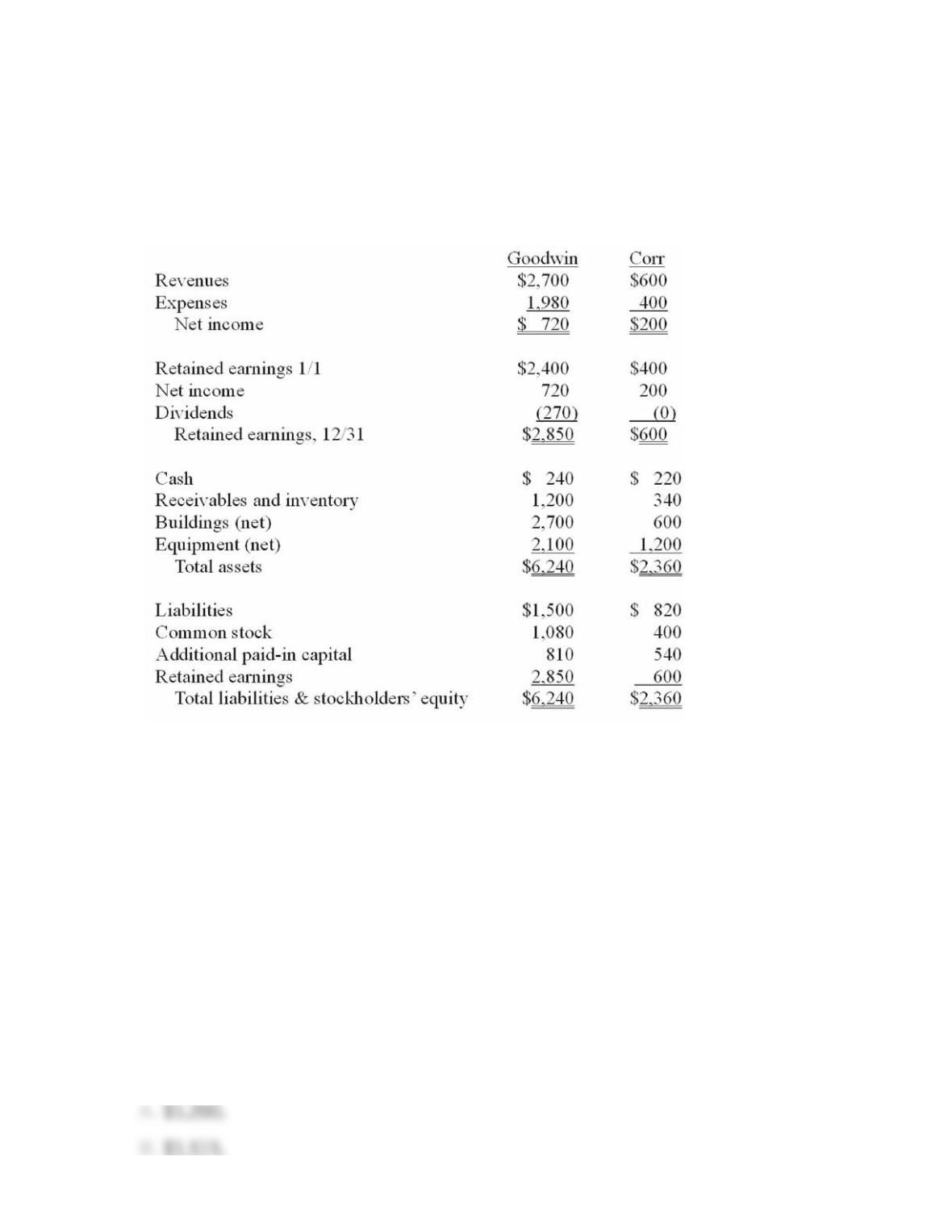

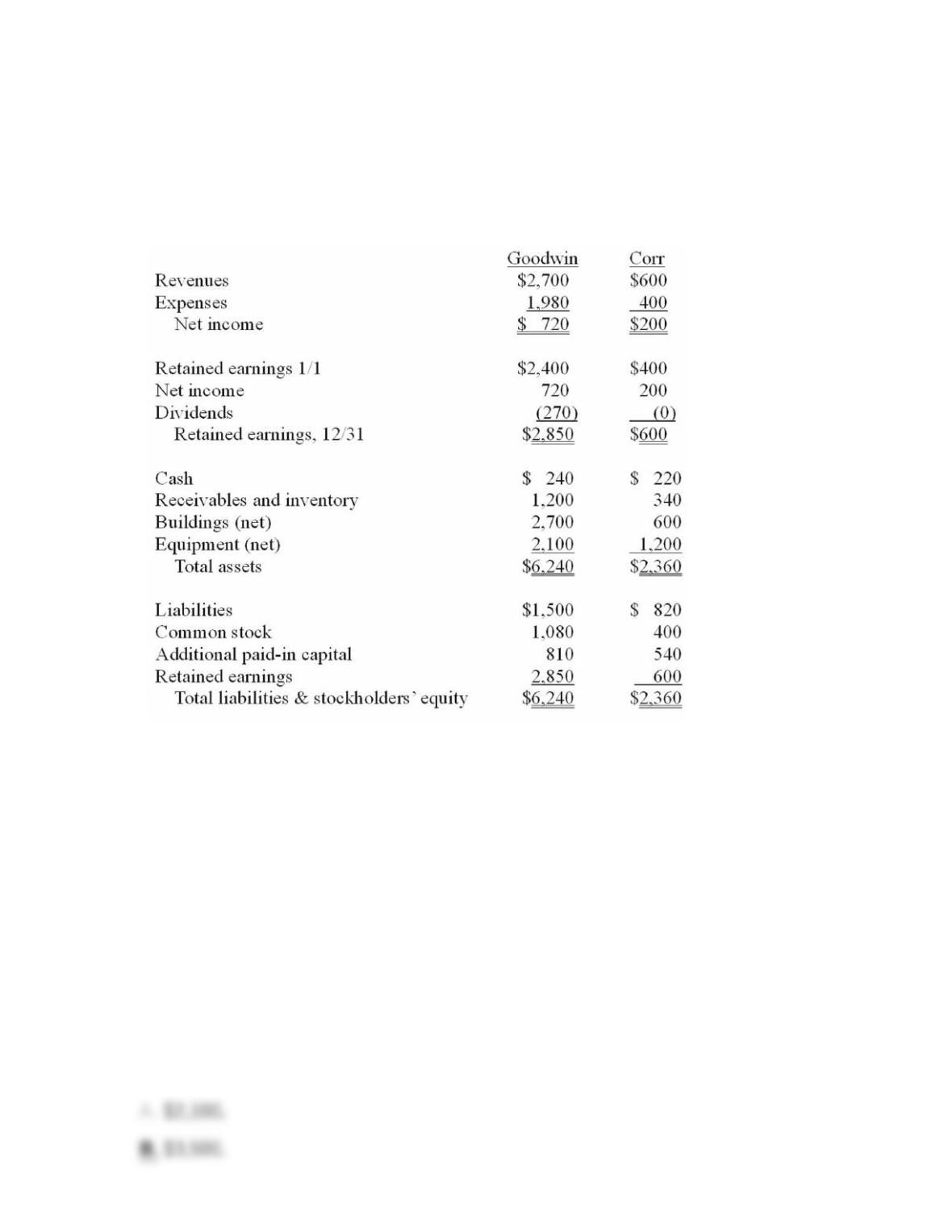

34. The financial statements for Goodwin, Inc., and Corr Company for the year

ended December 31, 20X1, prior to Goodwin’s acquisition business combination

transaction regarding Corr, follow (in thousands):

On December 31, 20X1, Goodwin issued $600 in debt and 30 shares of its $10

par value common stock to the owners of Corr to acquire all of the outstanding

shares of that company. Goodwin shares had a fair value of $40 per share.

Goodwin paid $25 to a broker for arranging the transaction. Goodwin paid $35 in

stock issuance costs. Corr’s equipment was actually worth $1,400 but its

buildings were only valued at $560.

Compute the consolidated receivables and inventory for 20X1.

35. The financial statements for Goodwin, Inc., and Corr Company for the year

ended December 31, 20X1, prior to Goodwin’s acquisition business combination

transaction regarding Corr, follow (in thousands):

On December 31, 20X1, Goodwin issued $600 in debt and 30 shares of its $10

par value common stock to the owners of Corr to acquire all of the outstanding

shares of that company. Goodwin shares had a fair value of $40 per share.

Goodwin paid $25 to a broker for arranging the transaction. Goodwin paid $35 in

stock issuance costs. Corr’s equipment was actually worth $1,400 but its

buildings were only valued at $560.

Compute the consolidated expenses for 20X1.

36. The financial statements for Goodwin, Inc., and Corr Company for the year

ended December 31, 20X1, prior to Goodwin’s acquisition business combination

transaction regarding Corr, follow (in thousands):

On December 31, 20X1, Goodwin issued $600 in debt and 30 shares of its $10

par value common stock to the owners of Corr to acquire all of the outstanding

shares of that company. Goodwin shares had a fair value of $40 per share.

Goodwin paid $25 to a broker for arranging the transaction. Goodwin paid $35 in

stock issuance costs. Corr’s equipment was actually worth $1,400 but its

buildings were only valued at $560.

Compute the consolidated cash account at December 31, 20X1.

37. The financial statements for Goodwin, Inc., and Corr Company for the year

ended December 31, 20X1, prior to Goodwin’s acquisition business combination

transaction regarding Corr, follow (in thousands):

On December 31, 20X1, Goodwin issued $600 in debt and 30 shares of its $10

par value common stock to the owners of Corr to acquire all of the outstanding

shares of that company. Goodwin shares had a fair value of $40 per share.

Goodwin paid $25 to a broker for arranging the transaction. Goodwin paid $35 in

stock issuance costs. Corr’s equipment was actually worth $1,400 but its

buildings were only valued at $560.

Compute the consolidated buildings (net) account at December 31, 20X1.

38. The financial statements for Goodwin, Inc., and Corr Company for the year

ended December 31, 20X1, prior to Goodwin’s acquisition business combination

transaction regarding Corr, follow (in thousands):

On December 31, 20X1, Goodwin issued $600 in debt and 30 shares of its $10

par value common stock to the owners of Corr to acquire all of the outstanding

shares of that company. Goodwin shares had a fair value of $40 per share.

Goodwin paid $25 to a broker for arranging the transaction. Goodwin paid $35 in

stock issuance costs. Corr’s equipment was actually worth $1,400 but its

buildings were only valued at $560.

Compute the consolidated equipment (net) account at December 31, 20X1.