196)

Nutley Company uses a job order cost system and last period incurred $70,000 of overhead and

$100,000 of direct labor. Nutley estimates that its overhead next period will be $65,000. The

company also expects to incur $100,000 of direct labor. If Nutley bases its overhead applied on

direct labor cost, what should be the overhead rate for the next period?

197)

A company’s job order costing system applies overhead based on direct labor cost. The company’s

estimated production costs for were: direct labor, $57,600; direct materials, $76,800; and factory

overhead, $9,600. Calculate the company’s overhead rate.

198)

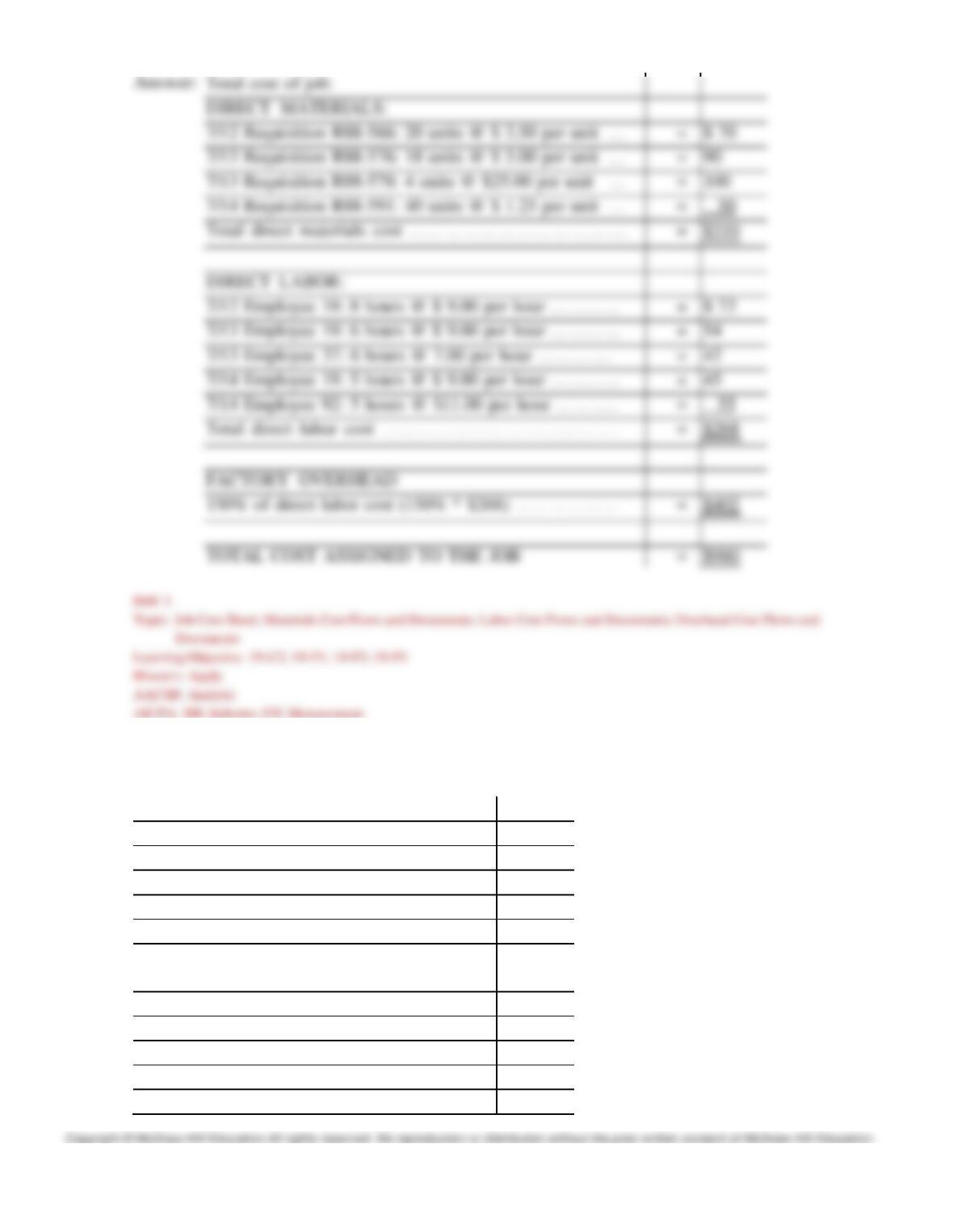

The job cost sheet for Job number 83-421 includes the following information:

DIRECT MATERIALS:

7/12 Requisition R88-566: 20 units @ $ 3.50 per unit

7/13 Requisition R88-576: 18 units @ $ 5.00 per unit

7/13 Requisition R88-578: 4 units @ $25.00 per unit

7/14 Requisition R88-591: 40 units @ $ 1.25 per unit

DIRECT LABOR:

7/12 Employee 19: 8 hours @ $ 9.00 per hour

7/13 Employee 19: 6 hours @ $ 9.00 per hour

7/13 Employee 37: 6 hours @ $ 7.00 per hour

7/14 Employee 19: 5 hours @ $ 9.00 per hour

7/14 Employee 92: 5 hours @ $11.00 per hour

FACTORY OVERHEAD: Assigned at 150% of direct labor cost.

What is the total cost of Job number 83-421?

135

DIRECT MATERIALS:

7/12 Requisition R88-566: 20 units @ $ 3.50 per unit …

$ 70

7/13 Requisition R88-576: 18 units @ $ 5.00 per unit …

7/13 Requisition R88-578: 4 units @ $25.00 per unit …

7/14 Requisition R88-591: 40 units @ $ 1.25 per unit …

50

7/12 Employee 19: 8 hours @ $ 9.00 per hour …………

$ 72

7/13 Employee 19: 6 hours @ $ 9.00 per hour …………

7/14 Employee 19: 5 hours @ $ 9.00 per hour …………

7/14 Employee 92: 5 hours @ $11.00 per hour ………..

55

FACTORY OVERHEAD

199)

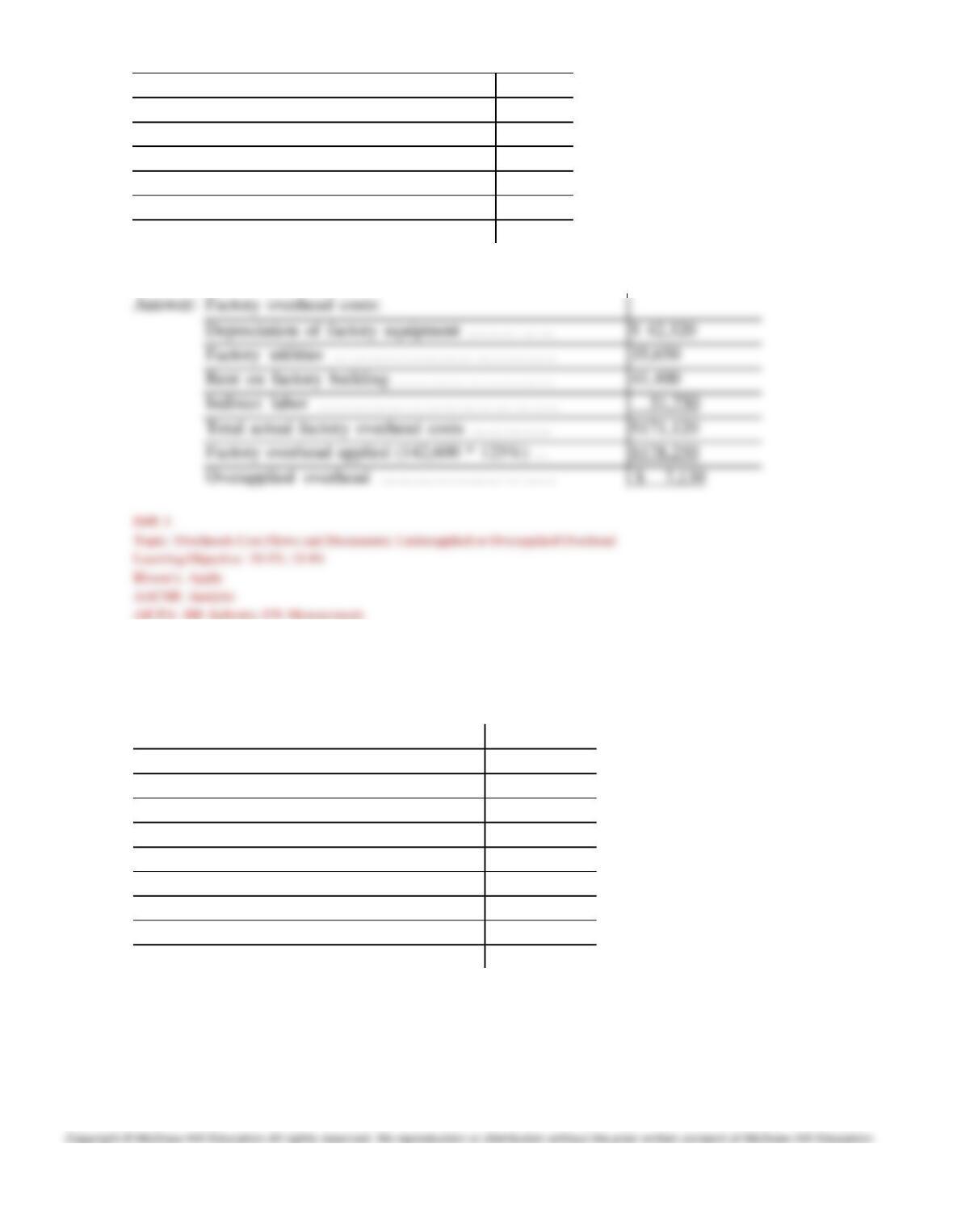

The following calendar year information about the Tchulahota Corporation is available on December

31:

Advertising expense……………………………

$ 28,800

Depreciation of factory equipment……………

42,320

Depreciation of office equipment……………..

10,800

Direct labor……………………………………

142,600

Factory utilities…………………………………

35,650

Interest expense…………………………………

6,650

Inventories, January 1:

Raw materials……………………………

3,450

Work in Process…………………………

17,250

Finished goods……………………………

35,600

Inventories, December 31:

Raw materials……………………………

136

..

2,300

137

Raw materials……………………………..

2,300

Work in Process…………………………..

20,700

Finished goods……………………………

31,050

Raw materials purchases………………………

132,450

Rent on factory building………………………

41,400

Indirect labor…………………………………..

51,750

Sales commissions……………………………..

16,500

The company applies overhead on the basis of 125% of direct labor costs. Calculate the amount of

over- or underapplied overhead.

Factory overhead costs:

Depreciation of factory equipment ……………

$ 42,320

Factory utilities ………………………………..

35,650

Rent on factory building ………………………

41,400

Indirect labor …………………………………..

51,750

Total actual factory overhead costs …………..

$171,120

Factory overhead applied (142,600 * 125%) …

$178,250

200)

The predetermined overhead rate for Foster, Inc., is based on estimated direct labor costs of $400,000

and estimated factory overhead of $500,000. Actual costs incurred were:

Direct materials……………………………..

$240,000

Direct labor…………………………………..

410,000

Indirect materials……………………………

55,000

Indirect labor………………………………..

125,000

Sales commissions………………………….

55,000

Factory depreciation…………………………

170,000

Property taxes, factory………………………

15,000

Factory utilities……………………………..

35,000

Advertising…………………………………..

62,500

Factory equipment rental……………………

110,000

(a) Calculate the predetermined overhead rate and calculate the overhead applied during the year.

(b) Determine the amount of over- or underapplied overhead and prepare the journal entry to

eliminate the over- or underapplied overhead assuming that it is not material in amount.

201)

A company charged the following amounts of overhead to jobs during the current year: $12,000 to

jobs still in process, $42,000 to jobs completed but not sold, and $66,000 to jobs finished and sold.

At year-end, the company‘s Factory Overhead account has a credit balance of $9,000, which is not

a material amount. What entry (if any) should the company make at year-end related to this

overhead balance?

139

Applied overhead (60% * $275,000)* ……………

165,000

Cost of Goods Sold ………………………………

$24,000

202)

Oddley Corp. uses a job order costing system. The following is selected information pertaining to

costs applied to jobs during the year:

Jobs still in process at the end of the year:

$167,000, which includes $65,000 direct labor costs.

Jobs finished and sold during the year:

$395,000, which includes $172,000 direct labor costs.

Jobs finished but unsold during the year:

$103,000, which includes $38,000 direct labor costs.

Oddley Corp.’s predetermined overhead rate is 60% of direct labor cost. At the end of the year, the

company’s records show that $189,000 of factory overhead has been incurred.

(a) Determine the amount of overapplied or underapplied overhead.

(b) Prepare the necessary journal entry to close the Factory Overhead account assuming that any

remaining balance is not material.

203)

Taylor Corp. uses a job order costing system and worked only on Job 101 during the current period.

Job 101 was sold for $460,000. The following information pertains to costs incurred for Job 101.

Direct Materials

$90,000

Indirect Materials

$30,000

Direct Labor

$130,000

Indirect Labor

$75,000

Depreciation of Machinery

$10,000

Factory Supplies

$8,000

Overhead Application Rate

90% of direct labor

After adjusting for the amount of over or underapplied overhead, determine the amount of gross

profit earned on Job 101.

140

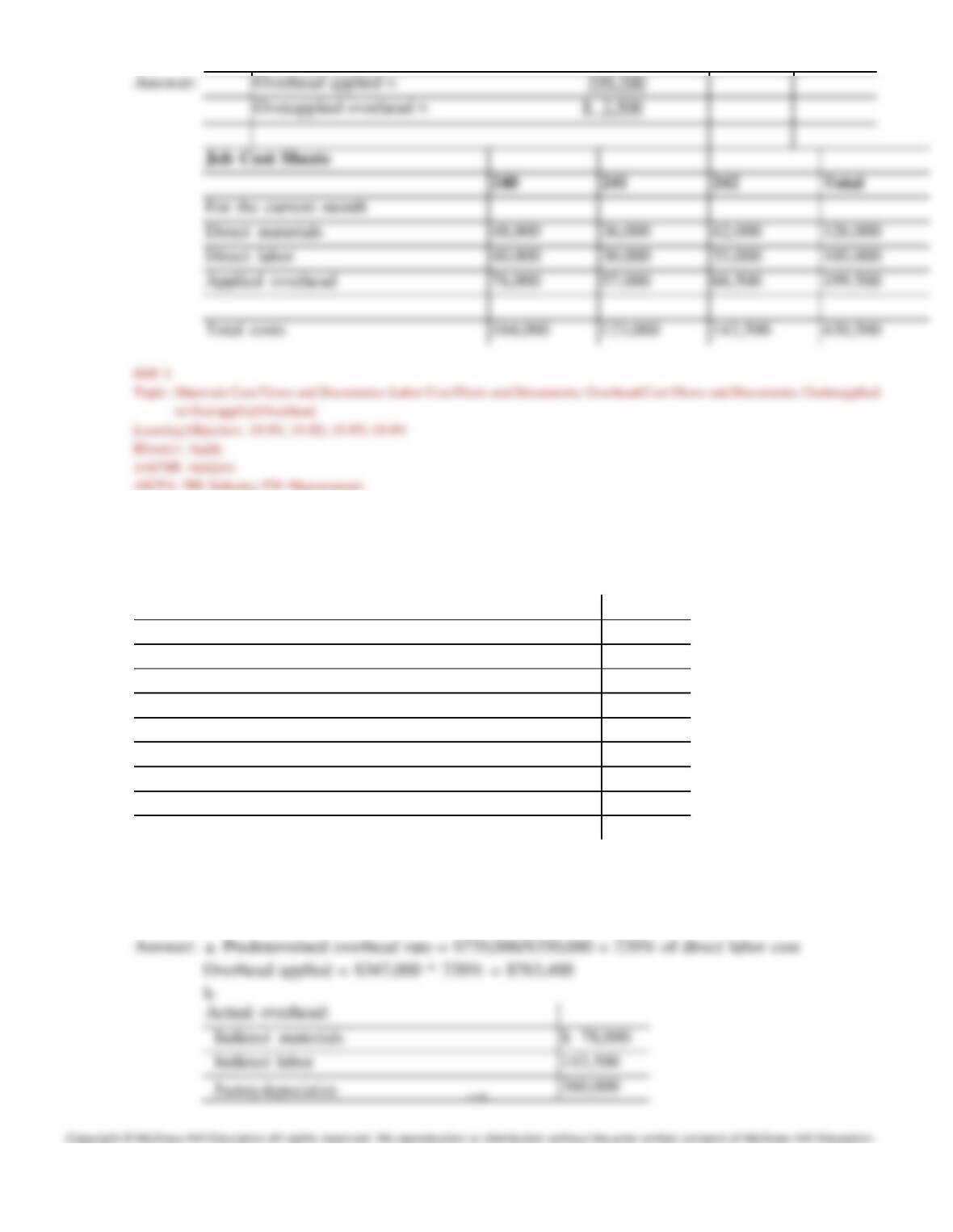

204)

At the end of June, the job cost sheets for Kennedy Manufacturing show the following total costs

accumulated on three custom jobs.

Job 203

Job 204

Job 205

Direct materials

$32,000

$47,000

$43,000

Direct labor

18,000

22,000

25,000

Overhead

26,100

31,900

36,250

Job 203 was started in production in May and the following costs were assigned to it in May: direct

materials, $12,000; direct labor, $6,000; and overhead $8,700. Jobs 204 and 205 are started in June.

Overhead cost is applied with a predetermined rate based on direct labor cost. Jobs 203 and 204 are

finished in June, and Job 205 will be finished in July. No raw materials are used indirectly in June.

Using this information, answer the following questions assuming the company’s predetermined

overhead rate did not change.

a. What is the cost of the raw materials requisitioned in June for each of the three jobs?

b. How much direct labor cost is incurred during June for each of the three jobs?

c. What predetermined overhead rate is used during June?

d. How much total cost is transferred to finished goods during June?

205)

Booth Manufacturing uses a job order costing system that charges overhead to jobs on the basis of

direct material cost. At year-end, the Work in Process Inventory account shows the following.

Date

Explanation

Debit

Credit

Balance

Dec. 31

Direct materials cost

980,000

980,000

31

Direct labor cost

320,000

1,300,000

31

Overhead costs

637,000

1,937,000

31

To finished goods

1,818,000

119,000

a. Determine the overhead rate used (based on direct material cost).

b. Only one job remained in the Work in Process inventory at December 31. Its direct materials cost

is $60,000. How much direct labor cost and overhead cost are assigned to it?

Total cost of job in process

$119,000

Less materials costs of job in process

60,000

$59,000

Less overhead applied ($60,000 * .65)

39,000

206)

Franklin Manufacturing uses a job order costing system that charges overhead to jobs on the basis

of direct labor cost. Franklin used the following cost predictions: overhead costs $1,285,750, and

direct labor costs of $695,000. At year-end, the company’s records show that actual overhead costs

for the year are $1,278,800, and actual direct labor costs are $692,000.

a. Determine the predetermined overhead rate for the year.

b. Compute the amount of overapplied or underapplied overhead.

c. Prepare the adjusting entry to allocate the over- or underapplied overhead assuming the amount is

immaterial.

207)

Drop Anchor takes special orders to manufacture sail boats for high end customers. Complete the job

cost sheets for Drop Anchor for September based on the following information. Prepare journal

entries to record the transactions as well as post to the job cost sheets.

a. Purchased raw materials on credit, $145,000.

b. Materials requisitions: Job 240, $48,000; Job 241, $36,000; Job 242, $42,000; indirect materials

were $12,000.

c. Time tickets used to charge labor to jobs: Job 240, $40,000; Job 241, $30,000; Job 242, $35,000,

indirect labor is $25,000.

d. The company incurred the following additional overhead costs: depreciation of factory building,

$70,000; depreciation of factory equipment, $60,000; expired factory insurance, $10,000; utilities

and maintenance cost of $20,000 were paid in cash.

e. Applied overhead to all three jobs. The predetermined overhead rate is 190% of direct labor cost.

f. Transferred jobs 240 and 242 to Finished Goods Inventory.

g. Sold job 240 for $300,000 for cash.

h. Closed the under- or over-applied overhead account balance.

Job Cost Sheets

240

241

242

Total

For the current month

Direct materials

Direct labor

Applied overhead

143

Applied overhead

Total costs

Accounts Payable

145,000

Raw Materials Inventory

126,000

Cost of Goods Sold

164,000

Factory Overhead

2,500

Cost of Goods Sold

2,500

Overhead applied = 199,500

For the current month

Direct materials

48,000

36,000

42,000

126,000

Direct labor

40,000

30,000

35,000

105,000

Applied overhead

76,000

57,000

66,500

199,500

208)

The predetermined overhead rate for Shilling Manufacturing is based on estimated direct labor costs

of $350,000 and estimated factory overhead of $770,000. Actual costs incurred were:

Direct materials

$475,000

Direct labor

347,000

Indirect materials

78,000

Indirect labor

143,500

Sales commissions

150,000

Factory depreciation

260,000

Property taxes, factory

35,000

Factory utilities

65,000

Advertising

62,500

Factory supervision

185,000

a. Calculate the predetermined overhead rate and calculate the overhead applied during the year.

b. Determine the amount of over- or underapplied overhead and prepare the journal entry to

eliminate the over- or underapplied overhead assuming that it is not material in amount.

143,500

SHORT ANSWER QUESTIONS

209)

A ________ accounting system records production activities using a perpetual inventory system.

210)

, or customized production, produces products in response to customer orders.

211)

A ________ is a separate record maintained for each job.

212)

The collection of job cost sheets for all jobs in process makes up the subsidiary ledger controlled

by the Inventory.

213)

In a job order costing system, raw materials requisitioned as direct materials are debited to

________; indirect materials are debited to ________.

214)

When factory payroll is assigned to specific jobs, ________ is debited.

215)

When factory payroll for indirect labor is assigned, ________ is debited.

216)

A is calculated by relating total estimated factory overhead to an allocation factor such

as total estimated direct labor cost, and is used to allocate factory overhead to specific jobs.

217)

When the actual overhead incurred during an accounting period is more than the overhead applied

to jobs, the overhead is said to be ________.

218)

Immaterial amounts of overapplied overhead should be ________ to the ________ account when

closed.