17–81

91.

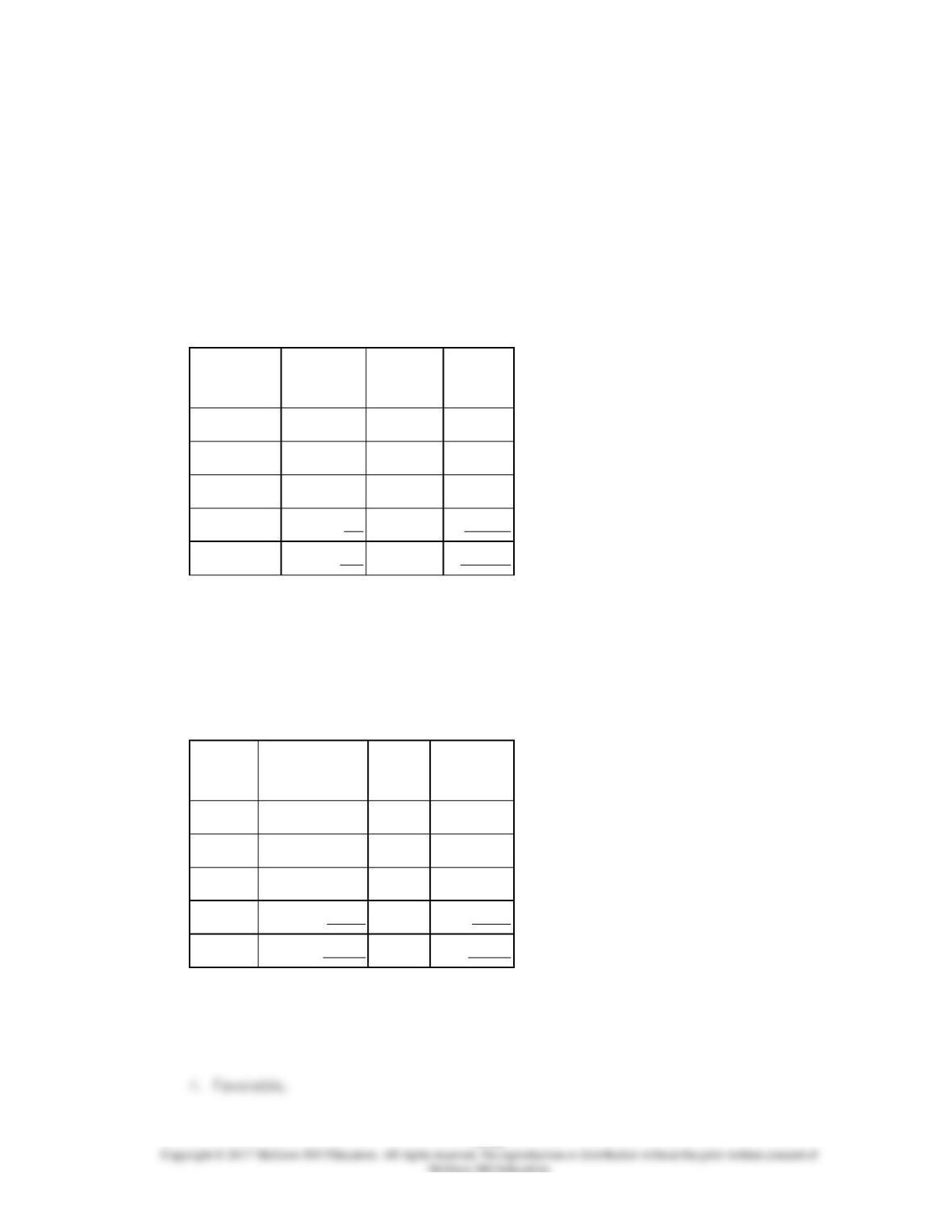

The Becton Enterprises (BE) produces a gasoline additive, Charger Power. This product

increases engine efficiency and improves gasoline mileage by creating a more complete

burn in the combustion process. Careful controls are required during the production

process to insure that the proper mix of input chemicals is achieved and that evaporation

is controlled. Loss of output and efficiency may result if the controls are not effective.

The standard cost of producing a 500-liter batch of Charger Power is $135. The standard

materials mix and related standard cost of each chemical used in a 500-liter batch are:

Chemical

Std input

quantity

Std cost

per liter

Total

cost

Echol

200

$0.200

$40.00

Protex

100

0.425

42.50

Benz

250

0.150

37.50

CT–40

50

0.300

15.00

600

$135.00

The quantities of chemicals purchased and used during the current production period are

shown in the schedule below. A total of 140 batches of Charger Power were manufactured

during the current production period. The controller of BE has determined its costs and

chemical usage variations at the end of the production period.

Chemical

Quantity

Purchased

Total

Cost

Quantity

Used

Echol

25,000

$5,365

26,600

Protex

13,000

6,240

12,880

Benz

40,000

5,840

37,800

CT–40

7,500

2,220

7,140

85,500

84,420

17–83

92.

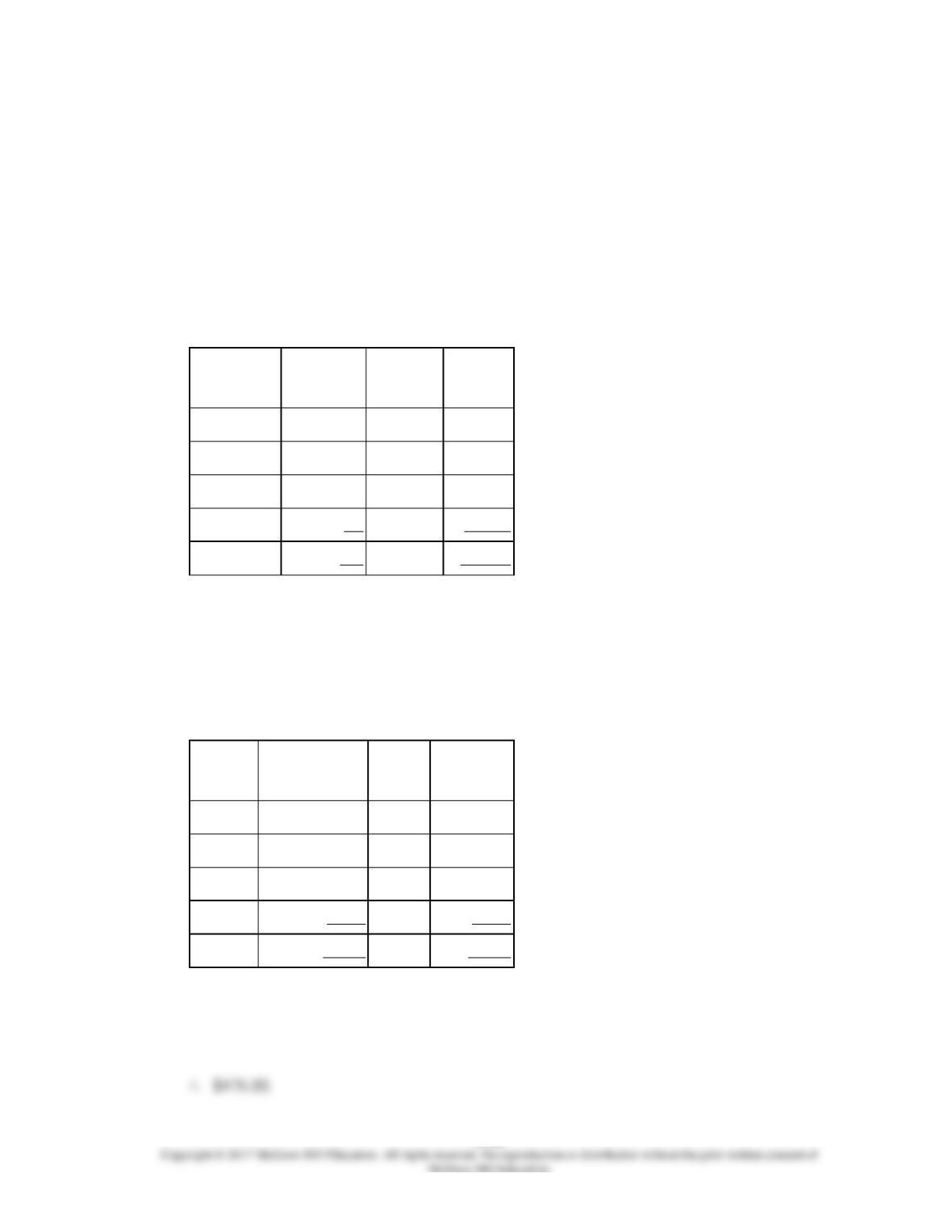

The Becton Enterprises (BE) produces a gasoline additive, Charger Power. This product

increases engine efficiency and improves gasoline mileage by creating a more complete

burn in the combustion process. Careful controls are required during the production

process to insure that the proper mix of input chemicals is achieved and that evaporation

is controlled. Loss of output and efficiency may result if the controls are not effective.

The standard cost of producing a 500-liter batch of Charger Power is $135. The standard

materials mix and related standard cost of each chemical used in a 500-liter batch are:

Chemical

Std input

quantity

Std cost

per liter

Total

cost

Echol

200

$0.200

$40.00

Protex

100

0.425

42.50

Benz

250

0.150

37.50

CT–40

50

0.300

15.00

600

$135.00

The quantities of chemicals purchased and used during the current production period are

shown in the schedule below. A total of 140 batches of Charger Power were manufactured

during the current production period. The controller of BE has determined its costs and

chemical usage variations at the end of the production period.

Chemical

Quantity

Purchased

Total

Cost

Quantity

Used

Echol

25,000

$5,365

26,600

Protex

13,000

6,240

12,880

Benz

40,000

5,840

37,800

CT–40

7,500

2,220

7,140

85,500

84,420

17–85

93.

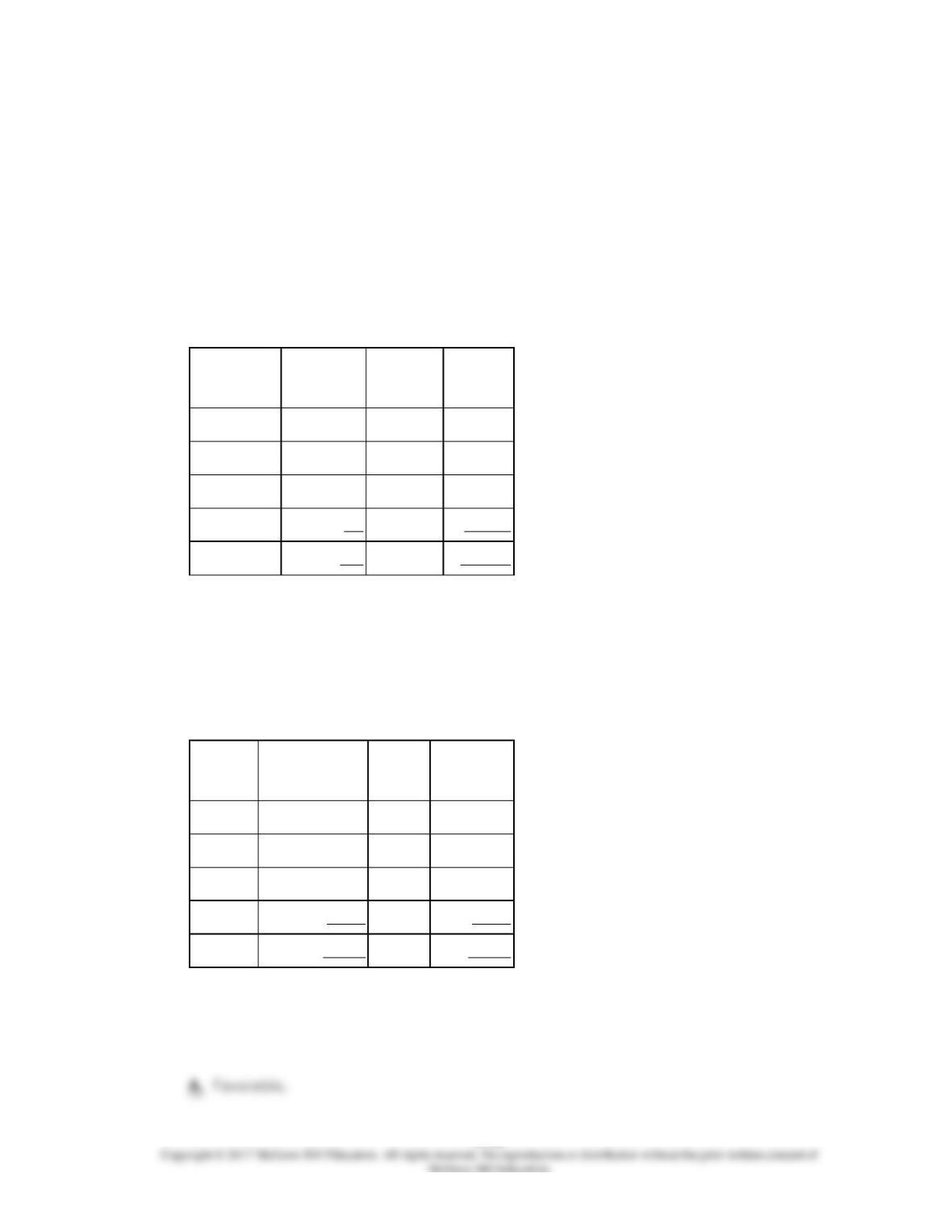

The Becton Enterprises (BE) produces a gasoline additive, Charger Power. This product

increases engine efficiency and improves gasoline mileage by creating a more complete

burn in the combustion process. Careful controls are required during the production

process to insure that the proper mix of input chemicals is achieved and that evaporation

is controlled. Loss of output and efficiency may result if the controls are not effective.

The standard cost of producing a 500-liter batch of Charger Power is $135. The standard

materials mix and related standard cost of each chemical used in a 500-liter batch are:

Chemical

Std input

quantity

Std cost

per liter

Total

cost

Echol

200

$0.200

$40.00

Protex

100

0.425

42.50

Benz

250

0.150

37.50

CT–40

50

0.300

15.00

600

$135.00

The quantities of chemicals purchased and used during the current production period are

shown in the schedule below. A total of 140 batches of Charger Power were manufactured

during the current production period. The controller of BE has determined its costs and

chemical usage variations at the end of the production period.

Chemical

Quantity

Purchased

Total

Cost

Quantity

Used

Echol

25,000

$5,365

26,600

Protex

13,000

6,240

12,880

Benz

40,000

5,840

37,800

CT–40

7,500

2,220

7,140

85,500

84,420

94.

A company makes a product using two materials, one of which is interchangeable with a

third material. The standards for producing one 200-pound batch are presented below.

The last 200-pound batch was produced using 140 pounds of M and 90 pounds of O. The

price of M was $0.03 per pound and the actual price of O was $0.10.

Material

Standard

Quantity

(lbs)

LBS

Standard

Cost/lb.

Total

Cost

O

0

$.10

$0

H

80

.08

6.40

M

120

.02

2.40

200

$8.80

95.

A company makes a product using two materials, one of which is interchangeable with a

third material. The standards for producing one 200-pound batch are presented below.

The last 200-pound batch was produced using 140 pounds of M and 90 pounds of O. The

price of M was $0.03 per pound and the actual price of O was $0.10.

Material

Standard

Quantity

(lbs)

LBS

Standard

Cost/lb.

Total

Cost

O

0

$.10

$0

H

80

.08

6.40

M

120

.02

2.40

200

$8.80

Is the materials mix variance favorable or unfavorable?

96.

A company makes a product using two materials, one of which is interchangeable with a

third material. The standards for producing one 200-pound batch are presented below.

The last 200-pound batch was produced using 140 pounds of M and 90 pounds of O. The

price of M was $0.03 per pound and the actual price of O was $0.10.

Material

Standard

Quantity

(lbs)

LBS

Standard

Cost/lb.

Total

Cost

O

0

$.10

$0

H

80

.08

6.40

M

120

.02

2.40

200

$8.80

97.

A company makes a product using two materials, one of which is interchangeable with a

third material. The standards for producing one 200-pound batch are presented below.

The last 200-pound batch was produced using 140 pounds of M and 90 pounds of O. The

price of M was $0.03 per pound and the actual price of O was $0.10.

Material

Standard

Quantity

(lbs)

LBS

Standard

Cost/lb.

Total

Cost

O

0

$.10

$0

H

80

.08

6.40

M

120

.02

2.40

200

$8.80

98.

Bonner Company’s direct labor cost for March was as follows:

Actual direct labor hours

30,000

Standard direct labor hours

31,500

Rate variance

$4,500

U

Total payroll

$189,000

Labor mix variance

$4,225

U

99.

Bonner Company’s direct labor cost for March was as follows:

Actual direct labor hours

30,000

Standard direct labor hours

31,500

Rate variance

$4,500

U

Total payroll

$189,000

Labor mix variance

$4,225

U

Is the direct labor yield variance favorable or unfavorable?

100.

Prince Inc. has the following information:

Total payroll

$165,300

Standard direct labor hours

45,000

Labor rate variance

$8,700

F

Labor mix variance

$4,000

F

Labor yield variance

$2,000

F

101.

Prince Inc. has the following information:

Total payroll

$165,300

Standard direct labor hours

45,000

Labor rate variance

$8,700

F

Labor mix variance

$4,000

F

Labor yield variance

$2,000

F

17–95

102.

The following data for April has been provided by Cowle Corporation.

Level of activity

8,800

machine-

hours

Budgeted fixed

manufacturing overhead

costs

$178,640

Actual level of activity

9,200

machine-

hours

Standard machine-hours

allowed for the actual

output

9,300

machine-

hours

Actual fixed manufacturing

overhead costs

$172,980

103.

The following data for April has been provided by Cowle Corporation.

Level of activity

8,800

machine-

hours

Budgeted fixed

$178,640

manufacturing overhead

costs

Actual level of activity

9,200

machine-

hours

Standard machine-hours

allowed for the actual

output

9,300

machine-

hours

Actual fixed manufacturing

overhead costs

$172,980

machine-

hours

104.

Yellon Company uses a standard cost system in which it applies manufacturing overhead

to units of product on the basis of standard direct labor-hours (DLHs). The following data

pertain to last month’s operations:

Budgeted fixed manufacturing

overhead costs

$5,000

Actual fixed manufacturing

overhead costs

$5,500

Standard hours allowed for output

2,400

DLHs

Predetermined overhead rate ($2

variable + $3 fixed)

$5

per

DLH

105.

106.

107.

Which of the following factors should not be considered when deciding whether to

investigate a variance?

17-100

108.

There are several reasons why actual results differ from standards. Which of the following

does not represent a reason why a variance might occur?

Essay Questions