109.

17-102

110.

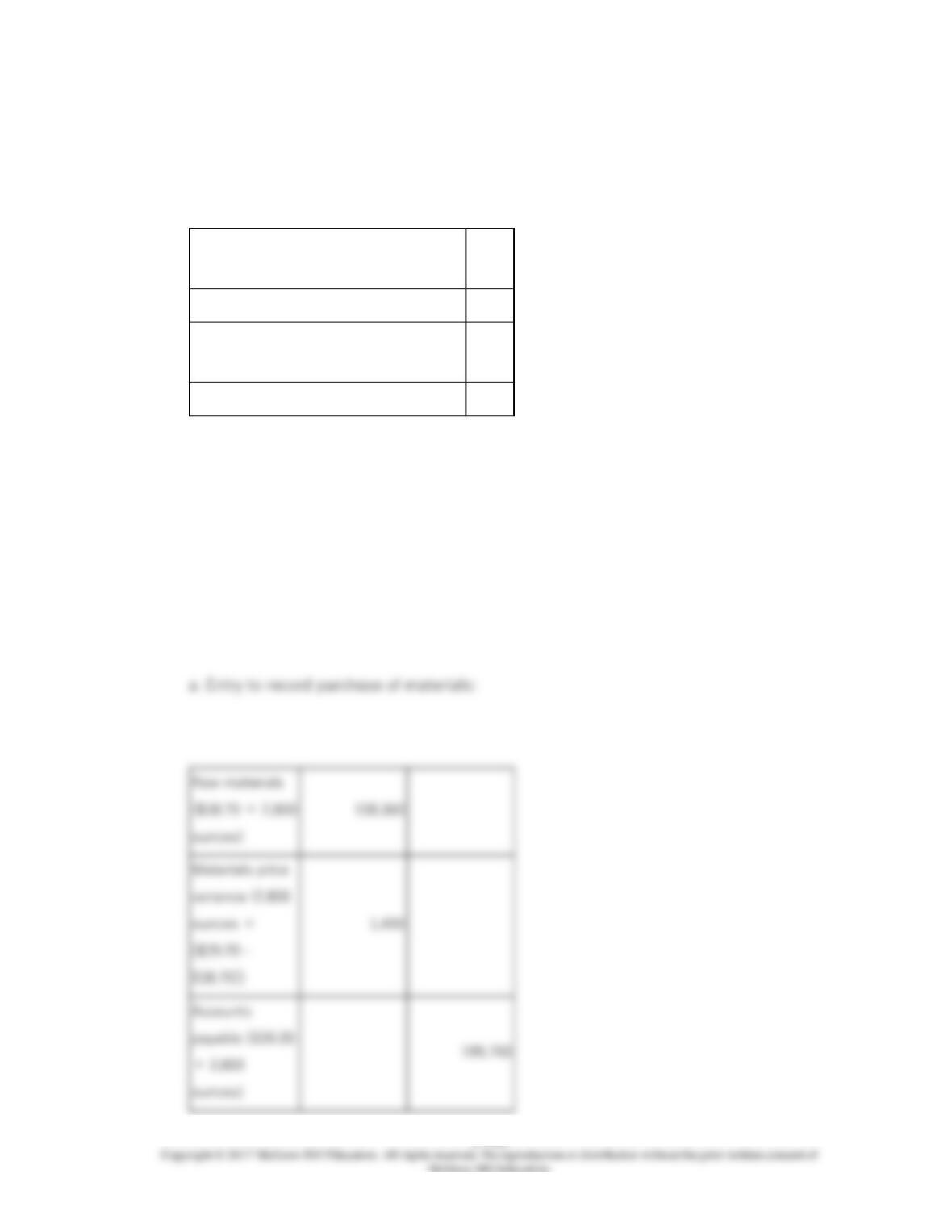

Malloy Corporation has provided the following data concerning its most important raw

material, compound I51D:

Standard cost, per liter

$30.50

Standard quantity, liters per unit of

output

4.6

Cost of material purchased in October,

per liter

$30.70

Material purchased in October, liters

4,000

Material used in production in October,

liters

3,580

Actual output in October, units

800

17-104

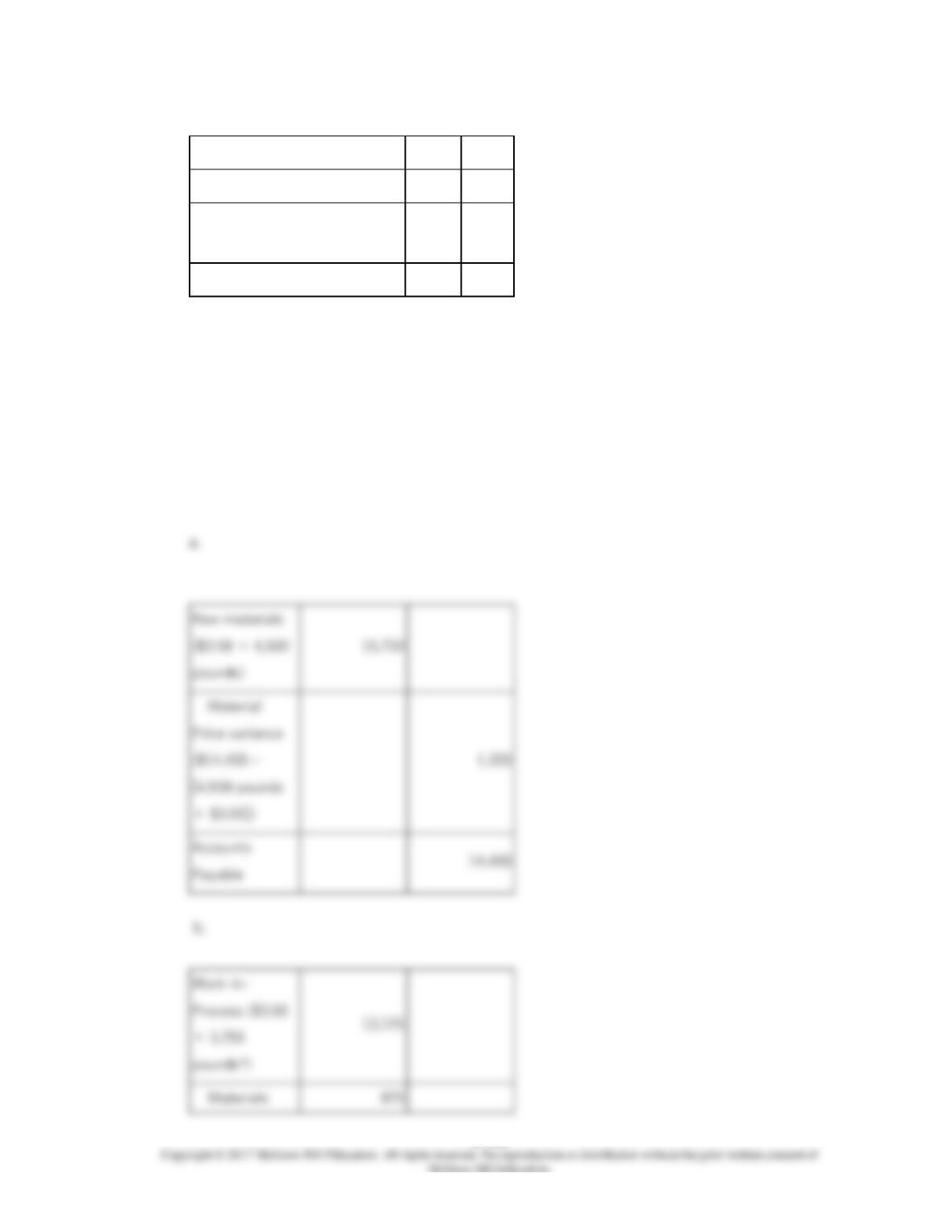

111.

The data below relate to a product of Omaha Company.

Standard costs:

Materials, 3 pounds at $7 per

pound

$21

per

unit

Labor, 4 hours at $18 per hour

$72

per

unit

Budgeted production for the

year

2,000

units

Actual results were:

Production

1,800

units

Material purchases, 6,000

pounds

$48,230

Labor, 7,420 hours

$140,170

Material used in production

5,750

pounds

17-106

112.

Compound Y23Z is used by Carrington Corporation to make one of its products. The

standard cost of compound Y23Z is $38.70 per ounce and the standard quantity is 4.6 per

unit of output. Data concerning the compound in the most recent month appear below:

Cost of material purchased in November,

per ounce

$39.20

Material purchased in November, ounces

2,800

Material used in production in November,

ounces

2,360

Actual output in November, units

500

17-108

113.

The following standards have been established for a raw material used to make product

P62:

Standard quantity of the

material per unit of output

6.3

pounds

Standard price of the material

$15.50

per

pound

The following data pertain to a recent month’s operations:

Actual material

purchased

6,700

pounds

Actual cost of material

purchased

$100,500

Actual material used in

production

6,400

pounds

Actual output

920

units of

product P62

17-109

114.

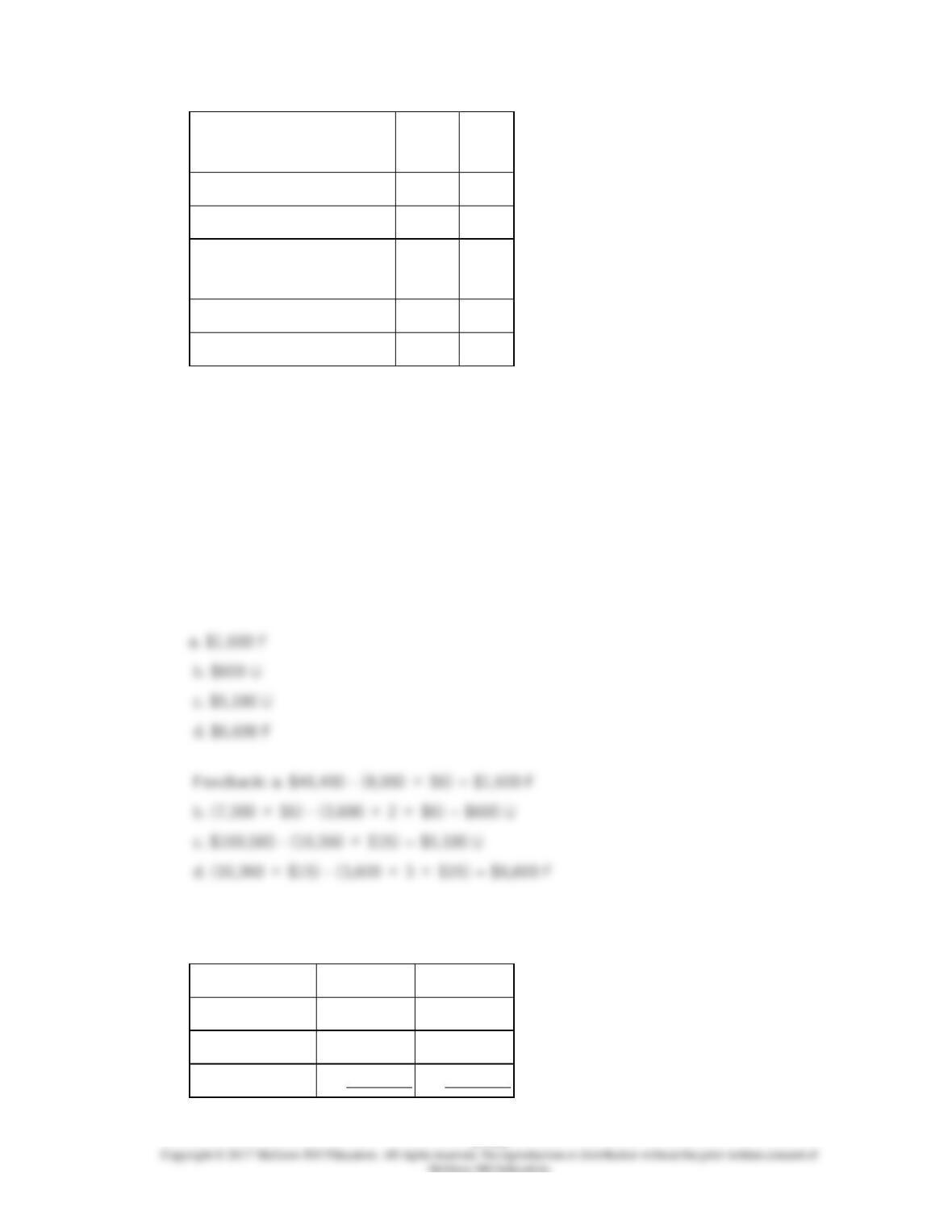

115.

The Oregon Company produces and sells a single product. Standards have been

established for the product as follows:

Direct materials: 5 pounds @ $3.50 per pound = $17.50

Direct labor: 3 hours @ $5.50 per hour = $16.50

Actual cost and usage figures for the past month follow:

17-110

Units produced

750

Direct materials used

4,000

pounds

Direct materials purchased

(4,500 pounds)

$14,400

Direct labor cost (2,000 hours)

$11,200

Payable

Materials

17-111

116.

The data below relate to a product of Bullfrog Company.

Standard costs:

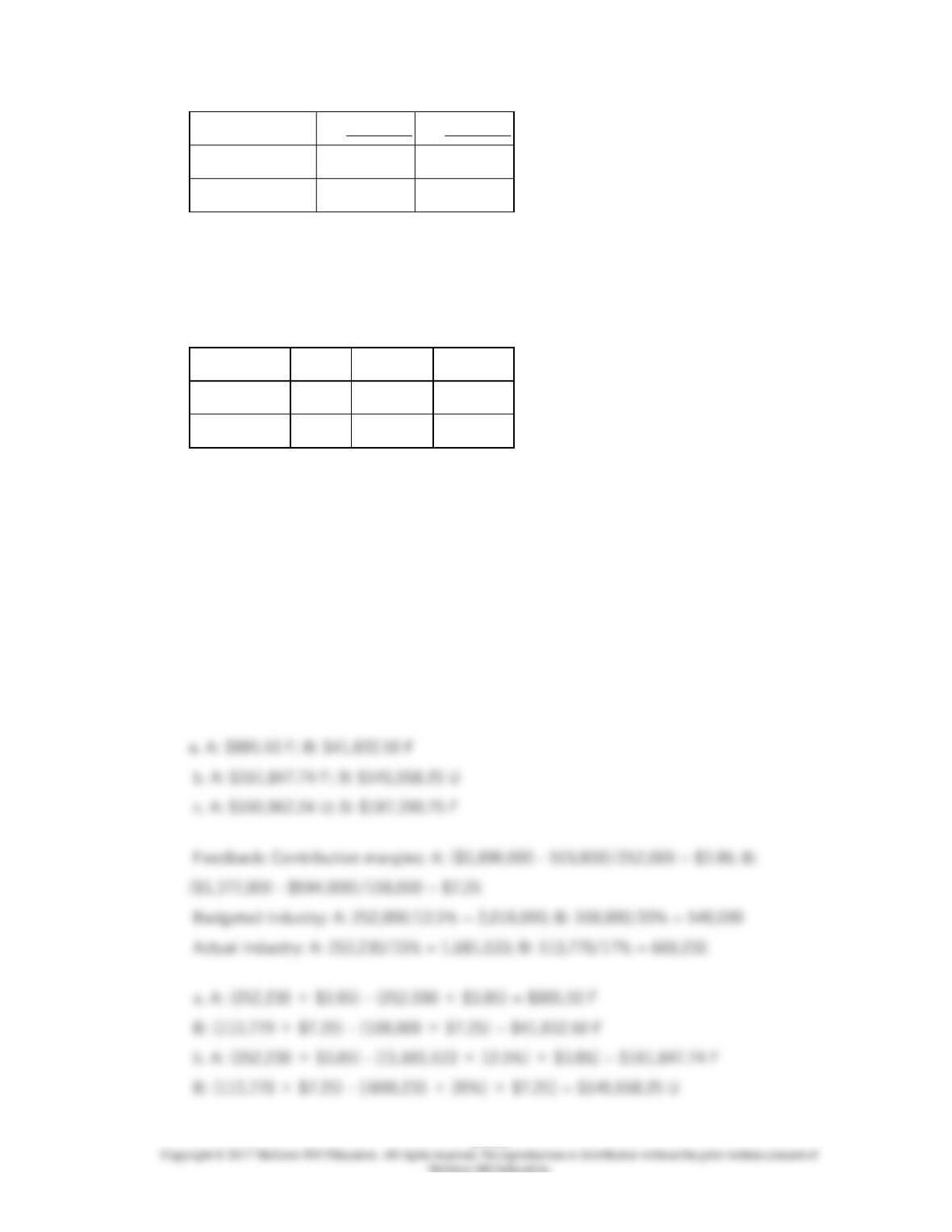

Materials, 2 pounds at $6 per

pound

$12

per

unit

Labor, 3 hours at $15 per hour

$45

per

unit

17-112

Budgeted production for the

year

4,000

units

Actual results were:

Production

3,600

units

Material purchases, 8,000

pounds

$46,400

Labor, 10,360 hours

$160,580

Material used in production

7,300

pounds

117.

The next year’s budget for Howard, Inc., a multi-product company, is given below:

Product A

Product B

Sales

$1,890,000

$1,377,000

Variable costs

919,800

594,000

Fixed costs

500,000

500,000

17-113

Net income

$470,200

283,000

Units

252,000

108,000

Market share

12.5%

20.0%

At the end of the year, the total fixed costs and the variable costs per unit were exactly as

budgeted, but the following units per product line were sold. Howard analyzes the effects

its sales variances have on the profitability of the company.

Product Line

Units

Sales

Mkt share

A

252,230

$1,848,579

15.0%

B

113,770

$1,479,010

17.0%

17-114

118.

The Buffett Company had the following expectations:

Total market for the product

175,000

units

Buffett’s budgeted sales

54,250

Contribution margin per unit

$13.00

Actual results for the year were:

Total market for the product

166,250

units

Buffett’s actual sales

56,525

17-115

119.

The next year’s budget for Alton, Inc., is given below:

Product 1

Product 2

Sales

$945,000

$688,500

Variable costs

459,900

297,000

Fixed costs

300,000

300,000

Net income

$185,100

$91,500

Units

126,000

54,000

Market share

12%

20.0%

At the end of the year, the total fixed costs and the variable costs per unit were exactly as

budgeted, but the following units per product line were sold:

Product Line

Units

Sales

Mkt share

1

126,200

$958,579

16.0%

2

56,800

$721,010

14.2%

17-117

120.

The Stangle Company had the following expectations:

Total market for the product

350,000

units

Stangle’s budgeted sales

108,500

Contribution margin per unit

$12.00

Actual results for the year were:

Total market for the product

332,500

units

Stangle’s actual sales

113,050

121.

Porcini Enterprises produces two products, AR and QT. Actual and budgeted information

for the year ending April 30 is provided below:

Product AR

Product QT

Budget

Actual

Budget

Actual

Unit sales

2,000

2,800

6,000

5,600

Sales

$6,000

$7,560

$12,000

$11,760

Fixed costs

1,800

1,900

2,400

2,800

Variable costs

2,400

2,800

6,000

5,880

17-119

122.

The next year’s budget for Canfield, Inc., a multi-product company, is given below:

Product 1

Product 2

Sales

$1,890,000

$1,377,000

Variable costs

919,800

594,000

Fixed costs

500,000

500,000

Net income

$470,200

$283,000

Units

252,000

108,000

At the end of the year, the total fixed costs and the variable costs per unit were exactly as

budgeted, but the following units per product line were sold. Canfield analyzes the effects

its sales variances have on the profitability of the company.

Product Line

Units

Sales

A

252,230

$1,848,579

B

113,770

$1,479,010