56

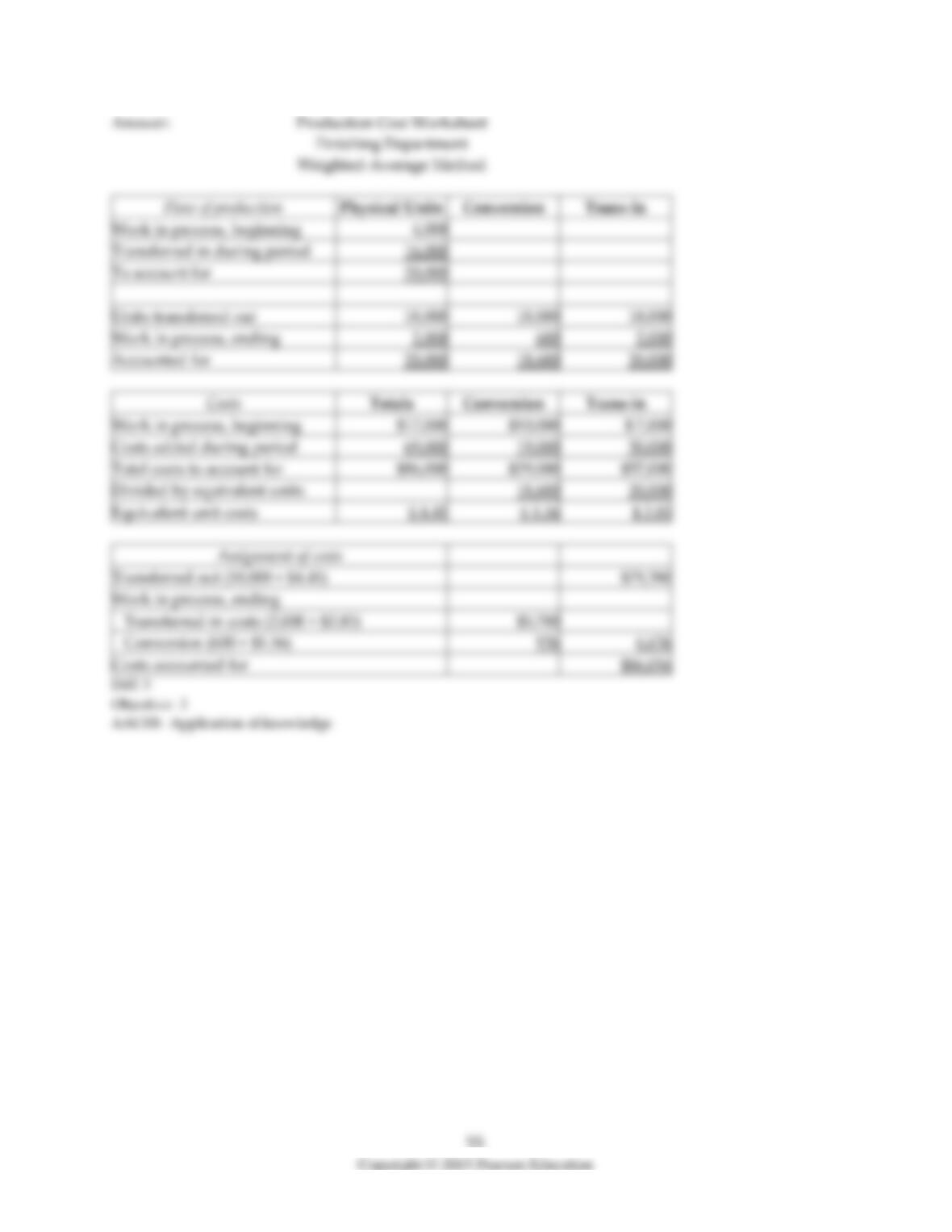

13) Lexington Company produces baseball bats and cricket paddles. It has two departments that process

all products. During July, the beginning work in process in the cutting department was half completed as

to conversion, and complete as to direct materials. The beginning inventory included $40,000 for

materials and $60,000 for conversion costs. Ending work-in-process inventory in the cutting department

was 40% complete. Direct materials are added at the beginning of the process.

Beginning work in process in the finishing department was 80% complete as to conversion. Direct

materials for finishing the units are added near the end of the process. Beginning inventories included

$24,000 for transferred-in costs and $28,000 for conversion costs. Ending inventory was 30% complete.

Additional information about the two departments follows:

Cutting

Finishing

Beginning work-in-process units

20,000

24,000

Units started this period

60,000

Units transferred this period

64,000

68,000

Ending work-in-process units

20,000

Material costs added

$48,000

$34,000

Conversion costs

28,000

68,500

Transferred-out cost

128,000

Required:

Prepare a production cost worksheet, using FIFO for the finishing department.

14) When there are multiple support departments within an organization, it is common to use journal

entries to transfer-in costs from one department to another. What are some of the points to remember

about these costs?

1) Which of the following companies is most likely to use an operation-costing system?

A) a company involved in manufacture of ball bearing on a large scale

B) a company that has been awarded a contract to construct a bridge for the government

C) a company that makes suits for which the basic design is same, but depending on specifications, each

batch of suits varies somewhat from other batches

D) a furniture making company which makes furnitures as per the specifications of the customers

2) Which of the following companies is likely to use a hybrid-costing system?

A) Best Fit Corp., which manufactures pharmaceuticals

B) Rida Corp., which processes and sells, after import, a single variant of Turkish marble to real estate

companies

C) Fast run, which sells a limited range of televisions, which go through similar manufacturing process

D) Karoline Corp., which manufactures and sells a single model of cap

3) Managers find operation costing useful in cost management because it ________.

A) often results in profit maximization

B) results in cost minimization

C) focuses on control of physical processes of a given production system

D) uses job costing to account for the conversion costs and process costing for the material and

customizable components

4) An operation is a standardized method or technique performed repetitively, often on different

materials, resulting in different finished goods.

5) In hybrid-costing systems, managers use process costing to account for the conversion costs and job

costing for the material and customizable components.

6) A hybrid-costing system is a variant of process-costing that allows it to incorporate benefits of standard

costing and activity-based costing.

7) An operation-costing system is a hybrid-costing system applied to batches of similar, but NOT

identical, products.

8) Ford Motor Company is said to use a hybrid costing system. What is a hybrid costing system, and

what would be the advantage to Ford of such a system?

Objective 17.A

1) Emerging Dock Company manufactures boat docks on an assembly line. Its standard costing system

uses two cost categories, direct materials and conversion costs. Each product must pass through the

Assembly Department and the Finishing Department. Direct materials are added at the beginning of the

production process. Conversion costs are allocated evenly throughout production.

Data for the Assembly Department for May 20X5 are:

Work in process, beginning inventory: 70 units

Direct materials (100% complete)

Conversion costs (25% complete)

Units started during May 40 units

Work in process, ending inventory: 10 units

Direct materials (100% complete)

Conversion costs (50% complete)

Costs for May:

Standard costs for Assembly:

Direct materials $8,000 per unit

Conversion costs $32,000 per unit

Work in process, beginning inventory:

Direct materials $280,000

Conversion costs $520,000

What is the balance in ending work–in-process inventory?

A) $164,000

B) $240,000

C) $310,000

D) $340,000

2) Which of the following entries is used to record the standard costs of direct materials assigned to units

worked on and total direct materials variances?

A) Work in Process (at standard costs)

Direct Materials Variances

Direct Materials Control

B) Work in Process (at actual costs)

Direct Materials Variances

Direct Materials Control

C) Direct Materials Variances

Direct Materials Control

Work in Process (at standard costs)

D) Direct Materials Variances

Direct Materials Control

Work in Process (at actual costs)

Answer the following questions using the information below:

Emerging Dock Company manufactures boat docks on an assembly line. Its standard costing system uses

two cost categories, direct materials and conversion costs. Each product must pass through the Assembly

Department and the Finishing Department. Direct materials are added at the beginning of the production

process. Conversion costs are allocated evenly throughout production.

Data for the Assembly Department for May 20X5 are:

Work in process, beginning inventory: 70 units

Direct materials (100% complete)

Conversion costs (25% complete)

Units started during May 40 units

Work in process, ending inventory: 10 units

Direct materials (100% complete)

Conversion costs (50% complete)

Costs for May:

Standard costs for Assembly:

Direct materials $8,000 per unit

Conversion costs $32,000 per unit

Work in process, beginning inventory:

Direct materials $280,000

Conversion costs $520,000

3) Which of the following journal entries records the Assembly Department’s conversion costs at actual

costs for the month, assuming conversion costs are 20% higher than expected?

A) Assembly Department Conversion Cost Control 3,360,000

Various accounts 3,360,000

B) Materials Inventory 3,360,000

Assembly Department Conversion Cost Control 3,360,000

C) Assembly Department Conversion Cost Control 2,800,000

Materials Inventory 2,800,000

D) Materials Inventory 3,360,000

Work in Process — Assembly 3,360,000

4) Which of the following journal entries records the total conversion costs variances of the Assembly

Department, assuming that conversion costs are 20% higher than expected?

A) Work in Process — Assembly 3,360,000

Conversion-Cost Variances 560,000

Assembly Department Conversion Cost Control 2,800,000

B) Assembly Department Conversion Costs Allocated 3,360,000

Direct Materials Variances 560,000

Finishing Department Conversion Cost Control 2,800,000

C) Assembly Department Conversion Costs Allocated 2,800,000

Conversion-Cost Variances 560,000

Assembly Department Conversion Cost Control 3,360,000

D) Work in Process — Assembly 560,000

Assembly Department Conversion Cost Control 560,000

5) Which of the following journal entries records the standard costs of direct materials assigned to units

worked on and total direct materials variances assuming that the Assembly Department used 10% less

materials than expected?

A) Work in Process — Assembly 320,000

Assembly Department Materials Cost Control 320,000

B) Work in Process — Assembly 320,000

Direct Materials Variance 32,000

Assembly Department Materials Cost Control 288,000

C) Work in Process — Assembly 32,000

Assembly Department Materials Cost Control 32,000

D) Work in Process — Assembly 288,000

Direct Materials Variances 32,000

Assembly Department Materials Cost Control 320,000

Answer the following questions using the information below:

Morgan Clay Products manufactures clay molded pottery on an assembly line. Its standard costing

system uses two cost categories, direct materials and conversion costs. Each product must pass through

the Molding Department and the Finishing Department. Direct materials are added at the beginning of

the production process. Conversion costs are allocated evenly throughout production.

Data for the Assembly Department for August 2015 are:

Work in process, beginning inventory: 1,200 units

Direct materials (100% complete)

Conversion costs (40% complete)

Units started during August 675 units

Work in process, ending inventory: 450 units

Direct materials (100% complete)

Conversion costs (60% complete)

Costs for August:

Standard costs for Assembly:

Direct materials $15 per unit

Conversion costs $27.50 per unit

Work in process, beginning inventory:

Direct materials $11,000

Conversion costs $8,250

6) What is the balance in ending work-in-process inventory?

A) $25,500

B) $19,250

C) $15,600

D) $14,175

7) Which of the following journal entries records the Molding Department’s conversion costs for the

month, assuming conversion costs are 10% higher than expected?

A) Molding Department Conversion Cost Control 3,341.25

Various accounts 3,341.25

B) Materials Inventory 33,412.50

Molding Department Conversion Cost Control 33,412.50

C) Molding Department Conversion Cost Control 36,753.75

Various accounts 36,753.75

D) Materials Inventory 36,753.75

Work in Process — Molding 36,753.75

8) From an accounting standpoint, favorable cost variances are debit entries, while unfavorable ones are

credits.

9) Under standard costing the cost per equivalent-unit calculation is more difficult than in either

weighted average or FIFO.

10) Both, the standard-costing method and FIFO, assumes that the earliest equivalent units in beginning

work in process are completed first.

11) Standard costing is NOT possible in a firm that uses process costing.

12) Process-costing systems using standard costs record standard direct material costs in Direct Materials

Control and standard conversion costs in Conversion Costs Control.

13) In companies that produce masses of identical or similar units of output and consequently use

process-costing systems, it is relatively easy to set standards and use a standard cost as the cost per

equivalent unit.

14) BIG Manufacturing Products has been using FIFO process costing for tracking the costs of its

manufacturing activities. However, in recent months, the system has become somewhat bogged down

with details. It seems that, when the company purchased Brown Electronics last year, its product lines

increased six-fold. This has caused both the accountants and the suppliers of the information, the line

managers, great difficulty in keeping the costs of each product line separate. Likewise, the estimation of

the completion of ending work-in-process inventories and the associated costs has become very

cumbersome. The chief financial officer of the company is looking for ways to improve the reporting

system of product costs.

Required:

What can you recommend to improve the situation?