28) What is the estimated net realizable value of the skim goat ice cream at the splitoff point?

A) $271,000

B) $287,400

C) $672,000

D) $712,600

29) Using estimated net realizable value, what amount of the joint costs would be allocated Xyla and the

skim goat ice cream?

A) $672,000 and $271,000

B) $131,464 and $53,016

C) $92,240 and $92,240

D) $144,480 and $72,140

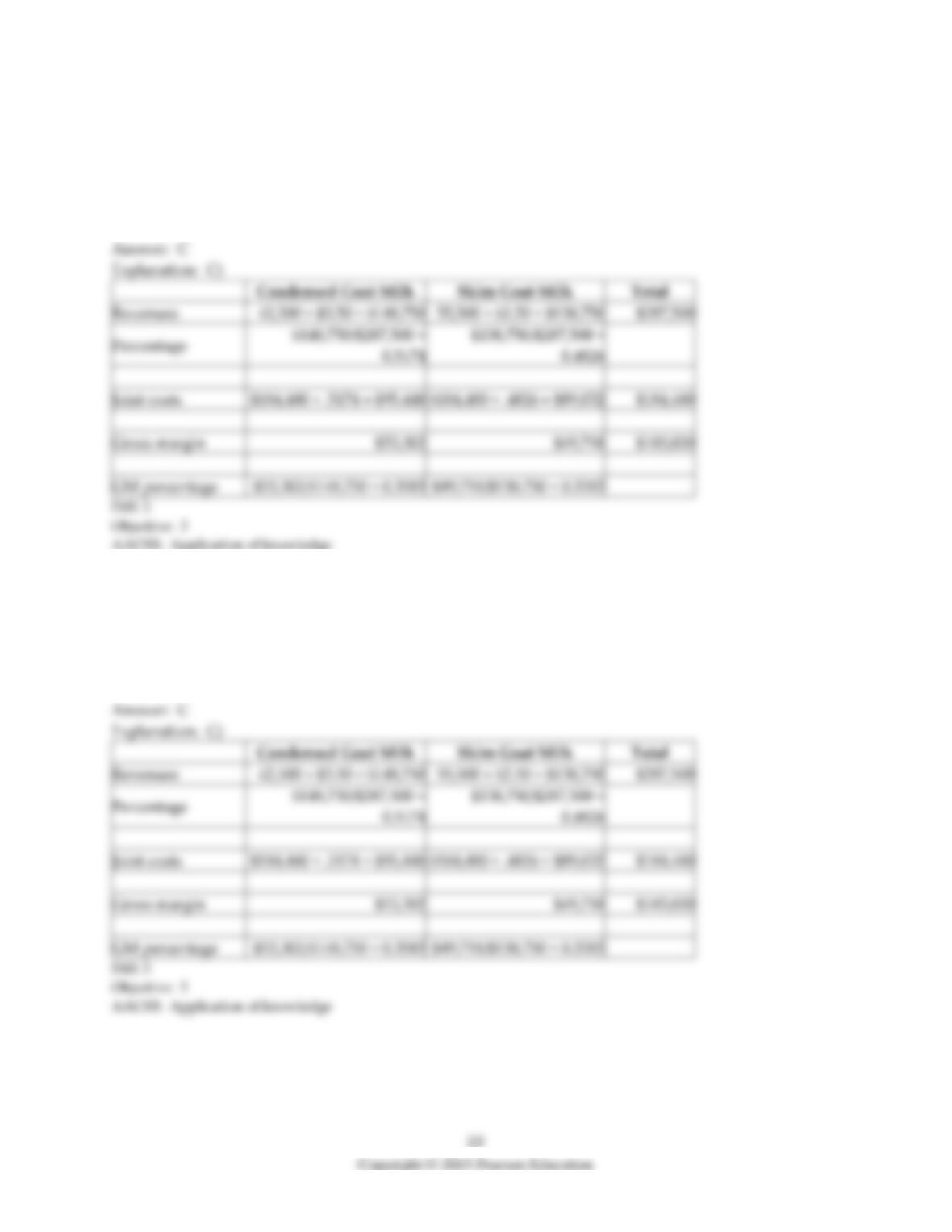

30) Using the sales value at splitoff method, what is the gross-margin percentage for condensed goat milk

at the splitoff point?

A) 51.74%

B) 50.00%

C) 35.83%

D) 48.26%

31) Using the sales value at splitoff method, what is the gross-margin percentage for skim goat milk at the

splitoff point?

A) 51.74%

B) 50.00%

C) 35.83%

D) 48.26%

32) How much (if any) extra income would Green earn if it produced and sold all of the Xyla from the

condensed goat milk? Allocate joint processing costs based upon relative sales value on the splitoff.

(Extra income means income in excess of what Green would have earned from selling condensed goat

milk.)

A) $576,552

B) $132,250

C) $523,250

D) $181,968

33) How much (if any) extra income would Green earn if it produced and sold skim milk ice cream from

goats rather than goat skim milk? Allocate joint processing costs based upon the relative sales value at the

splitoff point.

A) $132,250

B) $576,552

C) $523,250

D) $181,968

34) Chem Manufacturing Company processes direct materials up to the splitoff point where two products

(X and Y) are obtained and sold. The following information was collected for the month of November:

Direct materials processed: 10,000 gallons (10,000 gallons yield 9,500 gallons of good product and 500

gallons of shrinkage)

Production: X 5,000 gallons

Y 4,500 gallons

Sales: X 4,750 at $150 per gallon

Y 4,000 at $100 per gallon

The cost of purchasing 10,000 gallons of direct materials and processing it up to the splitoff point to yield

a total of 9,500 gallons of good products was $975,000.

The beginning inventories totaled 50 gallons for X and 25 gallons for Y. Ending inventory amounts

reflected 300 gallons of Product X and 525 gallons of Product Y. October costs per unit were the same as

November.

Using the physical-volume method, what is Product X’s approximate gross-margin percentage?

A) 32%

B) 34%

C) 35%

D) 38%

35) Beverage Drink Company processes direct materials up to the splitoff point where two products, A

and B, are obtained. The following information was collected for the month of July:

Direct materials processed: 2,500 liters (with 20% shrinkage)

Production: A 1,500 liters

B 500 liters

Sales: A $15.00 per liter

B $10.00 per liter

The cost of purchasing 2,500 liters of direct materials and processing it up to the splitoff point to yield a

total of 2,000 liters of good products was $4,500. There were no inventory balances of A and B.

Product A may be processed further to yield 1,375 liters of Product Z5 for an additional processing cost of

$150. Product Z5 is sold for $25.00 per liter. There was no beginning inventory and ending inventory was

125 liters.

Product B may be processed further to yield 375 liters of Product W3 for an additional processing cost of

$275. Product W3 is sold for $30.00 per liter. There was no beginning inventory and ending inventory was

25 liters.

If Product Z5 and Product W3 are produced, what are the expected sales values of production,

respectively?

A) $11,250 and $34,375

B) $22,500 and $ 5,000

C) $31,250 and $10,500

D) $34,375 and $11,250

36) Cola Drink Company processes direct materials up to the splitoff point where two products, A and B,

are obtained. The following information was collected for the month of July:

Direct materials processed: 2,500 liters (with 20% shrinkage)

Production: A 1,500 liters

B 500 liters

Sales: A $15.00 per liter

B $10.00 per liter

The cost of purchasing 2,500 liters of direct materials and processing it up to the splitoff point to yield a

total of 2,000 liters of good products was $4,500. There were no inventory balances of A and B.

Product A may be processed further to yield 1,375 liters of Product Z5 for an additional processing cost of

$150. Product Z5 is sold for $25.00 per liter. There was no beginning inventory and ending inventory was

125 liters.

Product B may be processed further to yield 375 liters of Product W3 for an additional processing cost of

$275. Product W3 is sold for $30.00 per liter. There was no beginning inventory and ending inventory was

25 liters.

What is Product Z5’s estimated net realizable value at the splitoff point?

A) $11,100

B) $22,350

C) $34,225

D) $34,375

37) Which of the following is true of the physical-measure approach of allocating joint costs?

A) Costs cannot be allocated if the measurement basis for each product are different.

B) Physical measures usually result in less costs being allocated to the product that weighs the most.

C) The physical measure reflects a product’s ability to generate revenues.

D) Obtaining comparable physical measures for all products is always straightforward.

Answer the following questions using the information below:

The Kenton Company processes unprocessed milk to produce two products, Butter Cream and

Condensed Milk. The following information was collected for the month of June:

Direct Materials processed: 18,000 gallons (after shrinkage)

Production:

Butter Cream

7,500

gallons

Condensed Milk

10,500

gallons

Sales:

Butter Cream

7,000

gallons

Condensed Milk

10,000

gallons

Sales Price:

Butter Cream

$3.5

per gallon

Condensed Milk

$7.5

per gallon

Separable costs in

total:

Butter Cream

$12,500

Condensed Milk

$34,700

The cost of purchasing the of unprocessed milk and processing it up to the splitoff point to yield a total of

18000 gallons of saleable product was $46,000.

The company uses constant gross-margin percentage NRV method to allocate the joint costs of

production.

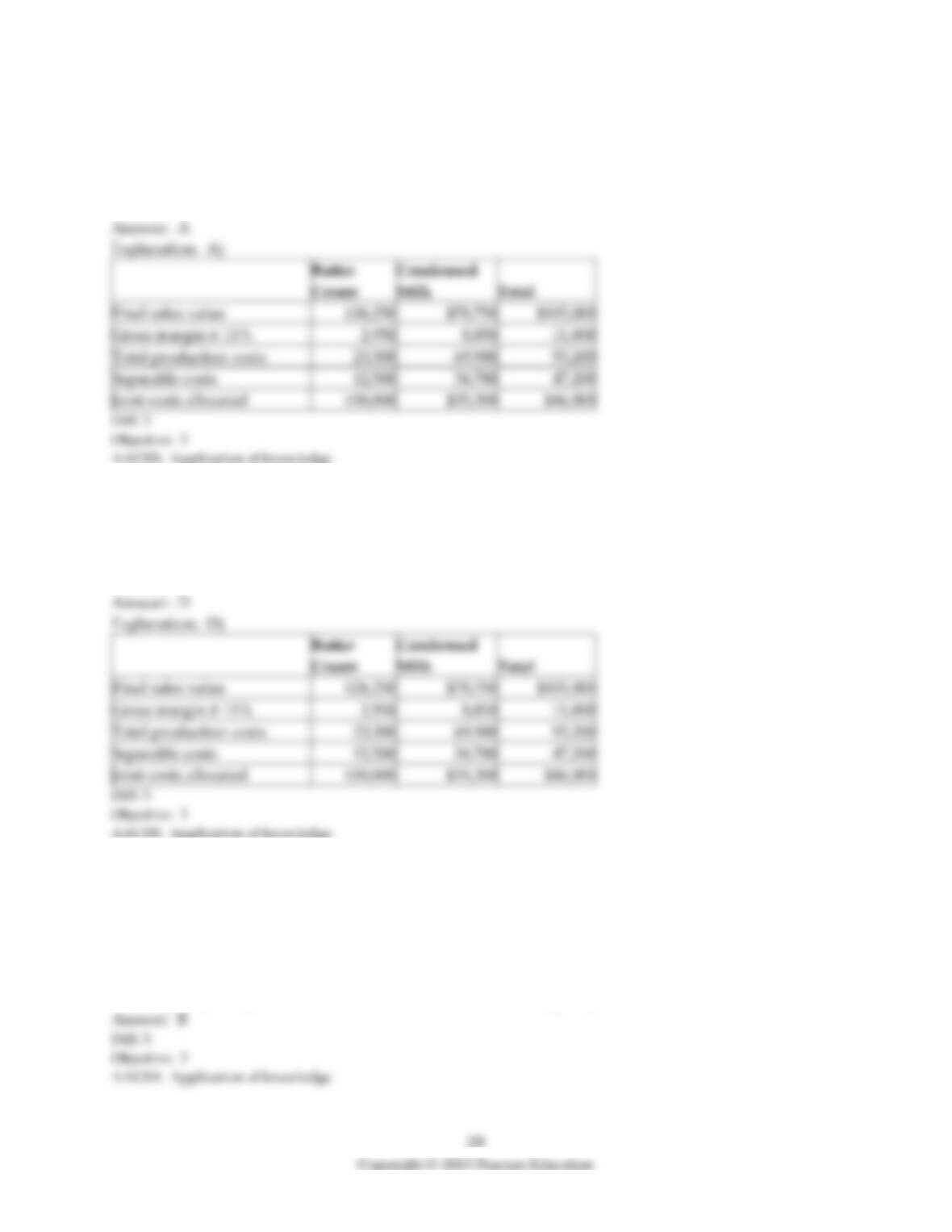

38) What is the constant gross-margin percent for Kenton?

A) 10%

B) 6.3%

C) 11%

D) 6.5%

Total final sales value (7,500 × $3.5) + (10,500 × $7.5)

Total production costs ($46,000 + $12,500 + $34,700)

Gross margin

Gross margin %

39) What is the allocated joint costs of Condensed Milk?

A) $35,200

B) $10,800

C) $12,500

D) $34,700

40) What is the allocated joint costs of Butter Cream?

A) $35,200

B) $12,500

C) $34,700

D) $10,800

41) Which of the following statements is true of Kenton’s joint cost allocations?

A) The gross margin is same for both products because constant gross margin percentage NRV method

ignores profits earned before the splitoff point.

B) One product can receive negative joint costs allocations to bring the other unprofitable product to the

overall average gross margin.

C) Kenton has chosen the easiest method for allocating its joint costs of production.

D) The gross profit percent of condensed milk is lower than the gross profit of butter cream.

42) Which of the methods of allocating joint costs usually is considered the simplest to implement?

A) estimated net realizable value

B) constant gross-margin percentage NRV

C) sales value at splitoff

D) physical measures

43) Which of the following statements is true of the methods for allocating joint costs?

A) Under the cause-and-effect criterion, the physical-measure method is highly desirable.

B) Byproducts are never excluded from the denominator used in the physical-measure method.

C) The NRV method is never used when the selling prices of joint products vary frequently.

D) The sales value at splitoff method follows the benefits-received criterion of cost allocation.

Answer the following questions using the information below:

The Brital Company processes unprocessed milk to produce two products, Butter Cream and Condensed

Milk. The following information was collected for the month of June:

Direct Materials processed: 28,000 gallons

Production:

Butter Cream

12,500

gallons

Condensed Milk

15,500

gallons

Sales:

Butter Cream

12,000

gallons

Condensed Milk

15,000

gallons

Sales:

Butter Cream

$2.5

per gallon

Condensed Milk

$5.5

per gallon

Separable costs in

total:

Butter Cream

$13,500

Condensed Milk

$33,700

The costs of purchasing the of unprocessed milk and processing it up to the splitoff point to yield a total

of 28,000 gallons of saleable product was $46,000.

The company uses constant gross-margin percentage NRV method to allocate the joint costs of

production.

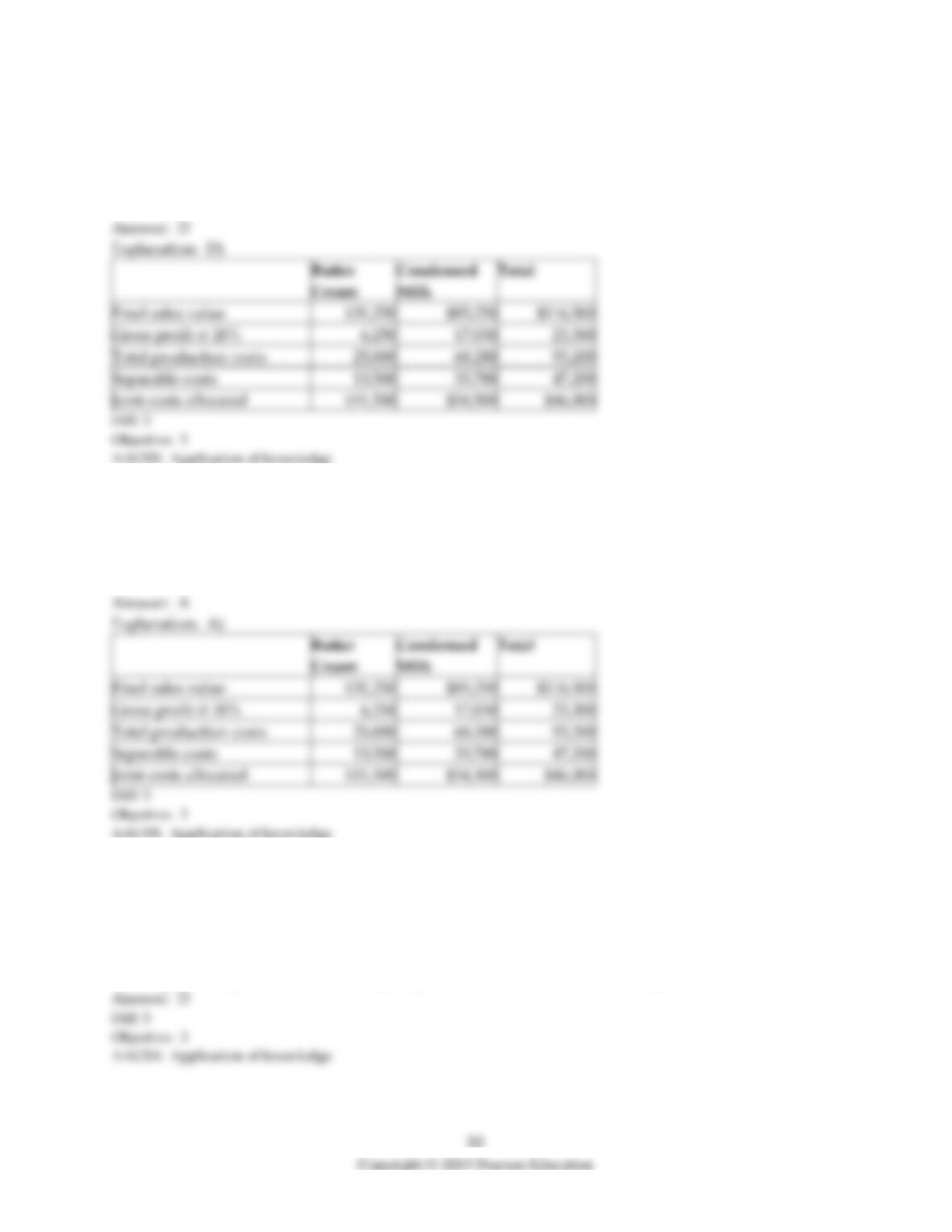

44) What is the constant gross margin percent for Brital?

A) 15%

B) 22%

C) 20%

D) 30%

Total final sales value (12,500 × $2.5) + (15,500 × $5.5)

Total production costs ($46,000 + $13,500 + $33,700)

Gross margin

Gross margin %

45) What is the allocated joint costs of Butter Cream?

A) $33,700

B) $13,500

C) $34,500

D) $11,500

46) What is the allocated joint costs of Condensed Milk?

A) $34,500

B) $13,500

C) $33,700

D) $11,500

47) Which of the following statements is true of Brital?

A) The gross profit percent of condensed milk is lower than the gross profit of butter cream.

B) The gross margin is same for both products because constant gross margin percentage NRV method

ignores profits earned before the splitoff point.

C) The gross profit of condensed milk is lower than the gross profit of butter cream.

D) The gross margin is allocated to the joint products in order to determine the joint-cost allocations.

48) If separable costs of Butter Cream was 16,000 and constant gross margin was 25%, what would have

been the allocated joint costs of Condensed Milk?

A) $7,438

B) $7,538

C) $30,238

D) $30,338

49) If separable costs of Butter Cream was 16,000 and constant gross margin was 25%, what would have

been the total allocated joint costs of production?

A) $37,675

B) $33,700

C) $30,238

D) $34,500

50) Why do accountants criticize the practice of carrying inventories at estimated net realizable values?

A) The costs of producing the products are usually estimates.

B) There is usually no clearly defined realizable value for any inventories.

C) In effect, this practice recognizes income before sales are made.

D) It will result in higher cost of goods sold and lesser profits.

51) The constant gross-margin percentage NRV method of joint cost allocation ________.

A) involves allocating costs in such a way that maintaining the same gross margin percentage for each

product that was obtained in prior years

B) computes gross margin before allocating the costs to the products

C) is the same as the estimated NRV method

D) is the same as the sales-value at splitoff method

52) In joint costing, the constant gross-margin percentage NRV method is an example of allocating costs

using physical measures.

53) In joint costing, using physical measures at splitoff to allocate costs enables the accountant to obtain

individual product costs and gross margins.

54) An advantage of the physical-measure method is that obtaining physical measures for all products is

an easy task.

55) In joint costing, the sales value at splitoff method allocates joint costs entirely to joint products sold

during the accounting period on the basis of the relative total sales value at the splitoff point.

56) In joint costing, the sales value at splitoff method is typically used in preference to the NRV method

only when net realizable value for one or more products at splitoff do not exist.

57) The net realizable value (NRV) method allocates joint costs to joint products produced during the

accounting period on the basis of their relative NRV—final sales value plus separable costs.

58) In joint costing, the physical measures are generally used for products or services that are processed

and, after splitoff, additional value is added to the product and a selling price can be determined.

59) The net realizable value (NRV) method method allocates joint costs to joint products produced during

the accounting period in such a way that each individual product achieves an identical gross-margin

percentage.

60) The constant gross-margin percentage method differs from market-based joint-cost allocation method

(sales value at splitoff and estimated net realizable value) since no account is taken of profits earned

before or after the splitoff point when allocating joint costs.

61) The sales value at splitoff method presupposes the exact number of subsequent steps undertaken for

further processing.

62) In joint costing, outputs with no sales value are always excluded when costs are allocated using

physical measures.

63) The only allowable method of joint cost allocation is specified by FASB.

64) The constant gross-margin percentage NRV method is the only method of allocating joint costs under

which products may receive negative allocations.

65) The sales-value at splitoff method of joint cost allocation involves computation of the relative

amounts of the sales value of the amount of each joint product sold during the period.

66) The constant gross-margin percentage NRV method allocates joint costs to joint products in such a

way that the gross margin on each joint product is the same as it was in the previous year.

67) The constant gross-margin percentage NRV method is the only method whereby products can receive

negative allocations.

68) Under the benefits-received criterion, the physical-measure method is much less desirable than the

sales value at splitoff method. Why?

69) For each of the following methods of allocating joint costs, give a positive or a negative aspect of

selecting each one to allocate joint costs.

a. sales value at splitoff

b. estimated net realizable value method

c. the constant gross margin method

d. a physical measure such as volume