16.3 Understand the implications of new IT developments, such as XBRL, and changes in the

external reporting requirements, such as IFRS, for the design and operation of the general ledger

and reporting system.

1) Which of the following statements is not true regarding XBRL?

A) XBRL is a variant of XML.

B) XBRL is specifically designed for use in communicating the content of financial data.

C) XBRL creates unique tags for each data item.

D) XBRL’s adoption will require accountants and systems professionals tag data for their clients.

2) The benefits of XBRL include

A) organizations can publish financial information only once, using standard XBRL tags.

B) tagged data is readable and interpretable by computers, so users don’t need re-enter data into

order to work with it.

C) Both are benefits of XBRL.

D) Neither is a benefit of XBRL.

3) Communications technology and the Internet can be used to reduce the time and costs

involved in disseminating financial statement information. Users of such financial information

still struggle in that many recipients have different information delivery requirements and may

have to manually reenter the information into their own decision analysis tools. The ideal

solution to solve these problems and efficiently transmit financial information via the Internet is

to use

A) HTML code.

B) XML.

C) pdf file.

D) XBRL.

4) Which of the following statements is not true about an XBRL instance document?

A) An instance document includes instruction code as to how the document should be physically

arranged and displayed.

B) An instance document contains facts about specific financial statement line items.

C) An instance document uses separate tags for each specific element.

D) An instance document can be used to tag financial and nonfinancial elements.

5) IFRS is an acronym for what?

A) International Financial Reporting Standards

B) Internal Forensic Response System

C) Input and Financial Reporting Standards

D) Internal Fault Recovery System

6) Which of the following is true about IFRS?

A) There is a global trend towards using IFRS for reporting purposes, though U.S. companies are

not currently required to do so.

B) The switch to IFRS is required by the Sarbanes-Oxley Act.

C) IFRS is only slightly different than U.S. GAAP.

D) The switch to IFRS is cosmetic only—there isn’t any real impact on AIS.

7) Which of the following scenarios will not be allowed under IFRS?

A) A landscaping and garden retail store keeps piles of river rock, gravel, paving stones, and

small decorative rocks in a fenced area on the side of the store. The store uses the most recent

inventory costs when calculating cost of goods sold, since new inventory is piled on top of the

older inventory.

B) A grocery store strictly enforces a shelf rotation policy, so that older inventory is always at

the front and sold first. The store uses the oldest inventory costs to calculate cost of goods sold.

C) A farm chemical supplier maintains a large holding tank of chemicals, into which deliveries

are periodically combined with the older chemicals. The supplier averages the cost of all

inventory to calculate cost of goods sold.

D) All of the above are acceptable under IFRS.

8) Which of the following is true about accounting for fixed assets?

A) Depreciation expense under IFRS will likely be higher than under GAAP, because

acquisitions of assets with multiple components must be separately depreciated under IFRS,

whereas under GAAP assets could be bundled and depreciated over the longest of the useful life

for any of the components.

B) IFRS doesn’t allow capitalization of any asset that separately accounts for less than 20% of

total assets.

C) Depreciation expense under IFRS will likely be less than under GAAP, because standards for

depreciable lives on asset classes are much longer than under GAAP.

D) IFRS and GAAP account for fixed assets in much the same way.

9) Explain the benefits of XBRL.

10) Identify the year the SEC will require American companies to switch from U.S.-based

GAAP to IFRS as the basis for preparing financial statements.

A) 2016

B) 2018

C) 2020

D) At this point it is unclear when the SEC will require American companies to implement IFRS,

though the SEC remains committed to requiring U.S. companies use IFRS at some point.

11) A major way in which IFRS differs from GAAP that will affect the design of a company’s

general ledger and reporting system is an IFRS principle known as

A) componentization.

B) monetization.

C) securitization.

D) none of the above

12) At a minimum, a switch to IFRS from GAAP will affect companies’ accounting information

system by

A) requiring companies to increase the processing power of their existing accounting information

systems.

B) requiring IT departments to hire programmers that are fluent in languages besides English.

C) requiring the creation of additional fields in research and development (R&D) records to

capture information about the stage of research and development that costs are incurred in.

D) requiring firms to completely redesign their existing accounting information systems because

current systems are not compatible with IFRS accounting principles.

13) XBRL stands for

A) extensible business reporting language.

B) extreme business reporting ledgers.

C) external business reporting language.

D) extensive business report logic.

14) True or False: The SEC requires U.S. companies to use XBRL when submitting their filings.

15) Each specific data item in an XBRL document is called a(n)

A) taxonomy.

B) element.

C) instance.

D) schema.

16.4 Discuss how tools like responsibility accounting, balanced scorecards, and graphs can be

used to provide information managers need to effectively monitor performance.

1) The ________ is the managerial report that shows planned cash inflows and outflows for

major investments or acquisitions.

A) journal voucher list

B) statement of cash flows

C) operating budget

D) capital expenditures budget

2) The operating budget

A) compares estimated cash flows from operations with planned expenditures.

B) shows cash inflows and outflows for each capital project.

C) depicts planned revenues and expenditures for each organizational unit.

D) is used to plan for the purchase and retirement of property, plant, and equipment.

3) Budgets used for internal planning purposes and performance evaluation should be developed

on the basis of

A) responsibility accounting.

B) generally accepted accounting principles.

C) financial accounting standards.

D) managerial accounting standards.

4) Performance reports for cost centers should compare actual versus budget ________ costs.

A) controllable

B) uncontrollable

C) fixed

D) variable

5) Performance reports for sales departments should compare actual revenue versus budgeted

A) revenue.

B) cost.

C) return on investment.

D) profit.

6) Departments that mostly provide services to other units and charge those units for services

rendered should be evaluated as ________ centers.

A) cost

B) profit

C) investment

D) revenue

7) As responsibility reports are rolled up into reports for higher level executives, they

A) become less detailed.

B) become more detailed.

C) become narrower in scope.

D) look about the same.

8) Variances for variable costs will be misleading when the planned output differs from budgeted

output. A solution to this problem would be

A) calling all costs fixed.

B) to use flexible budgeting.

C) better prediction of output.

D) to eliminate the budgeting process.

9) Which of the following balanced scorecard dimensions provides measures on how efficiently

and effectively the organization is performing key business processes?

A) financial

B) internal operations

C) innovation and learning

D) customer

10) Which of the following is not one of the principles of proper graph design for bar charts?

A) Include data values with each element.

B) Use 3-D rather than 2-D bars to make reading easier.

C) Use colors or shades instead of patterns to represent different variables.

D) Use titles that summarize the basic message.

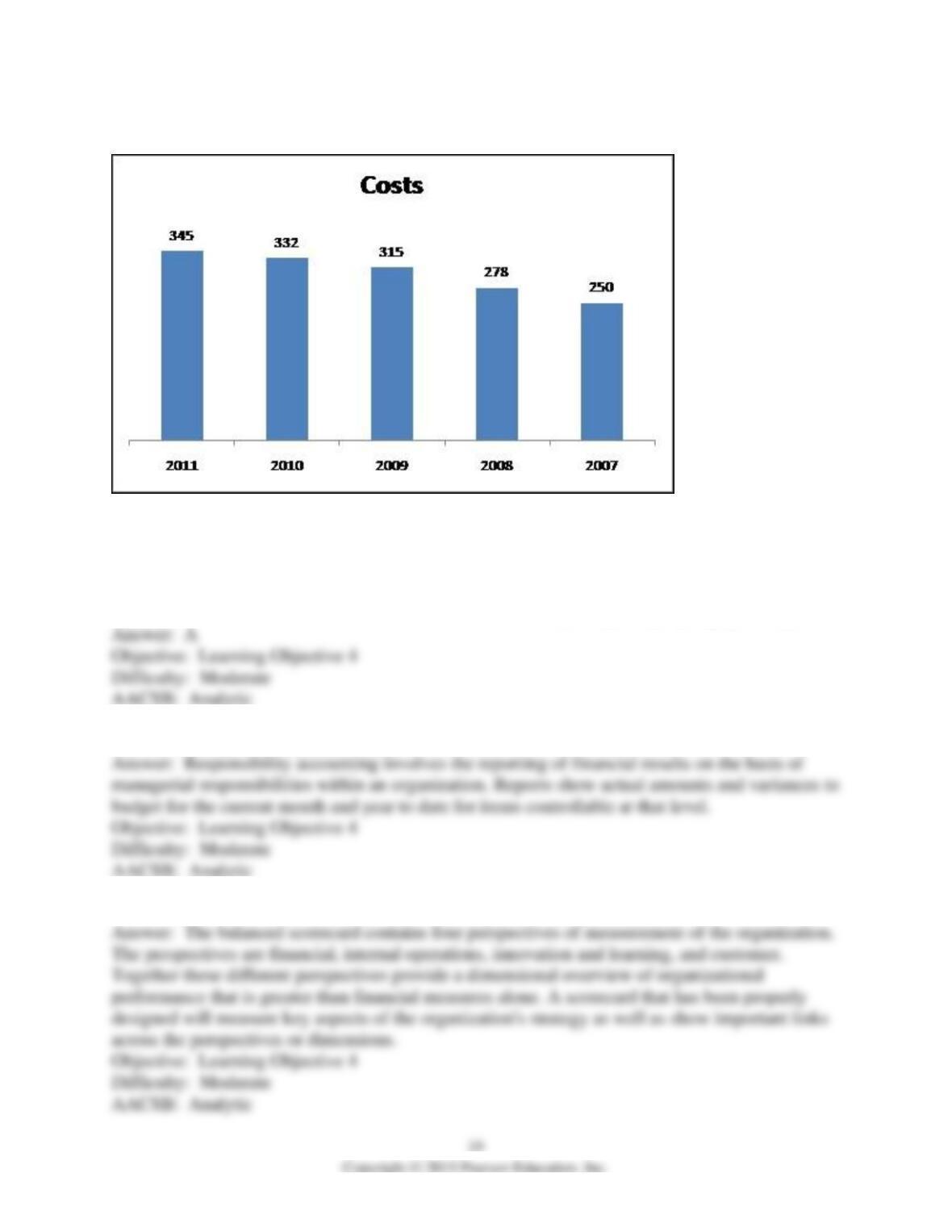

11) Which of the following statements is true about the chart below?

A) The x-axis is in reverse chronological order, which violates a principle of proper graph

design.

B) The chart appears to conform to the principles of proper graph design.

C) The vertical axis doesn’t appear to start at the origin (zero).

D) The chart used 2-D bars instead of 3-D, which violates a principle of proper graph design.

12) What is responsibility accounting?

13) How is a balanced scorecard used to assess organizational performance?

14) Discuss the value and role of budgets as managerial reports.

15) The balanced scorecard attempts to solve what major issue associated with traditional

accounting reports?

A) Traditional accounting reports focus too narrowly on financial performance.

B) Traditional accounting reports are not easily understood by non-accountants.

C) Traditional accounting reports are expensive to produce.

D) Traditional accounting reports are produced too slowly to provide value.

16) Which of the following is not a perspective reflected in the balanced scorecard?

A) customer perspective

B) internal operations perspective

C) financial perspective

D) efficiency and effectiveness perspective

17) True or False: Organizations should set their balanced scorecard targets to reflect industry

benchmark values.

18) Which type of graph is the most commonly used to display trends in financial data?

A) pie chart

B) scatterplot chart

C) bar chart

D) stochastic chart

19) Which of the following balanced scorecard dimensions provides measures on new products?

A) financial

B) internal operations

C) innovation and learning

D) customer