1. The method of evaluating financial data that change under different courses of action is

called:

2. Braizen, Inc. produces a product with a $30 per-unit variable cost and an $80 per-unit

sales price. Fixed manufacturing overhead costs are $100,000. The firm has a one-time

opportunity to sell an additional 1,000 units at $60 each that would not affect its current sales.

Assuming the company has sufficient capacity to produce the additional units, how would the

acceptance of the special order affect net income?

3. Opportunity costs are:

4. A sunk cost is a cost that:

5. _____________ is a cost management technique in which the firm determines the required

cost for a product or service in order to earn a desired profit when the marketplace establishes

the product’s selling price:

6. ______________ can be measured as the income that could have been earned on an asset,

based on the potential rate of return that is lost or sacrificed when one alternative use of the

asset is chosen over another:

7. _____________ costs between two alternative projects are those that would result from

selecting one alternative instead of the other:

8. Which of the following cost classifications would not be considered relevant in comparing

decision alternatives?

9. In considering whether to accept a special order at a price less than the normal selling

price of the product and where the additional sales will make use of present idle capacity, which

of the following costs will not be relevant?

10. A cost classified “for decision-making purposes” would include:

11. Relevant costs in decision-making:

12. A cost is considered relevant if:

13. If a cost is irrelevant to a decision, the cost could not be a:

14. The potential rental value of space used in the manufacturing process:

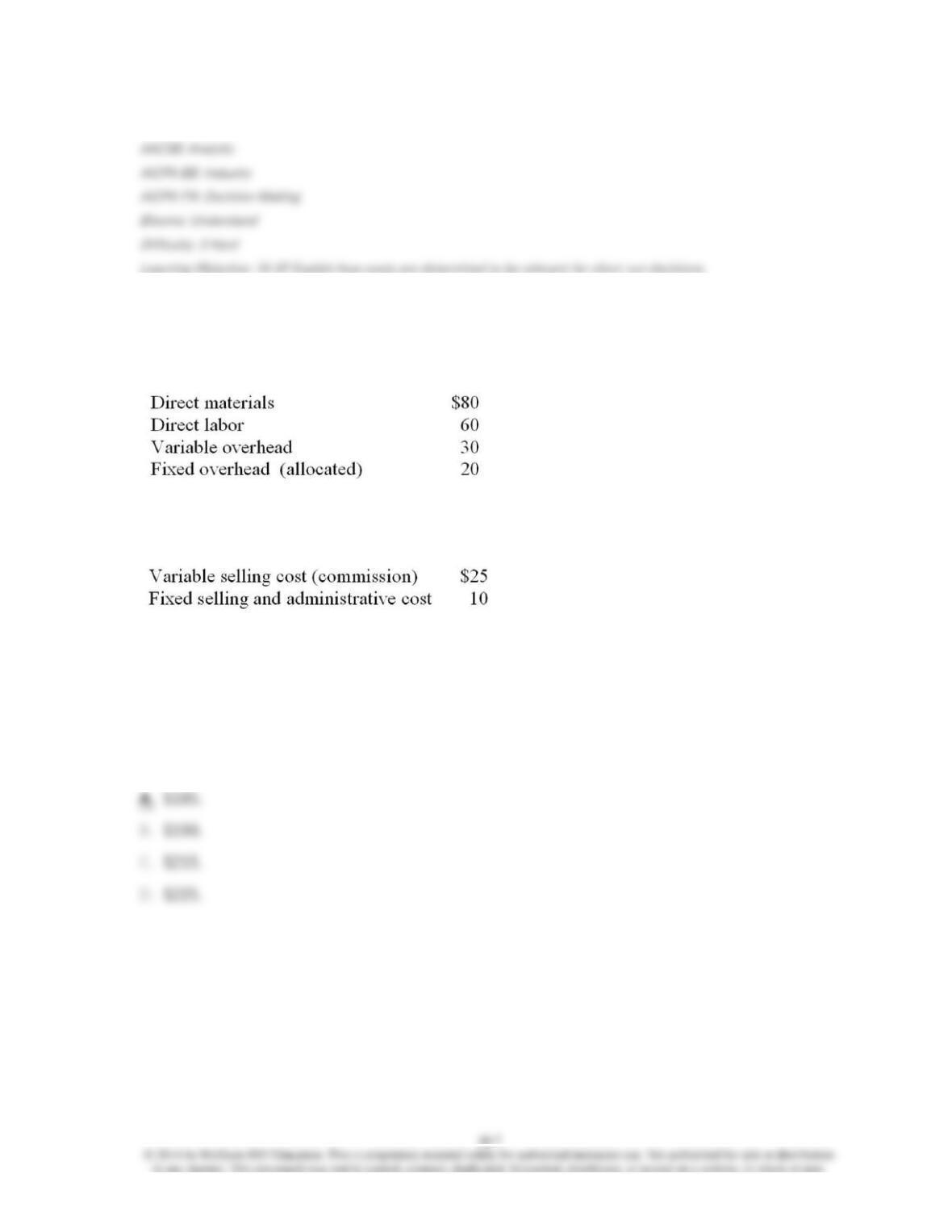

15. Greenland Sports, Inc. has been asked to submit a bid to the National Hockey League on

supplying 1,000 pairs of professional quality skates. The cost per pair of skates has been

determined as follows:

Other non-manufacturing costs associated with each pair of skates are:

Assume the commission on the sale of skates to the National Hockey League would be reduced

to $15 per pair and that available production capacity exists to produce the 1,000 pairs of skates,

the lowest price the firm can bid is some price greater than:

16. The key to analyzing a sell as is or process further decision is to determine that:

17. In a make or buy decision, which of the following costs would be considered relevant?

18. Which of the following qualitative factors favors the buy option in the make or buy

decision?

19. Product Z sells for $18 per unit as is, but if enhanced it can be sold for $24 per unit. The

enhancement process will cost $50,000 for 10,000 units. If the 10,000 units of Product Z are sold

as is without further processing, the company:

20. A(n) _____________ is the minimum cost that can be incurred, which when subtracted

from the selling price, allows for a desired profit to be earned.

21. Product X sells for $80 per unit in the marketplace and ABC Company requires a 35%

minimum profit margin on all product lines. In order to compete in this market, the target cost for

Product X must be equal to or lower than:

22. Which of the following costs are not relevant in a decision to continue or discontinue a

segment of the organization?

23. The decision to continue or discontinue a segment of the business should focus on:

24. The decision for solving production mix problems involving multiple products and scarce

production resources should focus on:

25. XYZ Company produces three products: A, B, and C. Product A has a contribution margin

of $20 and requires 1 hour of machine time. Product B has a contribution margin of $30 and

requires 2 hours of machine time. Product C has a contribution margin of $36 and requires 1.5

hours of machine time. If machine hours are considered scarce, in what product mix order should

XYZ Company schedule the production of Products A, B, and C for the available machine hours?

26. A principal difference between operational budgeting and capital budgeting is the time

frame of the budget. Because of this difference, capital budgeting:

27. Capital budgeting differs from operational budgeting because:

28. Capital expenditure analysis, which leads to the capital budget, attempts to determine

the impact of a proposed capital expenditure on the organization’s:

29. The cost of capital used in the capital budgeting analytical process is primarily a function

of:

30. For most firms, the cost of capital is probably in the range of:

31. When the present value analysis of a proposed investment results in an indication that

the proposal has a rate of return greater than the cost of capital, the investment might not be

made because:

32. Which of the following is not an important qualitative factor to consider in the capital

budgeting decision?

33. Which of the following is typically not important when calculating the net present value of

a project?

34. Depreciation expense is not a cash flow item but it will affect the calculation of which

cash flow item?

35. In order to calculate the net present value of a proposed investment, it is necessary to

know:

36. Discounting a future cash inflow at an 8% discount rate will result in a higher present

value than discounting it at a:

37. If a project promises to generate a higher rate of return than the firm’s cost of capital,

accepting the project will:

38. If the net present value of the investment is $8,510, then:

39. If the net present value of a proposed investment is positive:

40. The present value ratio of a proposed investment will be:

41. The principal weakness of the payback method for evaluating proposed investments is

that it does not: