Name:

Class:

Date:

chapter 15

Indicate whether the statement is true or false.

1. Investments in stocks that are expected to be held for the long term are listed in the Stockholders’ Equity section of the

balance sheet.

a.

True

b.

False

2. When a corporation owns less than 20% of the stock of another company, dividends received are not treated as

revenue.

a.

True

b.

False

3. Comprehensive income does not affect net income or retained earnings.

a.

True

b.

False

4. When a bond is purchased as an investment, the purchase price, minus the brokerage commission, plus any accrued

interest is recorded.

a.

True

b.

False

5. As with other assets, the cost of a bond investment includes all costs related to the purchase.

a.

True

b.

False

6. Investments―Bonds is listed on the balance sheet after Bonds Payable.

a.

True

b.

False

7. Under the equity method, a stock purchase is recorded at its original cost and is not adjusted to fair market value each

accounting period.

a.

True

b.

False

8. Any difference between the fair market values of trading securities and their cost is a realized gain or loss.

a.

True

b.

False

9. The investor carrying an investment by the equity method records cash dividends received as an increase in the amount

of the investment.

a.

True

b.

False

10. Comprehensive income is all changes in stockholders’ equity during the period except those resulting from dividends

and stockholders’ investments.

a.

True

Name:

Class:

Date:

chapter 15

b.

False

11. Any gains or losses on the sale of bonds normally would be reported in the Other Revenue (Loss) section of the

income statement.

a.

True

b.

False

12. The amount of interest paid when buying a bond as an investment should be credited to Interest Revenue.

a.

True

b.

False

13. When bonds held as long-term investments are purchased at a price other than the face value, the premium or discount

should be amortized over the remaining life of the bonds.

a.

True

b.

False

14. In order to maintain a record of the original cost of a trading security, the fair value adjustments are debited or credited

to the account Valuation Allowance for Trading Investments.

a.

True

b.

False

15. The financial statements resulting from combining parent and subsidiary statements are called consolidated

statements.

a.

True

b.

False

16. To record a bond investment made between interest payment dates, Investment in Bonds would be debited and Cash

and Interest Revenue would be credited.

a.

True

b.

False

17. If the proceeds from the sale of bond investments exceed the carrying amount of the bonds, a gain is realized.

a.

True

b.

False

18. An equity investment in less than 20% of another company’s outstanding stock is accounted for using the fair value

method.

a.

True

b.

False

19. Comprehensive income must be reported on the income statement.

a.

True

b.

False

20. Unrealized gains and losses on trading securities are not included in the computation of income from operations.

a.

True

Name:

Class:

Date:

chapter 15

b.

False

21. Investments―Bonds is reported on the balance sheet at lower of cost or market.

a.

True

b.

False

22. Accounting for the sale of stock is the same for both the fair value and equity methods of accounting for investments.

a.

True

b.

False

23. Growth firms generally pay regular dividends to stockholders.

a.

True

b.

False

24. Equity investments do not have a fixed maturity date.

a.

True

b.

False

25. Held-to-maturity securities are reported on the balance sheet at fair market value.

a.

True

b.

False

26. If bonds are purchased between interest dates, the buyer must also pay the seller any accrued interest since the last

interest payment date.

a.

True

b.

False

27. Held-to-maturity investments are recorded at their cost, which would include broker’s commissions.

a.

True

b.

False

28. Held-to-maturity securities maturing beyond a year are reported as noncurrent assets.

a.

True

b.

False

29. The equity method causes the investment account to mirror the proportional changes in book value of the investee.

a.

True

b.

False

30. Investments in bonds that management intends to hold to maturity are called trading securities.

a.

True

b.

False

31. Trading securities are reported on the balance sheet at cost.

a.

True

b.

False

Name:

Class:

Date:

chapter 15

32. When long-term investments in bonds are sold before their maturity date, the seller deducts any accrued interest since

the last interest payment date from the selling price.

a.

True

b.

False

33. Ordinarily, a corporation owning a significant portion of the voting stock of another corporation accounts for the

investment using the equity method.

a.

True

b.

False

34. A foreign currency adjustment is an example of an item that would be included in other comprehensive income.

a.

True

b.

False

35. Trading securities should be reported on the financial statements at fair market value.

a.

True

b.

False

36. The cumulative effects of other comprehensive income items may be reported separately from retained earnings and

paid-in capital on the balance sheet as accumulated other comprehensive income.

a.

True

b.

False

37. A corporation owning all or a majority of the voting stock of another corporation is known as the parent company.

a.

True

b.

False

38. Most companies invest excess cash in bonds as investments in order to profit long-term from the growth of the

investment.

a.

True

b.

False

39. It is not possible for one company to influence the operating policies of another company unless it owns more than a

50% interest in that company.

a.

True

b.

False

40. The cumulative effects of other comprehensive income items are included in retained earnings on the balance sheet.

a.

True

b.

False

41. The equity method is usually more appropriate for accounting for investments where the purchaser does not have

significant influence over the investee.

a.

True

b.

False

Name:

Class:

Date:

chapter 15

42. Available-for-sale securities are securities that management expects to sell in the future, but not in the near term.

a.

True

b.

False

Indicate the answer choice that best completes the statement or answers the question.

43. On June 1, $40,000 of bonds were purchased between interest dates. The brokerage commission was $600. The bonds

pay interest at 12%, which is paid semiannually on January 1 and July 1. How much interest revenue will be recorded on

July 1?

a.

$400

b.

$406

c.

$2,000

d.

$2,400

44. If one company owns more than 50% of the common stock of another company,

a.

a partnership exists

b.

a parent-subsidiary relationship exists

c.

the company whose stock is owned must be liquidated

d.

the cost method should be used to account for the investment

45. When the fair value method is used to account for an equity investment, the carrying value of the investment is

affected by

a.

the dividend distributions of the investee

b.

the periodic net income of the investee

c.

the earnings and dividend distributions of the investee

d.

neither the earnings nor the dividends of the investee

46. Cash generated from operations can be used for which of the following investment purposes?

a.

supporting current operating activities

b.

investing in temporary and long-term investments to earn additional revenue and/or realize an appreciation in

value

c.

investing in the stock of other companies for strategic reasons

d.

All of these choices

47. The account Unrealized Gain (Loss) on Available-for-Sale Investments should be included on the

a.

income statement in the Other Revenue and Expense section

b.

balance sheet as an adjustment to the asset account

c.

balance sheet as an adjustment to stockholders’ equity

d.

statement of retained earnings

48. Held-to-maturity securities

a.

are reported at fair market value

b.

include stocks as well as bonds

c.

may be reported as current or noncurrent assets

d.

All of these choices

Name:

Class:

Date:

chapter 15

49. Alan Company purchased $400,000 of ABC Co. 5% bonds at 100 plus accrued interest of $4,500. Alan later sold

$250,000 of the bonds at 97. The journal entry for the purchase would include a

a.

credit to Interest Receivable for $4,500

b.

credit to Interest Revenue for $4,500

c.

debit to Interest Receivable for $4,500

d.

debit to Interest Revenue for $4,500

Use this information for Pierce Company to answer the questions that follow.

On May 1, Pierce Company purchased $60,000 of Stanton Company’s 12% bonds at 100 plus accrued interest of $2,400.

On June 30, Pierce received its first semiannual interest. On February 1, Pierce sold $50,000 of the bonds at 103 plus

accrued interest.

50. The journal entry Pierce records on June 30 will include a

a.

credit to Interest Revenue for $2,400

b.

debit to Cash for $3,600

c.

credit to Cash for $2,400

d.

credit to Interest Receivable for $1,200

51. Ruben Company purchased $100,000 of Evans Company bonds at 100 plus $1,500 in accrued interest. The bond

interest rate is 8%, and interest is paid semiannually. The journal entry for the receipt of interest on the next interest

payment date would be

a.

debit Cash, $4,000; credit Interest Revenue, $4,000

b.

debit Cash, $4,000; credit Interest Receivable, $4,000

c.

debit Cash, $4,000; credit Interest Receivable, $1,500, and Interest Revenue, $2,500

d.

debit Cash, $2,500; credit Interest Revenue, $2,500

52. Long-term investments that involve the purchase of a significant portion of the stock of another company may be held

for a strategic purpose, such as

a.

the receipt of dividends

b.

expansion into new markets

c.

the gains from the increase in market value

d.

the receipt of interest revenue

53. The valuation allowance for the trading investments account is found on the

a.

income statement in the Other Revenue and Expense section

b.

balance sheet as an adjustment to the asset account

c.

balance sheet as an adjustment to stockholders’ equity

d.

statement of retained earnings

54. Which of the following is not a part of comprehensive income?

a.

foreign currency adjustments

b.

cash flows from stock investments

c.

unrealized gains and losses on available-for-sale securities

d.

pension liability adjustments

Name:

Class:

Date:

chapter 15

55. The market price that would be received for a security if it were sold is the

a.

fair value

b.

test value

c.

investing value

d.

historical value

56. An investor purchased 500 shares of common stock, $25 par, for $19,250. Subsequently, 100 shares were sold for $35

per share. What is the amount of gain or loss on the sale?

a.

$3,500 gain

b.

$350 gain

c.

$350 loss

d.

$500 gain

57. Temporary investments such as in trading securities are

a.

recorded at cost but reported at fair market value

b.

recorded at cost and reported at cost

c.

recorded at cost but reported at lower of cost or fair market value

d.

recorded at fair market value and reported at fair market value

58. The equity method of accounting for investments requires

a.

a year-end adjustment to revalue the stock to lower of cost or market

b.

the investment to be reported at its original cost

c.

the investment to be increased by the reported net income of the investee

d.

the investment to be increased by the dividends paid by the investee

59. For accounting purposes, the method used to account for investments in common stock is determined by

a.

the amount paid for the stock by the investor

b.

whether the acquisition of the stock by the investor was “friendly” or “hostile”

c.

the extent of an investor’s influence over the operating and financial affairs of the investee

d.

whether the stock has paid dividends in past years

60. An investor purchased 500 shares of common stock, $25 par, for $21,750. Subsequently, 100 shares were sold for

$49.50 per share. What is the amount of gain or loss on the sale?

a.

$12,750 gain

b.

$600 gain

c.

$600 loss

d.

$9,250 loss

61. Gale Company owns 87% of the outstanding stock of Leonardo Company. Leonardo Company is referred to as the

a.

parent company

b.

minority interest

c.

affiliate company

d.

subsidiary company

Name:

Class:

Date:

chapter 15

62. Which of the following statements is not a reason a company may purchase another company’s stock?

a.

earning a return on excess cash

b.

sustaining the other company’s stock price

c.

gaining control of another company’s operations

d.

developing or maintaining business relationships

63. The method of accounting for investments in equity securities in which the investor records its share of periodic net

income of the investee is the

a.

cost method

b.

fair value method

c.

income method

d.

equity method

64. Debt securities include

a.

preferred stock

b.

common stock

c.

notes and bonds

d.

All of these choices

65. Which of the following items would not affect the investor’s income for the period?

a.

interest received on a temporary investment in bonds

b.

dividends received on a long-term investment in stock where the investor owns 10% of the investee’s stock

c.

dividends received on a long-term investment in stock where the investor owns 30% of the investee’s stock

d.

interest received on a long-term investment in bonds

66. When shares of stock held as an investment are sold, the difference between the proceeds and the carrying amount of

the investment is recorded as a(n)

a.

prior period adjustment

b.

operating income and loss

c.

paid-in capital addition

d.

gain or loss

67. Ruben Company purchased $100,000 of Evans Company bonds at 100 plus $1,500 in accrued interest. The bond

interest rate is 8% and interest is paid semiannually. The journal entry for the purchase would be

a.

debit Investments—Evans Company Bonds, $101,500; credit Cash, $101,500

b.

debit Investments—Evans Company Bonds, $100,000; credit Interest Revenue, $1,500, and Cash, $98,500

c.

debit Investments—Evans Company Bonds, $100,000, and Interest Receivable $1,500; credit Cash, $101,500

d.

debit Investments—Evans Company Bonds, $100,000; credit Cash, $100,000

68. Jacks Corporation purchases $200,000 bonds plus accrued interest for 2 months of $2,000 from Kennedy Company on

March 1. The bonds have an annual interest rate of 6% payable on June 30 and December 31. The entry for the purchase

of the bonds would include a

a.

debit to Interest Receivable for $2,000

b.

debit to Investments—Kennedy Company Bonds for $202,000

c.

debit to Cash for $200,000

Name:

Class:

Date:

chapter 15

d.

credit to Interest Revenue for $2,000

69. Blanton Corporation purchased 15% of the outstanding shares of common stock of Worton Corporation as a long-term

investment. Subsequently, Worton Corporation reported net income and declared and paid cash dividends. What journal

entry would Blanton Corporation use for the dividends it receives?

a.

debit Investments—Worton Corporation Stock; credit Cash

b.

debit Cash; credit Dividend Revenue

c.

debit Investments—Worton Corporation Stock; credit Income of Worton Corporation

d.

debit Cash; credit Investments—Worton Corporation Stock

70. In general, consolidated financial statements should be prepared

a.

when a corporation owns more than 20% and less than 40% of the common stock of another company

b.

when a corporation owns more than 50% of the common stock of another company

c.

only when a corporation owns 100% of the common stock of another company

d.

whenever the market value of the stock investment is significantly lower than its cost

71. Yankton Company began the year without an investment portfolio. During the year, it purchased investments

classified as available-for-sale securities at a cost of $13,000. At the end of the year, the market value of the securities was

$11,000. Yankton Company’s financial statements for the current year should show

a.

an unrealized loss of $2,000 on the income statement and available-for-sale investments of $13,000 on the

balance sheet

b.

no loss on the income statement and available-for-sale investments of $13,000 on the balance sheet

c.

no loss on the income statement, net available-for-sale investments of $11,000 in the Current Assets section of

the balance sheet, and an unrealized loss of $2,000 as a stockholders’ equity adjustment on the balance sheet

d.

a realized loss of $2,000 on the income statement and net available-for-sale investments of $11,000 on the

balance sheet

72. GAAP requires trading and available-for-sale investments to be reported at their

a.

fair value

b.

historical cost

c.

market value

d.

net realizable value

73. Financial statements in which financial data for two or more companies are combined as a single entity are called

a.

conventional statements

b.

consolidated statements

c.

audited statements

d.

constitutional statements

74. Zach Company owns 45% of the voting stock of Tomas Corporation and uses the equity method in recording this

investment. Tomas Corporation reported a $20,000 net loss. Zach Company‘s entry would include a

a.

credit to Cash for $9,000

b.

debit to the investment account for $9,000

c.

credit to the investment account for $9,000

d.

credit to a loss account for $9,000

Name:

Class:

Date:

chapter 15

75. The account Unrealized Gain (Loss) on Trading Investments should be included on the

a.

income statement in the Other Revenue and Expense section

b.

balance sheet as an adjustment to the asset account

c.

balance sheet as an adjustment to stockholders’ equity

d.

statement of retained earnings

76. Edison Corporation paid a dividend of $10 per share on its $100 par preferred stock and $4 per share on its $20 par

common stock. The market value of the common stock is $80 per share. Edison’s dividend yield is

a.

5%

b.

10%

c.

25%

d.

20%

77. Which of the following is not a reason to invest excess cash in temporary investments?

a.

earn interest revenue

b.

influence the operations of another company

c.

receive dividends

d.

realize gains from the increase in market value of the securities

78. Parker Company owns 83% of the outstanding stock of Tadeo Company. Parker Company is referred to as the

a.

parent company

b.

minority interest

c.

affiliate company

d.

subsidiary company

79. Equity securities include

a.

preferred stock

b.

notes

c.

bonds

d.

bank deposits

80. Which of the following stock investments should be accounted for using the fair value method?

a.

investments of less than 20% ownership

b.

investments between 20% and 50% ownership

c.

all investments of less 50% ownership

d.

investments of over 50% ownership

81. On February 12, Addison, Inc. purchased 6,000 shares of Lucas Company at $22 per share plus a $240 brokerage fee.

On August 22, Lucas paid a dividend per share of $0.42. On November 10, 4,000 shares of Lucas stock were sold for $28

per share less a $160 brokerage fee. The journal entry for the sale would include a

a.

debit to Cash for $111,840

b.

credit to Investments—Lucas Company Stock for $112,000

c.

credit to Loss on Sale for $23,680

d.

debit to Cash for $112,000

Name:

Class:

Date:

chapter 15

82. On February 12, Addison, Inc., purchased 6,000 shares of Lucas Company at $22 per share plus a $240 brokerage

fee. On August 22, Lucas paid a dividend per share of $0.42. On November 10, 4,000 shares of Lucas stock were sold for

$28 per share less a $160 brokerage fee. The journal entry for the purchase would include a

a.

debit to Investments—Lucas Company Stock for $132,000

b.

credit to Cash for $132,000

c.

debit to Investments—Lucas Company Stock for $132,240

d.

credit to Investments—Lucas Company Stock for $240

83. A company whose stock is more than 50% owned by another company is called the

a.

controlling company

b.

investee company

c.

subsidiary company

d.

sibling company

84. The fair value method of accounting for stock

a.

recognizes dividends as income

b.

is only appropriate as part of a consolidation

c.

requires the investment to be increased by the reported net income of the investee

d.

requires the investment to be decreased by the reported net income of the investee

85. Ruben Company purchased $100,000 of Evans Company bonds at 100. Ruben later sold the bonds for $104,500 plus

$500 in accrued interest. The journal entry for the sale of the bonds would be

a.

debit Cash, $105,000; credit Investments—Evans Company Bonds, $104,500, and Interest Revenue, $500

b.

debit Cash, $105,000; credit Investments—Evans Company Bonds, $100,000, and Gain on Sale of

Investments, $5,000

c.

debit Cash, $104,500, and Interest Receivable, $500; credit Investments—Evans Company Bonds, $100,000,

Gain on Sale of Investments, $4,500, and Interest Revenue, $500

d.

debit Cash, $105,000; credit Investments—Evans Company Bonds, $100,000, Gain on Sale of Investments,

$4,500, and Interest Revenue, $500

86. Temporary investments

a.

are reported as current assets

b.

include cash equivalents

c.

do not include equity securities

d.

include cash used to expand current operations

87. Yankton Company began the year without an investment portfolio. During the year, it purchased investments

classified as trading securities at a cost of $13,000. At the end of the year, the market value of the securities was $11,000.

Yankton Company’s financial statements for the current year should show

a.

a realized loss of $2,000 on the income statement and net trading investments of $13,000 on the balance sheet

b.

no loss on the income statement and net trading investments of $13,000 on the balance sheet

c.

no loss on the income statement, net trading investments of $11,000, and an unrealized loss of $2,000 as a

stockholders’ equity adjustment on the balance sheet

d.

an unrealized loss of $2,000 on the income statement and net trading investments of $11,000 on the balance

sheet

Name:

Class:

Date:

chapter 15

Use this information for Pierce Company to answer the questions that follow.

On May 1, Pierce Company purchased $60,000 of Stanton Company’s 12% bonds at 100 plus accrued interest of $2,400.

On June 30, Pierce received its first semiannual interest. On February 1, Pierce sold $50,000 of the bonds at 103 plus

accrued interest.

88. The journal entry Pierce records on February 1 will include a

a.

credit to Interest Revenue for $1,500

b.

credit to Gain on Sale of Investments for $1,500

c.

credit to Cash for $52,500

d.

credit to Interest Receivable for $600

89. Armando Company owns 17,000 of the 70,000 shares of common stock outstanding of Tito Company and exercises a

significant influence over its operating and financial policies. The investment should be accounted for by the

a.

equity method

b.

fair value method

c.

consolidation method

d.

fair value or equity method

90. Under the equity method, the receipt of cash dividends on an investment in common stock of Vallerio Corporation is

accounted for as a debit to Cash and a credit to

a.

Investment in Vallerio Corporation Stock

b.

Retained Earnings

c.

Dividend Revenue

d.

Dividends Receivable

91. Trading securities are

a.

reported at fair value in the Assets section of the balance sheet and any associated unrealized gains or losses

are reported in the Other Revenue (Loss) section of the income statement

b.

reported in the Stockholders’ Equity section of the balance sheet and any associated unrealized gains or losses

are reported in the Other Revenue (Loss) section of the income statement

c.

reported at cost on the balance sheet and any associated unrealized gains or losses are reported as an expense

against operating revenue on the income statement

d.

reported at fair value in the Assets section of the balance sheet and any associated unrealized gains or losses

are reported as an adjustment in the Stockholders’ Equity section of the balance sheet

92. Held-to-maturity securities

a.

are reported at their fair market value on the balance sheet date

b.

include both stocks and bonds

c.

are primarily purchased to earn interest revenue

d.

All of these choices

93. Which of the following is part of the primary objective of investing in temporary investments?

a.

All of these choices

b.

realize gains from increases in market price of the securities

c.

receive dividends

Name:

Class:

Date:

chapter 15

d.

earn interest revenue

Use this information for Pierce Company to answer the questions that follow.

On May 1, Pierce Company purchased $60,000 of Stanton Company’s 12% bonds at 100 plus accrued interest of $2,400.

On June 30, Pierce received its first semiannual interest. On February 1, Pierce sold $50,000 of the bonds at 103 plus

accrued interest.

94. What are the total proceeds from the February 1 sale?

a.

$52,400

b.

$51,500

c.

$50,000

d.

$52,000

95. On June 1, $50,000 of bonds were purchased between interest dates. The brokerage commission was $500. The bonds

pay interest at 12%, which is paid semiannually on January 1 and July 1. What is the total cost to be debited to

Investments—Bonds?

a.

$50,000

b.

$50,500

c.

$49,500

d.

$53,000

96. On January 1, Butte Company’s valuation allowance for trading investments account has a debit balance of $23,200.

On December 31, the cost of the trading securities portfolio was $80,000. The fair value was $98,000. Which of the

following would Butte report on the income statement for the current year?

a.

an unrealized loss on trading investments, $5,200

b.

an unrealized gain on trading investments, $5,200

c.

an unrealized gain on trading investments, $18,000

d.

an unrealized loss on trading investments, $18,000

97. On April 1, Alliance Company purchased $50,000 of Tetter Company’s 12% bonds at 100 plus accrued interest of

$2,000. On June 30, Alliance received its first semiannual interest. On February 1, Alliance sold $40,000 of the bonds at

103 plus accrued interest. The journal entry Alliance will record on April 1 for the purchase of the bonds will include a

a.

credit to Interest Payable for $2,000

b.

debit to Investments—Tetter Company Bonds for $52,000

c.

debit to Cash for $50,000

d.

debit to Investments—Tetter Company Bonds for $50,000

98. A company that has 25,000 shares of $5.00 par common stock issued and outstanding paid a dividend of $0.40 per

share. The market value of the stock is $16 per share. The company’s dividend yield is

a.

2.5%

b.

400%

c.

16%

d.

40%

99. The dividend yield is measured as

Name:

Class:

Date:

chapter 15

a.

Dividends per Share of Common Stock ÷ Market Price per Share of Common Stock

b.

Dividends per Share of Preferred Stock ÷ Market Price per Share of Common Stock

c.

Dividends per Share of Common Stock ÷ Market Price per Share of Preferred Stock

d.

Dividends per Share of Preferred Stock ÷ Market Price per Share of Preferred Stock

100. Companies may report comprehensive income on each of the following statements except

a.

the income statement

b.

a separate statement of comprehensive income

c.

the statement of cash flows

d.

None of these choices

101. Which of the following would be considered an “other comprehensive income” item?

a.

net income

b.

extraordinary loss related to flood

c.

gain on disposal of discontinued operations

d.

unrealized loss on available-for-sale securities

102. Wendell Company owns 28% of the common stock of Porter Company and accounts for the investment using the

equity method. Assuming that Wendell Company purchased the stock several years ago, the balance in the investment

account would be equal to the original cost of the

a.

investment

b.

investment plus Wendell’s share of Porter’s net income earned since the investment was purchased

c.

investment plus the total amount of dividends Wendell has received from Porter since the investment was

purchased

d.

investment plus Wendell’s share of Porter’s net income earned since the investment was purchased minus the

total amount of dividends Wendell has received from Porter since the investment was purchased

103. Interest revenue on bonds is reported as

a.

an addition to the investment in bonds account

b.

part of comprehensive income but not as part of net income

c.

part of Other Revenue (Loss)

d.

part of income from operations

104. Blanton Corporation purchased 35% of the outstanding shares of common stock of Worton Corporation as a long–

term investment. Subsequently, Worton Corporation reported net income and declared and paid cash dividends. What

journal entry would Blanton Corporation use for the dividends it receives from Worton Corporation?

a.

debit Investments—Worton Corporation Stock; credit Cash

b.

debit Cash; credit Dividend Revenue

c.

debit Investments—Worton Corporation Stock; credit Income of Worton Corporation

d.

debit Cash; credit Investments—Worton Corporation Stock

105. Jarvis Corporation makes an investment in 100 shares of Saxton Company’s common stock. The stock is purchased

for $45 a share plus brokerage fees of $280. The journal entry for the purchase is

a.

Cash 4,500

Investments—Saxton Company Stock 4,500

Name:

Class:

Date:

chapter 15

b.

Investments—Saxton Company Stock 4,780

Cash 4,780

c.

Investments—Saxton Company Stock 4,500

Brokerage Fee Expense 280

Cash 4,780

d.

Investments—Saxton Company Stock 4,500

Cash 4,500

106. On July 5, Winter Company had a market price of $58 per share of common stock. For the previous year, Winter

Company paid an annual dividend of $3.48 per share. What is the dividend yield for Winter Company?

a.

6.0%

b.

0.6%

c.

16.67%

d.

1.67%

Match each of the definitions that follow with the appropriate investment term (a–j).

a.

Equity method

b.

Parent company

c.

Subsidiary company

d.

Consolidated financial statements

e.

Fair value

f.

Unrealized gain or loss on investments.

g.

Valuation allowance for investments

h.

Dividend yield

i.

Amortized cost

j.

Fair value method

107. A corporation owning all or the majority of the voting stock of another corporation

108. A balance sheet account where the fair value adjustment for investments is reported

109. A corporation controlled by another corporation that owns all or the majority of its voting stock

110. The method of accounting for investments of 20% to 50% in another company’s stock

111. The market price that would be received if an investment were sold

112. Measurement of the rate of return to stockholders based on cash dividends

113. Combined reporting of a corporation and another corporation it controls

114. Recognition of changes in the fair value of short-term investments

Name:

Class:

Date:

chapter 15

115. The value assigned to held-to-maturity securities

116. Appropriate method for accounting for small stock investments

Match each of the definitions that follow with the appropriate investment term (a–j).

a.

Debt securities

b.

Equity securities

c.

Investor

d.

Investee

e.

Fair value method

f.

Trading securities

g.

Available-for-sale securities

h.

Held-to-maturity securities

i.

Equity method

j.

Business combination

117. Debt and equity securities purchased and sold to earn short-term profits from changes in the market price

118. Preferred and common stock that represent ownership in a company and do not have a fixed maturity date

119. The method of reporting an investment that represents less than 20% of the voting stock of another company

120. When using this, dividends are treated as a reduction of the investment

121. Notes and bonds that pay interest and have a fixed maturity

122. Debt investments that a company intends to keep until their maturity date

123. Securities not held for trading or to maturity or other strategic reasons

124. The company investing in another company’s stock

125. What occurs when a company purchases 50% or more of another company’s stock

126. The company whose stock is purchased by another entity

127. LM, Inc., reported net income for the year ending December 31 of $483,500. Dividends paid during the year totaled

$52,900. The company holds available-for-sale securities with an original cost of $162,000 and a fair value of $181,000 at

the end of the year. It also holds trading securities with an original cost of $150,000 and a fair value of $147,000. Retained

earnings on January 1 was $736,400, and accumulated other comprehensive income on January 1 was $16,200.

Compute the following balances to be reported in the financial statements dated December 31:

a. Valuation allowance for available-for-sale securities

b. Comprehensive income

c. Retained earnings

d. Accumulated other comprehensive income

Name:

Class:

Date:

chapter 15

128. The income statement for Hudson Company reported net income of $345,000 for the year ended December 31 before

considering the following:

• During the year, the company purchased trading securities.

• At year-end, the fair value of the investment portfolio was $23,000 less than cost.

• The balance of Retained Earnings was $823,000 on January 1.

• Hudson Company paid $43,000 in cash dividends during the year.

Compute the balance of Retained Earnings on December 31.

129. The income statement for Dobson Corporation reported net income of $22,400 for the year ended December 31

before considering the following:

• During the year, the company purchased available-for-sale securities.

• At year-end, the fair value of the investment portfolio was $2,100 more than cost.

• The balance of Retained Earnings was $83,000 on January 1.

• Dobson Corporation paid $9,000 in cash dividends during the year.

Compute the balance of Retained Earnings on December 31.

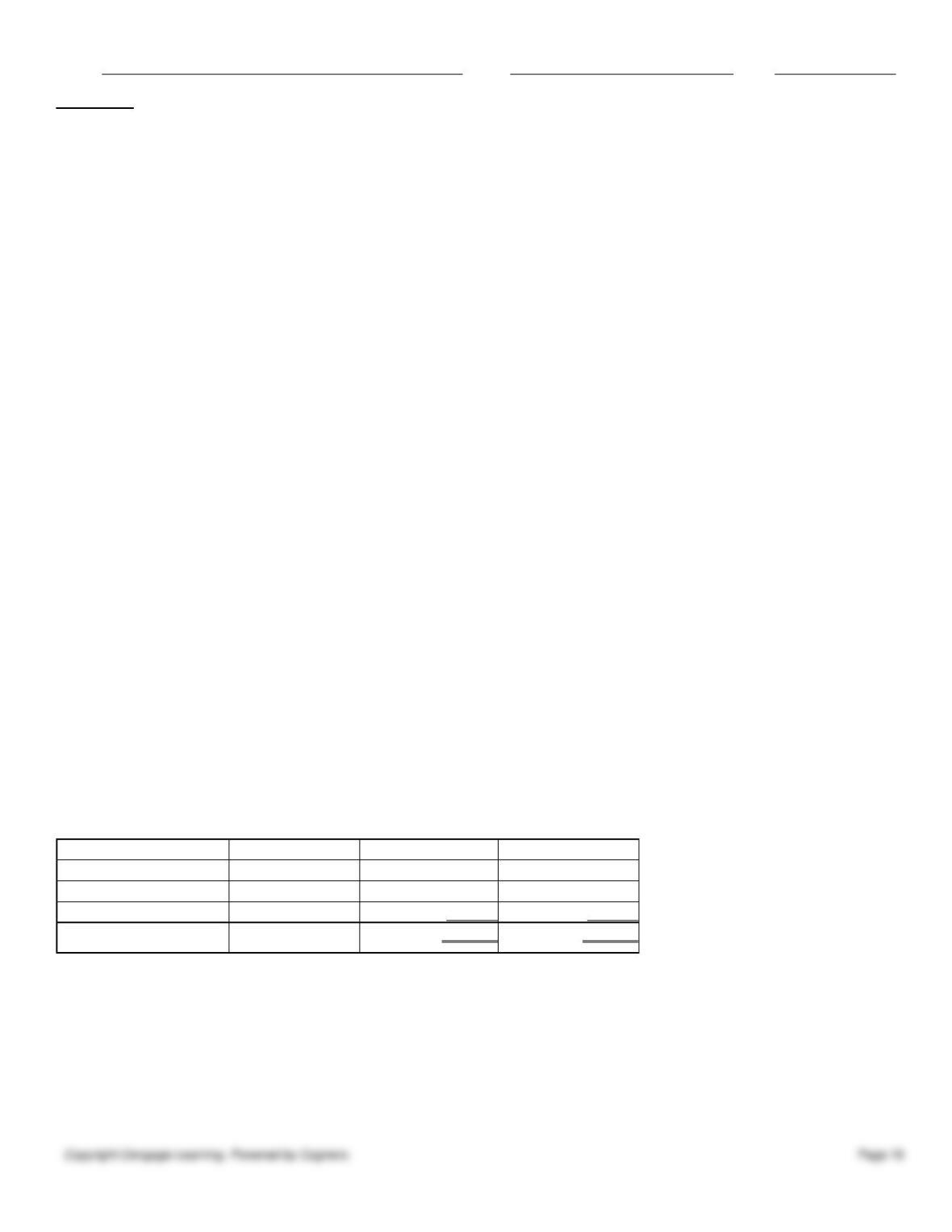

130. Skyline, Inc., purchased a portfolio of trading securities during the current fiscal year. The cost and fair value of this

portfolio on December 31 were as follows:

Issuing Company

Total Cost

Total Fair Value

Alcon, Inc.

$16,000

$15,000

Easton Company

23,000

21,500

Panther Company

9,000

9,200

Total

$48,000

$45,700

a. Journalize the adjusting entry for the fair value of the trading securities on December 31.

b. Where will the information from the journal entry be reported on the financial statements?

131. Journalize the entries for the following selected bond investment transactions for Southwest Bank:

Apr. 1 Purchased $400,000 of Daytona Beach 4.5% bonds at 100 plus accrued interest of $4,500.

July 1 Received the first semiannual interest payment.

Sept. 1 Sold $250,000 of the bonds at 97, plus accrued interest of $1,875.

132. Journalize the entries for the following selected equity investment transactions completed by Flurry Company during

the current year. Flurry’s purchase represents less than 20% of the total outstanding Braxter Co. stock.

Feb. 2

Purchased for cash 500 shares of Braxter Co. stock for $34 per

share plus a $250 brokerage commission.

Apr. 16

Received dividends of $0.35 per share on Braxter Co. stock.

June 17

Sold 100 shares of Braxter Co. stock for $40 per share less a $100

brokerage commission.

133. On May 1, Cedar Inc. purchases $100,000 of 10-year, Madison Corporation 6% bonds dated March 1 at 100 plus

accrued interest. Journalize the entry for the semiannual receipt of interest on September 1.

134. On September 1, Year 1, Parsons Company purchased $84,000 of 10-year, 7% government bonds at 100 plus

accrued interest. The semiannual interest payment dates are June 30 and December 31. Interest computations are done by

Name:

Class:

Date:

chapter 15

the month.

a. Journalize the entry for the bond purchase.

b. Journalize the receipt of interest on December 31 of the first year.

c. Journalize the sale of the bonds on February 1 of the second year for $82,000 plus accrued interest.

135. Ramiro Company purchased 40% of the outstanding stock of Marco Company on January 1. Marco reported net

income of $95,000 and declared dividends of $35,000 during the year. How much would Ramiro adjust its investment in

Marco Company under the equity method?

136. (a) What is comprehensive income? (b) How is it computed? (c) What are some examples of items included in other

comprehensive income? (d) Where is comprehensive income reported?

137. Herberto Company had a net income of $74,000 and other comprehensive loss of $8,500 for the year. On January 1,

the retained earnings balance was $425,000, and the accumulated other comprehensive income balance was

$52,000. Determine the (a) comprehensive income for the year, (b) the retained earnings balance on December 31, and (c)

the accumulated other comprehensive income on December 31.

138. Discuss the appropriate financial treatment when an investor has a greater than 50% ownership in another company.

139. On August 1, Year 1, Bee Company purchased $1,500,000 of Ant Company 10-year, 6% bonds, dated July 1, at 100

plus accrued interest. On March 1, Year 2, Bee sold half of the bonds for $782,500 plus accrued interest. Journalize the

following transactions:

a.

Purchase of bonds on August 1, Year 1.

b.

Receipt of first semiannual interest payment on December 31, Year 1.

c.

The sale of the bonds on March 1, Year 2.

140. On February 12, Addison, Inc., purchased 6,000 shares of Lucas Company at $22 per share plus a $240 brokerage

fee. This purchase represents less than 20% ownership of Lucas Company. On August 22, Lucas paid a dividend per share

of $0.42. On November 10, 4,000 shares of Lucas stock were sold for $28 per share less a $160 brokerage fee.

Journalize the entries for the original purchase, dividend, and sale.

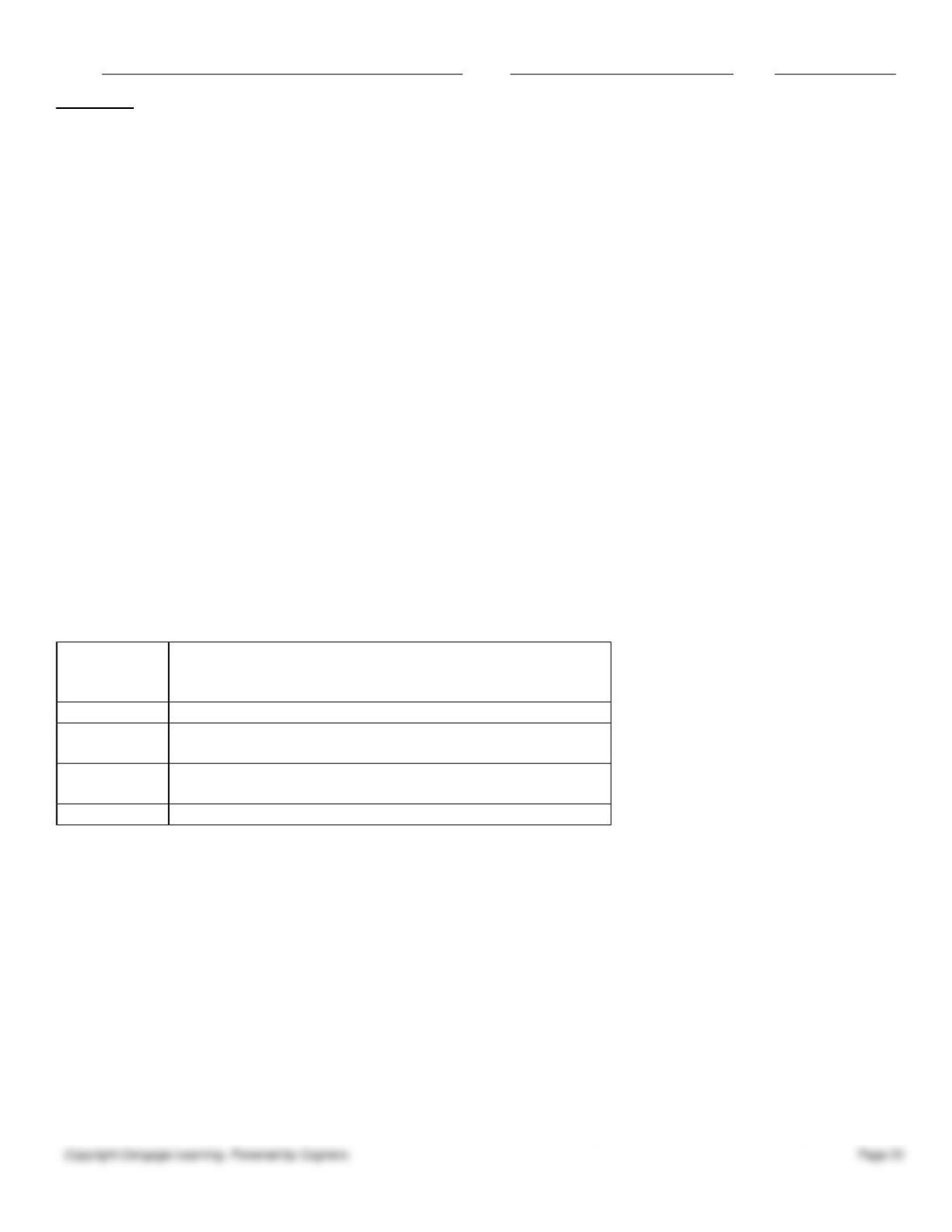

141. Skyline, Inc., purchased a portfolio of available-for-sale securities during the current fiscal year. The cost and fair

value of this portfolio on December 31 were as follows:

Issuing Company

Cost

Fair Value

Blackstone, Inc.

$ 4,000

$ 5,200

Flagler Company

3,000

2,700

Patterson Corporation

7,500

9,800

Total

$14,500

$17,700

a. Journalize the adjusting entry for the fair value of the portfolio of securities on December 31.

b. Where will the information from the journal entry be reported on the financial statements?

142. On March 1, Year 1, Chase Inc. purchases 35% of the outstanding shares of Glory Corporation stock for

$325,000. On December 31, Year 1, Glory reports net income of $162,000. On January 15, Year 2, Glory pays total

dividends to stockholders of $33,000.

Journalize the three transactions.

Name:

Class:

Date:

chapter 15

143. Journalize the entries for the following selected transactions of Oliver Co.:

May 1

Purchased $100,000 of Kruse Co. 6% bonds at their face amount plus accrued interest of $2,000.

July 1

Received first semiannual interest payment.

Sept. 1

Sold the bonds at 97 plus accrued interest of $1,000.

144. On May 1, Cedar Inc. purchases $150,000 of 10-year, Knox Corporation 8% bonds dated March 1 at 100 plus

accrued interest. Journalize the entry for the semiannual receipt of interest on March 1, Year 2.

145. Journalize the following selected transactions of Masterson Co.:

Aug. 1

Purchased 600 shares of the 100,000 shares outstanding of $10 par common shares of Dankin Corporation

for $5,100.

1

Purchased 3,500 of the 10,000 outstanding common shares of Ramon Co. for $45,700. The investment

was accounted for by the equity method.

Sept. 1

Received a cash dividend of $1 per share on the Dankin Corporation stock acquired on August 1.

1

Received a cash dividend of $2 per share on the Ramon Co. stock acquired on August 1.

Dec. 31

Sold 100 shares of the Dankin Corporation shares acquired on August 1 for $2,100.

31

Dankin Corporation reported net income of $30,000 and Ramon Company’s reported net income was $50,000.

146. On October 1, Marcus Corporation purchased $20,000 of 6% bonds of Roberts Corporation due in 8½ years. The

bonds were purchased at their face amount plus interest of $400 accrued from July 1, the date of the last semiannual

interest payment. Journalize the purchase.

147. On January 2, Todd Company acquired 40% of the outstanding stock of McGuire Company for $205,000. For the

year ending December 31, McGuire earned income of $48,000 and paid dividends of $14,000.

Journalize the entries for Todd Company for the purchase of the stock, share of McGuire Company income, and dividends

received from McGuire Company.

148. Nicer Corporation reported net income of $50,000 in the current year. There are 10,000 shares of $100 par, 6%

preferred stock and 50,000 shares of $2 par common stock outstanding. During the year, Nicer paid the preferred

stockholders a $6-per-share dividend and also paid $30,000 to common shareholders. The market value of Nicer’s

preferred stock is $95, and of Nicer’s common stock, $5.

a. Compute the dividend yield for Nicer Corporation.

b. Why does the dividend yield vary widely across firms?

149. Discuss why companies invest cash in short-term temporary investments versus long-term investments.

150. Gerardo Company had a net income of $75,000 and other comprehensive income of $12,500 for the year. On January

1, the retained earnings balance was $525,000 and the accumulated other comprehensive income balance was

$55,000. Determine the (a) comprehensive income for the year, (b) the retained earnings balance on December 31, and (c)

the accumulated other comprehensive income on December 31.

151. On January 1, the valuation allowance for trading investments account has a zero balance. On December 31, the cost

of trading securities portfolio was $64,200, and the fair value was $67,000.

Prepare the December 31 adjusting journal entry for the unrealized gain or loss on trading investments.

152. Pepito Company purchased 40% of the outstanding stock of Reyes Company on January 1. Reyes reported net

income of $75,000 and declared dividends of $15,000 during the year. How much would Pepito adjust its investment in

Reyes Company under the equity method?

Name:

Class:

Date:

chapter 15

153. On April 1, ValueTime, Inc., had a market price per common share of $24.00. For the previous year, ValueTime paid

a dividend of $1.50 per share. Compute the dividend yield for ValueTime, Inc.

154. On May 1, Knox Inc. purchases $100,000 of 10-year, 6% Madison Corporation bonds dated March 1 at 100 plus

accrued interest. Journalize the entry for the bond purchase.

155. Journalize the following transactions for Morgan Co.:

July 1

Morgan Co. purchased 32,000 of 100,000 outstanding shares of Gordon Corp. stock for $10 per share

plus a $400 commission.

Dec. 31

Gordon Corp.’s total earnings for the period are $80,000.

31

Gordon Corp. paid a total of $45,000 in cash dividends.

156. Journalize the following transactions for Batson Co.:

Sept. 1

Batson Co. purchased 1,200 of the 100,000 outstanding shares of Michael Corp. stock for $20.75 per

share plus a $70 commission.

Dec. 31

Michael Corp.’s total earnings for the period are $84,000.

31

Michael Corp. paid a total of $40,000 in cash dividends to shareholders of record.

157. Discuss the similarities and differences in reporting trading securities, available-for-sale securities, and held-to–

maturity securities.

158. Journalize the entries for the following selected equity investment transactions completed by Perry Company during

the current year. Perry accounts for the Dexter Co. investment using the fair value method.

Feb. 2

Purchased for cash 900 shares of Dexter Co. stock for $54 per

share plus a $450 brokerage commission. This represents a less

than 10% ownership interest in the company.

Apr. 16

Received dividends of $0.25 per share on Dexter Co. stock.

June 17

Sold 200 shares of Dexter Co. stock for $70 per share less a

$500 brokerage commission.

Aug. 19

Purchased 600 shares of Dexter Co. stock for $65 per share plus

a $300 brokerage commission.

Nov. 14

Received dividends of $0.30 per share on Dexter Co. stock.

159. Albright Company purchased as a long-term investment $500,000 of Benton Corporation 10-year, 9%

bonds. Journalize the following selected transactions:

Mar. 1

Purchased bonds at their face amount for $500,000.

May 1

Sold half the bonds at 98 plus accrued interest of $3,750. The broker deducted $200 for brokerage fees

and taxes, remitting the balance.

160. On January 1, the valuation allowance for available-for-sale investments account had a zero balance. On December

31, the cost of the available-for-sale securities was $48,700, and the fair value was $39,200. Journalize the adjusting entry

for the unrealized gain or loss for available-for-sale investments on December 31.

161. Define debt securities and equity securities. Include their similarities and differences in your discussion.

162. Sutton Company purchased 10% of the outstanding stock of Roberts Company on January 1. Roberts reported net

Name:

Class:

Date:

chapter 15

income of $155,000 and declared dividends of $40,000 during the year. How would these events be reported by Sutton

using the fair value method?

Name:

Class:

Date:

chapter 15

Answer Key

Name:

Class:

Date:

chapter 15

Name:

Class:

Date:

chapter 15

Name:

Class:

Date:

chapter 15

Name:

Class:

Date:

chapter 15

Name:

Class:

Date:

chapter 15

Name:

Class:

Date:

chapter 15

Name:

Class:

Date:

chapter 15

Name:

Class:

Date:

chapter 15

Name:

Class:

Date:

chapter 15

Name:

Class:

Date:

chapter 15

Name:

Class:

Date:

chapter 15