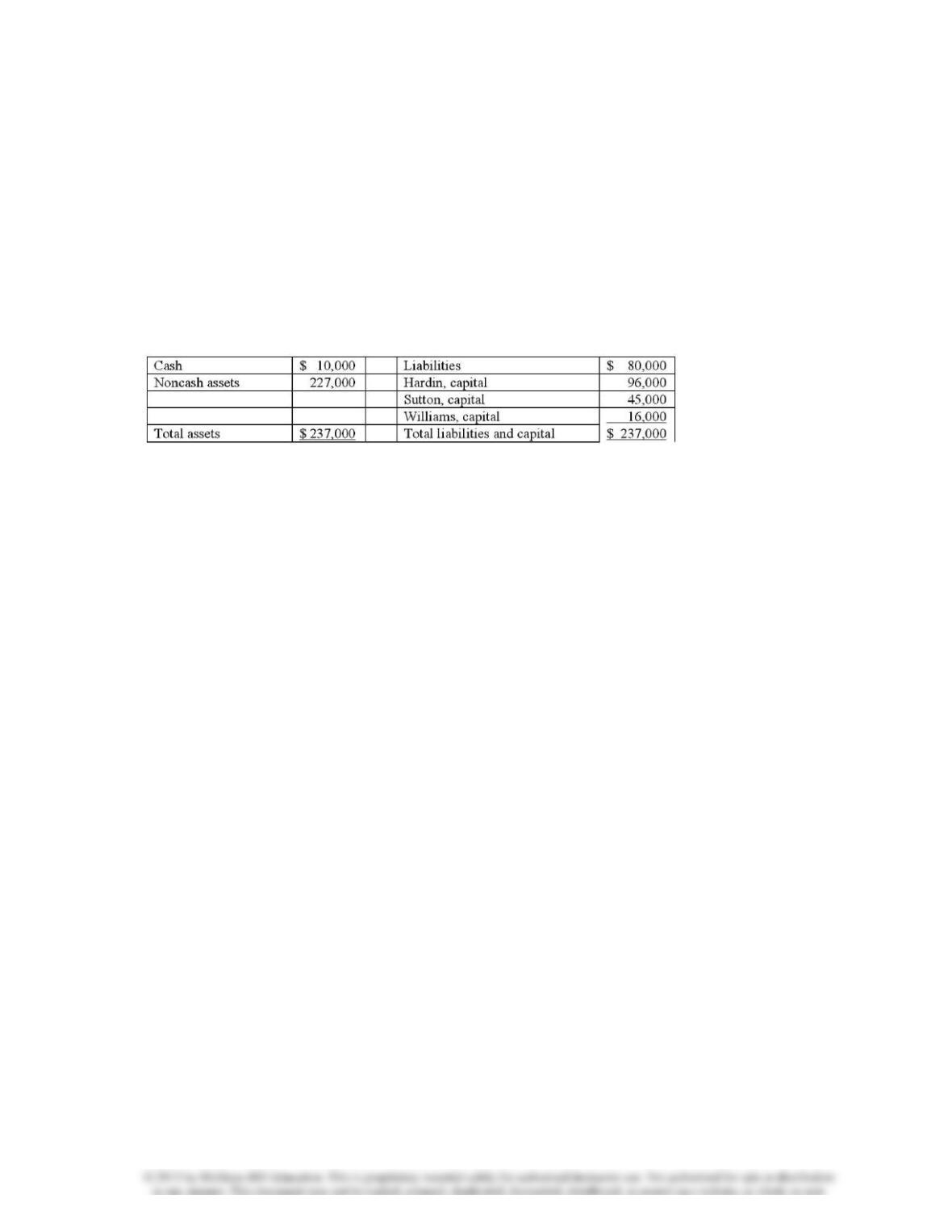

58. Hardin, Sutton, and Williams have operated a local business as a

partnership for several years. All profits and losses have been allocated in a 3:2:1

ratio, respectively. Recently, Williams has undergone personal financial

problems, and is insolvent. To satisfy Williams’ creditors, the partnership has

decided to liquidate.

The following balance sheet has been produced:

During the liquidation process, the following transactions take place:

– Noncash assets are sold for $116,000.

– Liquidation expenses of $12,000 are paid. No further expenses are expected.

– Safe capital distributions are made to the partners.

– Payment is made of all business liabilities.

– Any deficit capital balances are deemed to be uncollectible.

Develop a predistribution plan for this partnership, assuming $12,000 of

liquidation expenses are expected to be paid.

59. Hardin, Sutton, and Williams have operated a local business as a

partnership for several years. All profits and losses have been allocated in a 3:2:1

ratio, respectively. Recently, Williams has undergone personal financial

problems, and is insolvent. To satisfy Williams’ creditors, the partnership has

decided to liquidate.

The following balance sheet has been produced:

During the liquidation process, the following transactions take place:

60. Hardin, Sutton, and Williams have operated a local business as a

partnership for several years. All profits and losses have been allocated in a 3:2:1

ratio, respectively. Recently, Williams has undergone personal financial

problems, and is insolvent. To satisfy Williams’ creditors, the partnership has

decided to liquidate.

The following balance sheet has been produced:

During the liquidation process, the following transactions take place:

61. Jones, Marge, and Tate LLP decided to dissolve and liquidate the

partnership on September 30, 2011. After realization of a portion of the noncash

assets, the capital account balances were Jones $50,000; Marge $40,000; and

Tate $15,000. Cash of $35,000 and other assets with a carrying amount of

$100,000 were on hand. Creditors’ claims totaled $30,000. Jones, Marge, and

Tate shared net income and losses in a 2:1:1 ratio, respectively.

Prepare a working paper to compute the amount of cash that may be paid to

creditors and to partners at this time, assuming that no partner is solvent.

62. The balance sheet of Rogers, Dennis & Berry LLP prior to liquidation

included the following:

63. The balance sheet of Rogers, Dennis & Berry LLP prior to liquidation

included the following:

64. The balance sheet of Rogers, Dennis & Berry LLP prior to liquidation

included the following:

65. The balance sheet of Rogers, Dennis & Berry LLP prior to liquidation

included the following:

66. The partners of Donald, Chief & Berry LLP decided to liquidate on August

1, 2011. The balance sheet of the partnership is as follows, with the profit and

loss ratio of 25%, 45%, and 30%, respectively.

67. The partners of Donald, Chief & Berry LLP decided to liquidate on August

1, 2011. The balance sheet of the partnership is as follows, with the profit and

loss ratio of 25%, 45%, and 30%, respectively.

68. The partners of Donald, Chief & Berry LLP decided to liquidate on August

1, 2011. The balance sheet of the partnership is as follows, with the profit and

loss ratio of 25%, 45%, and 30%, respectively.

69. The partners of Donald, Chief & Berry LLP decided to liquidate on August

1, 2011. The balance sheet of the partnership is as follows, with the profit and

loss ratio of 25%, 45%, and 30%, respectively.

70. Matching

1. The schedule of liquidation A schedule should be

produced periodically by the accountant to disclose losses and gains that have

2. Safe capital balances One or more partners

may have a negative capital balance often as a result of losses incurred in

3. Deficit capital balances A provision for an

4. Predistribution plan At the start of a

liquidation, this document provides guidance for all payments made to the