Chapter 14: Performance Evaluation for Decentralized Operations

The following financial information was summarized from the accounting records of Globe

Corporation for the current year ended December 31:

Northern

Southern

Corporate

Division

Division

Total

Cost of goods sold

$310,000

$175,000

Direct operating expenses

250,000

115,000

Net sales

600,000

410,000

Interest expense

$ 12,000

General overhead

101,000

Income tax

26,700

90. The gross profit for the Southern Division is:

a. $150,000.

b. $295,000.

c. $235,000.

d. $120,000.

91. The income from operations for the Southern Division is:

a. $150,000.

b. $120,000.

c. $295,000.

d. $154,400.

92. The net income for Globe Corporation is:

a. $59,000.

b. $160,000.

c. $19,400.

d. $47,000.

93. How do the responsibilities of a manager in an investment center compare to the

responsibilities of managers in a cost or profit center?

a. Investment center managers have more authority and responsibility than managers of a cost

or profit center.

b. Investment center managers have more authority and responsibility than managers of a cost

center but less than managers of a profit center.

c. Investment center managers have about the same authority and responsibility as managers

of a cost or profit center.

d. Investment center managers have more authority and responsibility than managers of a

profit center but less than managers of a cost center.

Chapter 14: Performance Evaluation for Decentralized Operations

94. Plamba Corporation had $250,000 invested in assets, sales of $490,000, income from

operations amounting to $70,000, and a desired minimum rate of return of 15%. The rate of

return on investment for Plamba is:

a. 14%.

b. 28%.

c. 20%.

d. 15%.

95. Blancher Corporation had $495,000 in invested assets, sales of $660,000, income from

operations amounting to $99,000, and a desired minimum rate of return of 15%. The profit

margin for Blancher is:

a. 16%.

b. 20%.

c. 18%.

d. 15%.

96. Blancher Corporation had $495,000 in invested assets, sales of $660,000, income from

operations amounting to $99,000, and a desired minimum rate of return of 15%. The

investment turnover for Blancher is:

a. 1.20.

b. 1.00.

c. 1.10.

d. 1.33.

97. Plamba Corporation had $250,000 in invested assets, sales of $490,000, income from

operations amounting to $70,000, and a desired minimum rate of return of 15%. The residual

income for Plamba is:

a. $32,500.

b. $10,500.

c. $59,500.

d. $37,500.

98. In an investment center, the manager has the responsibility for and the authority to make

decisions that affect:

a. the assets invested in the center but not costs and revenues.

b. costs and assets invested in the center but not revenues.

c. both costs and revenues for the department or division.

d. not only costs and revenues but also assets invested in the center.

Chapter 14: Performance Evaluation for Decentralized Operations

99. Espinosa Corporation had $220,000 invested in assets, sales of $242,000, income from

operations amounting to $48,400, and a desired minimum rate of return of 3%. The rate of

return on investment for Espinosa is:

a. 20%.

b. 22%.

c. 3%.

d. 6.4%.

100. The profit margin for Division E is 28% and the investment turnover is 3.0. What is the rate of

return on investment for Division E?

a. 84%

b. 28%

c. 14%

d. 9%

101. Division M for Movism Company has a rate of return on investment of 20% and an investment

turnover of 1.5. What is the profit margin?

a. 20%

b. 13%

c. 15%

d. 30%

102. Division A of Purvis Company has a rate of return on investment of 15% and an investment

turnover of 1.6. What is the profit margin?

a. 10%

b. 12.5%

c. 9.4%

d. 24%

103. In an investment center, the manager has responsibility and authority for making decisions that

affect:

a. only costs.

b. both costs and revenues.

c. only assets.

d. costs, revenues, and assets.

Chapter 14: Performance Evaluation for Decentralized Operations

104. The profit margin for Division J is 12% and the investment turnover is 1.40. What is the rate

of return on investment for Division J?

a. 16.8%

b. 8.6%

c. 12.0%

d. 9.6%

105. The balanced scorecard measures:

a. only financial information.

b. only nonfinancial information.

c. both financial and nonfinancial information.

d. both external and internal information.

106. The profit margin is the ratio of:

a. income from operations to sales.

b. income from operations to invested assets.

c. assets to liabilities.

d. sales to invested assets.

107. The investment turnover is the ratio of:

a. income from operations to sales.

b. income from operations to invested assets.

c. assets to liabilities.

d. sales to invested assets.

108. Identify the formula for the rate of return on investment.

a. Invested Assets/Income From Operations

b. Sales/Invested Assets

c. Income From Operations/Sales

d. Income From Operations/Invested Assets

Chapter 14: Performance Evaluation for Decentralized Operations

109. Which of the following expressions is termed the profit margin factor as used in determining

the rate of return on investment?

a. Sales/Income From Operations

b. Income From Operations/Sales

c. Invested Assets/Sales

d. Sales/Invested Assets

110. Which of the following expressions is termed the investment turnover factor as used in

determining the rate of return on investment?

a. Invested Assets/Sales

b. Income From Operations/Invested Assets

c. Income From Operations/Sales

d. Sales/Invested Assets

111. Division M of Tenist Company has a rate of return on investment of 20% and a profit margin

of 13%. What is the investment turnover?

a. 3.6

b. 1.5

c. 5.0

d. .7

112. What additional information is needed to find the rate of return on investment if income from

operations is known?

a. Invested assets

b. Residual income

c. Direct expenses

d. Sales

113. The best measure of managerial efficiency in the use of investments in assets is:

a. rate of return on stockholders’ equity.

b. rate of return on investment.

c. income from operations.

d. inventory turnover.

Chapter 14: Performance Evaluation for Decentralized Operations

114. Two divisions of Crowson Company (Divisions X and Y) have the same profit margins.

Division X’s investment turnover is larger than that of Division Y (1.2 to 1.0). Which of the

following statements is true?

a. Division Y will have a higher return on investment as it is using its assets more efficiently

in generating sales.

b. Division X will have a higher return on investment as it is generating more income from its

operations.

c. Division X will have a higher return on investment as it is using its assets more efficiently

in generating sales.

d. Division Y will have a higher return on investment as it is generating more income from its

operations.

115. The excess of divisional income from operations over a minimum acceptable divisional

income from operations is termed:

a. profit margin.

b. residual income.

c. rate of return on investment.

d. gross profit.

116. Assume that divisional income from operations amounts to $325,000 and top management has

established 10% as the minimum rate of return on divisional assets totaling $1,250,000. The

residual income for the division is:

a. $200,000.

b. $292,500.

c. $125,000.

d. $0.

117. Which one of the following is not a measure that management can use in evaluating and

controlling investment center performance?

a. Rate of return on investment

b. Negotiated price

c. Residual income

d. Income from operations

Chapter 14: Performance Evaluation for Decentralized Operations

118. Assume that Division A has generated sales revenue of $4,550,000 and achieved income from

operations of $530,000 using $2,800,000 of invested assets. If management desires a minimum

rate of return of 15%, the residual income would be:

a. $110,000.

b. $152,500.

c. $79,500.

d. $530,000.

119. Assume that Division X has generated sales revenue of $3,025,000 and achieved income from

operations of $242,000 using $1,800,000 of invested assets. If management desires a minimum

rate of return of 12%, the profit margin would be:

a. 59.5%.

b. 13.4%.

c. 12%.

d. 8%.

120. A common balanced scorecard measures performance in all of the following areas except:

a. education.

b. internal process.

c. financial.

d. innovation and learning.

121. Which component of the balanced scorecard evaluates the economic performance of the

responsibility centers?

a. Internal process

b. Financial

c. Innovation and learning

d. Customer

122. Which of the following is true of the balanced scorecard?

a. It ignores the financial performance of the company.

b. It has the ability to reveal the underlying nonfinancial drivers of financial performance.

c. It aims to improve the nonfinancial performance of the business.

d. It focuses primarily on the short term performance of the business.

Chapter 14: Performance Evaluation for Decentralized Operations

123. Which of the following is not a approach used for setting transfer prices?

a. Market price approach

b. Revenue price approach

c. Negotiated price approach

d. Cost price approach

124. How much would Division A’s income from operations increase?

a. $175,000

b. $70,000

c. $105,000

d. $75,000

125. How much would Division B’s income from operations increase?

a. $75,000

b. $175,000

c. $105,000

d. $70,000

126. How much would Meeta-Products total income from operations increase?

a. $70,000

b. $175,000

c. $105,000

d. $100,000

Chapter 14: Performance Evaluation for Decentralized Operations

Materials used by Boone Company in producing Division C’s product are currently purchased

from outside suppliers at a cost of $20 per unit. However, the same materials are available

from Division A. Division A has unused capacity and can produce the materials needed by

Division C at a variable cost of $17 per unit. A transfer price of $19 per unit is negotiated and

60,000 units of material are transferred, with no reduction in Division A’s current sales.

127. How much would Division C’s income from operations increase?

a. $0

b. $180,000

c. $60,000

d. $120,000

128. How much would Division A’s income from operations increase?

a. $0

b. $180,000

c. $60,000

d. $120,000

129. How much would Boone’s total income from operations increase?

a. $180,000

b. $240,000

c. $120,000

d. $300,000

130. Which transfer price approach is used when the transfer price is set at the amount sold to

outside buyers?

a. Market price

b. Cost price

c. Negotiated price

d. Variable price

Chapter 14: Performance Evaluation for Decentralized Operations

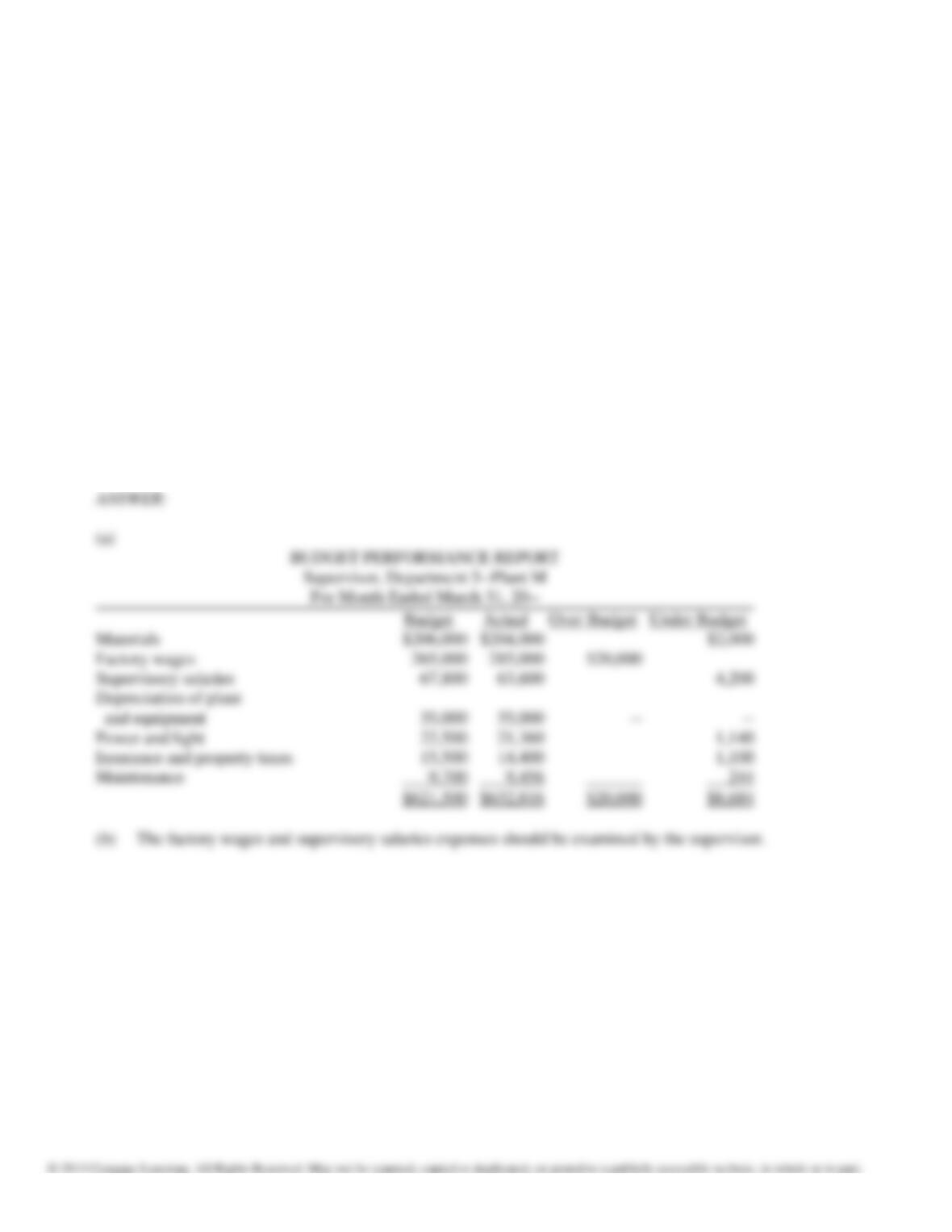

131. The budget for Department 5 of Plant M for the current month ending March 31 is as follows:

Materials

$206,000

Factory wages

265,000

Supervisory salaries

67,800

Depreciation of plant and equipment

35,000

Power and light

22,500

Insurance and property taxes

15,500

Maintenance

9,700

During March, the costs incurred in Department 5 of Plant M were materials, $204,000;

factory wages, $285,000; supervisory salaries, $63,600; depreciation of plant and equipment,

$35,000; power and light, $21,360; insurance and property taxes, $14,400; maintenance,

$9,456.

(a)

Prepare a budget performance report for the supervisor of Department 5 of Plant M for the

month of March.

(b)

Are there any significant variances (greater than 5%) of the budgeted amounts that should

be examined by the supervisor?

Factory wages

Depreciation of plant

and equipment

Insurance and property taxes

$621,500

$632,816

(b)

The factory wages and supervisory salaries expenses should be examined by the supervisor.

Chapter 14: Performance Evaluation for Decentralized Operations

132. A department store apportions payroll costs on the basis of the number of payroll checks

issued. Accounting costs are apportioned on the basis of the number of reports. The payroll

costs for the year were $100,000, and the accounting costs for the year totaled $50,000. The

number of payroll checks issued and the number of reports for each department are as follows:

Number of

Number

Payroll Checks

of Reports

Department R

300

45

Department S

850

80

Department T

100

125

Determine the amount of (a) payroll cost and (b) accounting cost to be apportioned to each

department.

133. A portion of the divisional income statement for the year just ended is presented below in a

condensed form.

Department F

Net sales

$93,800

Cost of goods sold

72,400

Gross profit

$21,400

Operating expenses

28,900

Loss from operations

$ (7,500)

The operating expenses of Department F include $16,000 for direct expenses.

It is estimated that the discontinuance of Department F would not have affected the sales of the

other departments nor have reduced the indirect expenses of the business. Assuming the

accuracy of these estimates, determine the effect (increase or decrease and the amount) on the

income from operations of the business if Department F had been discontinued.

Chapter 14: Performance Evaluation for Decentralized Operations

134. PDT Co. has two divisions, East and West. Invested assets and condensed income statement

data for each division for the past year ended December 31 are as follows:

East Division

West Division

Revenues

$1,200,000

$800,000

Operating expenses

950,000

640,000

Service department charges

145,000

72,000

Invested assets

800,000

500,000

(a) Prepare condensed income statements for the past year for each division.

(b) Using the expanded expression, determine the profit margin, investment turnover, and

rate of return on investment for each division. Round to one decimal place.

Chapter 14: Performance Evaluation for Decentralized Operations

135. The sales, income from operations, and invested assets for each division of Garner Company

are as follows:

Income from

Invested

Sales

Operations

Assets

Division E

$3,000,000

$470,000

$2,500,000

Division F

3,600,000

430,000

2,400,000

Division G

6,000,000

560,000

3,000,000

(a)

Using the expanded expression, determine the profit margin, investment turnover, and

rate of return on investment for each division. Round to one decimal place.

(b)

Which division is (are) the most profitable as per dollar invested?

(a)

Rate of Return on Investment:

$3,000,000

$3,000,000

$3,600,000

$6,000,000

(b)

Divisions E and G are almost equally profitable.

Chapter 14: Performance Evaluation for Decentralized Operations

136. The sales, income from operations, and invested assets for each division of Salem Company

are as follows:

Income from

Invested

Sales

Operations

Assets

Division C

$4,000,000

$410,000

$3,500,000

Division D

3,500,000

600,000

4,000,000

Division E

2,250,000

780,000

7,000,000

Management has established a minimum rate of return for invested assets of 11%.

(a) Determine the residual income for each division.

(b) Based on residual income, which division is the most profitable?

Residual income = $780,000 – (11% of $7,000,000)

= $780,000 – $770,000

= $10,000

137. Materials used by Ford Company in producing Division A’s product are currently purchased

from outside suppliers at a cost of $30 per unit. However, the same materials are available

from Division B. Division B has unused capacity and can produce the materials needed by

Division A at a variable cost of $20 per unit.

(a)

If a transfer price of $25 per unit is established and 60,000 units of material are

transferred with no reductions in Division B’s current sales, how much would Ford

Company’s total income from operations increase?

(b)

How much would the income from operations of Division A increase?

(c)

How much would the income from operations of Division B increase?

(d)

If the negotiated price approach is used, what would be the range of acceptable

transfer prices?