Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

63. What is the

dissolution

of a partnership?

64. By what methods can a person gain admittance to a partnership?

65. What events cause the

dissolution

of a partnership?

66. For what events or conditions should the Articles of Partnership make

provision?

The Articles of Partnership should be a comprehensive document that is fair to

all the partners. It should contain the following provisions:

67. How is accounting for a partnership different from accounting for a

corporation?

68. Why are the terms of the Articles of Partnership important to partners?

69. Brown and Green are forming a business as partners. If they do not create

a formal written partnership agreement, what risks are they exposing themselves

to?

70. What theoretical argument could be made against the recognition of

goodwill when there is a change in the ownership of a partnership?

71. Under what circumstances does a partner's balance in his or her capital

account have practical consequences for the partner?

72. Reed, Sharp, and Tucker were partners with capital account balances of

$80,000, $100,000, and $70,000, respectively. They agreed to admit Upton to the

partnership. Upton purchased 30% of each partner's interest, with payments

directly to Reed, Sharp, and Tucker of $32,000, $40,000, and $28,000,

respectively. Before the admission of Upton, the profit and loss sharing ratio was

2:3:2. The partners agreed to use the bonus method to account for the admission

of Upton to the partnership.

Required:

Prepare the journal entry to record the admission of Upton to the partnership.

73. Jipsom and Klark were partners with capital account balances of $80,000

and $100,000, respectively. Looney directly paid $32,000 to Jipsom and $40,000

to Klark for 30% of their interests in the partnership. Jipsom and Klark shared

income in the ratio of 2:3. They believed that revaluation of the partnership was

appropriate when a new partner was admitted.

Required:

Prepare the journal entries to record the admission of Looney to the partnership.

74. Norr and Caylor established a partnership on January 1, 2010. Norr

invested cash of $100,000 and Caylor invested $30,000 in cash and equipment

with a book value of $40,000 and fair value of $50,000. For both partners, the

beginning capital balance was to equal the initial investment. Norr and Caylor

agreed to the following procedure for sharing profits and losses:

- 12% interest on the yearly beginning capital balance

- $10 per hour of work that can be billed to the partnership's clients

- the remainder divided in a 3:2 ratio

The Articles of Partnership specified that each partner should withdraw no more

than $1,000 per month.

For 2010, the partnership's income was $70,000. Norr had 1,000 billable hours,

and Caylor worked 1,400 billable hours. In 2011, the partnership's income was

$24,000, and Norr and Caylor worked 800 and 1,200 billable hours respectively.

Each partner withdrew $1,000 per month throughout 2010 and 2011.

Determine the amount of net income allocated to each partner for 2010.

75. Norr and Caylor established a partnership on January 1, 2010. Norr

invested cash of $100,000 and Caylor invested $30,000 in cash and equipment

with a book value of $40,000 and fair value of $50,000. For both partners, the

beginning capital balance was to equal the initial investment. Norr and Caylor

agreed to the following procedure for sharing profits and losses:

- 12% interest on the yearly beginning capital balance

- $10 per hour of work that can be billed to the partnership's clients

- the remainder divided in a 3:2 ratio

76. Norr and Caylor established a partnership on January 1, 2010. Norr

invested cash of $100,000 and Caylor invested $30,000 in cash and equipment

with a book value of $40,000 and fair value of $50,000. For both partners, the

beginning capital balance was to equal the initial investment. Norr and Caylor

agreed to the following procedure for sharing profits and losses:

- 12% interest on the yearly beginning capital balance

- $10 per hour of work that can be billed to the partnership's clients

- the remainder divided in a 3:2 ratio

77. Determine the balance in both capital accounts at the end of 2011 to the

nearest dollar.

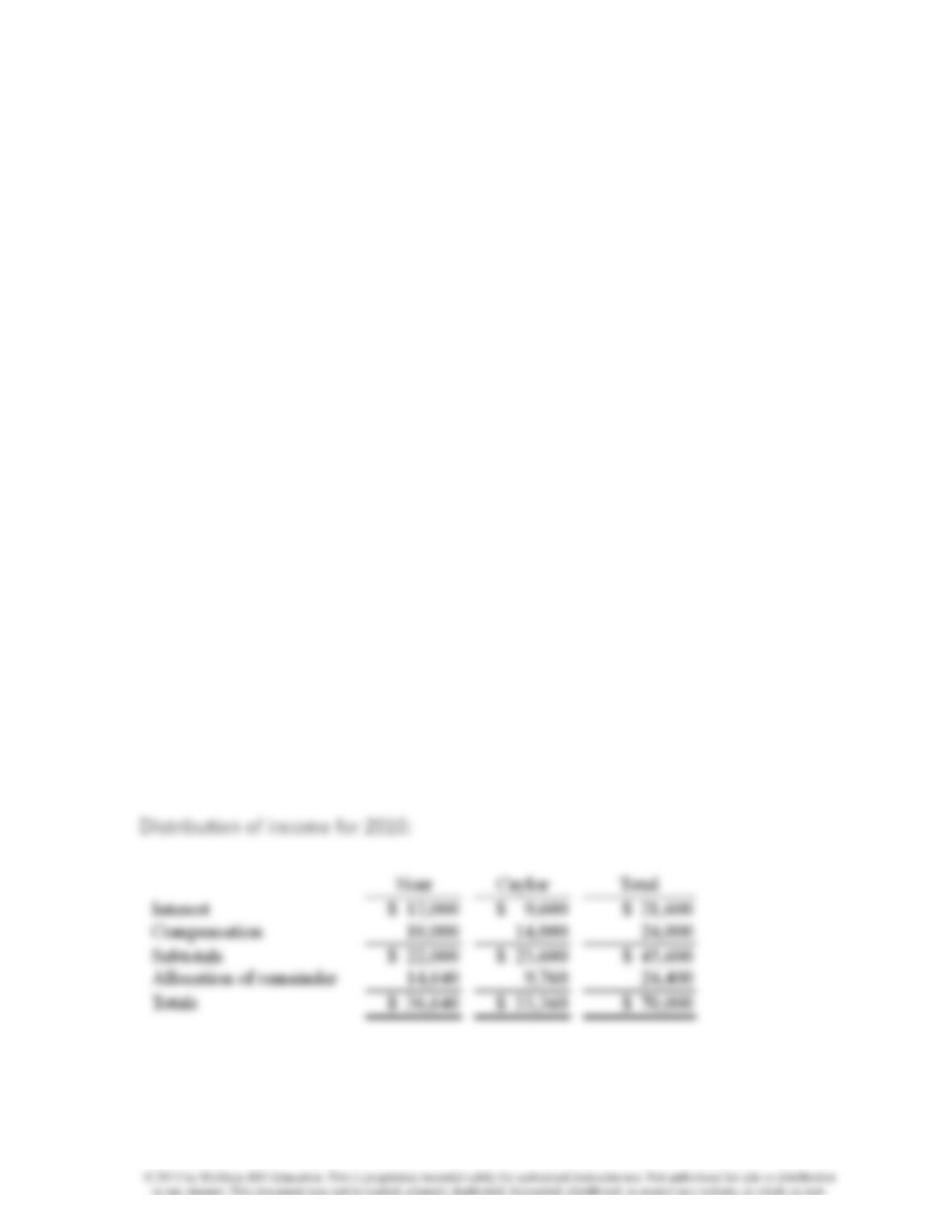

Capital account balances at the end of 2011:

78. The ABCD Partnership has the following balance sheet at January 1, 2010,

prior to the admission of new partner, Eden.