Accounting Information Systems, 12e (Romney/Steinbart)

Chapter 14 The Production Cycle

1) The AIS compiles and feeds information among the business cycles. What is the relationship between

the revenue and production cycles regarding the exchange of information?

A) The revenue cycle provides sales forecast and customer order information to the production cycle,

but the production cycle sends information back to revenue about finished goods production.

B) The revenue cycle receives information from the production cycle about raw materials needs.

C) The production cycle sends cost of goods manufactured information back to the revenue cycle.

D) The production cycle does not exchange information with the revenue cycle.

2) Which of the following is a key feature of materials requirements planning (MRP-II)?

A) Reducing required inventory levels by scheduling production, rather than estimating needs

B) Minimizing or eliminating carrying and stockout costs

C) Determining the optimal reorder points for all materials

D) Determining economic order quantity for all materials

3) The production cycle is different than the revenue and expenditure cycles for all the following reasons

except

A) there are no direct external data sources or destinations.

B) cost accounting is involved in all activities.

C) not all organizations have a production cycle.

D) very little technology exists to make activities more efficient.

4) An MRP inventory system reduces inventory levels by

A) reducing the uncertainty about when materials are needed.

B) computing exact costs of purchasing and carrying inventory.

C) delivering materials to the production floor exactly when needed and in exact quantities.

D) none of the above

5) Which of the following is not a product design objective?

A) Design a product that meets customer requirements.

B) Design a quality product.

C) Minimize production costs.

D) Make the design easy to track for cost accounting purposes.

6) The operations list shows

A) the labor and machine requirements.

B) the steps and operations in the production cycle.

C) the time expected to complete each step or operation.

D) all of the above

7) Push manufacturing is officially known as

A) manufacturing resource planning (MRP).

B) just-in-time manufacturing system (JIT).

C) the economic order quantity (EOQ) system.

D) ahead-of-time production implementation (ATPI).

8) Pull manufacturing is officially known as

A) manufacturing resource planning (MRP).

B) just-in-time manufacturing system (JIT).

C) the economic order quantity (EOQ) system.

D) ahead-of-time production implementation (ATPI).

9) What is the main difference between MRP-II and JIT manufacturing systems?

A) The length of the planning horizon.

B) JIT uses long-term customer demand for planning purposes, but MRP-II uses short-term customer

demand for planning purposes.

C) MRP-II relies on EDI, but JIT does not.

D) There are no significant differences between MRP-II and JIT.

10) A master production schedule is used to develop detailed

A) timetables of daily production and determine raw material needs.

B) reports on daily production and material usage.

C) daily reports on direct labor needs.

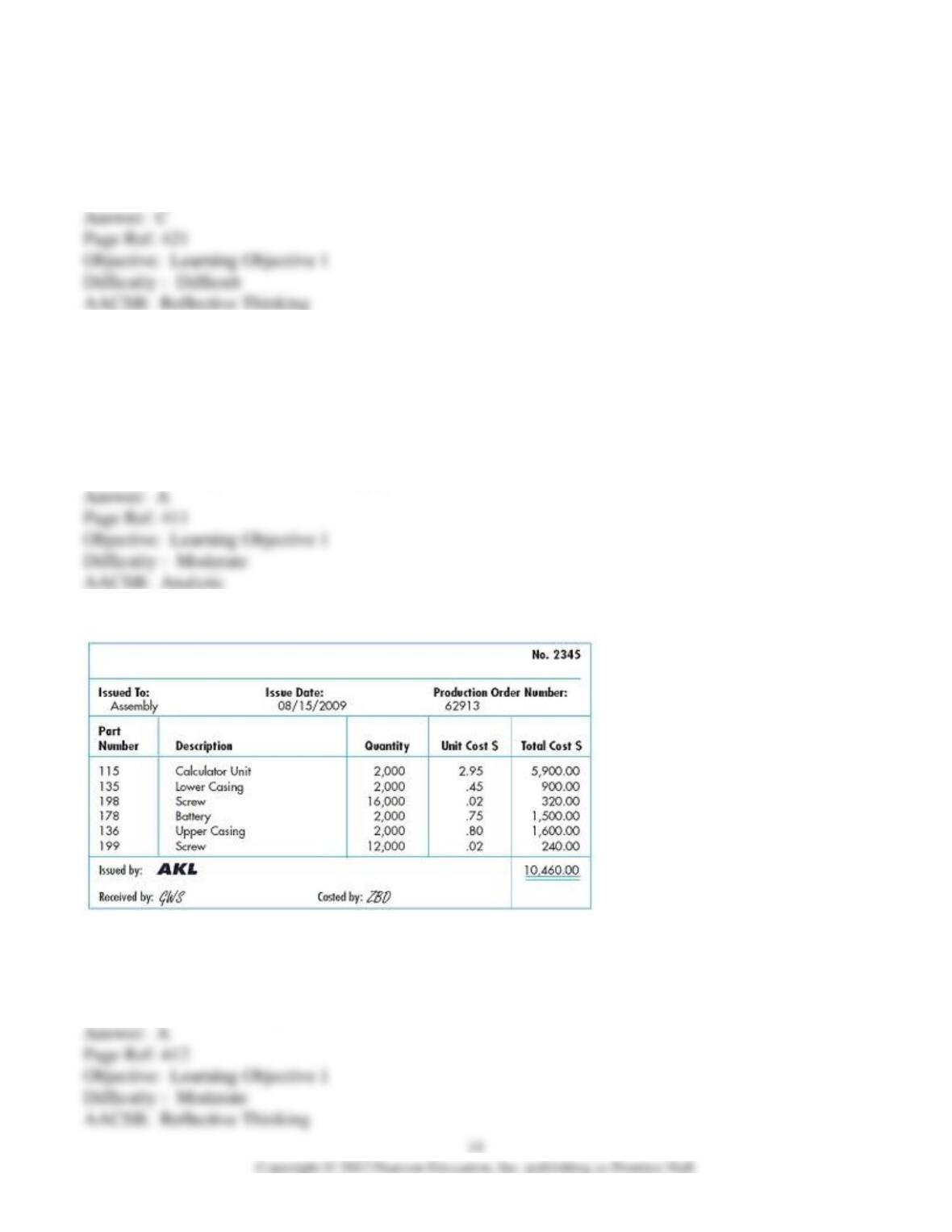

D) inventory charts.

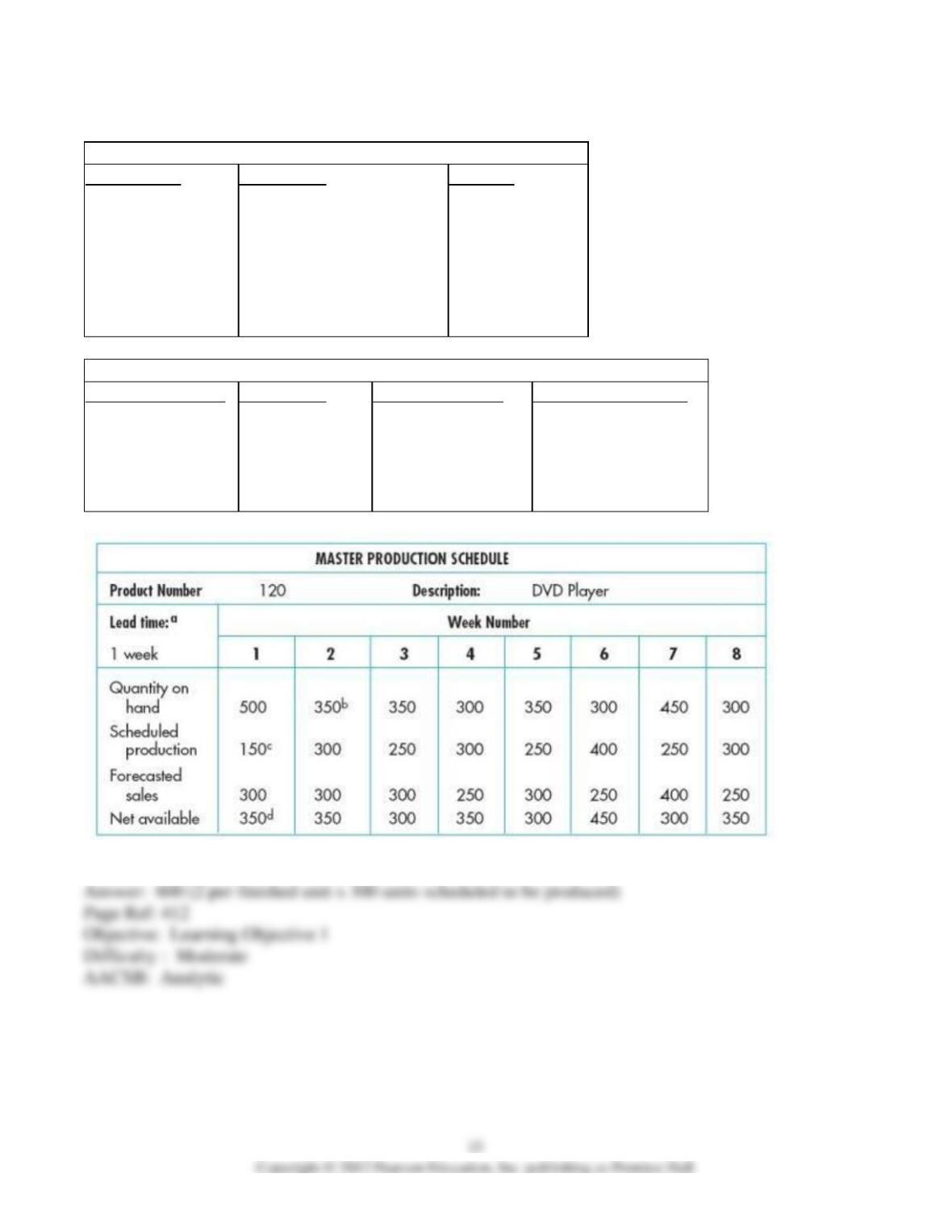

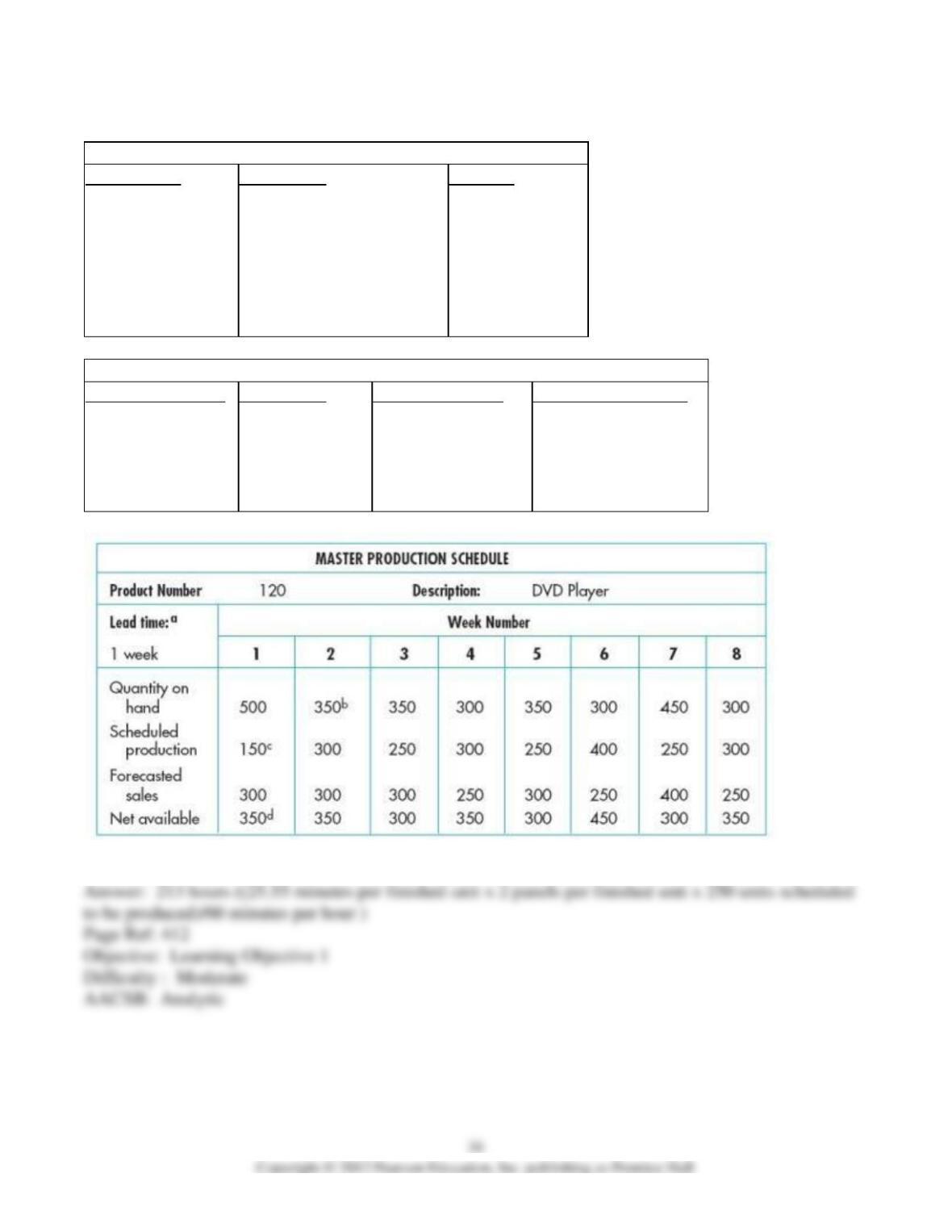

11) The production cycle document that specifies the quantity of each product to be produced and when

production should begin is the

A) bill of materials.

B) bill of lading.

C) master production schedule.

D) operations list.

12) What information is necessary to create the master production schedule?

A) engineering department specifications and inventory levels

B) engineering department specifications and sales forecasts

C) special orders information and engineering department specifications

D) sales forecasts, special orders information, and inventory levels

13) The document that authorizes the transfer of raw materials from the storeroom to the production

floor is referred to as

A) a bill of materials.

B) a production order.

C) a materials requisition.

D) a move ticket.

14) ______ is an efficient way to track and process information about raw materials used in production.

A) A just-in-time inventory system

B) Identifying materials with bar codes or RFID tags

C) A materials resources planning inventory system

D) Job-order costing

15) The use of various forms of information technology in the production process is referred to as

A) computerized investments and machines.

B) computerized integration of machines.

C) computer-integrated manufacturing.

D) computer intense manufacturing.

16) Using technology such as robots and computer-controlled machinery to shift from mass production

to custom order manufacturing is referred to as

A) computer integrated manufacturing (CIM).

B) lean manufacturing.

C) Six Sigma.

D) computer-aided design (CAD).

17) Which objective listed below is not a cost accounting objective for the production cycle?

A) provide information for planning, controlling, and evaluating the performance of production

operations

B) provide cost data about products used in pricing and product mix decisions

C) collect and process the information used to calculate inventory and cost of goods sold amounts that

appear in the financial statements

D) provide tests of audit control functions as part of the AIS

18) Which type of information below should not be maintained by the AIS in accounting for fixed

assets?

A) identification/serial number

B) cost

C) improvements

D) market value

19) Direct labor must be tracked and accounted for as part of the production process. Traditionally,

direct labor was tracked using ________ but an AIS enhancement is to use ________ to record and track

direct labor costs.

A) job-time tickets; coded identification cards

B) move tickets; coded identification cards

C) employee earnings records; job-time tickets

D) time cards; electronic time entry terminals

20) Detailed data about reasons for warranty and repair costs is considered an applicable control used to

mitigate the threat of

A) underproduction.

B) overproduction.

C) poor product design.

D) suboptimal investment of fixed assets.

21) For replacement of inventories and assets destroyed by fire or other disasters, an organization needs

A) stand-by facilities.

B) adequate insurance coverage.

C) source data automation.

D) All of the above are correct.

22) Overproduction or underproduction can be a threat to an organization. To which process or activity

does this threat relate?

A) product design

B) planning and scheduling

C) production operations

D) cost accounting

23) What specific control can help restrict the rights of authorized users to only the portion of a database

needed to complete their specific job duties?

A) an access control matrix

B) passwords and user IDs

C) closed-loop verification

D) specific authorization

24) To reduce the threat of theft or destruction of inventories and other fixed assets, the organization

may wish to implement which of the following controls?

A) review and approval of fixed asset acquisitions

B) improved and more timely reporting

C) better production and planning systems

D) document all movement of inventory through the production process

25) The best control procedure for accurate data entry is

A) the use of on-line terminals.

B) an access control matrix.

C) passwords and user IDs.

D) automation of data collection.

26) Which of the following organization controls should be implemented and maintained to counteract

the general threat that the loss of production data will greatly slow or halt production activity?

A) Store key master inventory and production order files on-site only to prevent their theft.

B) Back up data files only after a production run has been physically completed.

C) Access controls should apply to all terminals within the organization.

D) Allow access to inventory records from any terminal within the organization to provide efficient data

entry.

27) The threat of loss of data exposes the company to

A) the loss of assets.

B) ineffective decision making.

C) inefficient manufacturing.

D) All of the above are correct.

28) What is the primary drawback to using a volume-driven base, such as direct labor or machine hours,

to apply overhead to products in a traditional cost accounting system?

A) The cost accountant may not fully understand how to track direct labor or machine hours.

B) It is difficult for an AIS to incorporate such a measurement into its system.

C) It is difficult for an ERP to incorporate such a measurement into its integrated system.

D) Many overhead costs are incorrectly allocated to products since they do not vary with production

volume.

29) ________ identifies costs with the corporation’s strategy for production of goods and services.

A) Activity-based costing

B) Job-order costing

C) Process costing

D) Manufacturing costing

30) In an Activity-Based Costing (ABC) system, a cause-and-effect relationship is known as a

A) cost stimulator.

B) overhead stimulator.

C) cost driver.

D) cost catalyst.

31) What does the first term in the throughput formula, productive capacity, represent?

A) the maximum number of units that can be produced given current technology

B) the percentage of total production time used to manufacture a product

C) the percentage of “good” units produced given current technology

D) the percentage of “bad” units produced given current technology

32) ________ are incurred to ensure that products are created without defects the first time.

A) External failure costs

B) Inspection costs

C) Internal failure costs

D) Prevention costs

33) ________ are associated with testing to ensure that products meet quality standards.

A) External failure costs

B) Inspection costs

C) Internal failure costs

D) Prevention costs

34) The cost of a product liability claim can be classified as a(n)

A) prevention cost.

B) inspection cost.

C) internal failure cost.

D) external failure cost.

35) Dolly Salem owns and operates a bakery in Charleston, South Carolina. She maintains a file of

recipes that list the ingredients used to make her famous cakes and cookies. These recipes are examples

of a(an)

A) bill of materials.

B) operations list.

C) production order.

D) materials requisition.

36) Dolly Salem owns and operates a bakery in Charleston, South Carolina. She maintains a file that

lists the sequence of procedures required to make each of her famous cakes and cookies. These

instructions are examples of a(an)

A) bill of materials.

B) operations list.

C) production order.

D) materials requisition.

37) Dolly Salem owns and operates a bakery in Charleston, South Carolina. Each morning she prepares

a list that describes the quantity and variety of cakes and cookies that will be prepared during the day.

This list is an example of a(an)

A) bill of materials.

B) operations list.

C) production order.

D) materials requisition.

38) Dolly Salem owns and operates a bakery in Charleston, South Carolina. Each afternoon, she

prepares a shopping list that describes the quantity and variety of ingredients that she will purchase in

the evening from a local food wholesaler. The shopping list is an example of a(an)

A) bill of materials.

B) operations list.

C) production order.

D) materials requisition.

39) Wee Bee Trucking determines the cost per delivery by summing the average cost of loading,

unloading, transporting, and maintenance. This is an example of ________ costing.

A) job-order

B) unit-based

C) activity-based

D) process

40) Wee Bee Trucking determines the cost per delivery by averaging total cost over number of

deliveries. This is an example of ________ costing.

A) job-order

B) unit-based

C) activity-based

D) process

41) Wee Bee Trucking determines the cost per delivery by identifying variables as cost drivers, and

allocating overhead accordingly. This is an example of ________ costing.

A) job-order

B) unit-based

C) activity-based

D) process

42) In activity-based costing, expenses associated with the purchase of health care insurance for

employees are ________ overhead.

A) batch-related

B) product-related

C) companywide

D) expenditure-based

43) In activity-based costing, the expenses associated with planning and design of new products are

________ overhead.

A) batch-related

B) product-related

C) companywide

D) expenditure-based

44) At the end of each production run, preventive maintenance is done on the assembly line. The

expenses associated with this maintenance are ________ overhead.

A) batch-related

B) product-related

C) companywide

D) department-based

45) Which of the following is not a benefit of activity-based costing?

A) Lower cost

B) Better decisions

C) Improved cost management

D) Identification of cost drivers

46) The expenses associated with a product recall are ________ costs.

A) prevention

B) inspection

C) internal failure

D) external failure

47) The expenses associated with quality assurance activities are ________ costs.

A) prevention

B) inspection

C) internal failure

D) external failure

48) The expenses associated with the use of clean rooms in the production of computer hard drives are

________ costs.

A) prevention

B) inspection

C) internal failure

D) external failure

49) The expenses associated with disposal of defective products are ________ costs.

A) prevention

B) inspection

C) internal failure

D) external failure

50) Labor productivity is measured by the quantity produced divided by the labor time required to

produce it. All other things held constant, an increase in labor productivity will increase throughput by

A) increasing productive capacity.

B) increasing productive processing time.

C) increasing yield.

D) increasing all components of throughput.

51) In addition to identifying and dealing with defective products before they reach customers, quality

management is concerned with initiating process changes that will reduce the number of defective units

produced. All other things held constant, a decrease in the number of defective units will increase

throughput by

A) increasing productive capacity.

B) increasing productive processing time.

C) increasing yield.

D) increasing all components of throughput.

52) Folding Squid Technologies has installed a new production monitoring system that is expected to

reduce system breakdowns by 28%. This system will increase throughput by

A) increasing productive capacity.

B) increasing productive processing time.

C) increasing yield.

D) increasing all components of throughput.

53) Clint Smith operates a machine shop in Burbank, California. He places bids on small lot production

projects submitted by firms throughout the Los Angeles area. Which of the following is most likely to be

a cost driver for the allocation of utility costs?

A) Number of units produced

B) Number of labor hours

C) Number of projects completed

D) Sales revenue

54) Folding Squid Technologies initiated a just-in-time inventory system in 2010. Now the production

manager, Chan Ziaou, wants to apply the same principles to the entire production process. His

recommendation is for the company adopt a

A) lean manufacturing system.

B) master production scheduling system.

C) manufacturing resource planning system.

D) computer-integrated manufacturing system.

55) This document appears to be a

A) Materials Requisition.

B) Production Order.

C) Bill of Materials.

D) Move Ticket between production and warehouse functions.

56) How many side panels should the company budget for use in week two?

Bill of Materials

Finished Product: DVD Player

Part Number

105

125

148

155

173

195

199

Description

Control Unit

Back Panel

Side Panel

Top/Bottom Panel

Timer

Front Panel

Screw

Quantity

1

1

2

2

1

1

6

Operations List for: Create Side Panel

Operation Number

105

106

124

142

155

Description

Cut to shape

Corner cut

Turn and shape

Finish

Paint

Machine Number

ML15-12

ML15-9

S28-17

F54-5

P89-1

Standard Time (m:s)

2:00

3:15

4:00

7:10

9:30

57) How many labor hours should the company budget in week three to produce all side panels needed?

Round to the nearest hour, if necessary.

Bill of Materials

Finished Product: DVD Player

Part Number

105

125

148

155

173

195

199

Description

Control Unit

Back Panel

Side Panel

Top/Bottom Panel

Timer

Front Panel

Screw

Quantity

1

1

2

2

1

1

6

Operations List for: Create Side Panel

Operation Number

105

106

124

142

155

Description

Cut to shape

Corner cut

Turn and shape

Finish

Paint

Machine Number

ML15-12

ML15-9

S28-17

F54-5

P89-1

Standard Time (m:s)

2:00

3:15

4:00

7:10

9:30

58) Identify and discuss the two documents that are the result of product design activities.

59) Explain what CIM means and its benefits.

60) What types of data are accumulated by cost accounting? What is the accountant’s role in cost

accounting?

61) What role does the AIS play in the production cycle?

62) Discuss the role the accountant can play in the production cycle.

63) Identify and discuss the two common methods of production planning.

64) What are the two major types of cost accounting systems and what are the differences between the

two?

65) Describe five threats in the production cycle and the applicable control procedures used to mitigate

each threat.

66) Discuss two measures that can address the threats of inefficiencies and quality controls problems.

67) Discuss the criticisms of traditional cost accounting methods.

68) What is activity-based costing (ABC)? How does it compare with the traditional costing methods?

What are the benefits of activity-based costing?