Chapter 13: Budgeting and Standard Cost Systems

The standard factory overhead rate of Quaker Inc. is $10 per direct labor hour ($8 for variable

factory overhead and $2 for fixed factory overhead) based on 100% capacity of 30,000 direct

labor hours. The standard cost and the actual cost of factory overhead for the production of

5,000 units during May were as follows:

Standard:

25,000 hours at $10

$250,000

Actual:

Variable factory overhead

202,500

Fixed factory overhead

60,000

149. Refer to the information provided for Quaker Inc. What is the amount of the fixed factory

overhead volume variance?

a. $12,500 favorable

b. $10,000 unfavorable

c. $12,500 unfavorable

d. $10,000 favorable

150. Refer to the information provided for Quaker Inc. What is the amount of the variable factory

overhead controllable variance?

a. $10,000 favorable

b. $2,500 unfavorable

c. $10,000 unfavorable

d. $2,500 favorable

151. The cost of available but unused productive capacity is indicated by the:

a. fixed factory overhead volume variance.

b. direct labor cost time variance.

c. direct labor cost rate variance.

d. variable factory overhead controllable variance.

Chapter 13: Budgeting and Standard Cost Systems

152. The standard factory overhead rate is $7.50 per machine hour ($6.20 for variable factory

overhead and $1.30 for fixed factory overhead) based on 100% capacity of 80,000 machine

hours. The standard cost and the actual cost of factory overhead for the production of 15,000

units during August were as follows:

Actual:

Variable factory overhead

$360,000

Fixed factory overhead

104,000

Standard:

60,000 hours at $7.50

450,000

What is the amount of the variable factory overhead controllable variance?

a. $12,000 unfavorable

b. $12,000 favorable

c. $14,000 unfavorable

d. $26,000 unfavorable

153. Incurring actual indirect factory wages in excess of budgeted amounts for actual production

results in a:

a. unfavorable quantity variance.

b. unfavorable controllable variance.

c. favorable volume variance.

d. favorable labor rate variance.

154. The variable factory overhead controllable variance measures:

a. operating results at less than normal capacity.

b. the efficiency of using variable overhead resources.

c. operating results at more than normal capacity.

d. control over fixed overhead costs.

155. The unfavorable volume variance may be due to all of the following factors except:

a. failure to maintain an even flow of work.

b. machine breakdowns.

c. unexpected increases in the cost of utilities.

d. failure to obtain enough sales orders.

Chapter 13: Budgeting and Standard Cost Systems

156. Standard Corporation uses a standard cost system. The following information was provided for

the period that just ended:

Standard time per completed unit 3 hrs.

Actual total factory overhead $108,000

Fixed factory overhead $60,000

Standard fixed factory overhead rate $2.00 per labor hour

Standard variable factory overhead rate $1.50 per labor hour

Normal capacity 30,000 hours

Plant operated during the period 28,000 hours

Units completed during the period 9,000

The fixed factory overhead volume variance is

a. $6,000 favorable.

b. $3,000 favorable.

c. $3,000 unfavorable.

d. $6,000 unfavorable.

157. Favorable volume variances may be harmful when:

a. machine repairs cause work stoppages.

b. supervisors fail to maintain an even flow of work.

c. production in excess of normal capacity cannot be sold.

d. there are insufficient sales orders to keep the factory operating at normal capacity.

158. Assuming that the standard fixed overhead rate is based on full capacity, the cost of available

but unused productive capacity is indicated by the:

a. factory overhead cost volume variance.

b. direct labor cost time variance.

c. direct labor cost rate variance.

d. factory overhead cost controllable variance.

159. Which of the following doesn’t result in an unfavorable fixed overhead volume variance?

a. Sales orders at a low level

b. Machine breakdowns

c. Employee inexperience

d. Increase in utility costs

Chapter 13: Budgeting and Standard Cost Systems

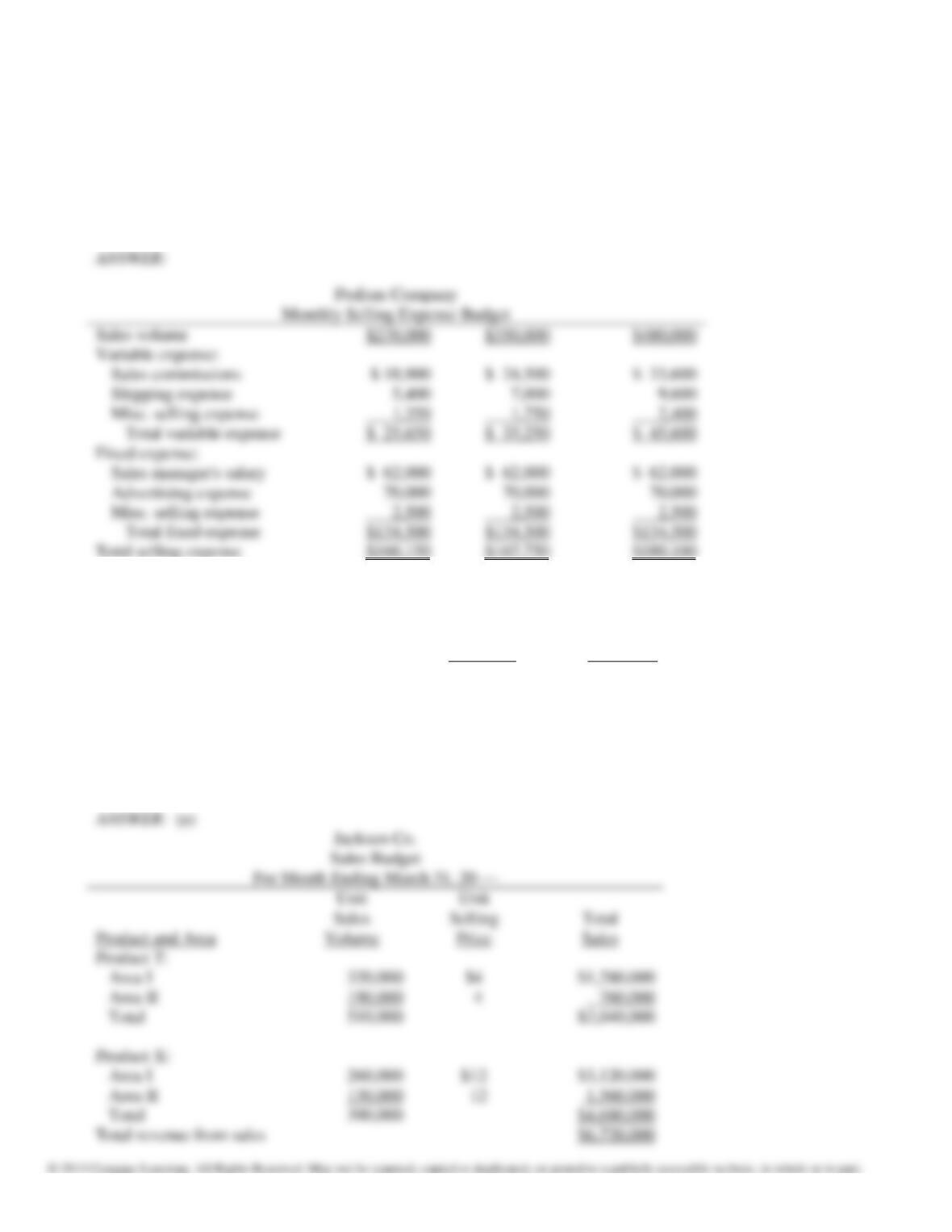

160. Prepare a monthly flexible selling expense budget for Podism Company for sales volumes of

$270,000, $350,000, and $480,000, based on the following data:

Sales commissions

7% of sales

Sales manager’s salary

$62,000 per month

Advertising expense

$70,000 per month

Shipping expense

2% of sales

Miscellaneous selling expense

$2,500 per month plus 1/2% of sales

Sales volume

Variable expense:

Sales commissions

Shipping expense

Misc. selling expense

Total variable expense

Fixed expense:

Sales manager’s salary

Advertising expense

Misc. selling expense

Total fixed expense

Total selling expense

161. Based on the following production and sales data of Jackson Co. for March of the current year,

prepare (a) a sales budget and (b) a production budget.

Product T Product X

Estimated inventory, March 1 26,000 units 18,000 units

Desired inventory, March 31 32,000 units 15,000 units

Expected sales volume:

Area I 320,000 units 260,000 units

Area II 190,000 units 130,000 units

Unit sales price $4 $12

Product and Area

Area I

Area II

Total

Product X:

Area II

Total

Chapter 13: Budgeting and Standard Cost Systems

(b)

Jackson Co.

Production Budget

For Month Ending March 31, 20 —

Product T

Product X

Sales

510,000 units

390,000 units

Plus desired ending inventory, March 31, 20 —

32,000

15,000

Total

542,000 units

405,000 units

Less estimated beginning inventory, March 1, 20 —

26,000

18,000

Total production

516,000 units

387,000 units

162. Microfix Company manufactures two models of Television, AR30 and AR33. Based on the

following production data for April of the current year, prepare a production budget for April.

AR30

AR33

Estimated inventory (units), April 1

2,500

3,700

Desired inventory (units), April 30

Expected sales volume (units):

3,700

3,700

Eastern zone

8,200

11,500

Midwest zone

13,000

17,500

Western zone

7,300

9,100

Chapter 13: Budgeting and Standard Cost Systems

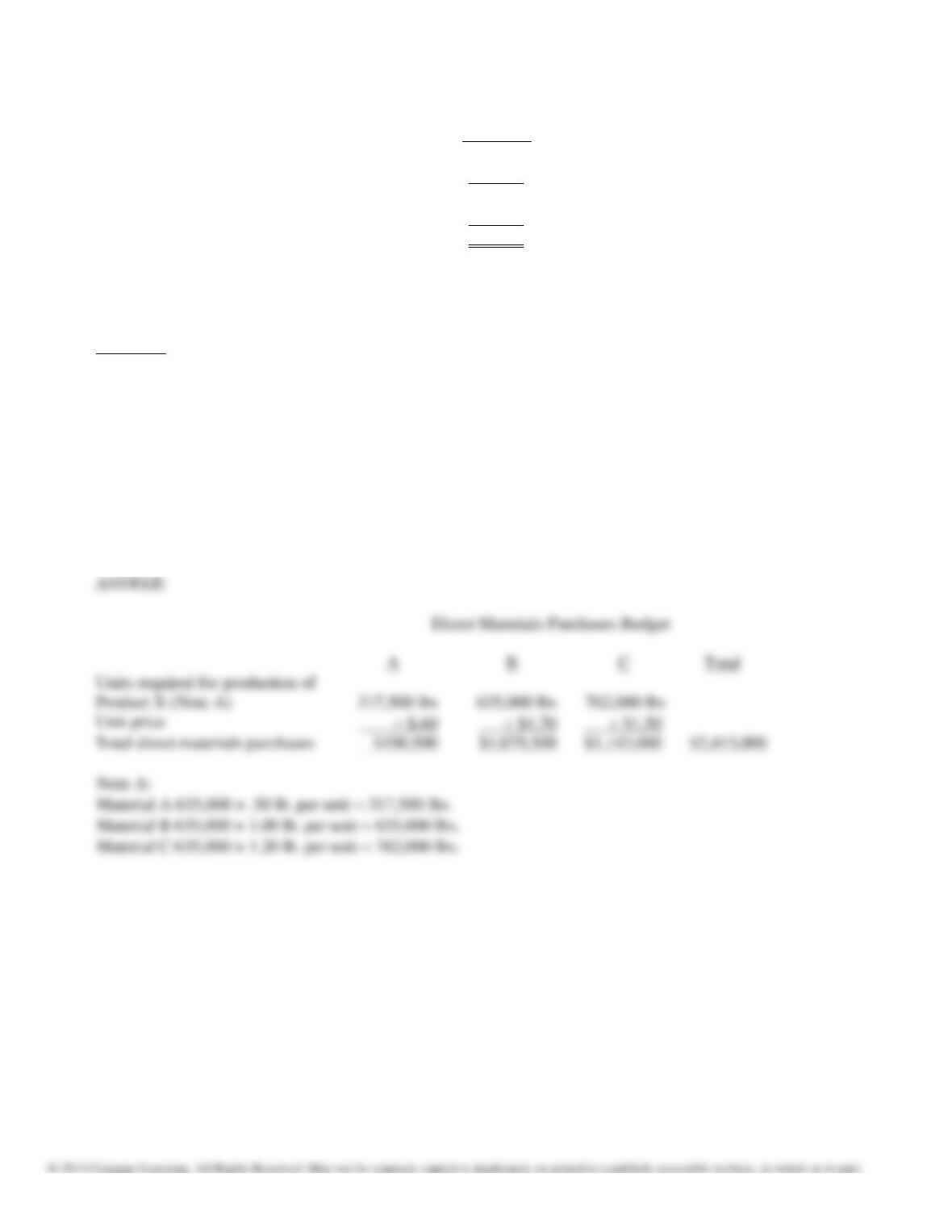

163. Brown Inc.’s production budget for Product X for the year ended December 31 is as follows:

Product X

Sales 640,000 units

Plus desired ending inventory 85,000

Total 725,000

Less estimated beginning inventory, Jan. 1 90,000

Total production 635,000

In Brown’s production operations, Materials A, B, and C are required to make Product X. The

quantities of direct materials expected to be used for each unit of product are as follows:

Product X

Material A .50 pound per unit

Material B 1.00 pound per unit

Material C 1.20 pound per unit

The prices of direct materials are as follows:

Material A $0.60 per pound

Material B $1.70 per pound

Material C $1.50 per pound

Prepare a direct materials purchases budget for Product X.

Chapter 13: Budgeting and Standard Cost Systems

164. The treasurer of Unisyms Company has accumulated the following budget information for the

first two months of the coming year:

March

April

Sales

$450,000

$520,000

Manufacturing costs

290,000

350,000

Selling and administrative expenses

41,400

46,400

Capital additions

250,000

—

The company expects to sell about 35% of its merchandise for cash. Of sales on account, 80%

are expected to be collected in full in the month of the sale and the remainder in the month

following the sale. One-fourth of the manufacturing costs are expected to be paid in the month

in which they are incurred and the other three-fourths in the following month. Depreciation,

insurance, and property taxes represent $6,400 of the probable monthly selling and

administrative expenses. Insurance is paid in February, and a $40,000 installment on income

taxes is expected to be paid in April. Of the remainder of the selling and administrative

expenses, one-half are expected to be paid in the month in which they are incurred, with the

balance paid in the following month. Capital additions of $250,000 are expected to be paid in

March.

Current assets as of March 1 are composed of cash of $45,000 and accounts receivable of

$51,000. Current liabilities as of March 1 are composed of accounts payable of $121,500

($102,000 for materials purchases and $19,500 for operating expenses). Management desires

to maintain a minimum cash balance of $20,000.

Prepare a monthly cash budget for March and April.

Chapter 13: Budgeting and Standard Cost Systems

165. Trapp Co. was organized on August 1 of the current year. Projected sales for the next three

months are as follows:

August

$100,000

September

185,000

October

225,000

The company expects to sell 40% of its merchandise for cash. Of the sales on account, one

third are expected to be collected in the month of the sale and the remainder in the following

month.

Prepare a schedule indicating cash collections of accounts receivable for August, September,

and October.

Chapter 13: Budgeting and Standard Cost Systems

166. Standard and actual costs for direct materials for the manufacture of 1,000 units of product

were as follows:

Actual costs 1,450 lbs. @ $8.10

Standard costs 1,500 lbs. @ $8.00

Determine the (a) quantity variance, (b) price variance, and (c) total direct materials cost

variance.

167. Compute the standard cost for one hat, based on the following standards for each hat:

Standard Material Quantity: 3/4 yard of fabric at $4.00 per yard

Standard Labor: 1 hour at $5.75 per hour

Factory Overhead: $2.90 per direct labor hour

Chapter 13: Budgeting and Standard Cost Systems

168. Standard and actual costs for direct materials for the manufacture of 2,000 units of product

were as follows:

Actual costs 2,750 lbs. @ $8.10

Standard costs 2,800 lbs. @ $8.00

Determine the (a) quantity variance, (b) price variance, and (c) total direct materials cost

variance.

169. Standard and actual costs for direct labor for the manufacture of 1,500 units of product were as

follows:

Actual costs 450 hours @ $17.00

Standard costs 455 hours @ $16.50

Determine the (a) time variance, (b) rate variance, and (c) total direct labor cost variance.

Chapter 13: Budgeting and Standard Cost Systems

170. The standard factory overhead rate is $12 per machine hour ($10 for variable factory overhead

and $2 for fixed factory overhead) based on 100% capacity of 42,000 machine hours. The

standard cost and the actual cost of factory overhead for the production of 2,000 units were as

follows:

Actual: Variable factory overhead $350,500

Fixed factory overhead 84,000

Standard: 35,000 hours @ $12 420,000

Determine the (a) volume variance, (b) controllable variance, and (c) total factory overhead

cost variance.