46) Jark Corporation has invested in a machine that cost $60,000, that has a useful life of six years,

and that has no salvage value at the end of its useful life. The machine is being depreciated by the

straight-line method, based on its useful life. It will have a payback period of four years. Given

these data, the simple rate of return on the machine is closest to (Ignore income taxes.):

A) 8.3%

B) 7.2%

C) 9.5%

D) 25%

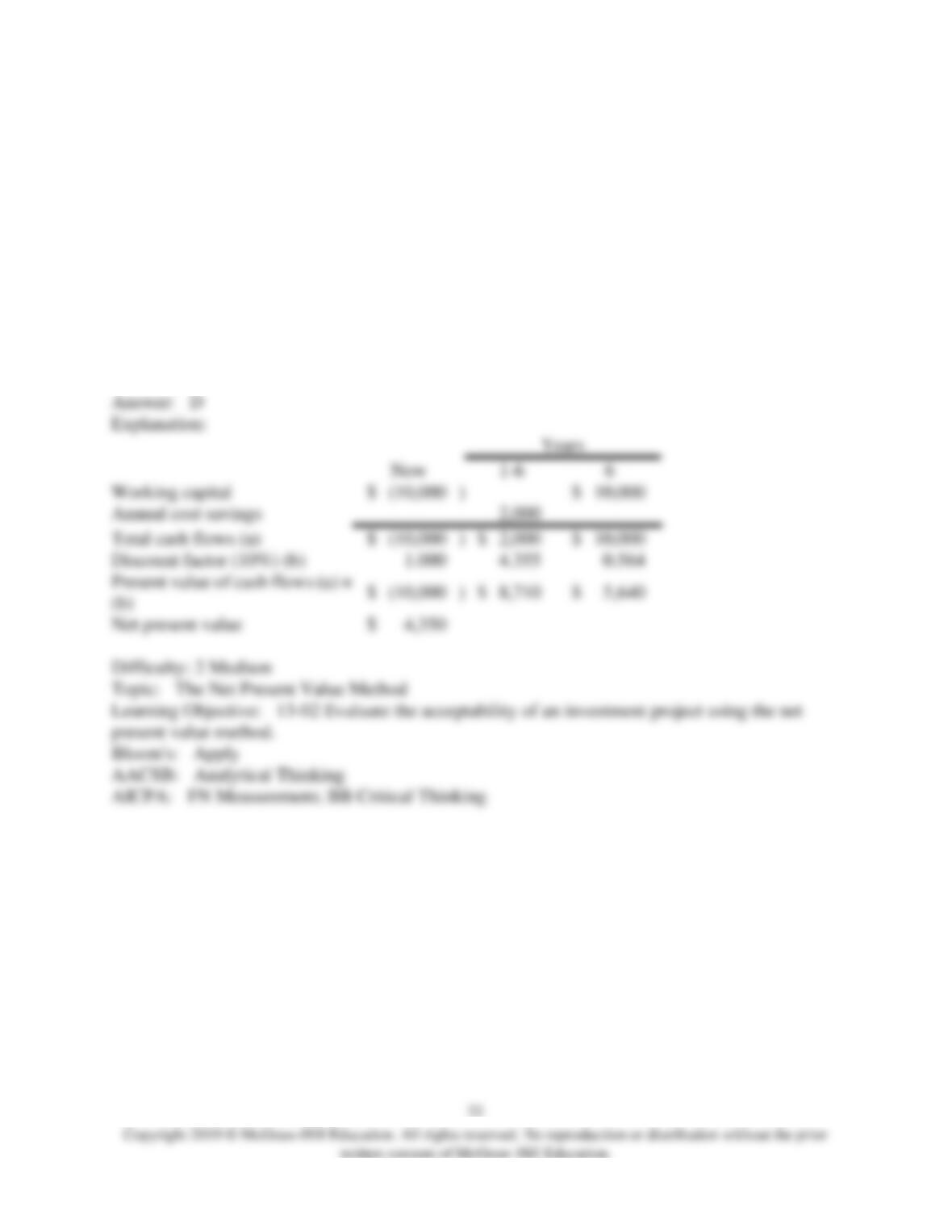

47) Parks Corporation is considering an investment proposal in which a working capital

investment of $10,000 would be required. The investment would provide cash inflows of $2,000

per year for six years. The working capital would be released for use elsewhere when the project is

completed. If the company’s discount rate is 10%, the investment’s net present value is closest to

(Ignore income taxes.):

See separate Exhibit 13B-1 and Exhibit 13B-2, to determine the appropriate discount factor(s)

using the tables provided.

A) $1,290

B) $(1,290)

C) $2,000

D) $4,350

48) In an effort to reduce costs, Pontic Manufacturing Corporation is considering an investment in

equipment that will reduce defects. This equipment will cost $420,000, will have an estimated

useful life of 10 years, and will have an estimated salvage value of $50,000 at the end of 10 years.

The company’s discount rate is 22%. What amount of cost savings will this equipment have to

generate per year in each of the 10 years in order for it to be an acceptable project? (Ignore income

taxes.).

See separate Exhibit 13B-1 and Exhibit 13B-2, to determine the appropriate discount factor(s)

using the tables provided.

A) $50,690 or more

B) $41,315 or more

C) $105,315 or more

D) $94,316 or more

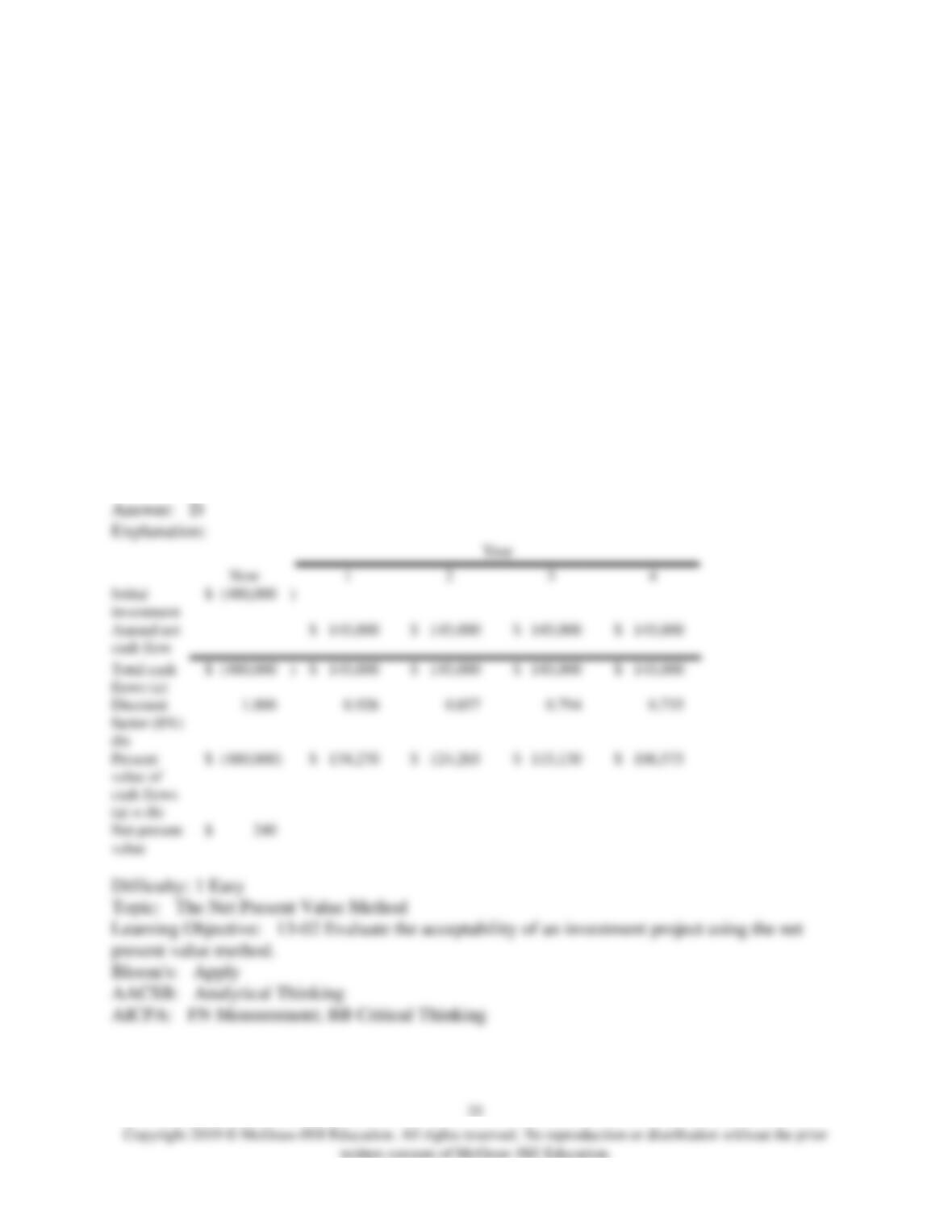

49) Respass Corporation has provided the following data concerning an investment project that it

is considering:

Initial investment

$

160,000

Annual cash flow

$

54,000

per year

Salvage value at the end of the project

$

11,000

Expected life of the project

4

years

Discount rate

15

%

See separate Exhibit 13B-1 and Exhibit 13B-2, to determine the appropriate discount factor(s)

using the tables provided.

The net present value of the project is closest to:

A) $67,000

B) $160,516

C) $516

D) $(5,776)

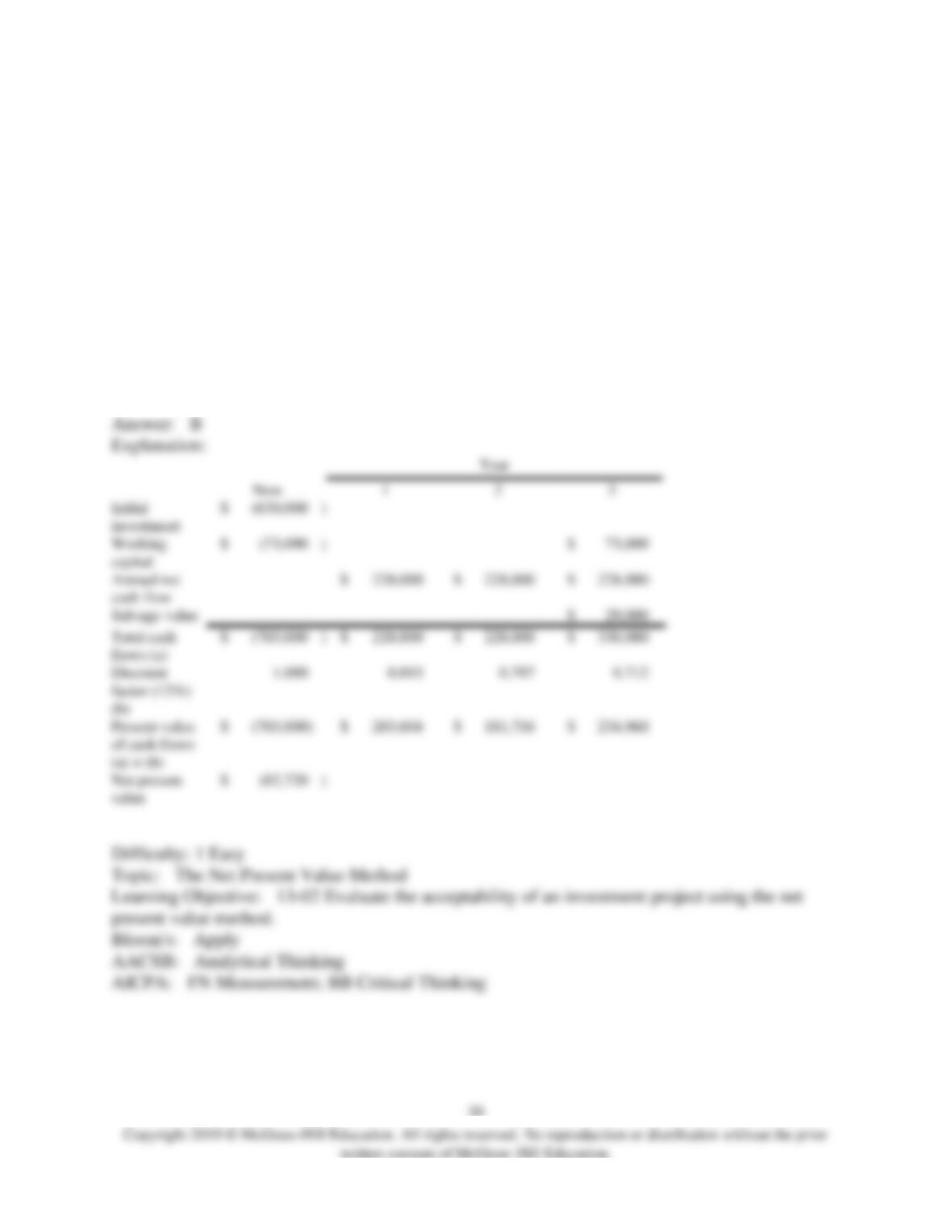

50) Puello Corporation has provided the following data concerning an investment project that it is

considering:

Initial investment

$

480,000

Annual cash flow

$

145,000

per year

See separate Exhibit 13B-1 and Exhibit 13B-2, to determine the appropriate discount factor(s)

using the tables provided.

The life of the project is 4 years. The company’s discount rate is 8%. The net present value of the

project is closest to:

A) $480,000

B) $480,240

C) $100,000

D) $240

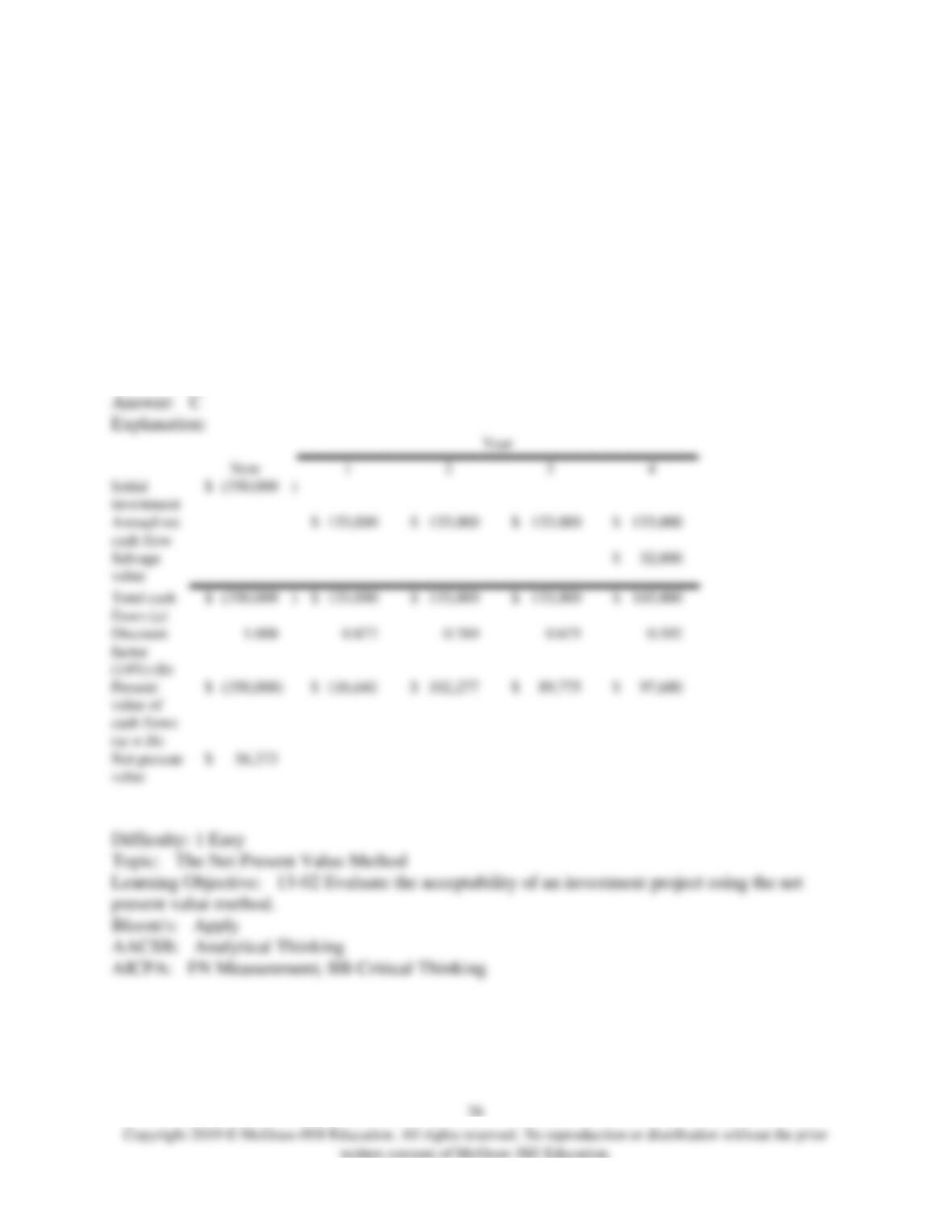

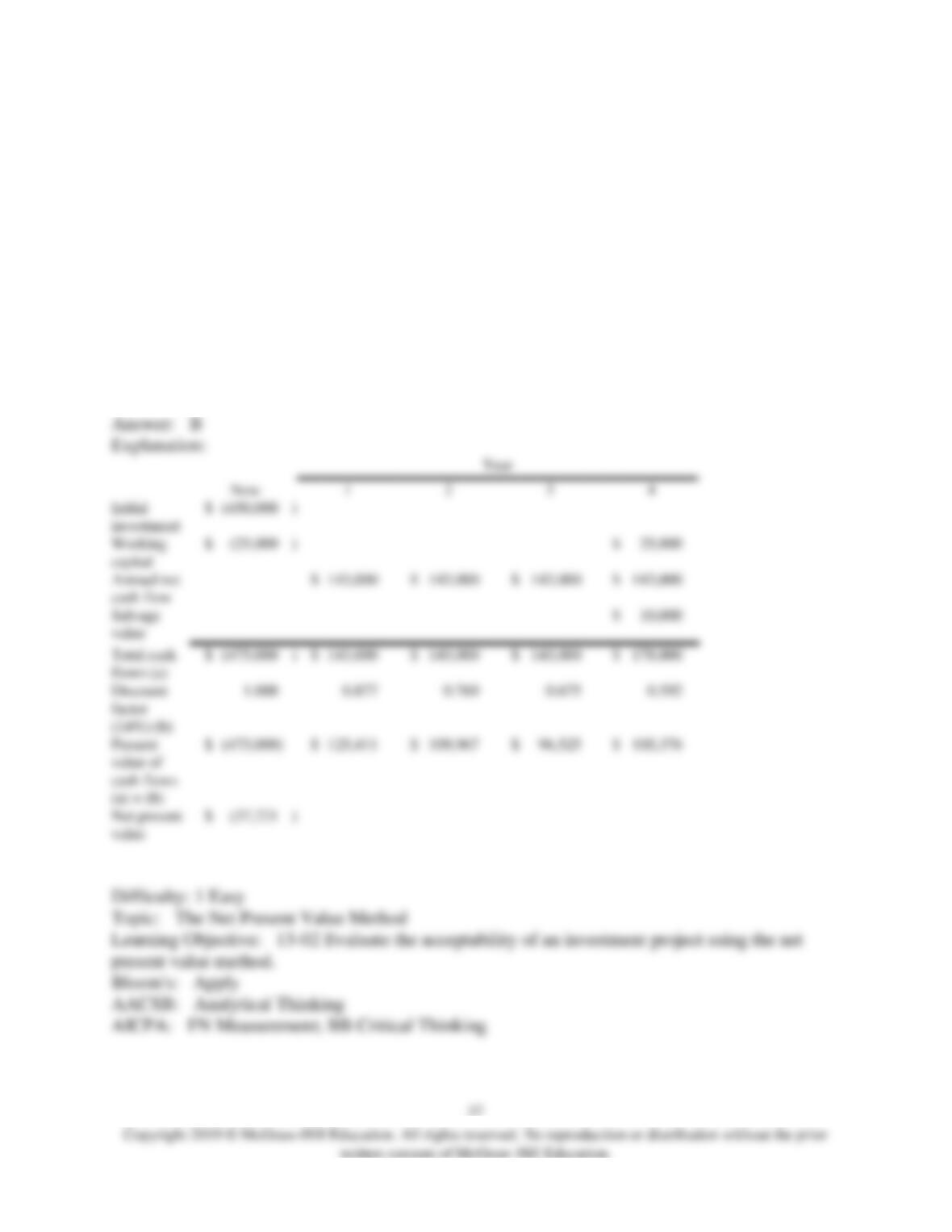

51) Haroldsen Corporation is considering a capital budgeting project that would require an initial

investment of $350,000. The investment would generate annual cash inflows of $133,000 for the

life of the project, which is 4 years. At the end of the project, equipment that had been used in the

project could be sold for $32,000. The company’s discount rate is 14%. The net present value of the

project is closest to:

See separate Exhibit 13B-1 and Exhibit 13B-2, to determine the appropriate discount factor(s)

using the tables provided.

A) $214,000

B) $37,429

C) $56,373

D) $406,373

52) Moates Corporation has provided the following data concerning an investment project that it is

considering:

Initial investment

$

410,000

Annual cash flow

$

117,000

per year

Expected life of the project

4

years

Discount rate

9

%

See separate Exhibit 13B-1 and Exhibit 13B-2, to determine the appropriate discount

factor(s) using the tables provided.

The net present value of the project is closest to:

A) $378,963

B) $(31,037)

C) $410,000

D) $58,000

53) Byerly Corporation has provided the following data concerning an investment project that it is

considering:

Initial investment

$

670,000

Working capital

$

61,000

Annual cash flow

$

227,000

per year

Salvage value at the end of the project

$

20,000

Expected life of the project

3

years

Discount rate

10

%

See separate Exhibit 13B-1 and Exhibit 13B-2, to determine the appropriate discount factor(s)

using the tables provided.

The working capital would be released for use elsewhere at the end of the project. The net present

value of the project is closest to:

A) $(151,658)

B) $(105,847)

C) $11,000

D) $(44,847)

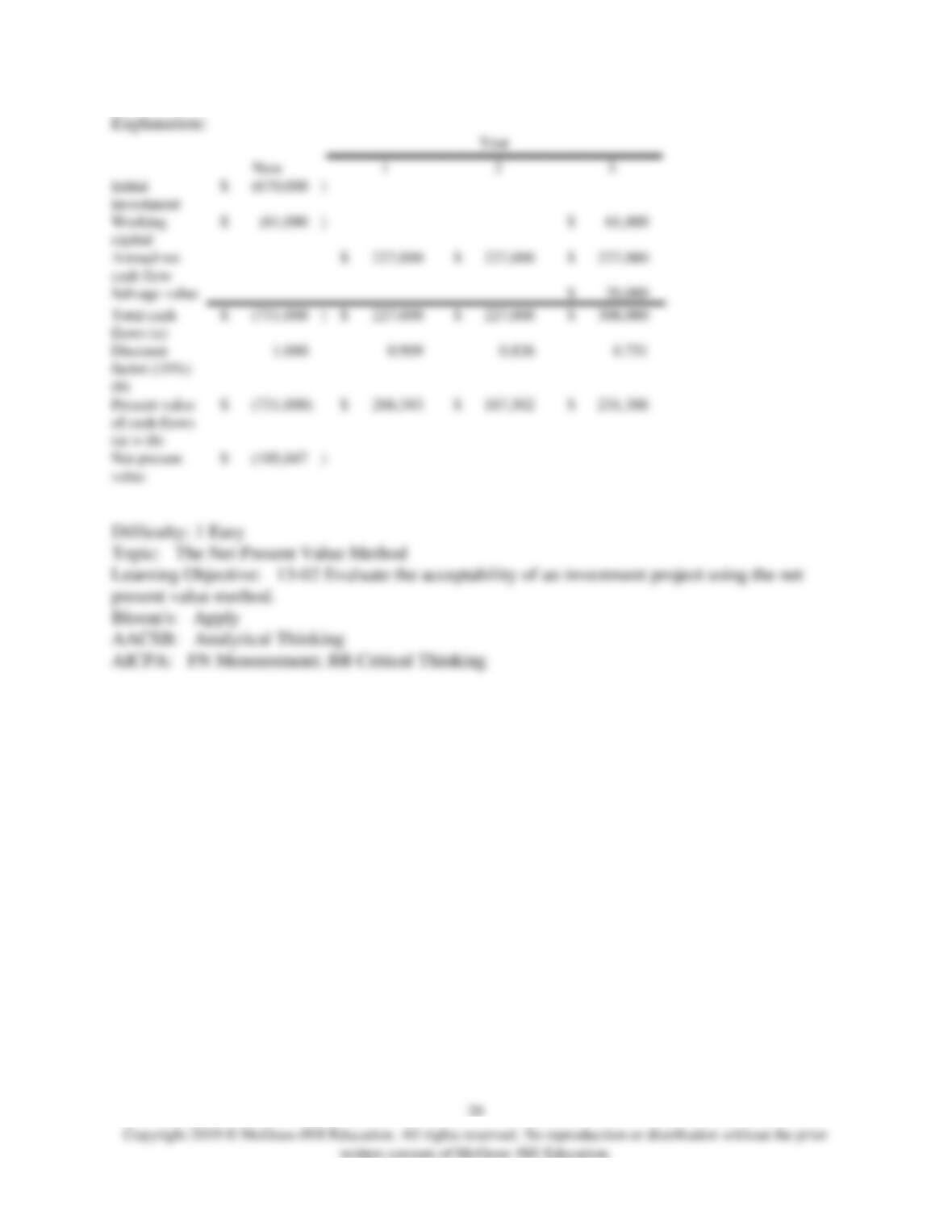

54) Penniston Corporation is considering a capital budgeting project that would require an initial

investment of $630,000 and working capital of $73,000. The working capital would be released for

use elsewhere at the end of the project in 3 years. The investment would generate annual cash

inflows of $228,000 for the life of the project. At the end of the project, equipment that had been

used in the project could be sold for $29,000. The company’s discount rate is 12%. The net present

value of the project is closest to:

See separate Exhibit 13B-1 and Exhibit 13B-2, to determine the appropriate discount factor(s)

using the tables provided.

A) $(134,696)

B) $(82,720)

C) $(9,720)

D) $54,000

55) The management of Penfold Corporation is considering the purchase of a machine that would

cost $440,000, would last for 7 years, and would have no salvage value. The machine would

reduce labor and other costs by $102,000 per year. The company requires a minimum pretax return

of 16% on all investment projects. The net present value of the proposed project is closest to

(Ignore income taxes.):

See separate Exhibit 13B-1 and Exhibit 13B-2 to determine the appropriate discount factor(s)

using the tables provided.

A) $(28,022)

B) $96,949

C) $(79,196)

D) $274,000

56) Dowlen, Inc., is considering the purchase of a machine that would cost $150,000 and would

last for 6 years. At the end of 6 years, the machine would have a salvage value of $23,000. The

machine would reduce labor and other costs by $36,000 per year. Additional working capital of

$6,000 would be needed immediately. All of this working capital would be recovered at the end of

the life of the machine. The company requires a minimum pretax return of 12% on all investment

projects. The net present value of the proposed project is closest to (Ignore income taxes.):

See separate Exhibit 13B-1 and Exhibit 13B-2, to determine the appropriate discount factor(s)

using the tables provided.

A) $9,657

B) $(2,004)

C) $6,699

D) $13,223

57) Stomberg Corporation has provided the following data concerning an investment project that it

is considering:

Initial investment

$

550,000

Annual cash flow

$

180,000

per year

Salvage value at the end of the project

14,000

See separate Exhibit 13B-1 and Exhibit 13B-2, to determine the appropriate discount factor(s)

using the tables provided.

The life of the project is 4 years. The company’s discount rate is 10%. The net present value of the

project is closest to:

A) $184,000

B) $579,982

C) $29,982

D) $20,420

58) Fossa Road Paving Corporation is considering an investment in a curb-forming machine. The

machine will cost $240,000, will last 10 years, and will have a $40,000 salvage value at the end of

10 years. The machine is expected to generate net cash inflows of $60,000 per year in each of the

10 years. Fossa’s discount rate is 18%. The net present value of the proposed investment is closest

to (Ignore income taxes.):

See separate Exhibit 13B-1 and Exhibit 13B-2, to determine the appropriate discount factor(s)

using the tables provided.

A) $5,840

B) $37,280

C) $(48,780)

D) $69,640

59) Charlie Corporation is considering buying a new donut maker. This machine will replace an

old donut maker that still has a useful life of 6 years. The new machine will cost $3,600 a year to

operate, as opposed to the old machine, which costs $3,800 per year to operate. Also, because of

increased capacity, an additional 20,000 donuts a year can be produced. The company makes a

contribution margin of $0.10 per donut. The old machine can be sold for $7,000 and the new

machine costs $30,000. The incremental annual net cash inflows provided by the new machine

would be (Ignore income taxes.):

A) $2,200

B) $200

C) $2,000

D) $5,000

60) The following data pertain to an investment proposal (Ignore income taxes.):

Cost of the investment

$

35,000

Annual cost savings

$

12,000

Estimated salvage value

$

6,000

Life of the project

5

years

Discount rate

18

%

See separate Exhibit 13B-1 and Exhibit 13B-2, to determine the appropriate discount factor(s)

using the tables provided.

The net present value of the proposed investment is closest to:

A) $2,622

B) $5,146

C) $2,524

D) $31,000

1-5

Initial investment

$

Working capital

Annual net cash flow

$

Salvage value

$

6,000

Total cash flows (a)

$

$

$

6,000

Discount factor (18%) (b)

0.437

(b)

$

)

$

$

2,622

Net present value

$

61) Kanzler Corporation is considering a capital budgeting project that would require an initial

investment of $450,000 and working capital of $25,000. The working capital would be released for

use elsewhere at the end of the project in 4 years. The investment would generate annual cash

inflows of $143,000 for the life of the project. At the end of the project, equipment that had been

used in the project could be sold for $10,000. The company’s discount rate is 14%. The net present

value of the project is closest to:

See separate Exhibit 13B-1 and Exhibit 13B-2, to determine the appropriate discount factor(s)

using the tables provided.

A) $(27,521)

B) $(37,721)

C) $(52,521)

D) $132,000

62) Nevland Corporation is considering the purchase of a machine that would cost $130,000 and

would last for 6 years. At the end of 6 years, the machine would have a salvage value of $18,000.

By reducing labor and other operating costs, the machine would provide annual cost savings of

$44,000. The company requires a minimum pretax return of 19% on all investment projects. The

net present value of the proposed project is closest to (Ignore income taxes.):

See separate Exhibit 13B-1 and Exhibit 13B-2, to determine the appropriate discount factor(s)

using the tables provided.

A) $38,040

B) $26,376

C) $74,902

D) $20,040

63) Facio Corporation has provided the following data concerning an investment project that it is

considering:

Initial investment

$

770,000

Working capital

$

65,000

Annual cash flow

$

274,000

per year

Salvage value at the end of the project

$

20,000

See separate Exhibit 13B-1 and Exhibit 13B-2, to determine the appropriate discount factor(s)

using the tables provided.

The working capital would be released for use elsewhere at the end of the project in 3 years. The

company’s discount rate is 8%. The net present value of the project is closest to:

A) $(113,022)

B) $(61,412)

C) $3,588

D) $52,000

64) Anthony operates a part time auto repair service. He estimates that a new diagnostic computer

system will result in increased cash inflows of $1,500 in Year 1, $2,100 in Year 2, and $3,200 in

Year 3. If Anthony’s required rate of return is 10%, then the most he would be willing to pay for the

new diagnostic computer system would be (Ignore income taxes.):

See separate Exhibit 13B-1 and Exhibit 13B-2, to determine the appropriate discount factor(s)

using the tables provided.

A) $4,599

B) $5,501

C) $5,638

D) $5,107