Name:

Class:

Date:

chapter 13

Indicate whether the statement is true or false.

1. A sale of treasury stock may result in a decrease in paid-in capital. All decreases should be charged to Paid-In Capital

from Sale of Treasury Stock.

a.

True

b.

False

2. The initial owners of stock of a newly formed corporation are called directors.

a.

True

b.

False

3. Retained Earnings represents past net income less past dividends; therefore, any balance in this account would be listed

on the income statement.

a.

True

b.

False

4. Twenty percent of all businesses in the United States are corporations, and they account for 80% of the total business

dollars generated.

a.

True

b.

False

5. A large retained earnings account means that there is cash available to pay dividends.

a.

True

b.

False

6. The amount of capital paid in by the stockholders of the corporation is called legal capital.

a.

True

b.

False

7. When common stock is issued in exchange for land, the land should be recorded in the accounts at the par value of the

stock issued.

a.

True

b.

False

8. Organizational expenses are classified as intangible assets on the balance sheet.

a.

True

b.

False

9. When a corporation issues stock at a premium, it reports the premium as an Other Income item on the income

statement.

a.

True

b.

False

10. If 20,000 shares are authorized, 15,000 shares are issued, and 500 shares are held as treasury stock, a cash dividend of

$1 per share would amount to $15,000.

a.

True

Name:

Class:

Date:

chapter 13

b.

False

11. The retained earnings statement may be combined with the income statement.

a.

True

b.

False

12. The number of shares of outstanding stock is equal to the number of shares authorized minus the number of shares

issued.

a.

True

b.

False

13. The two main sources of stockholders’ equity are investments contributed by stockholders and net income retained in

the business.

a.

True

b.

False

14. A large public corporation normally uses registrars and transfer agents to maintain the records of stockholders.

a.

True

b.

False

15. Preferred stockholders must receive their current-year dividends before the common stockholders can receive any

dividends.

a.

True

b.

False

16. A corporation has 10,000 shares of $100 par stock outstanding. If the corporation issues a 5-for-1 stock split, the

number of shares outstanding after the split will be 40,000.

a.

True

b.

False

17. If a corporation is liquidated, preferred stockholders are paid before the creditors and before the common

stockholders.

a.

True

b.

False

18. Under the Internal Revenue Code, corporations are required to pay federal income taxes.

a.

True

b.

False

19. If paid-in capital in excess of par―preferred stock is $30,000, preferred stock is $200,000, paid-in capital in excess of

par―common stock is $20,000, common stock is $525,000, and retained earnings is $105,000 (deficit), total stockholders’

equity is $880,000.

a.

True

b.

False

20. A stock split results in a transfer at market value from retained earnings to paid-in capital.

a.

True

Name:

Class:

Date:

chapter 13

b.

False

21. The declaration of a cash dividend decreases a corporation’s stockholders equity’ and decreases its assets.

a.

True

b.

False

22. The issuance of common stock affects both paid-in capital and retained earnings.

a.

True

b.

False

23. The cost of treasury stock is shown as a deduction following paid-in capital and retained earnings in the Stockholders’

Equity section of the balance sheet.

a.

True

b.

False

24. Cash dividends become a liability to a corporation on the date of record.

a.

True

b.

False

25. The reduction in the par or stated value of common stock, accompanies by the issuance of a proportionate number of

additional shares, is called a stock split.

a.

True

b.

False

26. If a company has preferred stock, the preferred stock dividend is added to net income when computing earnings per

common share.

a.

True

b.

False

27. The day on which the board of directors of the corporation distributes a dividend is called the declaration date.

a.

True

b.

False

28. A corporation is a separate entity for accounting purposes but not for legal purposes.

a.

True

b.

False

29. A restriction/appropriation of retained earnings establishes cash assets that are set aside for a specific purpose.

a.

True

b.

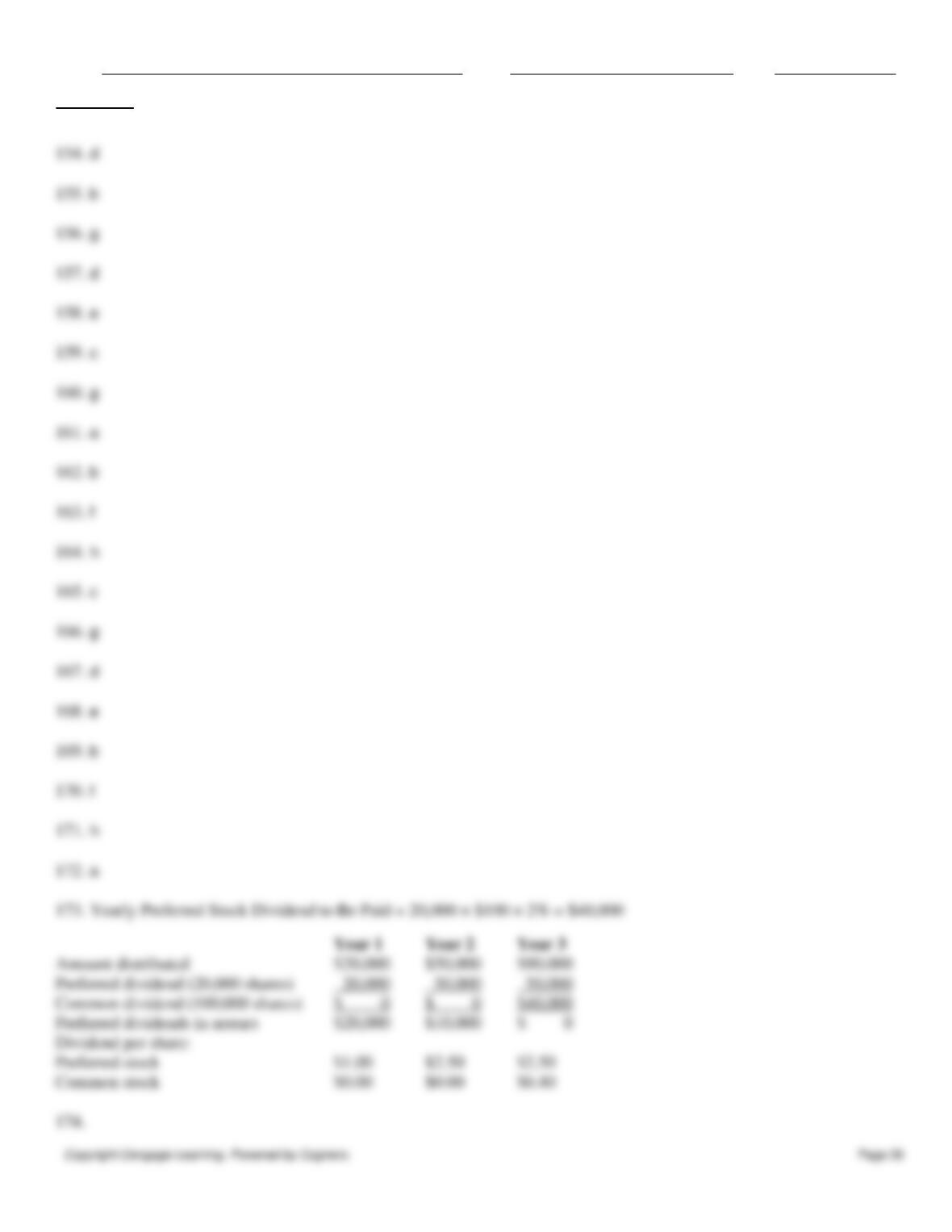

False

30. If the dividend amount of preferred stock, $50 par value, is quoted as 8%, then the dividend per share would be $4.

a.

True

b.

False

31. When the board of directors declares a cash or stock dividend, this action decreases retained earnings.

Name:

Class:

Date:

chapter 13

a.

True

b.

False

32. The declaration and issuance of a stock dividend do not affect the total amount of a corporation’s assets, liabilities, or

stockholders’ equity.

a.

True

b.

False

33. For accounting purposes, stated value is treated the same way as par value.

a.

True

b.

False

34. The primary purpose of a stock split is to reduce the number of shares outstanding in order to encourage more

investors to enter the market for the company’s shares.

a.

True

b.

False

35. The financial loss that each stockholder in a corporation can incur is usually limited to the amount invested by the

stockholder.

a.

True

b.

False

36. The stock dividends distributable account is listed in the Current Liabilities section of the balance sheet.

a.

True

b.

False

37. While some businesses have been granted charters under state laws, most businesses receive their charters under

federal laws.

a.

True

b.

False

38. If 50,000 shares are authorized, 41,000 shares are issued, and 2,000 shares are reacquired, the number of outstanding

shares is 43,000.

a.

True

b.

False

39. A 10% stock dividend will increase the number of shares outstanding, but the book value per share will decrease.

a.

True

b.

False

40. The net increase or decrease in Retained Earnings for a period is recorded by closing entries.

a.

True

b.

False

41. The amount of a corporation’s retained earnings that has been restricted/appropriated should be reported in the notes to

the financial statements.

Name:

Class:

Date:

chapter 13

a.

True

b.

False

42. Double taxation is a disadvantage of a corporation because the corporation has to pay income taxes at twice the rate

applied to partnerships.

a.

True

b.

False

43. Paid-in capital may originate from real estate transactions.

a.

True

b.

False

44. The cost method of accounting for the purchase and sale of treasury stock is a commonly used method.

a.

True

b.

False

45. When no-par common stock with a stated value is issued for cash, the common stock account is credited for an

amount equal to the cash proceeds.

a.

True

b.

False

46. One of the prerequisites to paying a cash dividend is sufficient retained earnings.

a.

True

b.

False

47. Cash dividends are normally paid on shares of treasury stock.

a.

True

b.

False

48. The declaration of a stock dividend decreases a corporation’s stockholders’ equity and increases its liabilities.

a.

True

b.

False

49. A prior period adjustment should be reported as an adjustment to the beginning balance of retained earnings on the

retained earnings statement in the period in which the adjustment was made.

a.

True

b.

False

50. A corporation has 12,000 shares of $20 par stock outstanding that has a current market value of $150. If the

corporation issues a 4-for-1 stock split, the market value of the stock will fall to approximately $50.

a.

True

b.

False

51. Under the cost method, when treasury stock is purchased by the corporation, the par value and the price at which the

stock was originally issued are important.

a.

True

Name:

Class:

Date:

chapter 13

b.

False

52. If 100 shares of treasury stock were purchased for $50 per share and then sold at $60 per share, $1,000 of income is

reported on the income statement.

a.

True

b.

False

53. The main source of paid-in capital is from issuing stock.

a.

True

b.

False

54. The par value of common stock must always be equal to its market value on the date the stock is issued.

a.

True

b.

False

55. Treasury stock is listed in the Stockholders’ Equity section of the balance sheet.

a.

True

b.

False

56. When no-par stock is issued, Common Stock is credited for the selling price of the stock issued.

a.

True

b.

False

57. The par value of stock is an assigned per-share amount defined in many states as legal capital.

a.

True

b.

False

58. A deficit in retained earnings is reported in the Stockholders’ Equity section of the balance sheet.

a.

True

b.

False

59. Before a stock dividend can be declared or paid, there must be sufficient cash.

a.

True

b.

False

60. The balance in Retained Earnings should be interpreted as representing surplus cash left over for dividends.

a.

True

b.

False

Indicate the answer choice that best completes the statement or answers the question.

61. A reduction of par or stated value of stock results from a

a.

liquidating dividend

b.

stock split

c.

stock option

d.

preferred dividend

Name:

Class:

Date:

chapter 13

62. Which of the following would not be considered an advantage of the corporate form of organization?

a.

government regulation

b.

separate legal existence

c.

continuous life

d.

limited liability of stockholders

63. The charter of a corporation provides for the issuance of 100,000 shares of common stock. Assume that 60,000 shares

were originally issued and 10,000 were subsequently reacquired. What is the amount of cash dividends to be paid if a $2–

per-share dividend is declared?

a.

$60,000

b.

$20,000

c.

$120,000

d.

$100,000

64. All of the following are normally found in a corporation’s Stockholders’ Equity section of the balance sheet except

a.

Common Stock

b.

Paid-In Capital in Excess of Par

c.

Dividends in Arrears

d.

Retained Earnings

65. Which of the following statements concerning taxation is accurate?

a.

Corporations pay federal income taxes but not state income taxes.

b.

Corporations pay federal and state income taxes.

c.

Only the owners must pay taxes on corporate income.

d.

Corporations pay income taxes but their owners do not.

66. A corporation has 50,000 shares of $25 par stock outstanding that has a current market value of $120. If the

corporation issues a 5-for-1 stock split, the par value of the stock after the split will be

a.

$5

b.

$60

c.

$25

d.

$24

67. Which of the following statements is not true about a 2-for-1 stock split?

a.

Par value per share is reduced to half of what it was before the split.

b.

Total contributed capital increases.

c.

The market price will probably decrease.

d.

A stockholder with 10 shares before the split owns 20 shares after the split.

68. Sabas Company has issued and outstanding 20,000 shares of $100 par, 2% cumulative preferred stock and 100,000

shares of $50 par common stock. The following amounts were distributed as dividends:

Year 1

$10,000

Year 2

45,000

Year 3

90,000

Name:

Class:

Date:

chapter 13

Determine the dividend per share for preferred and common stock for the second year.

a.

$2.25 and $0

b.

$2.25 and $0.45

c.

$0 and $0.45

d.

$2.00 and $0.45

69. What is the total stockholders’ equity based on the following account balances?

Common Stock

$375,000

Paid-In Capital in Excess of Par

90,000

Retained Earnings

190,000

Treasury Stock

15,000

a.

$670,000

b.

$655,000

c.

$640,000

d.

$565,000

70. A company with 100,000 authorized shares of $4 par common stock issued 40,000 shares at $8. Subsequently, the

company declared a 2% stock dividend on a date when the market price was $11 per share. What is the amount transferred

from the retained earnings account to paid-in capital accounts as a result of the stock dividend?

a.

$3,200

b.

$6,400

c.

$4,800

d.

$8,800

71. A corporation purchased 1,000 shares of its own $5 par common stock at $10 and subsequently sold 500 of the shares

at $20. What amount of revenue is realized from the sale?

a.

$0

b.

$5,000

c.

$2,500

d.

$10,000

72. Which of the following would appear as a prior period adjustment?

a.

loss resulting from the sale of fixed assets

b.

difference between the actual and estimated uncollectible accounts receivable

c.

error in the computation of depreciation expense in the preceding year

d.

loss from the restructuring of assets

73. Par value

a.

is the monetary value assigned per share in the corporate charter

b.

represents what a share of stock is worth

c.

represents the original selling price for a share of stock

d.

is established for a share of stock after it is issued

74. A restriction/appropriation of retained earnings

Name:

Class:

Date:

chapter 13

a.

decreases total assets

b.

increases total retained earnings

c.

decreases total retained earnings

d.

has no effect on total retained earnings

75. When a corporation completes a 3-for-1 stock split,

a.

the ownership interest of current stockholders is decreased

b.

the market price per share of the stock is decreased

c.

the par value per share is decreased

d.

the market price per share of the stock and the par value per share are decreased

76. Characteristics of a corporation include

a.

shareholders who are mutual agents

b.

direct management by the shareholders (owners)

c.

its inability to own property

d.

shareholders who have limited liability

77. When a stock dividend is declared, which of the following accounts is credited?

a.

Common Stock

b.

Dividends Payable

c.

Stock Dividends Distributable

d.

Retained Earnings

78. The journal entry for the issuance of 150 shares of $5 par common stock at par to an attorney in payment of legal fees

for organizing the corporation includes a credit to

a.

Organizational Expenses

b.

Goodwill

c.

Common Stock

d.

Cash

79. Nevada Corporation has 30,000 shares of $25 par stock outstanding that has a current market value of $120. If the

corporation issues a 5-for-1 stock split, the number of shares outstanding will be

a.

60,000

b.

6,000

c.

150,000

d.

15,000

80. The journal entry for the issuance of common stock at a price above par includes a debit to

a.

Organizational Expenses

b.

Common Stock

c.

Cash

d.

Paid-In Capital in Excess of Par—Common Stock

81. Dayton Corporation began the current year with a retained earnings balance of $32,000. During the year, the company

corrected an error made in the prior year, which was a failure to record depreciation expense of $3,000 on

Name:

Class:

Date:

chapter 13

equipment. Also, during the current year, the company earned net income of $12,000 and declared cash dividends of

$7,000. Compute the year-end retained earnings balance.

a.

$34,000

b.

$37,000

c.

$41,000

d.

$44,000

82. A company with 100,000 authorized shares of $4 par common stock issued 50,000 shares at $9. Subsequently, the

company declared a 2% stock dividend on a date when the market price was $10 per share. The effect of the declaration

and issuance of the stock dividend is to

a.

decrease retained earnings, increase common stock, and increase paid-in capital

b.

increase retained earnings, decrease common stock, and decrease paid-in capital

c.

increase retained earnings, decrease common stock, and increase paid-in capital

d.

decrease retained earnings, increase common stock, and decrease paid-in capital

83. Nexis Corp. issues 1,000 shares of $15 par value common stock at $22 per share. When the transaction is journalized,

credits are made to

a.

Common Stock, $15,000, and Paid-In Capital in Excess of Par—Common Stock, $7,000

b.

Common Stock, $22,000, and Retained Earnings, $15,000

c.

Common Stock, $7,000, and Paid-In Capital in Excess of Stated Value, $15,000

d.

Common Stock, $22,000

84. The liability for a dividend is recorded on which of the following dates?

a.

date of record

b.

date of payment

c.

last day of the fiscal year

d.

date of declaration

85. A corporation has 50,000 shares of $28 par stock outstanding that has a current market value of $150 per share. If the

corporation issues a 4-for-1 stock split, the market value of the stock will fall to approximately

a.

$7.00

b.

$112.00

c.

$37.50

d.

$600.00

86. The two main sources of stockholders’ equity are

a.

investments by stockholders and net income retained in the business

b.

investments by stockholders and dividends paid

c.

net income retained in the business and dividends paid

d.

investments by stockholders and purchases of assets

87. If Dakota Company issues 1,500 shares of $6 par common stock for $75,000,

a.

Common Stock will be credited for $75,000

b.

Paid-In Capital in Excess of Par will be credited for $9,000

c.

Paid-In Capital in Excess of Par will be credited for $66,000

Name:

Class:

Date:

chapter 13

d.

Cash will be debited for $66,000

88. Treasury stock should be reported in the financial statements of a corporation as a(n)

a.

investment

b.

liability

c.

current asset

d.

deduction from stockholders’ equity

89. A corporation has 50,000 shares of $25 par stock outstanding that has a current market value of $150 per share. If the

corporation issues a 5-for-1 stock split, the market value of the stock after the split will be approximately

a.

$25

b.

$150

c.

$5

d.

$30

90. The charter of a corporation provides for the issuance of 100,000 shares of common stock. Assume that 40,000 shares

were originally issued and 10,000 were subsequently reacquired. What is the number of shares outstanding?

a.

10,000

b.

40,000

c.

30,000

d.

50,000

91. One of the main disadvantages of the corporate form is the

a.

professional management

b.

double taxation of dividends

c.

charter

d.

requirement to stock

92. The primary purpose of a stock split is to

a.

increase paid-in capital

b.

reduce the market price of the stock per share

c.

increase the market price of the stock per share

d.

increase retained earnings

93. Significant changes in stockholders’ equity are reported on the

a.

income statement

b.

retained earnings statement

c.

statement of stockholders’ equity

d.

statement of cash flows

94. When Wisconsin Corporation was formed on January 1, the corporate charter provided for 100,000 shares of $10 par

value common stock. During its first month of operation, the corporation issued 8,500 shares of stock at a price of $16 per

share.

The journal entry for this transaction would include a

Name:

Class:

Date:

chapter 13

100. A corporation purchases 10,000 shares of its own $10 par common stock for $35 per share, recording it at cost. What

a.

debit to Cash for $85,000

b.

credit to Common Stock for $136,000

c.

credit to Paid-In Capital in Excess of Par—Common Stock for $51,000

d.

debit to Common Stock for $85,000

95. In which section of the financial statements would Paid-In Capital from Sale of Treasury Stock be reported?

a.

Other Expense section of the income statement

b.

Intangible Assets section of the balance sheet

c.

Stockholders’ Equity section of the balance sheet

d.

Other Income section of the income statement

96. The date on which a cash dividend becomes a binding legal obligation is the

a.

declaration date

b.

date of record

c.

payment date

d.

last day of the fiscal year

97. How is treasury stock shown on the balance sheet?

a.

as an asset

b.

as a decrease in stockholders’ equity

c.

as an increase in stockholders’ equity

d.

Treasury stock is not shown on the balance sheet.

98. Sabas Company has 20,000 shares of $100 par, 2% cumulative preferred stock and 100,000 shares of $50 par common

stock. The following amounts were distributed as dividends:

Year 1

$10,000

Year 2

45,000

Year 3

90,000

Determine the dividends in arrears for preferred stock for the second year.

a.

$25,000

b.

$10,000

c.

$0

d.

$30,000

99. What is the total stockholders’ equity based on the following data?

Common Stock

$360,000

Paid-in Capital in Excess of Par

735,000

Retained Earnings (deficit)

(56,000)

a.

$1,095,000

b.

$1,151,000

c.

$1,039,000

d.

$679,000

Name:

Class:

Date:

chapter 13

will be the effect on total stockholders’ equity?

a.

increase by $100,000

b.

increase by $350,000

c.

decrease by $100,000

d.

decrease by $350,000

101. Sabas Company has issued and outstanding 20,000 shares of $100 par, 2% cumulative preferred stock and 100,000

shares of $50 par common stock. The following amounts were distributed as dividends:

Year 1

$10,000

Year 2

45,000

Year 3

90,000

Determine the dividend per share for preferred and common stock for the third year.

a.

$4.50 and $0.25

b.

$3.25 and $0.25

c.

$4.50 and $0.90

d.

$2.00 and $0.25

102. Which of the following is not a reason for a corporation to buy back its own stock?

a.

resale to employees

b.

bonus to employees

c.

support the market price of the stock

d.

increase the shares outstanding

103. Treasury stock shares are

a.

shares held by the U.S. Treasury Department

b.

part of the total outstanding shares but not part of the total issued shares of a corporation

c.

unissued shares that are held by the treasurer of the corporation

d.

issued shares that have been reacquired by a corporation

104. The charter of a corporation provides for the issuance of 100,000 shares of common stock. Assume that 30,000

shares were originally issued and 5,000 were subsequently reacquired. What is the number of shares outstanding?

a.

35,000

b.

70,000

c.

25,000

d.

30,000

105. Treasury stock that had been purchased for $5,600 last month was reissued this month for $8,500. The journal entry

for the reissuance would include a credit to

a.

Treasury Stock for $8,500

b.

Paid-In Capital from Sale of Treasury Stock for $8,500

c.

Paid-In Capital in Excess of Par—Common Stock for $2,900

d.

Paid-In Capital from Sale of Treasury Stock for $2,900

106. Sneed Corporation issues 10,000 shares of $50 par preferred stock for cash at $75 per share. The journal entry for the

Name:

Class:

Date:

chapter 13

transaction will consist of a debit to Cash for $750,000 and a credit or credits to

a.

Preferred Stock for $750,000

b.

Preferred Stock for $500,000 and Paid-In Capital in Excess of Par—Preferred Stock for $250,000

c.

Preferred Stock for $500,000 and Retained Earnings for $250,000

d.

Paid-In Capital from Preferred Stock for $750,000

107. If common stock is issued for an amount greater than par value, the excess should be credited to

a.

Retained Earnings

b.

Cash

c.

Legal Capital

d.

Paid-In Capital in Excess of Par

108. Sabas Company has 20,000 shares of $100 par, 2% cumulative preferred stock and 100,000 shares of $50 par

common stock. The following amounts were distributed as dividends:

Year 1:

$10,000

Year 2:

45,000

Year 3:

90,000

Determine the dividend per share for preferred and common stock for the first year.

a.

$0.50 and $0.10

b.

$0 and $0.10

c.

$0.50 and $0

d.

$2.00 and $0

109. Those most responsible for the major policy decisions of a corporation are the

a.

management

b.

board of directors

c.

employees

d.

stockholders

110. Earnings per share

a.

is the net income per common share

b.

must be reported by a public company

c.

helps compare companies of different sizes

d.

All of these choices

111. The excess of sales price of treasury stock over its cost should be credited to

a.

Treasury Stock Receivable

b.

Premium on Capital Stock

c.

Paid-In Capital from Sale of Treasury Stock

d.

Income from Sale of Treasury Stock

112. The cumulative effect of the declaration and payment of a cash dividend on a company’s financial statements is to

a.

decrease total liabilities and stockholders’ equity

b.

increase total expenses and total liabilities

Name:

Class:

Date:

chapter 13

c.

increase total assets and stockholders’ equity

d.

decrease total assets and stockholders’ equity

113. On January 1, Vermont Corporation had 40,000 shares of $10 par value common stock issued and outstanding. All

40,000 shares had been issued in a prior period at $20 per share. On February 1, Vermont purchased 3,750 shares of

treasury stock for $24 per share and later sold the treasury shares for $21 per share on March 1.

The journal entry for the purchase of the treasury shares on February 1 would include a

a.

credit to Treasury Stock for $90,000

b.

debit to Treasury Stock for $90,000

c.

debit to a loss account for $112,500

d.

credit to a gain account for $112,500

114. Under the corporate form of business organization,

a.

ownership rights are easily transferred

b.

a stockholder is personally liable for the debts of the corporation

c.

stockholders’ acts can bind the corporation even though the stockholders have not been appointed as agents of

the corporation

d.

stockholders wishing to sell their corporate shares must get the approval of other stockholders

115. A corporation has 50,000 shares of $25 par stock outstanding. If the corporation issues a 3-for-1 stock split, the

number of shares outstanding after the split will be

a.

150,000 shares

b.

50,000 shares

c.

100,000 shares

d.

16,666 shares

116. Nebraska Inc. issues 3,000 shares of common stock for $45,000. The stock has a stated value of $10 per share. The

journal entry for the stock issuance would include a credit to Common Stock for

a.

$30,000

b.

$45,000

c.

$15,000

d.

$3,000

117. Stockholders’ equity

a.

is usually equal to cash on hand

b.

includes paid-in capital and liabilities

c.

includes retained earnings and paid–in capital

d.

is shown on the income statement

118. Which of the following is not classified as paid-in capital on the balance sheet?

a.

common stock

b.

common stock distributable

c.

excess of issue price over par

d.

treasury stock

Name:

Class:

Date:

chapter 13

119. The par value per share of common stock represents the

a.

minimum selling price of the stock established by the articles of incorporation

b.

minimum amount the stockholder will receive when the corporation is liquidated

c.

dollar amount assigned to each share

d.

amount of dividend per share to be received each year

120. A company with 100,000 authorized shares of $4 par common stock issued 40,000 shares at $8. Subsequently, the

company declared a 4% stock dividend on a date when the market price was $12 per share. What is the amount transferred

from the retained earnings account to paid-in capital accounts as a result of the stock dividend?

a.

$12,800

b.

$19,200

c.

$32,000

d.

$48,800

121. Alma Corp. issues 1,000 shares of $10 par common stock at $14 per share. When the transaction is journalized,

credits are made to

a.

Common Stock, $14,000

b.

Common Stock, $10,000, and Paid-In Capital in Excess of Par—Common Stock, $4,000

c.

Common Stock, $4,000, and Paid-In Capital in Excess of Stated Value, $10,000

d.

Common Stock, $10,000, and Retained Earnings, $4,000

122. Which of the following is not a characteristic of a corporation?

a.

The financial loss that a stockholder may suffer from owning stock in a public company is limited.

b.

Cash dividends paid by a corporation are deductible as expenses by the corporation.

c.

A corporation can own property in its name.

d.

Corporations are required to file federal income tax returns.

123. The price at which a stock can be sold depends on a number of factors. Which of the following is not one of those

factors?

a.

the financial condition, earnings record, and dividend record of the corporation

b.

investor expectations of the corporation‘s earning power

c.

how high the par value is

d.

general business and economic conditions and prospects

124. The ability of a corporation to obtain capital is

a.

less than the ability of a partnership

b.

about the same as the ability of a partnership

c.

restricted because of the limited life of the corporation

d.

enhanced because of limited liability and ease of share transferability

125. Oregon, Inc., reported net income of $105,000. During the current year, the company had 5,000 shares of $100 par,

5% preferred stock and 10,000 shares of $5 par common stock outstanding. Oregon’s earnings per share is

a.

$8.00

b.

$18.00

c.

$5.08

Name:

Class:

Date:

chapter 13

d.

$5.00

126. Which of the following amounts should be disclosed in the Stockholders’ Equity section of the balance sheet?

a.

the number of shares of common stock outstanding

b.

the number of shares of common stock issued

c.

the number of shares of common stock authorized

d.

All of these choices

127. Which of the following is not a right possessed by common stockholders of a corporation?

a.

the right to vote in the election of the board of directors

b.

the right to receive a minimum amount of dividends

c.

the right to sell their stock to anyone they choose

d.

the right to share in assets upon liquidation

128. The excess of issue price over par of common stock is termed a(n)

a.

discount

b.

income

c.

deficit

d.

premium

129. The state charter allows a corporation to issue only a certain number of shares of each class of stock. This amount of

stock is called

a.

treasury stock

b.

issued stock

c.

outstanding stock

d.

authorized stock

130. Which of the following is not true of a corporation?

a.

It may enter into binding legal contracts in its own name.

b.

It may sue and be sued.

c.

The acts of its owners bind the corporation.

d.

It may buy, own, and sell property.

131. A disadvantage of the corporate form of business entity is

a.

mutual agency for stockholders

b.

unlimited liability for stockholders

c.

corporations are subject to more governmental regulations

d.

the ease of transfer of ownership

132. The term deficit is used to refer to a debit balance in which of the following accounts of a corporation?

a.

Retained Earnings

b.

Treasury Stock

c.

Organizational Expenses

d.

Common Stock

Name:

Class:

Date:

chapter 13

133. Treasury stock that was purchased for $3,000 is sold for $3,500. As a result of these two transactions combined,

a.

income will be increased by $500

b.

stockholders’ equity will be increased by $3,500

c.

stockholders’ equity will be increased by $500

d.

stockholders’ equity will not change

134. The authorized stock of a corporation

a.

must be recorded in a formal accounting entry

b.

only reflects the initial capital needs of the company

c.

is indicated in its bylaws

d.

is indicated in its charter

135. Kansas Company acquired a building valued at $210,000 for property tax purposes in exchange for 12,000 shares of

its $5 par common stock. The stock is widely traded and selling for $15 per share. At what amount should the building be

recorded by Kansas Company?

a.

$60,000

b.

$180,000

c.

$210,000

d.

$120,000

136. The charter of a corporation provides for the issuance of 100,000 shares of common stock. Assume that 45,000

shares were originally issued and 5,000 were subsequently reacquired. What is the amount of cash dividends to be paid if

a $2-per-share dividend is declared?

a.

$80,000

b.

$10,000

c.

$90,000

d.

$100,00

137. Which of the following is the appropriate journal entry for the declaration of cash dividends?

a.

Retained Earnings

Cash

b.

Cash Dividends Payable

Cash

c.

Paid-In Capital

Cash Dividends Payable

d.

Cash Dividends

Cash Dividends Payable

138. Texas Inc. has 10,000 shares of 6%, $125 par value cumulative preferred stock and 50,000 shares of $1 par value

common stock outstanding at December 31. What is the annual dividend on the preferred stock?

a.

$60 per share

b.

$75,000 in total

c.

$10,000 in total

d.

$0.75 per share

139. Which of the following is not a prerequisite to paying a cash dividend?

Name:

Class:

Date:

chapter 13

a.

formal action by the board of directors

b.

market value in excess of par value per share

c.

sufficient cash

d.

sufficient retained earnings

140. Retained earnings

a.

is the same as contributed capital

b.

cannot have a debit balance

c.

changes are summarized in the retained earnings statement

d.

is equal to cash on hand

Match each of the following stockholders’ equity concepts to the most appropriate term (a–h).

a.

Authorized shares

b.

Issued shares

c.

Outstanding shares

d.

Par value

e.

Common stock

f.

Preferred stock

g.

Paid-In Capital in Excess of Par

h.

Transfer agent

141. The account used to record the difference when issue price exceeds par value of stock

142. The dollar amount assigned to each share of stock

143. The number of shares currently held by stockholders

144. A class of stock having first rights to dividends of a corporation

145. The maximum number of shares a company can issue to shareholders

146. The number of shares sold to stockholders

147. A class of stock that provides no preference rights to shareholders

148. A financial institution that records and maintains records of another company’s stockholders

Match each of the following stockholders’ equity concepts to the appropriate term (a–h).

a.

Cash dividend

b.

Date of record

c.

Stock Dividends Distributable

d.

Date of declaration

e.

Treasury stock

f.

Preferred stock

Name:

Class:

Date:

chapter 13

g.

Date of payment

h.

Paid-In Capital in Excess of Par

149. Equity account reflecting shares “owed” to stockholders

150. Shares of common stock that were issued and then reacquired by a company

151. Owners of this class of stock are entitled to receive dividends first

152. Cash distribution of a company’s earnings to stockholders

153. Account used when shares are issued for an amount greater than par value

154. The day of the event that creates a liability to company

155. The date that is used to determine the owners of stock who will receive the current dividend

156. The date when dividends are actually distributed to stockholders

Match each of the following stockholders’ equity concepts to the appropriate term (a–h).

a.

Articles of incorporation

b.

Limited liability

c.

Bylaws

d.

Corporation

e.

Public corporation

f.

Board of directors

g.

Private corporation

h.

Dividends

157. A legal entity, separate from the people who create and operate it

158. A company whose shares can be bought and sold in public markets

159. The rules and procedures for conducting a corporation’s affairs

160. A company whose shares are not bought or sold in public markets

161. Document that formally creates a corporation

162. Creditors cannot pursue stockholders’ personal assets to satisfy claims

163. Group that meets periodically to establish corporate policies

164. Corporate income distributed to stockholders

Match each of the following equations to the appropriate result (a–h).

a.

Treasury Stock

b.

Retained Earnings (ending)

Name:

Class:

Date:

chapter 13

c.

Preferred Stock

d.

Excess of Issue Price over Par (preferred)

e.

Common Stock

f.

Total Paid-In Capital

g.

Excess of Issue Price over Par (common)

h.

Total Stockholders’ Equity

165. Number of Shares of Preferred Stock Issued × Par Value of Preferred Stock

166. (Price of Common Stock – Par Value of Common Stock) × Number of Shares of Common Stock Issued

167. (Price of Preferred Stock – Par Value of Preferred Stock) × Number of Shares of Preferred Stock Issued

168. Par Value of Common Stock × Number of Shares of Common Stock Issued

169. Beginning Retained Earnings + Net Income – Cash Dividends

170. Preferred Stock + Excess of Issue Price over Par (Preferred) + Common Stock + Excess of Issue Price over Par

(Common) + Paid-In Capital from Sale of Treasury Stock

171. Total Paid-In Capital + Retained Earnings – Treasury Stock

172. Number of Reacquired Shares of Common Stock × Purchase Price of Common Stock

173. Sabas Company has 20,000 shares of $100 par, 2% cumulative preferred stock and 100,000 shares of $50 par

common stock. The following amounts were distributed as dividends:

Year 1

$20,000

Year 2

50,000

Year 3

90,000

Determine the dividend per share for preferred and common stock for each year.

174. On May 10, a company issued for cash 1,500 shares of no-par common stock (with a stated value of $2) at $14, and

on May 15, it issued for cash 2,000 shares of $15 par preferred stock at $58.

Journalize the entries for May 10 and 15, assuming that the common stock is to be credited with the stated value.

175. Selected transactions completed by Breezeway Construction during the current fiscal year are as follows:

Feb. 3

Split the common stock 2-for-1 and reduced the par from $40 to $20 per share. After the split,

there were 250,000 common shares outstanding.

Apr. 10

Declared semiannual dividends of $1.50 on 18,000 shares of preferred stock and $0.08 on the

common stock to stockholders of record on May 10, payable on June 9.

June 9

Paid the cash dividends.

Oct. 10

Declared semiannual dividends of $1.50 on the preferred stock and $0.04 on the common

Name:

Class:

Date:

chapter 13

stock (before the stock dividend). In addition, a 2% common stock dividend was declared on

the common stock outstanding. The fair market value of the common stock is estimated at

$36.

Dec. 9

Paid the cash dividends and issued the certificates for the common stock dividend.

Journalize these transactions.

176. A corporation, which had 18,000 shares of common stock outstanding, declared a 3-for-1 stock split.

a.

What will be the number of shares outstanding after the split?

b.

If the common stock had a market price of $240 per share before the stock split, what

would be an approximate market price per share after the split?

c.

Journalize the entry for the stock split.

177. A company had stock outstanding as follows during each of its first three years of operations: 2,500 shares of 10%,

$100 par, cumulative preferred stock and 50,000 shares of $10 par common stock. The amounts distributed as dividends

follow. Determine the total and per-share dividends for each class of stock for each year by completing the schedule.

Preferred

Common

Year

Dividends

Total

Per Share

Total

Per Share

1

$10,000

_________

_________

_________

_________

2

25,000

_________

_________

_________

_________

3

60,000

_________

_________

_________

_________

178. On April 2 a corporation purchased for cash 5,000 shares of its own $10 par common stock at $16 per share. It sold

3,000 of the treasury shares at $19 per share on June 10. The remaining 2,000 shares were sold on November 10 for $12

per share.

a. Journalize the entries for the purchase (treasury stock is recorded at cost).

b. Journalize the entries for the sale of the stock.

179. The dates of importance in connection with a cash dividend of $50,000 on a corporation’s common stock are January

15, February 15, and March 15. Journalize the entries required on each date.

180. Indicate whether the following actions would (+) increase, (–) decrease, or (0) not affect a company’s total assets,

liabilities, and stockholders’ equity.

Stockholders’

Assets

Liabilities

Equity

a.

Declaring a cash dividend

_______

_______

_______

b.

Paying the cash dividend declared in (a)

_______

_______

_______

c.

Declaring a stock dividend

_______

_______

_______

d.

Issuing stock certificates for the stock

dividend declared in (c)

_______

_______

_______

181. Sabas Company has issued and outstanding 20,000 shares of $100 par, 1% noncumulative preferred stock and

100,000 shares of $50 par common stock. The following amounts were distributed as dividends:

Year 1

$10,000

Year 2

15,000

Year 3

90,000

Determine the dividend per share for preferred and common stock for each year.

Name:

Class:

Date:

chapter 13

182. The following account balances appeared on the balance sheet of Osgood Industries at the beginning of the period:

Common Stock (300,000 shares authorized, $100 par)

$10,000,000

Paid-In Capital in Excess of Par—Common Stock

2,000,000

Retained Earnings

45,000,000

During the period, the board of directors declared a 2% stock dividend when the market price of the stock was $135 per

share.

a.

Journalize the entries for the following:

(1)

Declaration of the dividend, capitalizing an amount equal to market value

(2)

Issuance of the stock certificates

b.

Determine the following amounts before the stock dividend was declared:

(1)

Total paid-in capital

(2)

Total retained earnings

(3)

Total stockholders’ equity

c.

Determine the following amounts after the stock dividend was declared and closing

entries were made at the end of the year:

(1)

Total paid-in capital

(2)

Total retained earnings

(3)

Total stockholders’ equity

183. Journalize the following selected transactions completed during the current fiscal year:

Mar. 24

The board of directors of New Town, Inc., declared a stock split that reduced the par

of common shares from $100 to $20. This action increased the number of outstanding

shares to 500,000.

26

Declared a dividend of $1.75 per share on the outstanding shares of common stock.

Apr. 5

Paid the dividend declared on March 26.

Nov. 1

Declared a 5% stock dividend on the common stock outstanding (the fair market value

of the stock to be issued is $25).

Dec. 1

Issued the certificates for the common stock dividend declared on November 1.

184. Solar Company has 600,000 shares of $75 par common stock outstanding. On February 13, Solar declared a 3%

stock dividend to be issued on April 30 to stockholders of record on March 14. The market price of the stock was $90 per

share on February 13.

Journalize the entries required on February 13, March 14, and April 30.

185. Journalize the following transactions for Maine Corp.:

a.

Issued 2,000 shares of $10 par common stock at $72 for cash.

b.

Issued 2,500 shares of common stock in exchange for land with a fair market price of

$130,000.

c.

Purchased 400 shares of treasury stock at $70.

d.

Sold the 400 shares of treasury stock purchased in (c) at $76.

186. Vincent Corporation has 100,000 shares of $100 par common stock outstanding. On June 30, Vincent Corporation

Name:

Class:

Date:

chapter 13

declared a 5% stock dividend to be issued on July 30 to stockholders of record July 15. The market price of the stock was

$132 a share on June 30. Journalize the entries required on June 30, July 15, and July 30.

187. Sabas Company has issued and outstanding 40,000 shares of $100 par, 1% preferred stock and 100,000 shares of $50

par common stock. The following amounts were distributed as dividends:

Year 1

$50,000

Year 2

90,000

Year 3

130,000

Determine the dividend per share for preferred and common stock for each year.

188. On February 1, Marine Company reacquired 7,500 shares of its common stock at $30 per share. On March 15,

Marine sold 4,500 of the reacquired shares at $34 per share. On June 2, Marine sold the remaining shares at $28 per share.

Journalize the transactions of February 1, March 15, and June 2.

189. Torre Company has the following stockholders’ equity account balances on December 31:

Common Stock, $5 par (60,000 shares issued)

$300,000

Paid-In Capital in Excess of Par—Common Stock

600,000

Preferred Stock, $100 par (5,000 shares issued)

500,000

Paid-In Capital in Excess of Par—Preferred Stock

100,000

Retained Earnings

200,000

Treasury Stock (cost, $12 per share)

60,000

a.

How many shares of treasury stock are owned?

b.

What was the average market price per share at which common stock was issued?

c.

What was the average market price per share at which preferred stock was issued?

d.

What is the total value of the paid-in capital portion of stockholders’ equity?

e.

What is the total value of stockholders’ equity?

f.

How many shares of common stock are outstanding?

g.

If net income for the year was $75,000 and a preferred stock dividend of $20,000 was paid, what

was the beginning value of retained earnings? How much is earnings per share for the year?

190. On January 1, Year 1, a company had the following transactions:

• Issued 10,000 shares of $2 par common stock for $12 per share.

• Issued 3,000 shares of $50 par, 6% cumulative preferred stock for $70 per share.

• Purchased 1,000 shares of previously issued common stock for $15 per share.

The company had the following dividend information available:

Year 1

No dividend paid

Year 2

Paid $2,000 total dividends

Year 3

Paid $20,000 total dividends

Year 4

Paid $25,000 total dividends

Using the following format, fill in the correct values for each year:

Year 1

Year 2

Year 3

Year 4

Name:

Class:

Date:

chapter 13

Common stock dividend

______

______

______

______

Preferred stock dividend

______

______

______

______

Dividends in arrears

______

______

______

______

191. A company has 10,000 shares of $10 par common stock outstanding. Journalize the following transactions:

a.

Purchased 1,000 shares of treasury stock at $12. The treasury stock is accounted for by the

cost method. There were no previous purchases of treasury shares.

b.

Sold 500 shares of treasury stock at $15.

c.

Purchased equipment for $75,000, paying $25,000 in cash and issuing 4,000 shares of

common stock for the remaining.

d.

Sold 500 shares of treasury stock at $11.

192. On April 10, a company acquired land in exchange for 1,000 shares of $20 par common stock with a current market

price of $73. Journalize this transaction.

193. On May 1, 10,000 shares of $10 par common stock were issued at $30, and on May 7, 5,000 shares of $50 par

preferred stock were issued at $111. Journalize the entries for May 1 and 7.

194. On February 1 of the current year, Motor, Inc., issued 700 shares of $2 par common stock to an attorney in return for

preparing and filing the articles of incorporation. The value of the services is $9,600. Journalize this transaction.

195. A corporation was organized on January 1 of the current year with an authorization of 20,000 shares of 4%, $12 par

preferred stock and 100,000 shares of $3 par common stock.

The following selected transactions were completed during the first year of operations:

Jan. 3

Issued 15,000 shares of common stock at $23 per share for cash.

31

Issued 200 shares of common stock to an attorney in payment of legal

fees for organizing the corporation. The value of the stock at the time

of payment was $25 per share.

Feb. 24

Issued 20,000 shares of common stock in exchange for land, buildings,

and equipment with fair market prices of $65,000, $120,000, and

$45,000, respectively.

Mar. 15

Issued 2,000 shares of preferred stock at $56 for cash.

Journalize the transactions.

196. Journalize the following transactions:

a.

Issued 1,000 shares of $10 par common stock at $56 for cash.

b.

Issued 1,400 shares of $10 par common stock in exchange for equipment with a fair

market price of $21,000.

c.

Purchased 100 shares of treasury stock at $25.

d.

Sold the 100 shares of treasury stock purchased in (c) at $30.

197. A company had the following stockholders’ equity information available at year-end:

Issued 11,000 shares of $2 par common stock for $12 per share.

Issued 5,000 shares of $50 par, 6% preferred stock for $70 per share.

Name:

Class:

Date:

chapter 13

Purchased 1,000 shares of previously issued common stock for $15 per share.

Reported net income of $200,000.

Declared and paid the preferred stock dividend.

Determine the earnings per share for the current year.

198. On June 5, Belen Corporation reacquired 3,300 shares of its own common stock at $45 per share. On July 15, Belen

sold 2,000 of the reacquired shares at $48 per share. On August 30, Belen sold the remaining shares at $42 per share.

Journalize the transactions of June 5, July 15, and August 30.

199. Using the following accounts and balances, prepare the Stockholders’ Equity section of the balance sheet using

Method 1 (separating sources of additional paid-in capital). Fifty thousand shares of common stock are authorized, and

5,000 shares have been reacquired.

Common Stock, $50 par

$1,250,000

Paid-In Capital in Excess of Par

800,000

Paid-In Capital from Sale of Treasury Stock

42,000

Retained Earnings

4,350,000

Treasury Stock

155,000

200. Wonder Sales is authorized to issue 100,000 shares of 2%, $100 par preferred stock and 1,000,000 shares of $10 par

common stock. Journalize the following transactions:

a. On January 2, Wonder Sales issues 5,000 shares of preferred stock for $110 per share and 65,000 shares of

common stock at $10 per share.

b. On January 25, Wonder Sales issues 250 shares of preferred stock to Morton Law Firm for settlement of a $36,000

invoice for incorporation services.

c. On January 31, Wonder Sales issues 500 shares of common stock to Setup Inc. for fixtures that have a fair market

value of $8,500.

201. At December 31, Idaho Company had the following ending account balances:

Retained Earnings

$250,000

Preferred Stock ($100 par, 7% cumulative, 10,000 authorized, 5,000 issued and outstanding)

500,000

Treasury Stock

40,000

Paid-In Capital in Excess of Par—Common Stock

625,000

Paid-In Capital in Excess of Par—Preferred Stock

50,000

Common Stock ($5 par value, 500,000 shares authorized, 105,000 issued)

525,000

Prepare the Stockholders’ Equity section of the balance sheet using Method 2 (showing combined additional paid-in

capital).

202. The following transaction took place for XYZ Corporation:

Nov. 12

Declared a total cash dividend of $45,000 for stockholders of record November 20 payable on

December 1.

a. Journalize the entries required by these events.

b. Briefly describe the significance of November 20.

203. Firefly, Inc., reported the following results for the year ending July 31:

Name:

Class:

Date:

chapter 13

Retained earnings, August 1

$875,000

Net income

450,000

Cash dividends declared

140,000

Stock dividends declared

60,000

Prepare a retained earnings statement for the fiscal year ended July 31.

204. On April 10, Maranda Corporation issued for cash 11,000 shares of no-par common stock at $25. On May 5,

Maranda issued at par 1,000 shares of 4%, $50 par preferred stock for cash. On May 25, Maranda issued for cash 15,000

shares of 4%, $50 par preferred stock at $55.

Journalize the entries for the April 10, May 5, and May 25 transactions.

205. Journalize the following transactions:

a.

Issued 1,000 shares of $15 par common stock at $54 for cash.

b.

Issued 1,400 shares of no-par common stock in exchange for equipment with a fair

market price of $24,000.

c.

Purchased 100 shares of treasury stock at $26.

d.

Sold 100 shares of treasury stock purchased in (c) at $29.

206. Macy Company has issued and outstanding 10,000 shares of 2% cumulative preferred stock of $50 par and 25,000

shares of $75 par common stock. The following amounts were distributed as dividends:

Year 1

$30,000

Year 2

6,000

Year 3

80,000

Determine the dividend per share for preferred and common stock for each year.

207. Journalize the following transactions:

a.

Issued 1,000 shares of $10 par common stock at $59 for cash.

b.

Issued 1,400 shares of $10 par common stock in exchange for equipment with a fair

market price of $60,000.

c.

Purchased 100 shares of treasury stock at $32.

d.

Sold the 100 shares of treasury stock purchased in (c) at $42.

208. A company has 10,000 shares of $10 par common stock outstanding. Journalize the following transactions:

a.

Purchased 1,500 shares of treasury stock at $16. The treasury stock is accounted for by the

cost method. There were no previous purchases of treasury shares.

b.

Sold 1,000 shares of treasury stock at $19.

c.

Purchased equipment for $80,000, paying $25,000 in cash and issuing 4,000 shares of

common stock.

d.

Sold 500 shares of treasury stock at $14.

209. Carmen Company is a corporation that has issued both preferred and common stock. As of January 1, it had 50,000

shares of 2.75%, $100 par, preferred stock outstanding and 250,000 shares of $10 par common stock outstanding.

Journalize the following transactions:

a. On January 31, the board of directors issues a requirement to purchase 5,000 shares of its common stock at market

price. The shares are purchased at a market price of $22 per share.

b. On March 15, Carmen declares a dividend on preferred stock of $2.75 per share. The date of record is March 25 and the

Name:

Class:

Date:

chapter 13

date of payment is March 31.

c. On December 1, Carmen declares a cash dividend on common stock of $0.12 per share. The date of record is December

15 and the date of payment is December 21.

d. On December 27, the board orders that 2,500 shares of the treasury stock purchased in (a) be sold. The sale price is $25

per share.

210. Journalize the following selected transactions completed during the current fiscal year:

Feb. 1

The board of directors declared a stock split that reduced the par of common shares

from $100 to $20. This action increased the number of outstanding shares to 500,000.

11

Purchased 25,000 shares of the company’s own stock at $44, recording the treasury

stock at cost.

May 1

Declared a dividend of $2.50 per share on the outstanding shares of common stock.

15

Paid the dividend declared on May 1.

Oct. 19

Declared a 2% stock dividend on the common stock outstanding (the fair market value

of the stock to be issued is $55).

Nov. 12

Issued the certificates for the common stock dividend declared on October 19.

211. Journalize the following selected transactions completed during the current fiscal year:

Jan. 3

The board of directors declared a stock split that reduced the par of common shares

from $100 to $20. This action increased the number of outstanding shares to 400,000.

22

Declared a dividend of $1.75 per share on the outstanding shares of common stock.

Feb. 8

Paid the dividend declared on January 22.

Sept. 1

Declared a 5% stock dividend on the common stock outstanding (the fair market value

of the stock to be issued is $30.)

Oct. 1

Issued the certificates for the common stock dividend declared on September 1.

212. Using the following information, prepare the Stockholders’ Equity section of the balance sheet using Method 1

(separating sources of additional paid–in capital). Seventy thousand shares of common stock are authorized and 7,000

shares have been reacquired.

Common Stock, $75 par

$4,725,000

Paid-In Capital in Excess of Par

679,000

Paid-In Capital from Sale of Treasury Stock

25,200

Retained Earnings

2,032,800

Treasury Stock

600,000

213. On February 13, Epperson Company issued for cash 75,000 shares of no-par common stock (with a stated value of

$125) at $140. On September 9, Epperson issued at par 15,000 shares of 1%, $60 par preferred stock at par for cash. On

November 23, Epperson issued for cash 8,000 shares of 1%, $60 par preferred stock at $70.

Journalize the entries for the February 13, September 9, and November 23 transactions.

214. Marcos Company, which had 35,000 shares of common stock outstanding, declared a 4-for-1 stock split.

Name:

Class:

Date:

chapter 13

a.

What will be the number of shares outstanding after the split?

b.

If the common stock had a market price of $280 per share before the stock split, what

would be an approximate market price per share after the split?

215. On March 4 of the current year, Barefoot Bay, Inc. reacquired 5,000 shares of its common stock at $89 per share. On

August 7, Barefoot Bay sold 3,500 of the reacquired shares at $100 per share. The remaining 1,500 shares were sold at

$88 per share on November 29.

a.

Journalize the transactions of March 4, August 7, and November 29.

b.

What is the balance in Paid-In Capital from Sale of Treasury Stock on December 31 of

the current year?

c.

Why might Barefoot Bay, Inc. have purchased the treasury stock?

216. On April 1, 10,000 shares of $5 par common stock were issued at $22, and on April 7, 5,000 shares of $50 par

preferred stock were issued at $104. Journalize the entries for April 1 and 7.

217. Big Bluestem Inc. reported the following results for the year ending April 30:

Retained earnings, May 1

$3,750,000

Net income

720,000

Cash dividends declared

80,000

Stock dividends declared

220,000

Prepare a retained earnings statement for the fiscal year ended April 30.

Name:

Class:

Date:

chapter 13

Answer Key

Name:

Class:

Date:

chapter 13

Name:

Class:

Date:

chapter 13

Name:

Class:

Date:

chapter 13

Name:

Class:

Date:

chapter 13

Name:

Class:

Date:

chapter 13

Name:

Class:

Date:

chapter 13

Name:

Class:

Date:

chapter 13

Name:

Class:

Date:

chapter 13

Name:

Class:

Date:

chapter 13

Name:

Class:

Date:

chapter 13

Name:

Class:

Date:

chapter 13

Name:

Class:

Date:

chapter 13

Name:

Class:

Date:

chapter 13

Name:

Class:

Date:

chapter 13

Name:

Class:

Date:

chapter 13

Name:

Class:

Date:

chapter 13

Name:

Class:

Date:

chapter 13

Name:

Class:

Date:

chapter 13