11) Successful implementation of a product differentiation strategy will result in ________.

A) a large favorable growth and price-recovery components

B) a large favorable price-recovery and productivity components

C) a large favorable productivity and growth components

D) only a large favorable growth component

12) Assuming previous year’s production capacity was inadequate to produce current year output, the

cost effect of growth for fixed costs is calculated by multiplying the difference between ________ by price

per unit of capacity in the previous year.

A) capacity units required to produce previous year output in current year and the current year capacity

units

B) capacity units required to produce current year output in previous year and the current year capacity

units

C) capacity units required to produce previous year output in current year and the previous year capacity

units

D) capacity units required to produce current year output in previous year and the previous year

capacity units

13) Assuming previous year’s production capacity was adequate to produce current year output, the cost

effect of growth for fixed costs is calculated by multiplying the difference between ________ by price per

unit of capacity in the previous year.

A) actual units of capacity in current year and actual units of capacity in previous year

B) capacity units required to produce current year output in previous year and the current year capacity

units

C) actual units of capacity in previous year and actual units of capacity in previous year

D) capacity units required to produce previous year output in current year and the previous year

capacity units

14) The revenue effect of price recovery is calculated by multiplying the difference in selling price

(current year minus the previous year) by ________.

A) actual units sold in the current year

B) budgeted units sold in the previous year

C) budgeted units sold in the current year

D) actual units sold in the previous year

15) An operating income analysis of Argon Company revealed the following:

Operating income for 2014 $1,207,000

Add growth component 102,000

Deduct price-recovery component (95,000)

Add productivity component 90,000

Operating income for 2015 $1,304,000

Argon’s operating income gain is consistent with the ________.

A) product differentiation strategy

B) product leadership strategy

C) cost differentiation strategy

D) cost leadership strategy

16) The cost effect of productivity for variable costs is calculated by multiplying the difference in actual

input units used to produce current year output and units of input required to produce current year

output in previous year by the ________.

A) price per input unit of previous year

B) price per unit of capacity in the previous year

C) price per unit of capacity in the current year

D) price per input unit of current year

Meale Company makes a household appliance with model number X500. The goal for 2015 is to reduce

direct materials usage per unit. No defective units are currently produced. Manufacturing conversion

costs depend on production capacity defined in terms of X500 units that can be produced. The industry

market size for appliances increased 10% from 2014 to 2015. The following additional data are available

for 2014 and 2015:

2014 2015

Units of X500 produced and sold 10,000 11,000

Selling price $100 $95

Direct materials (square feet) 30,000 29,000

Direct material costs per square foot $10 $11

Manufacturing capacity for X500 (units) 12,500 12,000

Total conversion costs $250,000 $240,000

Conversion costs per unit of capacity $20 $20

17) What is operating income for 2014?

A) $450,000

B) $1,000,000

C) $750,000

D) $700,000

18) What is operating income for 2015?

A) $1,045,000

B) $726,000

C) $486,000

D) $476,000

19) Which of the following statements is true of strategic analysis of operating income?

A) Change in operating income from one period to any future period can be subdivided into product

differentiation, cost leadership, and growth components.

B) Subdividing the change in operating income to evaluate the success of a strategy has no similarity to

the variance analysis.

C) Management accountants compare actual and budgeted operating performance over the same time

periods.

D) It focuses on differences in individual categories of costs (direct materials, direct manufacturing labor,

and overheads).

Answer the following questions using the information below:

Crynton Company makes a household appliance with model number L800. The goal for 2015 is to reduce

direct materials usage per unit. No defective units are currently produced. Manufacturing conversion

costs depend on production capacity defined in terms of L800 units that can be produced. The industry

market size for appliances increased 5% from 2014 to 2015. The following additional data are available for

2014 and 2015:

2014 2015

Units of L800 produced and sold 30,000 31,500

Selling price $300 $285

Direct materials (square feet) 90,000 87,000

Direct material costs per square foot $30 $33

Manufacturing capacity for L800 (units) 37,500 36,000

Total conversion costs $750,000 $720,000

Conversion costs per unit of capacity $60 $60

20) What is the revenue effect of the growth component?

A) $450,000 U

B) $135,000 F

C) $135,000 U

D) $450,000 F

21) What is the cost effect of the growth component for direct materials?

A) $135,000 U

B) $450,000 F

C) $450,000 U

D) $135,000 F

22) What is the cost effect of the growth component for conversion costs?

A) $12,500 U

B) $0

C) $90,000 U

D) $90,000 F

23) Overall, was Crynton‘s strategy successful in 2015?

A) Yes, because total revenues increased

B) No, because operating income decreased

C) No, because direct materials usage per unit increased

D) No, because direct material cost per unit decreased

Answer the following questions using the information below:

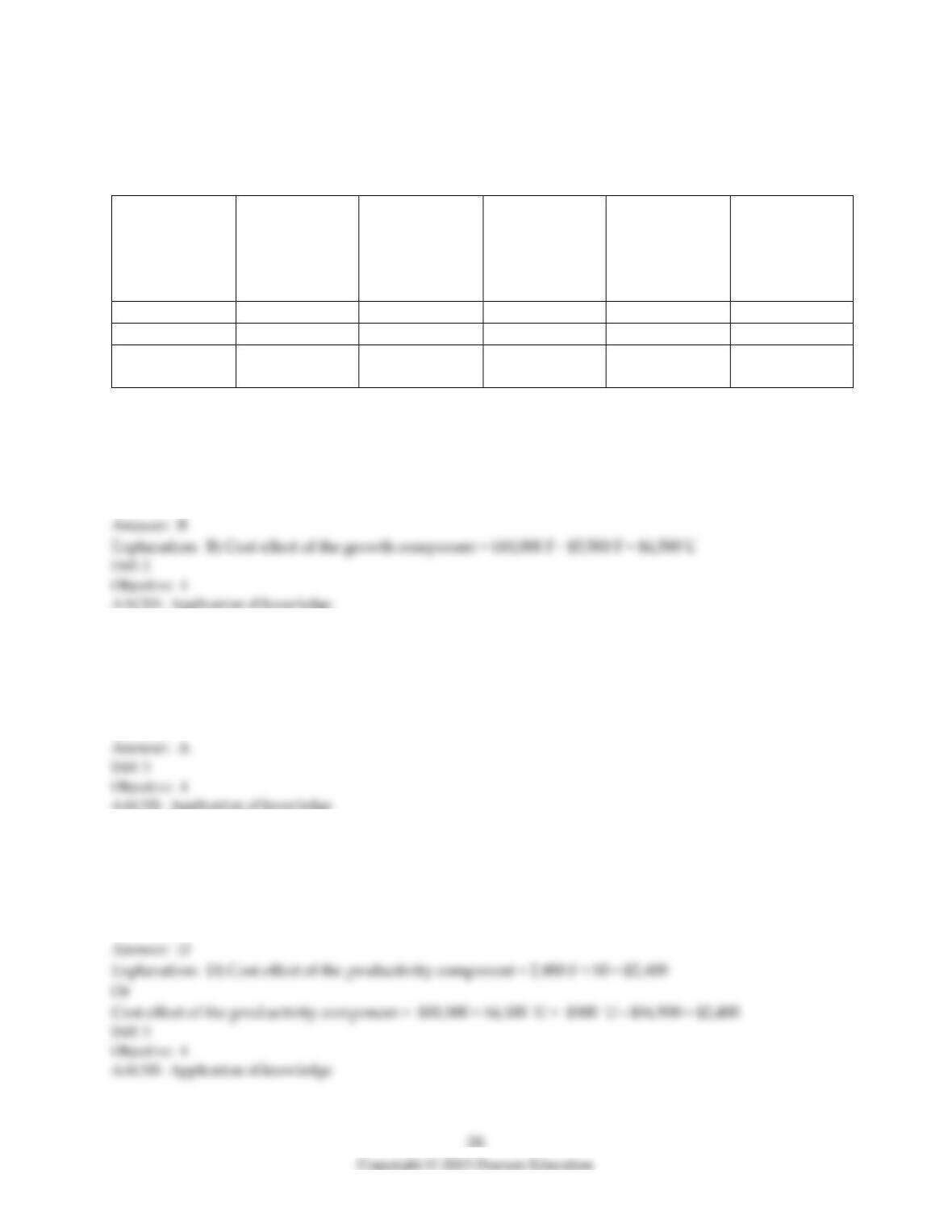

Strategic Analysis of Profitability of Ransham Company:

Income

Statement

Amounts

in 2014

Revenue and

Cost Effects

of Growth

Component

in 2015

Revenue and

Cost Effects of

Price-Recovery

Component

in 2015

Cost Effect of

Productivity

Component

in 2015

Income

Statement

Amounts

in 2015

Revenues ($)

34,000

10,000 F

1,000 U

(b)

(e)

Costs

23,500

(a)

500 U

(c)

26,100

Operating

income

10,500

5,500 F

1,500 U

2,400 F

(d)

24) What is the cost effect of the growth component (a)?

A) $15,500 F

B) $4,500 U

C) $15,500 U

D) $4,500 F

25) What is the revenue effect of the productivity component (b)?

A) $0

B) $2,400 U

C) $900 F

D) $2,400 F

26) What is the cost effect of the productivity component (c)?

A) $0

B) $1,200 U

C) $900 F

D) $2,400 F

27) What is the operating income amount for 2015 (d)?

A) $43,000

B) $25,000

C) $16,900

D) $46,000

28) What is the revenue amount for 2015 (e)?

A) $9,000

B) $25,000

C) $43,000

D) $16,900

Answer the following questions using the information below:

Following a strategy of product differentiation, Arseniq Company makes a high-end Appliance, XT15.

Arseniq presents the following data for the years 2014 and 2015:

2014 2015

Units of XT15 produced and sold 50,000 52,500

Selling price $500 $550

Direct materials (square feet) 150,000 153,750

Direct materials costs per square foot $50 $55

Manufacturing capacity in units of XT15 62,500 62,500

Total conversion costs $6,250,000 $6,875,000

Conversion costs per unit of capacity $100 $110

Selling and customer-service capacity (customers) 150 150

Total selling and customer-service costs $2,250,000 $2,343,750

Selling and customer-service capacity cost per customer $15,000 $15,625

Arseniq produces no defective units but it wants to reduce direct materials usage per unit of XT15.

Manufacturing conversion costs in each year depend on production capacity defined in terms of XT15

units that can be produced. Selling and customer-service costs depend on the number of customers that

the customer and service functions are designed to support. Arseniq had 140 customers in 2014 and 145

customers in 2015.

29) What is operating income for 2014?

A) $9,000,000

B) $11,200,000

C) $11,440,000

D) $9,207,000

30) What is operating income in 2015?

A) $11,440,000

B) $11,200,000

C) $9,000,000

D) $9,207,000

31) What is the change in operating income from 2014 to 2015?

A) $2,200,000 U

B) $3,875,000 F

C) $2,200,000 F

D) $3,875,000 U

32) What is the revenue effect of the growth component?

A) $2,625,000 F

B) $1,250,000 U

C) $2,625,000 U

D) $1,250,000 F

33) What is the cost effect of the growth component?

A) $375,000 U

B) $1,506,250 U

C) $1,506,250 O

D) $375,000 O

34) What is the net effect on operating income as a result of the growth component?

A) $1,118,750 F

B) $875,000 F

C) $875,000 U

D) $1,118,750 U

35) What is the revenue effect of the price-recovery component?

A) $2,625,000 U

B) $1,250,000 U

C) $1,250,000 F

D) $2,625,000 F

36) What is the cost effect of the price-recovery component?

A) $375,000 F

B) $375,000 U

C) $1,506,250 U

D) $1,506,250 F

37) What is the net effect on operating income as a result of the price-recovery component?

A) $1,118,750 F

B) $875,000 U

C) $1,118,750 U

D) $875,000 F

38) What is the net effect on operating income as a result of the productivity component?

A) $875,000 U

B) $206,250 F

C) $875,000 F

D) $206,250 U

39) An analysis of Baker, Inc.’s operating income for the last two years showed the following:

Operating income for 2011

$1,200,000

Add growth component

30,000

Add price-recovery component

200,000

Deduct productivity component

(16,000)

Operating income for 2012

$1,414,000

This gain in operating income is consistent with a ________.

A) downsizing strategy

B) reengineering strategy

C) product differentiation strategy

D) cost leadership strategy

40) Cobalt Company makes a household appliance with model number X500. The goal for 2015 is to

improve product design and outlook. No defective units are currently produced. Manufacturing

conversion costs depend on production capacity defined in terms of X500 units that can be produced. The

industry market size for appliances increased 10% from 2014 to 2015. The following additional data are

available for 2014 and 2015:

2014 2015

Units of X500 produced and sold 20,000 20,000

Selling price $150 $170

Direct materials (square feet) 30,000 32,500

Direct material costs per square foot $10 $10

Manufacturing capacity for X500 (units) 20,500 20,500

Total conversion costs $451,000 $493,250

Conversion costs per unit of capacity $22 $22.5

Out of the two basic strategies, Cobalt’s strategy is ________.

A) product differentiation because Cobalt is able to produce a given quantity of output with a lower cost

of inputs

B) cost leadership because Cobalt is able to produce a given quantity of output with a lower cost of inputs

C) cost leadership because Cobalt is able to increase its output price faster than the increase in its input

prices

D) product differentiation because Cobalt is able to increase its output price faster than the increase in its

input prices

41) When adequate capacity exists in the current year to produce next year’s output, the cost effect of

growth for capacity-related fixed costs will be zero.

42) The price-recovery component of the change in operating income measures solely the effect of price

changes on revenues and costs.

43) When analyzing the change in operating income, the strategy component of growth will increase

when more units are sold.

44) The revenue effect of growth is calculated by multiplying the difference in units sold (current year

minus the previous year) by selling price in the current year.

45) Cost effect of productivity for fixed costs is calculated by multiplying the difference in units of

capacity (current year capacity units minus the previous year capacity units) by price per unit of capacity

of the previous year.

46) The productivity component measures the amount by which operating income increases by using

inputs efficiently to lower costs.

47) An increase in production capacity will always result in a favorable cost effect of productivity for

variable costs in the short run.

48) An analysis of Ruthen Corporation’s operating income changes between 2015 and 2016 show the

following:

Operating income for 2015 $4,750,000

Add growth component 180,000

Deduct price-recovery component (60,000)

Add productivity component 285,000

Operating income for 2016 $5,155,000

Required:

Is Ruthen’s operating income gain consistent with the product differentiation or cost leadership strategy?

Explain briefly.

49) An analysis of Terbolt Corporation’s operating income changes between 2015 and 2016 show the

following:

Operating income for 2015 $4,750,000

Add growth component 75,000

Add price-recovery component 398,000

Deduct productivity component (50,000)

Operating income for 2016 $5,173,000

Required:

Is Terbolt’s operating income gain consistent with the product differentiation or cost leadership strategy?

Explain briefly.

50) Following a strategy of product differentiation, Sting Corporation makes a high-end computer

monitor, CM7. Sting Corporation presents the following data for the years 2012 and 2013:

2012 2013

Units of CM 7 produced and sold 5,000 5,500

Selling price $400 $440

Direct materials (pounds) 15,000 15,375

Direct materials costs per pound $40 $44

Manufacturing capacity for CM7 (units) 10,000 10,000

Conversion costs $1,000,000 $1,100,000

Conversion costs per unit of capacity $100 $110

Selling and customer-service capacity (customers) 60 58

Total selling and customer-service costs $360,000 $362,500

Selling and customer-service capacity cost per customer $6,000 $6,250

Sting Corporation produces no defective units but it wants to reduce direct materials usage per unit of

CM7 in 2013. Manufacturing conversion costs in each year depend on production capacity defined in

terms of CM7 units that can be produced. Selling and customer-service costs depend on the number of

customers that the customer and service functions are designed to support. Sting Corporation has 100

customers in 2012 and 115 customers in 2013. The industry market size for high-end computer monitors

increased 5% from 2012 to 2013.

Required:

a. What is operating income for 2012?

b. What is operating income in 2013?

c. What is the change in operating income from 2012 to 2013?

51) Following a strategy of product differentiation, Sting Corporation makes a high-end computer

monitor, CM7. Sting Corporation presents the following data for the years 2012 and 2013:

2012 2013

Units of CM7 produced and sold 5,000 5,500

Selling price $400 $440

Direct materials (pounds) 15,000 15,375

Direct materials costs per pound $40 $44

Manufacturing capacity for CM7 (units) 10,000 10,000

Conversion costs $1,000,000 $1,100,000

Conversion costs per unit of capacity $100 $110

Selling and customer-service capacity (customers) 60 58

Total selling and customer-service costs $360,000 $362,500

Selling and customer-service capacity cost per customer $6,000 $6,250

Sting Corporation produces no defective units but it wants to reduce direct materials usage per unit of

CM7 in 2013. Manufacturing conversion costs in each year depend on production capacity defined in

terms of CM7 units that can be produced. Selling and customer-service costs depend on the number of

customers that the customer and service functions are designed to support. Ernsting Corporation has 100

customers in 2012 and 115 customers in 2013. The industry market size for high-end computer monitors

increased 5% from 2012 to 2013.

Required:

a. What is the revenue effect of the growth component?

b. What is the cost effect of the growth component?

c. What is the net effect on operating income as a result of the growth component?