Name:

Class:

Date:

chapter 12

Indicate whether the statement is true or false.

1. The salary allocation to partners used in dividing net income would also appear as salary expense on the partnership

income statement.

a.

True

b.

False

2. A partnership’s asset accounts should be changed from cost to fair market value when a new partner is admitted to a

firm or an existing partner withdraws or dies.

a.

True

b.

False

3. The amount that a partner withdraws as a monthly salary allowance does not affect the division of net income.

a.

True

b.

False

4. If a new partner is to be admitted to a partnership and a bonus is attributed to the old partnership, the bonus should be

divided between the capital accounts of the original partners according to their capital balances.

a.

True

b.

False

5. An advantage of the partnership form of business is that each partner’s potential loss is limited to that partner’s

investment in the partnership.

a.

True

b.

False

6. The partner capital accounts may change due to capital additions, net income, or withdrawals.

a.

True

b.

False

7. The process of winding up the affairs of a partnership is referred to as realization.

a.

True

b.

False

8. For tax purposes, a limited liability company may elect to be treated as a partnership.

a.

True

b.

False

9. In the liquidating process, any uncollectible deficiency becomes a loss to the partnership and is divided among the

remaining partners’ capital balances based on their income-sharing ratio.

a.

True

b.

False

10. When the asset revaluation account is used to revalue assets prior to admitting a new partner, Asset Revaluation is

debited with an upward revaluation of an asset.

a.

True

Name:

Class:

Date:

chapter 12

b.

False

11. When a new partner is admitted by making an investment in the partnership, the old partners’ capital accounts are

always credited.

a.

True

b.

False

12. If the net income of a partnership is less than the total of the allowances provided by the partnership agreement, the

difference must be divided among the partners according to the income-sharing ratio.

a.

True

b.

False

13. When a partner invests noncash assets in a partnership, the assets are recorded at the partner’s book value.

a.

True

b.

False

14. In the distribution of income, the net income is less than the salary and interest allowances granted; the remaining

balance will be a negative amount that must be divided among the partners as though it were a net loss.

a.

True

b.

False

15. When a new partner is admitted to a partnership, all partnership assets should be revised to reflect current values.

a.

True

b.

False

16. Each partner has a separate capital and withdrawal account.

a.

True

b.

False

17. The asset revaluation account is a permanent balance sheet account.

a.

True

b.

False

18. X sells to A one-half of a partnership capital interest that totals $70,000 for $40,000. A’s capital account in the

partnership should be credited for $40,000.

a.

True

b.

False

19. Partner A devotes full time and Partner B devotes one-half time to their partnership. If the partnership agreement is

silent concerning the division of net income, Partner A will receive a $20,000 share of a net income of $30,000.

a.

True

b.

False

20. When a partner withdraws from the partnership, the partnership dissolves.

a.

True

b.

False

Name:

Class:

Date:

chapter 12

21. The equity reporting for a limited liability company is similar to that of a partnership, but the changes in capital are

shown on a statement of members’ equity.

a.

True

b.

False

22. Sarno has a capital balance of $42,000 after adjusting the assets to fair market value. Minton contributes $22,000 to

receive a 30% interest in the new partnership. The bonus paid by Minton is $2,800.

a.

True

b.

False

23. The statement of members’ equity is used for equity reporting of a partnership.

a.

True

b.

False

24. In a partnership liquidation, if a partner has a debit capital balance in his or her capital account, he or she is

responsible for contributing personal assets sufficient to eliminate the deficit.

a.

True

b.

False

25. If the articles of partnership provide for annual salary allowances of $36,000 and $18,000 to Partner X and Partner Y,

respectively, and net income is $30,000, Partner X’s share of net income is $20,000.

a.

True

b.

False

26. If the share of losses on realization of the sale of noncash assets exceeds the balance in a partner’s capital account, the

resulting balance is called a deficiency.

a.

True

b.

False

27. Details of the division of partnership income should normally be disclosed in the financial statements.

a.

True

b.

False

28. In admitting a new partner who purchases an interest, the capital interest of the new partner is obtained from the

current partners and both the total assets and total capital are increased.

a.

True

b.

False

29. One of the major disadvantages of the partnership is its limited life.

a.

True

b.

False

30. When a new partner purchases the entire interest of an old partner, the new partner’s capital account should be credited

for the amount he or she paid to the old partner.

a.

True

b.

False

Name:

Class:

Date:

chapter 12

b.

False

31. A disadvantage of partnerships is the mutual agency of all partners.

a.

True

b.

False

32. The limited liability company may elect to be manager-managed rather than member-managed, which means that only

authorized members may legally bind the corporation.

a.

True

b.

False

33. When a partner withdraws from the partnership by selling his or her interest back to the partnership, the remaining

partners must pay the withdrawing partner a specified amount from their personal assets.

a.

True

b.

False

34. A new partner contributes accounts receivable to a partnership, which appears in the ledger of his sole proprietorship

at $20,500, and there was an allowance for doubtful accounts of $750. If $600 of the accounts receivable are completely

worthless, the partnership Accounts Receivable should be debited for $19,900.

a.

True

b.

False

35. The chart of accounts for a partnership, with the exception of additional drawing and capital accounts, does not differ

from the chart of accounts for a sole proprietorship.

a.

True

b.

False

36. Many partnerships provide for the admission of new partners or withdrawals of present partners by amending existing

partnership agreements, so that the firm may continue to operate without executing a new agreement.

a.

True

b.

False

37. A partnership is subject to federal income taxes.

a.

True

b.

False

38. When a new partner is admitted by making an investment of assets in the partnership and the new partner has to pay a

premium for admission, a bonus is divided among the old partners’ capital accounts.

a.

True

b.

False

39. The distribution of cash, as the final process in winding up the affairs of a partnership, is based on the income-sharing

ratio.

a.

True

b.

False

40. When compared to a proprietorship, one of the major advantages of a partnership is its relative ease of formation.

a.

True

Name:

Class:

Date:

chapter 12

41. After all noncash assets have been converted to cash and all liabilities paid, A, B, and C have capital balances of

$10,000 (debit), $5,000 (debit), and $25,000 (credit). The cash available for distribution to the partners is $10,000.

a.

True

b.

False

42. With a partnership, there is no limitation on legal liability.

a.

True

b.

False

43. One reason that the division of income (loss) is reported at the bottom of the income statement is to provide the

information for recording a closing entry.

a.

True

b.

False

44. If not enough partnership cash or other assets are available to pay the withdrawing partner, a liability may be created

for the amount owed the withdrawing partner.

a.

True

b.

False

45. A partnership requires only an agreement between two or more persons to organize.

a.

True

b.

False

46. Each partner may withdraw the assets he or she contributed to the partnership at any time.

a.

True

b.

False

47. When a new partner is admitted to a partnership, bonuses attributable to either the old partnership or to the incoming

partner may be recognized in accordance with the agreement among the partners.

a.

True

b.

False

48. A limited liability company is a business entity form designed to overcome some of the disadvantages of the

partnership form.

a.

True

b.

False

49. The proprietorship is a less widely used form of business than the partnership.

a.

True

b.

False

50. If the partnership agreement does not otherwise state, partnership income is divided in proportion to the individual

partner’s capital balance.

a.

True

b.

False

Name:

Class:

Date:

chapter 12

51. In a general partnership, each partner is individually liable to creditors for debts incurred by the partnership.

a.

True

b.

False

52. In a partnership liquidation, gains and losses on the sale of partnership assets are divided among the partners’ capital

accounts on the basis of their capital balances.

a.

True

b.

False

53. Revenue per employee may be used to measure partnership (LLC) efficiency.

a.

True

b.

False

Indicate the answer choice that best completes the statement or answers the question.

54. Bobbi and Stuart are partners. The partnership capital of Bobbi is $40,000 and that of Stuart is $70,000. Bobbi sells

his interest in the partnership to John for $50,000. The journal entry for the admission of John as a new partner would

include a credit to

a.

John’s capital account for $40,000

b.

Stuart’s capital account for $10,000

c.

John’s capital account for $50,000

d.

John’s capital account for $40,000 and a credit to Stuart’s capital account for $10,000

55. Which of the following is not a characteristic of a limited liability company?

a.

unlimited life

b.

limited legal liability

c.

taxable

d.

moderate ability to raise capital

56. Benson and Orton are partners who share income in the ratio of 2:3 and have capital balances of $60,000 and $40,000,

respectively. Ramsey is admitted to the partnership and is given a 40% interest by investing $20,000. What is Benson’s

capital balance after admitting Ramsey?

a.

$20,000

b.

$24,000

c.

$48,800

d.

$71,200

57. If there is no written agreement as to the way income will be divided among partners,

a.

they will share income and losses equally

b.

they will share income and losses according to their capital balances

c.

they will share income and losses according to the time devoted to the business

d.

there really is no partnership

58. Jordon and Heidi share income equally. For the current year, the partnership net income is $40,000. Jordon made

withdrawals of $14,000, and Heidi made withdrawals of $15,000. At the beginning of the year, the capital account

balances were: Jordon, Capital, $40,000; Heidi, Capital, $58,000. Jordon’s capital account balance at the end of the year is

Name:

Class:

Date:

chapter 12

a.

$68,000

b.

$54,000

c.

$74,000

d.

$46,000

59. When a partner dies, the capital account balances of the remaining partners

a.

will increase

b.

will decrease

c.

will remain the same

d.

may increase, decrease, or remain the same

60. Benson and Orton are partners who share income in the ratio of 1:3 and have capital balances of $70,000 and $30,000,

respectively. Ramsey is admitted to the partnership and is given a 40% interest by investing $20,000. What is Orton’s

capital balance after admitting Ramsey?

a.

$20,000

b.

$9,000

c.

$70,000

d.

$63,000

61. At the end of the accounting period, the balance in the asset revaluation account will

a.

appear as an asset on the balance sheet

b.

appear as an expense on the income statement

c.

be closed to the capital accounts

d.

be distributed to the accumulated depreciation accounts

62. The Craig-Doran Partnership plans to form a new partnership with Alexis. The existing partnership owns inventory

that was purchased for $85,000, has a current replacement cost of $54,500, and is priced to sell for $98,000. At what

amount should the inventory be recorded in the accounts of the new partnership if Alexis is to be admitted?

a.

$98,000

b.

$54,500

c.

$85,000

d.

$79,167

63. Teri, Doug, and Brian are partners with capital balances of $20,000, $30,000, and $50,000, respectively. They share

income and losses in the ratio of 3:2:1. Revenue accounts for the period total $350,000. Expense accounts for the period

total $380,000. The revenue and expense accounts are closed to the capital accounts. Doug withdraws from the

partnership. How much cash does he receive upon withdrawal?

a.

$30,000

b.

$20,000

c.

$40,000

d.

$24,000

64. Jackson and Campbell have capital balances of $100,000 and $300,000, respectively. Jackson devotes full time and

Campbell devotes one-half time to the business. Determine the division of $150,000 of net income in the ratio of time

devoted to business.

Name:

Class:

Date:

chapter 12

a.

$75,000 and $75,000

b.

$37,500 and $112,500

c.

$100,000 and $50,000

d.

$112,500 and $37,500

65. Details of the division of net income for a partnership should be disclosed in the

a.

Assets section of the balance sheet

b.

partners’ subsidiary ledger

c.

statement of cash flows

d.

partnership income statement

Use this information to answer the questions that follow.

The capital accounts of Hawk and Martin have balances of $160,000 and $140,000, respectively, on January 1, the

beginning of the current fiscal year. On April 10, Hawk invested an additional $10,000. During the year, Hawk and

Martin withdrew $86,000 and $68,000, respectively, and net income for the year was $258,000. The articles of partnership

make no reference to the division of net income.

66. Based on this information, the statement of partners’ equity would show what amount in the capital account for Martin

on December 31?

a.

$173,000

b.

$211,000

c.

$201,000

d.

$232,000

67. Tanner and Teresa share income and losses in a 2:1 ratio (2/3 to Tanner and 1/3 to Teresa) after allowing for salaries

of $42,000 to Tanner and $60,000 to Teresa. Net income of the partnership is $132,000. How should income be divided

for Tanner and Teresa?

a.

Tanner, $57,000; Teresa, $75,000

b.

Tanner, $58,000; Teresa, $74,000

c.

Tanner, $75,000; Teresa, $57,000

d.

Tanner, $62,000; Teresa, $70,000

68. Everett, Miguel, and Ramona are partners, sharing income 1:2:3. After selling all of the assets for cash, dividing losses

on realization, and paying liabilities, the balances in the capital accounts are as follows: Everett, $50,000 Cr.; Miguel,

$40,000 Dr.; and Ramona, $30,000 Cr. How much cash is available for distribution to the partners?

a.

$120,000

b.

$30,000

c.

$40,000

d.

$90,000

69. Partners Ken and Macki each have a $40,000 capital balance and share income and losses in the ratio of 3:2. Cash

equals $20,000, noncash assets equal $120,000, and liabilities equal $60,000. If the noncash assets are sold for $80,000,

Macki’s capital account will

a.

decrease by $16,000

b.

decrease by $24,000

Name:

Class:

Date:

chapter 12

c.

increase by $24,000

d.

decrease by $40,000

70. Abby and Bailey are partners who share income in the ratio of 2:1 and have capital balances of $60,000 and $30,000,

respectively. With the consent of Bailey, Sandra buys one-half of Abby’s interest for $35,000. For what amount will

Abby’s capital account be debited to record admission of Sandra to the partnership?

a.

$40,000

b.

$15,000

c.

$35,000

d.

$30,000

71. Alpha and Beta are partners who share income in the ratio of 1:2 and have capital balances of $40,000 and $70,000,

respectively, at the time they decide to terminate the partnership. Noncash assets with a book value of $110,000 are sold

for $50,000. What amount of loss on realization should be allocated to Alpha?

a.

$60,000

b.

$20,000

c.

$30,000

d.

$50,000

72. Xavier and Yolanda have original investments of $50,000 and $100,000, respectively, in a partnership. The articles of

partnership include the following provisions regarding the division of net income: interest on original investment at 20%;

salary allowances of $27,000 and $18,000, respectively; and the remainder to be divided equally. How much of the net

income of $81,000 is allocated to Xavier?

a.

$37,000

b.

$40,000

c.

$42,000

d.

$42,500

73. When a partnership is formed, assets contributed by the partners should be recorded on the partnership books at their

a.

book values on the partners’ books prior to their being contributed to the partnership

b.

fair market value at the time of the contribution

c.

original costs to the partner contributing them

d.

assessed values for property tax purposes

74. Xavier and Yolanda have original investments of $50,000 and $100,000, respectively, in a partnership. The articles of

partnership include the following provisions regarding the division of net income: interest on original investment at 10%;

salary allowances of $38,000 and $28,000, respectively; and the remainder to be divided equally. How much of the net

income of $77,000 is allocated to Xavier?

a.

$66,000

b.

$41,000

c.

$36,000

d.

$43,000

Use this information to answer the questions that follow.

Sandra and Kelsey are forming a partnership. Sandra will invest a piece of equipment with a book value of $7,500 and a

Name:

Class:

Date:

chapter 12

fair market value of $18,000. Kelsey will invest a building with a book value of $40,000 and a fair market value of

$44,000.

75. What amount will be recorded to Sandra’s capital account?

a.

$18,000

b.

$7,500

c.

$25,500

d.

$10,500

76. A gain or loss on realization is divided among partners according to their

a.

income-sharing ratio

b.

capital balances

c.

drawing balances

d.

contribution of assets

77. Partners Ken and Macki each have a $40,000 capital balance and share income and losses in the ratio of 3:2. Cash

equals $20,000, noncash assets equal $120,000, and liabilities equal $60,000. If the noncash assets are sold for $60,000,

and both partners agree to make up any capital deficits with personal cash contributions, Partner Macki will eventually

receive cash of

a.

$0

b.

$4,000

c.

$16,000

d.

$24,000

78. A partner withdraws from a partnership by selling her interest to another person who currently is not associated with

the firm. As a result of this transaction, the capital account balance of the other partners in the partnership

a.

will increase

b.

will decrease

c.

will remain the same

d.

may increase, decrease, or remain the same

79. Soledad and Winston are partners who share income in the ratio of 1:3 and have capital balances of $100,000 and

$140,000, respectively, at the time they decide to terminate the partnership. After all noncash assets are sold and all

liabilities are paid, there is a cash balance of $130,000. What amount of loss on realization should be allocated to

Soledad?

a.

$60,000

b.

$27,500

c.

$92,500

d.

$32,500

80. The Calvin-Dogwood Partnership plans to form a new partnership with Alexis. The existing partnership owns

inventory that was purchased for $90,000, has a current replacement cost of $85,900, and is priced to sell for $125,000. At

what amount should the inventory be recorded in the accounts of the new partnership if Alexis is to be admitted?

a.

$129,100

b.

$85,900

c.

$90,000

Name:

Class:

Date:

chapter 12

d.

$125,000

81. Seth and Beth have original investments of $50,000 and $100,000, respectively, in a partnership. The articles of

partnership include the following provisions regarding the division of net income: interest on original investment at 10%;

salary allowances of $27,000 and $18,000, respectively; and the remainder to be divided equally. How much of the net

income of $42,000 is allocated to Seth?

a.

$20,000

b.

$23,000

c.

$32,000

d.

$0

82. Xavier and Yolanda have original investments of $50,000 and $100,000, respectively, in a partnership. The articles of

partnership include the following provisions regarding the division of net income: interest on original investment at 10%;

salary allowances of $38,000 and $28,000, respectively; and the remainder to be divided equally. How much of the net

income of $77,000 is allocated to Yolanda?

a.

$77,000

b.

$38,000

c.

$36,000

d.

$44,000

83. Harriet, Mickey, and Zack decide to liquidate their partnership. All assets are sold, and the liabilities are

paid. Following these transactions, the capital balances and profit and loss percentages are as follows: Harriet, $27,000

and 30%; Mickey, $(12,000) and 40%; Zack, $43,000 and 30%. Mickey is unable to contribute any assets to reduce the

deficit. How much cash will Harriet receive as a result of the partnership liquidation?

a.

$27,000

b.

$21,000

c.

$23,400

d.

$15,000

84. When a limited liability company is formed,

a.

the partnership activities are limited

b.

all partners have limited liability

c.

some of the partners have limited liability

d.

none of the partners has limited liability

Use this information to answer the questions that follow.

The capital accounts of Hawk and Martin have balances of $160,000 and $140,000, respectively, on January 1, the

beginning of the current fiscal year. On April 10, Hawk invested an additional $10,000. During the year, Hawk and

Martin withdrew $86,000 and $68,000, respectively, and net income for the year was $258,000. The articles of partnership

make no reference to the division of net income.

85. Based on this information, the statement of partners’ equity would show what amount as total capital for the

partnership on December 31?

a.

$384,600

b.

$412,600

c.

$404,000

Name:

Class:

Date:

chapter 12

d.

$414,000

86. Tomas and Saturn are partners who share income in the ratio of 3:1 (3/4 to Tomas and 1/4 to Saturn). Their capital

balances are $80,000 and $120,000, respectively. The partnership generated net income of $30,000. What is Saturn’s

capital balance after closing the revenue and expense accounts to the capital accounts?

a.

$102,500

b.

$120,000

c.

$112,500

d.

$127,500

87. Singer and McMann are partners in a business. Singer’s original capital was $40,000 and McMann’s was $60,000.

They agree to salaries of $12,000 and $18,000 for Singer and McMann, respectively, and 10% interest on original capital.

If they agree to share the remaining profits and losses in a 3:2 ratio, what will Singer’s share of the income be if the

income for the year is $15,000?

a.

$9,000

b.

$2,400

c.

$1,000

d.

$5,600

88. As part of the initial investment, Jackson contributes accounts receivable that had a balance of $22,500 in the accounts

of a sole proprietorship. Of this amount, $3,000 is deemed completely worthless. For the remaining accounts, the

partnership will establish a provision for possible future uncollectible accounts of $1,500. The amount debited to

Accounts Receivable for the new partnership is

a.

$18,000

b.

$22,500

c.

$21,000

d.

$19,500

89. When a new partner is admitted to a partnership, there should be a(n)

a.

revaluation of assets

b.

realization of assets

c.

allocation of assets

d.

return of assets

90. A new partner may be admitted to a partnership by

a.

inheriting a partnership interest

b.

contributing assets to the partnership

c.

purchasing a specific quantity of assets from the partnership

d.

a written approval under the federal law

91. Luke and John share income and losses in a 2:1 ratio (2/3 to Luke and 1/3 to John) after allowing for salaries of

$48,000 to Luke and $60,000 to John. Net income for the partnership is $93,000. Income should be divided as

a.

Luke, $46,500; John, $46,500

b.

Luke, $55,000; John, $38,000

c.

Luke, $65,000; John, $28,000

Name:

Class:

Date:

chapter 12

d.

Luke, $38,000; John, $55,000

92. When a new partner is admitted to a partnership, a bonus

a.

may be attributable to the existing partners

b.

may only result from more cash being given by the new partner than the value of the assets being purchased

c.

agreed upon by the partners is recorded as an asset so long as the amount is within the range set by the SEC

d.

is not recorded

Use this information to answer the questions that follow.

Sandra and Kelsey are forming a partnership. Sandra will invest a piece of equipment with a book value of $7,500 and a

fair market value of $18,000. Kelsey will invest a building with a book value of $40,000 and a fair market value of

$44,000.

93. What amount will be recorded to the building account?

a.

$24,000

b.

$14,000

c.

$40,000

d.

$44,000

94. When a new partner is admitted to a partnership, there should be a(n)

a.

increase in the total assets of the partnership

b.

new capital account added to the ledger for the new partner

c.

increase in the total owners’ equity of the partnership

d.

debit amount to the partner’s capital account for the cash received by the current partner

95. Which of the following is not a characteristic of a general partnership?

a.

The partnership is created by a contract.

b.

Mutual agency exists.

c.

Partners share equally in net income or net losses unless an agreement states differently.

d.

Dissolution occurs only when all partners agree.

96. Everett, Miguel, and Ramona are partners, sharing income 1:2:3. After selling all of the assets for cash, dividing losses

on realization, and paying liabilities, the balances in the capital accounts are as follows: Everett, $50,000 Cr.; Miguel,

$40,000 Dr.; and Ramona, $30,000 Cr. How much cash should be distributed to Everett assuming that Miguel pays the

deficiency?

a.

$50,000

b.

$20,000

c.

$30,000

d.

$40,000

97. As part of the initial investment, Ray Blake contributes equipment that had originally cost $125,000 and on which

accumulated depreciation of $100,000 has been recorded. If similar equipment would cost $150,000 to replace and the

partners agree on a valuation of $29,000 for the contributed equipment, what amount should be debited to the equipment

account?

a.

$29,000

Name:

Class:

Date:

chapter 12

b.

$150,000

c.

$125,000

d.

$100,000

98. The remaining cash of a partnership (after creditors have been paid) upon liquidation is divided among partners

according to their

a.

capital balances

b.

contribution of assets

c.

drawing balances

d.

income-sharing ratio

99. Rex and Kelsey are partners who share income in the ratio of 3:2 (3/5 to Rex and 2/5 to Kelsey). Their capital

balances are $95,000 and $140,000, respectively, on January 1. The partnership generated net income of $40,000 for the

year. What is Rex’s capital balance after closing the revenue and expense accounts to the capital accounts?

a.

$71,000

b.

$119,000

c.

$146,000

d.

$111,000

100. Benson and Orton are partners who share income in the ratio of 2:3 and have capital balances of $60,000 and

$40,000, respectively. Ramsey is admitted to the partnership and is given a 10% interest by investing $20,000. What is

Orton’s capital balance after admitting Ramsey?

a.

$44,800

b.

$35,200

c.

$20,000

d.

$16,000

101. Jefferson has a capital balance of $65,000 and devotes full time to a partnership. Washington has a capital balance of

$45,000 and devotes half time to the partnership. If no other information is available regarding distributions, how should

net income be divided?

a.

59% to Jefferson and 41% to Washington

b.

50% to Jefferson and 50% to Washington

c.

41% to Jefferson and 59% to Washington

d.

33% to Jefferson and 67% to Washington

102. Singer and McMann are partners in a business. Singer’s original capital was $40,000 and McMann’s was

$60,000. They agree to salaries of $12,000 and $18,000 for Singer and McMann, respectively, and 10% interest on

original capital. If they agree to share the remaining profits and losses on a 3:2 ratio (3/5 to Singer and 2/5 to McMann),

what will McMann’s share of the income be if the income for the year is $30,000?

a.

$20,000

b.

$18,000

c.

$18,600

d.

$17,400

103. Paradise Architects had total revenue of $5,400,000 and revenue per employee of $200,000 in 20Y1. In 20Y2, total

revenue increased to $5,700,000 and the number of employees expanded to 30. Did employee efficiency increase or

Name:

Class:

Date:

chapter 12

balances are $40,000 and $60,000, respectively. The partnership generated net income of $20,000. What is Saturn’s

decrease with the expansion, and by how much?

a.

increased by $300,000

b.

increased by $10,000

c.

decreased by $10,000

d.

decreased by $100,000

104. Singer and McMann are partners in a business. Singer’s original capital was $40,000 and McMann’s was $60,000.

They agree to salaries of $12,000 and $18,000 for Singer and McMann, respectively, and 10% interest on original capital.

If they agree to share the remaining profits and losses on a 3:2 ratio, what will McMann’s share of the income be if the

income for the year is $15,000?

a.

$6,000

b.

$9,400

c.

$12,600

d.

$14,000

105. Patty and Paul are partners who share income in the ratio of 3:2 (3/5 to Patty and 2/5 to Paul). Their capital balances

are $90,000 and $130,000, respectively, on January 1. The partnership generated net income of $40,000 for the year. What

is Paul’s capital balance after closing the revenue and expense accounts to the capital accounts?

a.

$120,000

b.

$146,000

c.

$164,000

d.

$160,000

106. Jackson and Campbell have capital balances of $100,000 and $300,000, respectively. Jackson devotes full time and

Campbell devotes one-half time to the business. Determine the division of $150,000 of net income in the ratio of capital

balances.

a.

$75,000 and $75,000

b.

$37,500 and $112,500

c.

$100,000 and $50,000

d.

$50,000 and $100,000

Use this information to answer the questions that follow.

The capital accounts of Hawk and Martin have balances of $160,000 and $140,000, respectively, on January 1, the

beginning of the current fiscal year. On April 10, Hawk invested an additional $10,000. During the year, Hawk and

Martin withdrew $86,000 and $68,000, respectively, and net income for the year was $258,000. The articles of partnership

make no reference to the division of net income.

107. Based on this information, the statement of partners’ equity would show what amount in the capital account for

Hawk on December 31?

a.

$211,600

b.

$213,000

c.

$201,000

d.

$203,000

108. Tomas and Saturn are partners who share income in the ratio of 3:1 (3/4 to Tomas and 1/4 to Saturn). Their capital

Name:

Class:

Date:

chapter 12

capital balance after closing the revenue and expense accounts to the capital accounts?

a.

$55,000

b.

$75,000

c.

$45,000

d.

$65,000

109. Which of the following is a characteristic of a partnership?

a.

taxable

b.

simple to form

c.

limited liability

d.

limited life

110. A ratio of 4:2:1 is the same as

a.

40%:20%:10%

b.

4/7:2/7:1/7

c.

4/10:2/10:1/20

d.

7/4:7/2:7/1

111. Adriana and Belen are partners who share income in the ratio of 3:2 and have capital balances of $50,000 and

$90,000, respectively, at the time they decide to terminate the partnership. After all noncash assets are sold and all

liabilities are paid, there is a cash balance of $90,000. How much cash should be distributed to Adriana?

a.

$50,000

b.

$20,000

c.

$30,000

d.

$45,000

112. Immediately prior to the admission of Abbott, the Smith-Jones Partnership determines that equipment that cost

$20,000, with accumulated depreciation of $5,000, has a current market value of $12,000. Assuming an asset revaluation

account is used, the journal entry to revalue the equipment will include

a.

a debit to Asset Revaluation of $12,000

b.

a debit to Asset Revaluation of $3,000

c.

a credit to Equipment of $3,000

d.

a credit to Accumulated Depreciation of $3,000

113. Xavier and Yolanda have original investments of $50,000 and $100,000, respectively, in a partnership. The articles

of partnership include the following provisions regarding the division of net income: interest on original investment at

20%; salary allowances of $34,000 and $26,000, respectively; and the remainder to be divided equally. How much of the

net income of $120,000 is allocated to Xavier?

a.

$59,000

b.

$61,000

c.

$49,000

d.

$44,000

114. A partnership liquidation occurs when

a.

a new partner is admitted

Name:

Class:

Date:

chapter 12

b.

a partner dies

c.

the ownership interest of one partner is sold to a new partner

d.

the assets are sold, liabilities paid, and business operations terminated

115. Which of the following forms of legal business entity provides limited liability to its owners but is not taxable?

a.

sole proprietorship

b.

corporation

c.

partnership

d.

limited liability company (LLC)

116. Which of the following is a characteristic of a general partnership?

a.

The partners have co-ownership of partnership property.

b.

The partnership is subject to federal income tax.

c.

The partnership has an unlimited life.

d.

The partners have limited liability.

117. Xavier and Yolanda have original investments of $50,000 and $100,000, respectively, in a partnership. The articles

of partnership include the following provisions regarding the division of net income: interest on original investment at

10%; salary allowances of $27,000 and $18,000, respectively; and the remaining income (loss) equally. How much of the

net loss of $(6,000) is allocated to Yolanda?

a.

$(1,000)

b.

$(3,000)

c.

$(5,000)

d.

$0

118. Lambert invests $20,000 for a 1/3 interest in a partnership in which the other partners have capital totaling $34,000

before admitting Lambert. What is Lambert’s capital after admission?

a.

$18,000

b.

$20,000

c.

$6,667

d.

$11,333

119. Immediately prior to the admission of Allen, the Sanson-Jeremy Partnership assets had been adjusted to current

market prices and the capital balances of Sanson and Jeremy were $80,000 and $120,000, respectively. If the parties agree

that the business is worth $240,000, what is the amount of bonus that should be recognized in the accounts at the

admission of Allen?

a.

$60,000

b.

$80,000

c.

$40,000

d.

$100,000

120. Singer and McMann are partners in a business. Singer’s original capital was $40,000 and McMann’s was

$60,000. They agree to salaries of $12,000 and $18,000 for Singer and McMann, respectively, and 10% interest on

original capital. If they agree to share the remaining profits and losses in a 3:2 ratio (3/5 to Singer and 2/5 to McMann),

what will Singer’s share of the income (loss) be if the net loss for the year is $(10,000)?

a.

$(12,600)

Name:

Class:

Date:

chapter 12

b.

$(14,000)

c.

$(6,000)

d.

$(10,000)

121. An advantage of the proprietorship form of business organization is

a.

unlimited liability

b.

mutual agency

c.

ease of formation

d.

limited life

Use this information to answer the questions that follow.

The capital accounts of Harrison and Marti have balances of $160,000 and $110,000, respectively, on January 1, the

beginning of the current fiscal year. On April 10, Harrison invested an additional $20,000. During the year, Harrison and

Marti withdrew $96,000 and $78,000, respectively, and net income for the year was $264,000. The articles of partnership

make no reference to the division of net income.

122. Based on this information, the statement of partners’ equity would show what amount in the capital account for Marti

on December 31?

a.

$216,000

b.

$164,000

c.

$380,000

d.

$52,000

123. Sadie and Sam share income equally. For the current year, the partnership net income is $40,000. Sadie made

withdrawals of $14,000 and Sam made withdrawals of $15,000. At the beginning of the year, the capital account balances

were: Sadie, Capital, $42,000; Sam, Capital, $58,000. Sam’s capital account balance at the end of the year is

a.

$78,000

b.

$43,000

c.

$63,000

d.

$93,000

124. Singer and McMann are partners in a business. Singer’s original capital was $40,000 and McMann’s was

$60,000. They agree to salaries of $12,000 and $18,000 for Singer and McMann, respectively, and 10% interest on

original capital. If they agree to share the remaining profits and losses on a 3:2 ratio (3/5 to Singer and 2/5 to McMann),

what will Singer’s share of the income be if the income for the year is $50,000?

a.

$24,000

b.

$22,000

c.

$16,000

d.

$23,400

125. Seth and Rachel have original investments of $50,000 and $100,000, respectively, in a partnership. The articles of

partnership include the following provisions regarding the division of net income: interest on original investments at 15%;

salary allowances of $24,000 and $20,000, respectively; and the remainder to be divided equally. How much of the net

income of $90,000 is allocated to Seth?

a.

$42,750

Name:

Class:

Date:

chapter 12

b.

$47,750

c.

$45,000

d.

$43,250

126. The characteristic of a partnership that gives the authority to any partner to legally bind the partnership and all other

partners to business contracts is called

a.

unlimited liability

b.

ease of formation

c.

mutual agency

d.

dissolution

127. Tomas and Saturn are partners who share income in the ratio of 3:1 (3/4 to Tomas and 1/4 to Saturn). Their capital

balances are $80,000 and $120,000, respectively. The partnership generated net income of $30,000. What is Tomas’s

capital balance after closing the revenue and expense accounts to the capital accounts?

a.

$102,500

b.

$22,500

c.

$57,500

d.

$127,500

128. Soledad and Winston are partners who share income in the ratio of 1:3 and have capital balances of $100,000 and

$140,000, respectively, at the time they decide to terminate the partnership. After all noncash assets are sold and all

liabilities are paid, there is a cash balance of $130,000. What amount of loss on realization should be allocated to

Winston?

a.

$110,000

b.

$97,500

c.

$42,500

d.

$82,500

129. Which of the following is a characteristic of a general partnership?

a.

simple to form

b.

limitation on legal liability

c.

unlimited life

d.

not taxable

130. Douglas pays Selena $45,000 for her 30% interest in a partnership with net assets of $125,000. Following this

transaction, Douglas’s capital account should have a credit balance of

a.

$37,500

b.

$45,000

c.

$13,500

d.

more than $45,000

131. Paul and Roger are partners who share income in the ratio of 3:2 (3/5 to Paul and 2/5 to Roger). Their capital

balances are $90,000 and $130,000, respectively. The partnership generated net income of $50,000 for the year. What is

Paul’s capital balance after closing the revenue and expense accounts to the capital accounts?

a.

$108,000

Name:

Class:

Date:

chapter 12

b.

$120,000

c.

$115,000

d.

$180,000

Use this information to answer the questions that follow.

The capital accounts of Harrison and Marti have balances of $160,000 and $110,000, respectively, on January 1, the

beginning of the current fiscal year. On April 10, Harrison invested an additional $20,000. During the year, Harrison and

Marti withdrew $96,000 and $78,000, respectively, and net income for the year was $264,000. The articles of partnership

make no reference to the division of net income.

132. Based on this information, the statement of partners’ equity would show what amount as total capital for the

partnership on December 31?

a.

$216,000

b.

$164,000

c.

$380,000

d.

$52,000

133. Paul and Roger are partners who share income in the ratio of 3:2 (3/5 to Paul and 2/5 to Roger). Their capital

balances are $90,000 and $130,000, respectively. The partnership generated net income of $50,000 for the year. What is

Roger’s capital balance after closing the revenue and expense accounts to the capital accounts?

a.

$155,000

b.

$150,000

c.

$110,000

d.

$115,000

134. Xavier and Yolanda have original investments of $50,000 and $100,000, respectively, in a partnership. The articles

of partnership include the following provisions regarding the division of net income: interest on original investment at

20%; salary allowances of $34,000 and $26,000, respectively; and the remainder to be divided equally. How much of the

net income of $120,000 is allocated to Yolanda?

a.

$46,000

b.

$61,000

c.

$60,000

d.

$66,000

135. Franco and Jason share income and losses in a 2:1 (2/3 to Franco and 1/3 to Jason) ratio after allowing for salaries of

$15,000 and $30,000, respectively. If the partnership suffers a $15,000 loss, by how much would Jason’s capital account

increase?

a.

$10,000

b.

$20,000

c.

$40,000

d.

$25,000

136. Partnership income and losses are usually divided on the basis of interest, salaries, and stated ratios because

a.

partners seldom contribute time and resources equally

b.

this method reflects the amount of time devoted to the partnership by the partners

Name:

Class:

Date:

chapter 12

b.

$164,000

c.

it is simpler than following the legal rules

d.

it prevents arguments among the partners

137. Nick is admitted to an existing partnership by investing cash. Nick agrees to pay a bonus for his ownership interest

because of the past success of the partnership. When Nick’s investment in the partnership is recorded,

a.

his capital account will be credited for more than the cash he invested

b.

his capital account will be credited for the amount of cash he invested

c.

a bonus will be credited for the amount of cash he invested

d.

a bonus will be distributed to the old partners’ capital accounts

138. The balance sheet of Morgan and Rockwell was as follows immediately prior to the partnership‘s liquidation: cash,

$20,000; other assets, $160,000; liabilities, $40,000; Morgan, capital, $60,000; Rockwell, capital, $80,000. The other

assets were sold for $139,000. Morgan and Rockwell share profits and losses in a 2:1 ratio. As a final cash distribution

from the liquidation, Morgan will receive cash totaling

a.

$46,000

b.

$51,000

c.

$60,000

d.

$49,500

139. Seth and Rachel have original investments of $50,000 and $100,000, respectively, in a partnership. The articles of

partnership include the following provisions regarding the division of net income: interest on original investment at 10%;

salary allowances of $27,000 and $18,000, respectively; and the remainder divided equally. How much of the net loss of

$16,000 is allocated to Seth?

a.

$8,000

b.

$6,000

c.

$4,000

d.

$16,000

140. Antonio and Barbara are partners who share income in the ratio of 1:2 and have capital balances of $40,000 and

$70,000, respectively, at the time they decide to terminate the partnership. After all noncash assets are sold and all

liabilities are paid, there is a cash balance of $80,000. What amount of loss on realization should be allocated to Barbara?

a.

$80,000

b.

$10,000

c.

$20,000

d.

$30,000

Use this information to answer the questions that follow.

The capital accounts of Harrison and Marti have balances of $160,000 and $110,000, respectively, on January 1, the

beginning of the current fiscal year. On April 10, Harrison invested an additional $20,000. During the year, Harrison and

Marti withdrew $96,000 and $78,000, respectively, and net income for the year was $264,000. The articles of partnership

make no reference to the division of net income.

141. Based on this information, the statement of partners’ equity would show what amount in the capital account for

Harrison on December 31?

a.

$216,000

Name:

Class:

Date:

chapter 12

c.

$380,000

d.

$52,000

142. Benton and Orton are partners who share income in the ratio of 1:3 and have capital balances of $70,000 and

$30,000, respectively. Ramsey is admitted to the partnership and is given a 40% interest by investing $20,000. What is

Benton’s capital balance after admitting Ramsey?

a.

$20,000

b.

$7,000

c.

$70,000

d.

$63,000

143. Partners Ken and Macki each have a $40,000 capital balance and share income and losses in the ratio of 3:2. Cash

equals $20,000, noncash assets equal $120,000, and liabilities equal $60,000. If the noncash assets are sold for $50,000,

and each partner is personally insolvent, Partner Macki will eventually receive cash of

a.

$0

b.

$10,000

c.

$12,000

d.

$20,000

144. Samuel and Darci are partners. The partnership capital for Samuel is $50,000 and that of Darci is $60,000. Josh is

admitted as a new partner by investing $50,000 cash. Josh is given a 20% interest in return for his investment. The amount

of the bonus to the old partners is

a.

$0

b.

$18,000

c.

$8,000

d.

$10,000

145. Carla and Eliza share income equally. For the current year, the partnership net income is $40,000. Carla made

withdrawals of $12,000, and Eliza made withdrawals of $21,000. At the beginning of the year, the capital account

balances were: Carla, Capital, $42,000; Eliza, Capital, $55,000. Eliza’s capital account balance at the end of the year is

a.

$34,000

b.

$54,000

c.

$78,000

d.

$75,000

Use this information to answer the questions that follow.

Sandra and Kelsey are forming a partnership. Sandra will invest a piece of equipment with a book value of $7,500 and a

fair market value of $18,000. Kelsey will invest a building with a book value of $40,000 and a fair market value of

$44,000.

146. What amount will be recorded to Kelsey’s capital account?

a.

$14,000

b.

$24,000

c.

$40,000

d.

$44,000

Name:

Class:

Date:

chapter 12

147. Carrie and Callie form a partnership in which Carrie contributes $85,000 in assets and agrees to devote half time to

the partnership. Callie contributes $50,000 in assets and agrees to devote full time to the partnership. If no additional

information is available, how will Carrie and Callie share in the division of income?

a.

63% to Carrie and 37% to Callie

b.

33% to Carrie and 67% to Callie

c.

50% to Carrie and 50% to Callie

d.

67% to Carrie and 33% to Callie

148. Tucker and Titus are partners who share income in the ratio of 3:1 (3/4 to Tucker and 1/4 to Titus). Their capital

balances are $40,000 and $60,000, respectively. The partnership generated net income of $40,000 for the year. What is

Tucker’s capital balance after closing the revenue and expense accounts to the capital accounts?

a.

$40,000

b.

$70,000

c.

$10,000

d.

$80,000

149. Henry Jones contributed equipment, inventory, and $44,000 cash to a partnership. The equipment had a book value

of $35,000 and market value of $28,000. The inventory had a book value of $25,000 but only had a market value of

$12,000 due to obsolescence. The partnership also assumed a $15,000 note payable owed by Henry that was originally

used to purchase the equipment.

What amount should be recorded to Henry’s capital account?

a.

$104,000

b.

$89,000

c.

$69,000

d.

$84,000

150. Jackson and Campbell have capital balances of $100,000 and $300,000, respectively. Jackson devotes full time and

Campbell devotes one-half time to the business. Determine the division of $150,000 of net income when there is no

reference to division in the partnership agreement.

a.

$75,000 and $75,000

b.

$37,500 and $112,500

c.

$100,000 and $50,000

d.

$112,500 and $37,500

151. Hannah Johnson contributed equipment, inventory, and $53,000 cash to a partnership. The equipment had a book

value of $25,000 and a market value of $28,000. The inventory had a book value of $50,000 but only had a market value

of $15,000 due to obsolescence. The partnership also assumed a $12,000 note payable owed by Hannah that was

originally used to purchase the equipment.

What amount should be recorded to Hannah’s capital account?

a.

$96,000

b.

$84,000

c.

$108,000

d.

$116,000

152. When an additional partner is admitted to a partnership by contribution of assets to the partnership,

Name:

Class:

Date:

chapter 12

a.

the total assets of the partnership do not change

b.

no liabilities can be contributed at the same time

c.

the amount of the cash contribution is the same as the amount of the debit to the new partner’s capital account

d.

the total of the owners’ equity accounts increases

Match each of the following statements to the term (a–h) it best describes.

a.

Deficiency

b.

Realization

c.

Proprietorship

d.

Partnership

e.

Mutual agency

f.

Liquidation

g.

Income-sharing ratio

h.

Statement of partnership equity

153. Where changes in partner capital accounts for a period of time are reported

154. The share of loss on realization is greater than the balance in partner capital

155. Each partner may act on behalf of the entire partnership so that the liabilities created by one partner become the

liabilities of all partners

156. An association of two or more persons to own and manage a business for profit

157. Business owned by a single individual

158. A step during liquidation when partnership assets are sold

159. Used to divide the excess of allowances over loss when net losses occur

160. The winding-up process of a partnership

Match each of the following statements to the term (a–h) it best describes.

a.

Partnership

b.

Partnership agreement

c.

Distribution of remaining cash to partners

d.

Mutual agency

e.

Equally

f.

Death of a partner

g.

Liquidation

h.

Unlimited liability

161. When a partnership cannot pay its debts with business assets, the partners must use personal assets to meet the debt.

162. Agreement that is the contract between partners

Name:

Class:

Date:

chapter 12

163. A voluntary association of two or more persons who co-own a business for profit

164. Every partner can bind the business to a contract within the scope of the partnership’s regular business operations.

165. The process of going out of business by selling the entity’s assets and paying its liabilities

166. Without an agreement, the law will stipulate this method of sharing profits and losses.

167. The final step in the liquidation of a partnership

168. Causes the closing of accounts and settling with a partner’s estate

169. Gavin invested $45,000 in the Jason and Kelly Partnership for ownership equity of $45,000. Prior to the investment,

land was revalued to a market value of $320,000 from a book value of $200,000. Jason and Kelly shared net income in a

1:2 ratio.

a. Journalize the entry for the revaluation of land. (The partnership does not use the temporary asset revaluation account.)

b. Journalize the entry to admit Gavin.

170. The capital accounts of Hope and Indiana have balances of $115,000 and $95,000, respectively. Clint and Casey are

to be admitted to the partnership. Clint buys 20% of Hope’s interest for $30,000 and 25% of Indiana’s interest for

$20,000. Casey contributes $45,000 cash to the partnership, for which he is to receive an ownership equity of $45,000.

a. Journalize the entries for the admission of (1) Clint and (2) Casey.

b. What are the capital balances of each partner after the admission of the new partners?

171. Holly and Luke formed a partnership, investing $240,000 and $80,000, respectively. Determine their participation in

the year’s net income of $200,000 under each of the following independent assumptions:

a.

No agreement concerning division of net income

b.

Divided in the ratio of original capital investment

c.

Interest at the rate of 15% allowed on original investments and the remainder divided in

the ratio of 2:3 (2/5 to Holly and 3/5 to Luke)

d.

Salary allowances of $50,000 and $70,000, respectively, and the balance divided

equally

e.

Allowance of interest at the rate of 15% on original investments, salary allowances of

$50,000 and $70,000, respectively, and the remainder divided equally

172. Derek and Hailey, partners sharing net income in the ratio of 2:1, admit Ben to the partnership in accordance with the

following agreement:

• Merchandise inventory recorded in the partnership accounts at $62,500 is to be revalued at its current replacement

price of $68,500.

• Ben invested $48,000 in cash for a 30% interest in the partnership, which has total net assets (assets minus

liabilities) of $130,000 that includes the inventory revaluation and the cash invested by Ben.

• The income-sharing ratio of Derek, Hailey, and Ben is to be 2:1:1.

a.

Journalize the entries for the revaluation of merchandise inventory and the admission of

Ben to the partnership. (The partnership does not use the temporary asset revaluation

account.)

Name:

Class:

Date:

chapter 12

b.

A few years later, the capital balances of Derek, Hailey, and Ben were $150,000, $90,000,

and $55,000, respectively. At this time, Kacy is admitted to the partnership by the purchase

of one-half of Derek’s interest for $80,000. Journalize the entry for the admission of Kacy

to the partnership.

173. The partnership of Miner Company began operations on January 1, with contributions as follows:

Waverley

$35,000

Marquez

40,000

The following additional partner transactions took place during the year:

• In early January, Houston is admitted to the partnership by contributing $25,000 cash for a 25% interest.

• Net income of $160,000 was earned. In addition, Waverley received a salary allowance of $30,000 for the

year. The three partners agree to an income-sharing ratio equal to their capital balances after admitting Houston.

• The partners’ withdrawals are equal to half of their respective distributions of income after salary (i.e., half their

respective portions of the $130,000).

Prepare a statement of partnership equity for the year ended December 31.

174. Jackson and Campbell have capital balances of $100,000 and $300,000 respectively. Jackson devotes full time and

Campbell one-half time to the business. Determine the division of $120,000 of net income under each of the following

assumptions:

a.

No agreement as to division of net income

b.

In ratio of capital balances

c.

In ratio of time devoted to business

d.

Interest of 10% on capital balances and the remainder divided equally

e.

Interest of 10% on capital balances, salaries of $40,000 to Jackson and $20,000 to

Campbell, and the remainder divided equally

175. Emerson and Dakota formed a partnership dividing income as follows:

1. Annual salary allowance to Emerson of $58,000

2. Interest of 8% on each partner’s capital balance on January 1

3. Any remaining net income divided equally

Emerson and Dakota had $25,000 and $140,000, respectively, in their January 1 capital balances. Net income for the year

was $220,000.

How much net income should be distributed to Dakota?

176. Prior to liquidating their partnership, Samuel and Brian had capital accounts of $60,000 and $240,000, respectively.

The partnership assets were sold for $120,000. The partnership had no liabilities. Samuel and Brian share income and

losses equally.

a. Determine the amount of Samuel’s deficiency.

b. Determine the amount distributed to Brian, assuming Samuel is unable to satisfy the deficiency.

177. Wonder purchased one-half of Darwin’s interest in the Todd and Darwin Partnership for $50,000. Prior to the

investment, land was revalued to a market value of $175,000 from a book value of $100,000. Todd and Darwin share net

income equally. Darwin had a capital balance of $40,000 prior to these transactions.

a. Journalize the entry for the revaluation of land. (The partnership does not use the temporary asset revaluation account.)

Name:

Class:

Date:

chapter 12

b. Journalize the entry to admit Wonder.

178. Gentry, sole proprietor of a hardware business, decides to form a partnership with Noel. Gentry’s accounts are as

follows:

Book Value

Market Value

Cash

$ 25,000

$ 25,000

Accounts Receivable (net)

52,000

45,000

Inventory

112,000

125,000

Land

40,000

100,000

Building (net)

300,000

340,000

Accounts Payable

25,000

25,000

Mortgage Payable

145,000

145,000

Noel agrees to contribute $80,000 for a 20% interest. Journalize the entries for (a) Gentry’s investment and (b) Noel’s

investment.

179. S. Stephens and J. Perez are partners in Space Designs. Stephens and Perez share income equally. D. Fredericks will

be admitted to the partnership. Prior to the admission, equipment was revalued downward by $8,000. The capital balances

of each partner are $100,000 and $139,000, respectively, prior to the revaluation. Space Designs does not use the

temporary asset revaluation account.

a.

Journalize the entry for the asset revaluation.

b.

Journalize the entry for Fredericks’ admission under the following independent

situations:

(1)

Fredericks purchased a 20% interest for $50,000.

(2)

Fredericks purchased a 30% interest for $125,000.

180. Gleason invested $90,000 in the James and Kirk Partnership for ownership equity of $90,000. Prior to the

investment, land was revalued to a market value of $425,000 from a book value of $200,000. James and Kirk share net

income in a 1:2 ratio.

a. Journalize the entry for the revaluation of land. (The partnership does not use the temporary asset revaluation account.)

b. Journalize the entry to admit Gleason.

181. Amazon invested $128,000 in the Jungle and River Partnership for ownership equity of $128,000. Prior to the

investment, equipment was revalued to a market value of $90,000 from a book value of $72,000. Jungle and River share

net income in a 2:1 ratio.

a. Journalize the entry for the revaluation of equipment. (The partnership does not use the temporary asset revaluation

account.)

b. Journalize the entry to admit Amazon.

182. Top Dog, LLC provides repair services for oil rigs. The firm has five members in the LLC, which did not change

between the first year and the second year. During Year 2, the business expanded into three new regions of the country.

The following revenue and employee information is provided:

Year 1

Year 2

Revenues (in thousands)

$60,525

$58,500

Number of employees

120

160

a. For Years 1 and 2, determine the revenue per employee (excluding members).

b. Interpret the results.

Name:

Class:

Date:

chapter 12

183. Malcolm has a capital balance of $90,000 after adjusting to fair market value. Celeste contributes $45,000 to receive

a 25% interest in a new partnership with Malcolm.

Determine the amount and recipient of the partner bonus.

184. Barton and Fallows form a partnership by combining the assets of their separate businesses. Barton contributes

accounts receivable with a face amount of $50,000 and equipment with a cost of $190,000 and accumulated depreciation

of $100,000. The partners agree that the equipment is to be valued at $85,000, that $3,500 of the accounts receivable are

completely worthless and are not to be accepted by the partnership, and that $1,500 is a reasonable allowance for the

uncollectibility of the remaining accounts receivable. Fallows contributes cash of $28,500 and merchandise inventory of

$55,500. The partners agree that the merchandise inventory is to be valued at $60,000. Journalize the entries in the

partnership accounts for (a) Barton’s investment and (b) Fallows’s investment.

185. Benson contributed land, inventory, and $22,000 cash to a partnership. The land had a book value of $65,000 and a

market value of $111,000. The inventory had a book value of $60,000 and a market value of $58,000. The partnership

also assumed a $52,000 note payable owned by Benson that was used originally to purchase the land.

Journalize the entry for Benson’s contribution to the partnership.

186. The capital accounts of Heidi and Moss have balances of $90,000 and $65,000, respectively, on January 1, the

beginning of the current fiscal year. On April 10, Heidi invested an additional $8,000. During the year, Heidi and Moss

withdrew $40,000 and $32,000, respectively. Revenues were $540,000 and expenses were $420,000 for the year. The

articles of partnership make no reference to the division of net income.

a. Prepare a statement of partnership equity for the partnership of Heidi and Moss.

b. Journalize the entries to:

(1) Close the revenues and expenses accounts.

(2) Close the drawing accounts.

187. After the tangible assets have been adjusted to current market prices, the capital accounts of Harper and Kahlil have

balances of $60,000 and $90,000, respectively. Fay is to be admitted to the partnership, contributing $45,000 cash, for

which she is to receive an ownership equity of $60,000. All partners share equally in income.

a. Journalize the entry for the admission of Fay, who is to receive a bonus of $15,000.

b. What are the capital balances of each partner after the admission of the new partner?

188. Sharp and Townson had capital balances of $60,000 and $120,000, respectively, on January 1 of the current year. On

May 8, Sharp invested an additional $10,000 in the partnership. During the year, Sharp and Townson withdrew $25,000

and $45,000, respectively. The revenue account at the end of the year had a balance of $600,000, and the expense

accounts had a balance of $510,000. Sharp and Townson have agreed to split net income on a 2:1 basis (2/3 to Sharp and

1/3 to Townson).

a. Prepare the statement of partnership equity for the current year.

b. Journalize the entries to close the revenue and expense accounts and the drawing accounts.

189. Trevor Smith contributed equipment, inventory, and $54,000 cash to a partnership. The equipment had a book value

of $30,000 and a market value of $36,000. The inventory had a book value of $60,000, but only had a market value of

$20,000, due to obsolescence. The partnership also assumed a $17,000 note payable owed by Smith that was used

originally to purchase the equipment.

Journalize the entry for Smith’s contribution to the partnership.

Name:

Class:

Date:

chapter 12

190. Prior to liquidating their partnership, Craig and Jenny had capital accounts of $70,000 and $110,000,

respectively. The partnership assets were sold for $285,000. The partnership had $25,000 of liabilities. Craig and Jenny

share income and losses equally. Determine the amount received by Jenny as a final distribution from liquidation of the

partnership.

191. Hamir, Darci, and Pete are partners sharing income in the ratio of 3:2:1. After the firm’s loss from liquidation is

distributed, the capital account balances were Hamir, $45,000 Dr.; Darci, $90,000 Cr., and Pete, $64,000 Cr. If Hamir is

personally bankrupt and unable to pay any of the $45,000, what will be the amount of cash received by Darci and Pete

upon liquidation? Show your work.

192. Reardon and Reese had capital balances of $140,000 and $160,000, respectively, at the beginning of the current

fiscal year. The partnership agreement provides for salary allowances of $25,000 and $35,000, respectively; an allowance

of interest at 12% on the capital balances at the beginning of the year; and the remaining net income divided equally. Net

income for the current year was $120,000.

a.

Present the Division of Net Income section of the income statement for the current year.

b.

Assuming that the net income had been $76,000 instead of $120,000, present the Division

of Net Income section of the income statement for the current year.

193. Jackson and Campbell have capital balances of $100,000 and $300,000, respectively. Jackson devotes full time and

Campbell one-half time to the business. Determine the division of $150,000 of net income under each of the following

assumptions:

a.

No agreement as to division of net income

b.

In ratio of capital balances

c.

In ratio of time devoted to business

194. Emmett and Sierra formed a partnership dividing income as follows:

1. Annual salary allowance to Emmett of $48,000

2. Interest of 8% on each partner’s capital balance on January 1

3. Any remaining net income divided equally

Emmett and Sierra had $25,000 and $140,000, respectively, in their January 1 capital balances. Net income for the year

was $200,000.

How much net income should be distributed to Emmett?

195. After discontinuing the ordinary business operations and closing the accounts on May 7, the ledger of the partnership

of Anna, Brian, and Cole indicated the following:

Cash

$ 7,500

Noncash Assets

105,000

Liabilities

$ 27,500

Anna, Capital

45,000

Brian, Capital

15,000

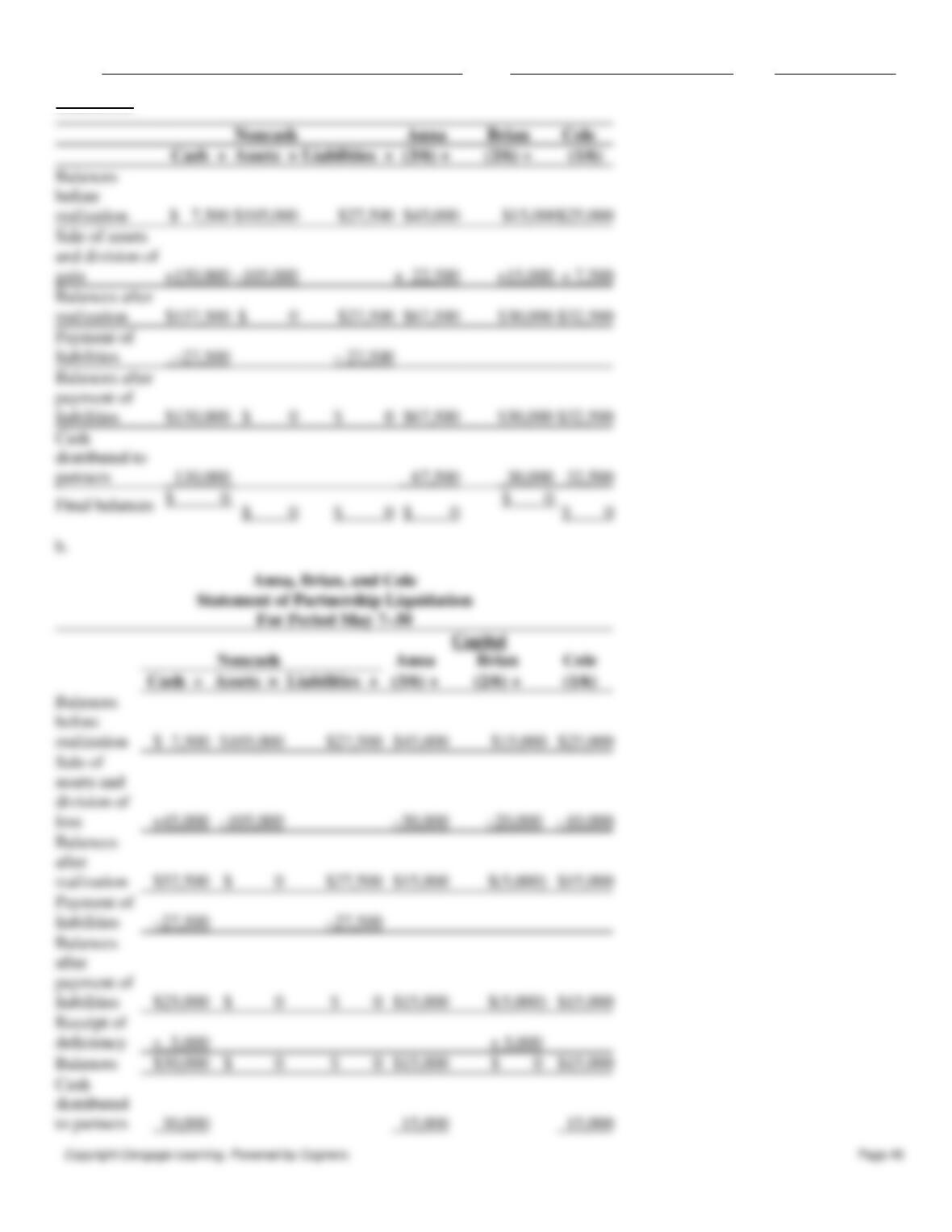

Cole, Capital

25,000

$112,500

$112,500

The partners share net income and losses in the ratio of 3:2:1. Between May 7 and May 30, the noncash assets were sold

for $150,000, the liabilities were paid, and the remaining cash was distributed to the partners.

a.

Prepare a statement of partnership liquidation.

Name:

Class:

Date:

chapter 12

b.

Assume the same facts as in (a), except that the noncash assets were sold for $45,000

and any partner with a capital deficiency pays the amount of the deficiency to the

partnership. Prepare a statement of partnership liquidation.

196. Prior to liquidating their partnership, Porter and Robert had capital account balances of $160,000 and $100,000,

respectively. Prior to liquidation, the partnership had no cash assets other than what was realized from the sale of the

partnership assets. These partnership assets were sold for $250,000. The partnership had $10,000 of liabilities. Porter and

Robert share income and losses equally.

Determine the amount received by Porter as a final distribution from liquidation of the partnership.

197. Rodgers and Winter had capital balances of $60,000 and $90,000, respectively, at the beginning of the current fiscal

year. The articles of partnership provide for salary allowances of $25,000 and $30,000, respectively; an allowance of

interest at 12% on the capital balances at the beginning of the year; and the remaining net income divided equally. Net

income for the current year was $110,000.

a.

Present the Division of Net Income section of the income statement for the current year.

b.

Assuming that the net income had been $65,000 instead of $110,000, present the Division of

Net Income section of the income statement for the current year.

198. Watson purchased one-half of Dalton’s interest in the Patton and Dalton Partnership for $45,000. Prior to the

investment, land was revalued to a market value of $135,000 from a book value of $93,000. Patton and Dalton share net

income equally. Dalton had a capital balance of $35,000 prior to these transactions.

a. Journalize the entry for the revaluation of land. (The partnership does not use the temporary asset revaluation account.)

b. Journalize the entry to admit Watson.

199. What is a partnership? Describe a partnership in terms of its characteristics.

200. Immediately prior to the process of liquidation, partners Micco, Niccum, and Orwell have capital balances of

$70,000, $20,000, and $30,000, respectively. There is a cash balance of $10,000, noncash assets total $160,000, and

liabilities total $50,000. The partners share net income and losses in the ratio of 2:2:1.

Journalize the entries for the following liquidation using Noncash Assets as the account title for the noncash assets and

Liabilities as the account title for all creditors’ claims.

a.

Sold the noncash assets for $80,000 in cash.

b.

Divided the loss on realization.

c.

Paid the liabilities.

d.

Received cash from the partner with the deficiency.

e.

Distributed the cash to the partners.

201. Kala and Leah, partners in Best Designs, have capital balances of $40,000 and $60,000, respectively. Adam joins the

partnership by buying one-half of Kala’s interest for $30,000. In addition, because of Adam’s outstanding sales skills, the

partners agree to increase his interest to 40% if he invests another $10,000. The income-sharing ratio of Kala, Leah, and

Adam is 4:3:1.

a.

Journalize the entries for the admission of Adam to the partnership.

b.

Immediately after Adam’s admission to the partnership, Leah sells one-fourth of her

interest to Denton for $35,000. Journalize the entry for this transaction.

202. Holly and Luke formed a partnership, investing $240,000 and $80,000, respectively. Determine their participation in

the year’s net income of $380,000 under each of the following independent assumptions:

Name:

Class:

Date:

chapter 12

a.

No agreement concerning division of net income

b.

Divided in the ratio of original capital investment

c.

Interest at the rate of 15% allowed on original investments and the remainder divided in

the ratio of 2:3 (2/5 to Holly and 3/5 to Luke)

d.

Salary allowances of $50,000 and $70,000, respectively, and the balance divided equally

e.

Allowance of interest at the rate of 15% on original investments, salary allowances of

$50,000 and $70,000, respectively, and the remainder divided equally

203. Jesse and Tim form a partnership by combining the assets of their separate businesses. Jesse contributes accounts

receivable with a face amount of $50,000 and equipment with a cost of $180,000 and accumulated depreciation of

$100,000. The partners agree that the equipment is to be valued at $58,000, that $3,500 of the accounts receivable are

completely worthless and are not to be accepted by the partnership, and that $2,000 is a reasonable allowance for the

uncollectibility of the remaining accounts receivable. Tim contributes cash of $21,000 and merchandise inventory of

$44,500. The partners agree that the merchandise inventory is to be valued at $48,000. Journalize the entries in the

partnership accounts for (a) Jesse’s investment and (b) Tim’s investment.