101. Return on assets is calculated as net income divided by ending total assets.

102. Profit margin measures the income earned on each dollar of sales, and is calculated by

dividing net income by net sales.

103. Asset turnover measures sales volume in relation to the investment in assets, and is

calculated as net sales divided by average total assets.

104. Return on equity is calculated by dividing the stock return by average stockholders’

equity.

105. The price-earnings (PE) ratio compares a company’s share price with its earnings per

share.

106. Growth stocks have high expectations of future earnings growth, and therefore, usually

trade at higher PE ratios.

107. Value stocks have lower share prices in relationship to their fundamental ratios, and

therefore, trade at lower PE ratios.

108. A discontinued operation is the sale or disposal of any long-term asset.

109. We report any profits or losses on discontinued operations in the current year, separately

from profits and losses on the portion of the business that will continue.

110. To be an extraordinary item, an event that produces a gain or loss must be either unusual

in nature or infrequent in occurrence.

111. We report extraordinary items separately, net of taxes, near the bottom of the income

statement just below discontinued operations.

112. If an item meets one but not both criteria for extraordinary item treatment, it is correctly

excluded from extraordinary items and included with other revenue and expenses.

113. The location where a loss is reported in the income statement does not really matter as

long as the loss is reported.

114. When using a company’s current earnings to estimate future earnings performance,

investors normally should exclude discontinued operations and extraordinary items.

115. Conservative accounting practices are those that result in reporting higher income, higher

assets, and lower liabilities.

116. Conservative accounting practices are those that result in reporting lower income, lower

assets, and higher liabilities.

117. A larger estimation of the allowance for uncollectible accounts, the write-down of

overvalued inventory and the use of a shorter useful life for depreciation are all examples of

conservative accounting.

118. Aggressive accounting practices result in reporting higher income, higher assets, and

lower liabilities.

119. Changes in accounting estimates usually have no effect on a company’s underlying cash

flows.

120. Listed below are seven terms followed by a list of phrases that describe or characterize

the terms. Match each phrase with the best term placing the number designating the term in

the space provided.

1. Vertical

analysis

2. Horizontal

analysis

3. Liquidity

4. Value Stocks

5. Growth stocks

6. Solvency

7. Profitability

ratios

(A)Analyzes trends in financial statement data for a

single company over time.

(B) Have lower share prices in relationship to their

fundamental ratios and therefore trade at lower PE ratios.

(C) Expresses each item in a financial statement as a

percentage of the same base amount.

(D) Refers to a company’s ability to pay its current

liabilities.

(E) Refers to a company’s ability to pay its long-term

liabilities.

(F) Have high expectations of future earnings and

therefore usually trade at higher P/E ratios.

(G) Measure the earnings or operating effectiveness of a

company.

121. Listed below are eight terms followed by a list of phrases that describe or characterize

the terms. Match each phrase with the best term placing the number designating the term in

the space provided.

1. Liquidity

2. Conservative

accounting practices

3. Solvency

4. Extraordinary item

5. Discontinued operation

6. Horizontal analysis

7. Vertical analysis

8. Aggressive accounting

practices

(A)A company’s ability to pay its current

liabilities.

(B)Accounting choices that result in reporting

lower income, lower assets, and higher liabilities.

(C)A profit or loss unusual in nature and

infrequent in occurrence.

(D)Accounting choices that result in reporting

higher income, higher assets, and lower liabilities.

(E)A tool to analyze trends in financial statement

data for a single company over time.

(F)The sale or disposal of a significant

component of a company’s operations.

(G)A means to express each item in a financial

statement as a percentage of a base amount.

(H)A company’s ability to pay its long-term

liabilities.

122. Listed below are eight risk ratios followed by a list of phrases that describe or

characterize the ratios. Match each phrase with the correct ratio placing the number

designating the ratio in the space provided.

1. Debt to equity

ratio

2. Acid-test ratio

3. Receivables

turnover ratio

4. Times interest

earned ratio

5. Inventory

turnover ratio

6. Average

collection period

7. Average days in

inventory

8. Current ratio

(A)Cost of goods sold divided by average inventory; the

number of times the firm sells its average inventory balance

during a reporting period.

(B)Total liabilities divided by total stockholders’ equity;

measure a company’s solvency risk.

(C)Approximate number of days the average inventory

is held.

(D) Ratio that compares interest expense with income

available to pay those charges.

(E)Net sales divided by average accounts receivable; the

number of times during a year that the average accounts

receivable balance is collected.

(F)Cash, short-term investments, and accounts

receivable divided by current liabilities; measures the

availability of liquid current assets to pay current liabilities.

(G) Current assets divided by current liabilities; measures

the availability of current assets to pay current liabilities.

(H)Approximate number of days the average accounts

receivable balance is outstanding.

Answer:

1(B); 2(F); 3(E); 4(D); 5(A); 6(H); 7(C); 8(G)

123. Listed below are six profitability ratios followed by a list of phrases that describe or

characterize the ratios. Match each phrase with the correct ratio placing the number

designating the ratio in the space provided.

1. Price-earnings

(PE) ratio

2. Return on equity

3. Asset turnover

4. Profit margin

5. Return on assets

6. Gross profit ratio

(A) Net income divided by average total assets;

measures the amount of net income generated for each

dollar invested in assets.

(B) Compares a company’s share price with its earnings

per share.

(C) Net income divided by average stockholders’

equity; measures the income generated per dollar of

equity.

(D)Gross profit divided by net sales; measures the

amount by which the sale price of inventory exceeds its

cost per dollar of sales.

(E)Net sales divided by average total assets; which

measures the sales per dollar of assets invested.

(F)Net income divided by net sales; indicates the

earnings per dollar of sales.

124. Listed below are five terms followed by a list of phrases that describe or characterize the

terms. Match each phrase with the best term placing the number designating the term in the

space provided.

1. Quality of earnings

2. Aggressive

accounting practices

3. Discontinued

operation

4. Extraordinary item

5. Conservative

accounting practices

(A) An event that is (1) unusual in nature and (2)

infrequent in occurrence.

(B) The sale or disposal of a significant component of

a company’s operations.

(C) Refers to the ability of reported earnings to reflect

the company’s true earnings, as well as the usefulness of

reported earnings to predict future earnings.

(D)Practices that result in reporting lower income,

lower assets, and higher liabilities.

(E)Practices that result in reporting higher income,

higher assets, and lower liabilities.

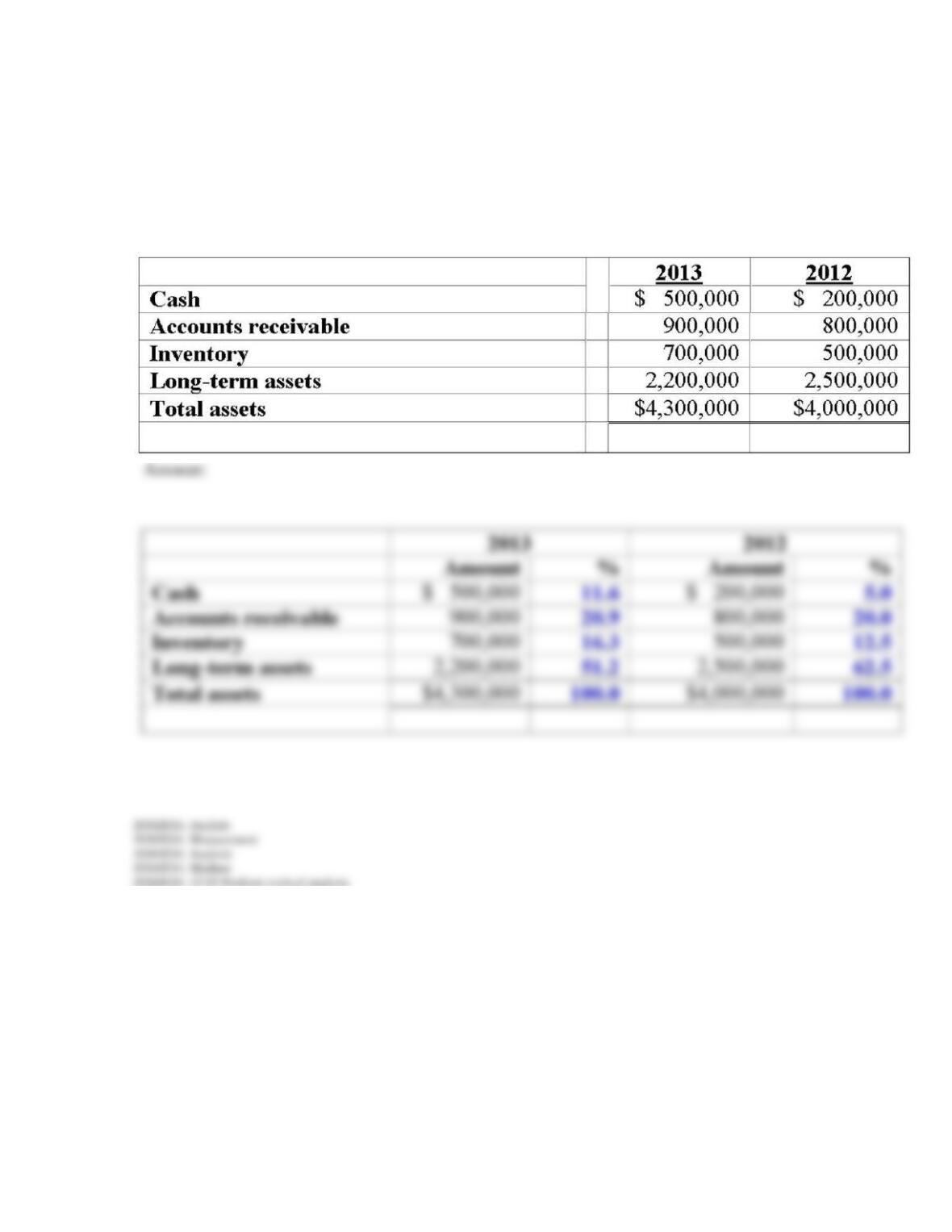

125. Perform a vertical analysis on the following information:

126. Explain the difference between vertical and horizontal analysis.

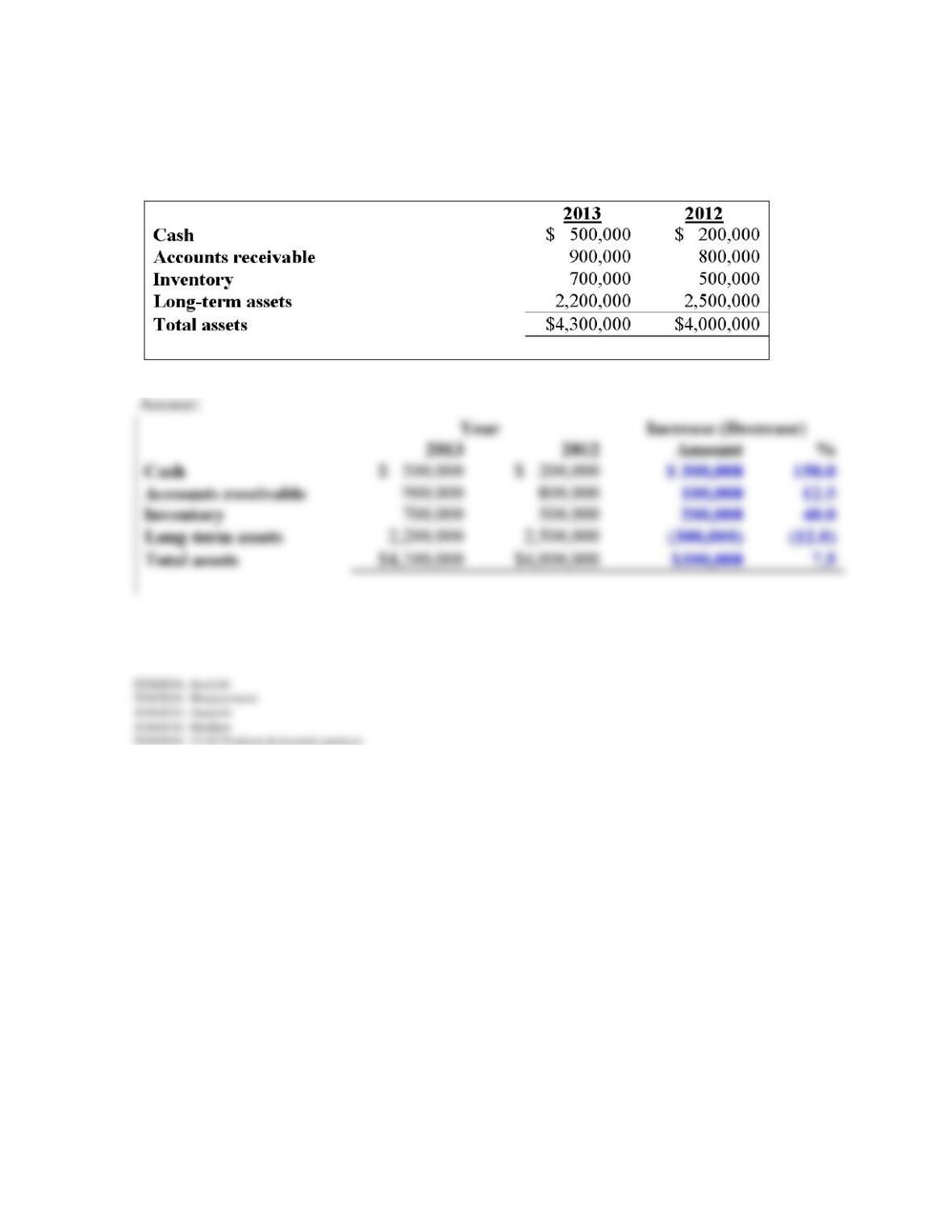

127. Perform a horizontal analysis on the following information providing both the dollar

amount and percentage change:

128. Assume a company’s sales are $1.6 million in 2011, $1.8 million in 2012, and $1.7

million in 2013. What is the percentage change from 2011 to 2012? What is the percentage

change from 2012 to 2013? Be sure to indicate whether the percentage change is an increase

or a decrease.

129. If a company’s sales are $648,000 in 2012, and this represents an 8% increase over sales

in 2011, what were sales in 2011?

130. United Products began the year with an Accounts Receivable balance of $250,000, and

had a year-end balance of $280,000. Credit sales of $800,000 generated a gross profit of

$150,000. Calculate the receivables turnover ratio for the year.