46. Stealth Company’s 2013 profit margin is:

47. Stealth Company’s 2013 asset turnover is:

48. Stealth Company’s 2013 return on equity is:

49. TPX Company’s 2013 gross profit ratio is:

50. TPX Company’s 2013 return on assets is:

51. TPX Company’s 2013 profit margin is:

52. TPX Company’s 2013 asset turnover is:

53. TPX Company’s 2013 return on equity is:

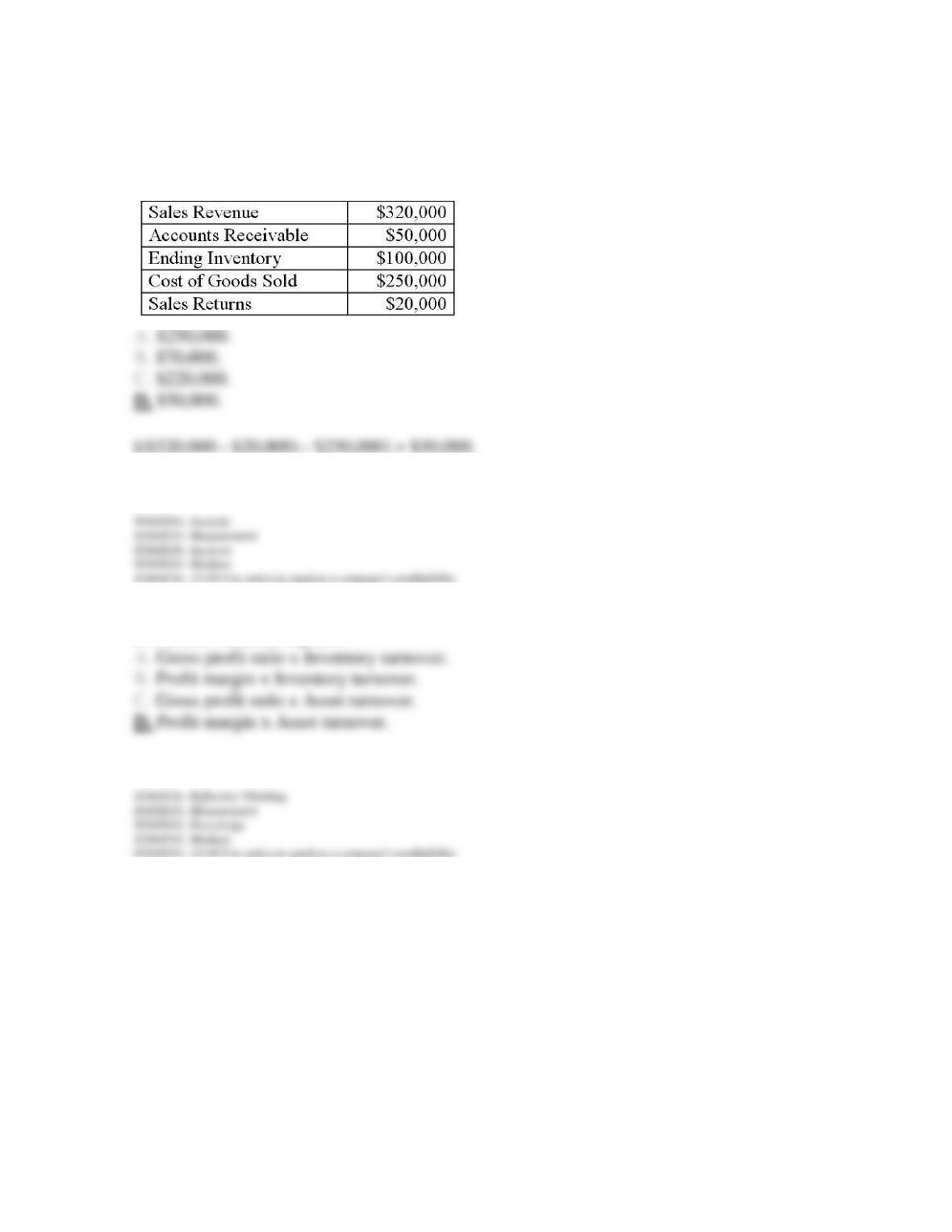

54. Given the information below, what is the company’s gross profit?

55. Return on assets equals:

56. Nerf Mania reports net income of $500,000, net sales of $4,000,000, and average assets of

$2,000,000. The return on assets is:

57. Nerf Mania reports net income of $500,000, net sales of $4,000,000, and average assets of

$2,000,000. The profit margin is:

58. Nerf Mania reports net income of $500,000, net sales of $4,000,000, and average assets of

$2,000,000. The asset turnover is:

59. Richard’s Sporting Goods reports net income of $100,000, net sales of $500,000, and

average assets of $1,000,000. The return on assets is:

60. Richard’s Sporting Goods reports net income of $100,000, net sales of $500,000, and

average assets of $1,000,000. The profit margin is:

61. Richard’s Sporting Goods reports net income of $100,000, net sales of $500,000, and

average assets of $1,000,000. The asset turnover is:

62. The sale or disposal of a significant component of a company’s operations is referred to

as:

63. A discontinued operation refers to:

64. An extraordinary item must meet which of the following criteria?

65. Extraordinary items:

66. Which of the following items is most likely to be reported as an extraordinary loss?

67. What is the correct order to present the following items on the income statement?

68. Popson Inc. incurred a material loss which was not unusual in character, but was clearly

an infrequent occurrence. This loss should be reported as:

69. The financial statements of a firm that uses more aggressive accounting practices would

be likely to report:

70. Which of the following is NOT an example of applying conservatism in accounting?

71. Which of the following is a conservative accounting practice?

72. Which of the following is an aggressive accounting practice?

73. Which of the following is a conservative accounting practice?

74. Which of the following is an aggressive accounting practice?

75. We can use ratios to help evaluate a firm’s performance and financial position.

76. Vertical analysis expresses each item in a financial statement as a percentage of the same

base amount.

77. Vertical analysis calculates the amount and percentage change of an account over time.

78. We use vertical analysis for income statement accounts, but not balance sheet accounts.

79. We use vertical analysis to express each income statement item as a percentage of sales.

80. For vertical analysis, we express each balance sheet item as a percentage of sales.

81. Horizontal analysis analyzes trends in financial statement data for a single company over

time.

82. If the base-year amount is zero, we can’t calculate a percentage change under horizontal

analysis.

83. Using horizontal analysis, if the base year is negative and the following year is positive,

the percentage change is just as useful as if the base year and the following year were both

positive.

84. We use horizontal analysis to analyze trends in financial statement data, such as the dollar

amount of change and the percentage change, for one company over time.

85. We measure income statement accounts at a point in time and balance sheet accounts over

a period of time.

86. Ratios that compare an income statement account with a balance sheet account should

express the balance sheet account as an average of the beginning and ending balances.

87. Every liquidity ratio is calculated using one or more current asset accounts.

88. Solvency refers to a company’s ability to pay its current liabilities while liquidity refers to

a company’s ability to pay its long-term liabilities.

89. The receivables turnover ratio measures how many times, on average, a company collects

its receivables during the year.

90. A low receivables turnover ratio is a positive sign that a company can quickly turn its

receivables into cash.

91. The average collection period converts the receivables turnover ratio into days.

92. A low inventory turnover ratio usually is a positive sign and indicates that inventory is

selling quickly.

93. An extremely high inventory turnover ratio may be a signal that the company is losing

sales due to inventory shortages.

94. The average days in inventory converts the inventory turnover ratio into days.

95. A low current ratio indicates that a company has sufficient current assets to pay current

liabilities as they become due.

96. The acid-test ratio is always smaller than the current ratio.

97. Other things being equal, the higher the debt to equity ratio, the higher the risk of

bankruptcy.

98. We use the times interest earned ratio to compare interest payments with a company’s

income available to pay those charges.

99. We calculate the times interest earned ratio by dividing net income by interest expense.

100. The gross profit ratio is calculated as gross profit divided by net sales.