1. In a standard costing system, underapplied or overapplied fixed manufacturing overhead is

equal to the sum of the fixed manufacturing overhead budget variance and the fixed

manufacturing overhead volume variance.

2. In a standard costing system where the denominator activity for the predetermined

overhead rate is labor-hours, overhead costs are applied to work in process on the basis of actual

hours worked.

3. A company has a standard cost system in which fixed and variable manufacturing

overhead costs are applied to products on the basis of direct labor-hours. The company’s choice

of the denominator level of activity affects the Fixed component of the predetermined overhead

rate.

4. A company has a standard cost system in which fixed and variable manufacturing

overhead costs are applied to products on the basis of direct labor-hours. The company’s choice

of the denominator level of activity affects the Variable component of the predetermined

overhead rate.

5. A company has a standard cost system in which fixed and variable manufacturing

overhead costs are applied to products on the basis of direct labor-hours. The amount of

overhead that the company would apply to finished production would ordinarily be the standard

hours allowed for the actual units of finished output times the predetermined overhead rate per

direct labor-hour.

6. A volume variance and an efficiency variance are computed for fixed manufacturing

overhead costs.

7. The budget variance represents the difference between the actual fixed manufacturing

overhead cost incurred during a period and the budgeted fixed manufacturing overhead cost.

8. The fixed manufacturing overhead budget variance is not controllable by managers

because fixed costs are not controllable.

9. If the fixed manufacturing overhead volume variance is unfavorable, too much has been

spent on fixed manufacturing overhead items.

10. An unfavorable volume variance means that a firm operated at an activity level that was

above the activity level planned for the period.

11. The fixed manufacturing overhead volume variance will be unfavorable if production

volume is less than sales volume.

12. A company has a standard cost system in which fixed and variable manufacturing

overhead costs are applied to products on the basis of direct labor-hours. A fixed manufacturing

overhead volume variance will necessarily occur in a month in which there is a fixed

manufacturing overhead budget variance.

13. The terms “standard quantity allowed” or “standard hours allowed” means:

14. The higher the denominator level of activity:

15. Overhead is applied to work in process in a standard costing system by:

16. In a standard cost system, the volume variance will be unfavorable when:

17. Rameriz Company erred in selecting a denominator activity and chose a much higher level

than was realistic. This error would most likely result in a large:

18. The economic impact of the inability to reach a target denominator level of activity would

best be measured by:

19. Dosier Corporation has a standard cost system in which it applies manufacturing

overhead to products on the basis of standard machine-hours (MHs). The company has provided

the following data for the most recent month:

What was the fixed manufacturing overhead budget variance for the month?

20. Moralez Corporation has a standard cost system in which it applies manufacturing

overhead to products on the basis of standard machine-hours (MHs). The company has provided

the following data for the most recent month:

What was the total of the variable overhead rate and fixed manufacturing overhead budget

variances for the month?

21. Sommers Fabrication Corporation has a standard cost system in which it applies

manufacturing overhead to products on the basis of standard machine-hours (MHs) at $9.70 per

MH. The company budgeted its fixed manufacturing overhead cost at $67,000 for the month.

During the month, the actual total variable manufacturing overhead was $66,660 and the actual

total fixed manufacturing overhead was $70,000. The actual level of activity for the period was

6,600 MHs. What was the total of the variable overhead rate and fixed manufacturing overhead

budget variances for the month?

22. Meister Electronics Corporation has a standard cost system in which it applies

manufacturing overhead to products on the basis of standard machine-hours (MHs). The

company had budgeted its fixed manufacturing overhead cost at $68,800 for the month and its

level of activity at 2,000 MHs. The actual total fixed manufacturing overhead was $73,300 for the

month and the actual level of activity was 1,800 MHs. What was the fixed manufacturing

overhead budget variance for the month to the nearest dollar?

23. The Ammon Company uses a standard cost system in which manufacturing overhead is

applied to units on the basis of standard machine-hours. During July, the company budgeted

$350,000 in manufacturing overhead cost at a denominator activity of 25,000 machine-hours. At

standard, each unit of finished product requires 5 machine-hours. The following cost and activity

were recorded during July:

The amount of overhead cost that the company applied to work in process for July was:

24. At the end of the year, actual manufacturing overhead costs were $110,000 and applied

manufacturing overhead costs were $118,800. If the denominator activity for the year was 20,000

machine-hours, and if 22,000 standard machine-hours were allowed for the year’s production, the

predetermined overhead rate per machine-hour was:

25. Rubyor Corporation bases its predetermined overhead rate on variable manufacturing

overhead cost of $10.70 per machine-hour and fixed manufacturing overhead cost of $821,104

per period. If the denominator level of activity is 7,300 machine-hours, the variable element in the

predetermined overhead rate would be:

26. Heersink Corporation bases its predetermined overhead rate on variable manufacturing

overhead cost of $10.50 per machine-hour and fixed manufacturing overhead cost of $108,108

per period. If the denominator level of activity is 2,700 machine-hours, the fixed element in the

predetermined overhead rate would be:

27. Morisey Corporation bases its predetermined overhead rate on variable manufacturing

overhead cost of $8.60 per machine-hour and fixed manufacturing overhead cost of $457,002 per

period. If the denominator level of activity is 6,300 machine-hours, the predetermined overhead

rate would be:

28. Jaune Company uses a standard cost system in which it applies manufacturing overhead

to units of product on the basis of standard direct labor-hours (DLHs). The following data pertain

to last month’s operations:

The fixed manufacturing overhead budget variance is:

29. Jay Company uses a standard cost system in which it applies manufacturing overhead to

units of product on the basis of standard direct labor-hours (DLHs). The information below

pertains to a recent month’s activity:

The volume variance would be:

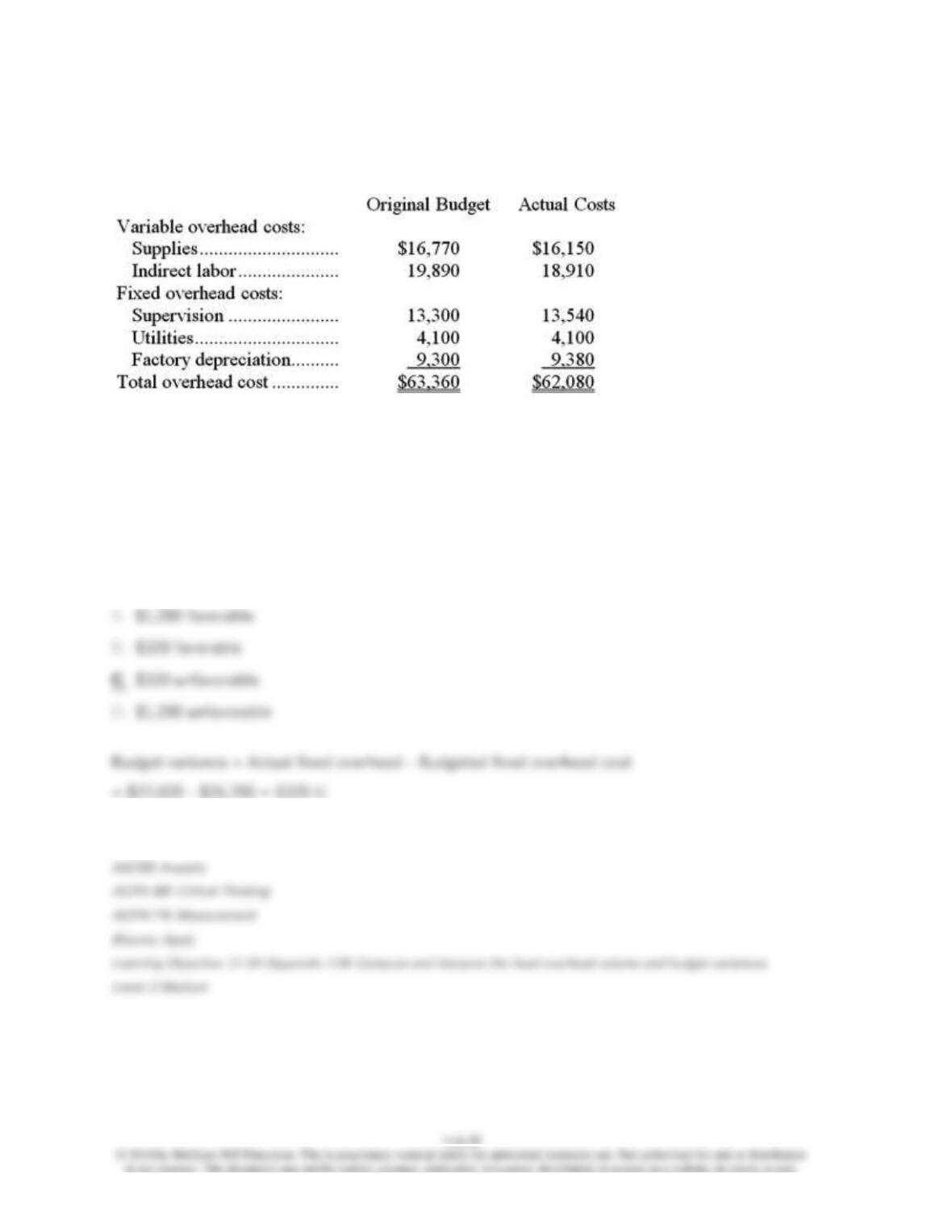

30. Coskey Corporation applies manufacturing overhead to products on the basis of standard

machine-hours. Budgeted and actual overhead costs for the month appear below:

The company based its original budget on 3,900 machine-hours. The company actually worked

3,580 machine-hours during the month. The standard hours allowed for the actual output of the

month totaled 3,770 machine-hours. What was the overall fixed manufacturing overhead budget

variance for the month?