Chapter 11: Cost Behavior and Cost-Volume-Profit Analysis

83. Which ratio indicates the percentage of each sales dollar that is available to cover fixed costs

and to provide a profit?

a. Margin of safety ratio

b. Contribution margin ratio

c. Costs and expenses ratio

d. Profit ratio

84. Variable costs as a percentage of sales for Protoveo Inc. are 65%, sales are $500,000, and

fixed costs are $125,000. How much would operating income change if sales decrease by

$10,000?

a. $3,500 increase

b. $3,500 decrease

c. $3,250 decrease

d. $3,500 increase

85. If sales are $820,000, variable costs are 68% of sales, and operating income is $260,000, what

is the contribution margin ratio?

a. 53%

b. 38%

c. 47%

d. 32%

86. Alpha Inc. operated at 75% of capacity for the past year during which fixed costs were

$225,000, variable costs were 70% of sales, and sales were $850,000. Operating profit was:

a. $ 225,000

b. $595,000

c. $56,250

d. $30,000.

87. What is the contribution margin ratio of SuperGalaxy Enterprises with sales of $120,000, 65%

of sales are variable costs, and operating income of $24,000?

a. 56%

b. 35%

c. 20%

d. 25%

Chapter 11: Cost Behavior and Cost-Volume-Profit Analysis

88. Wiles Inc.’s unit selling price is $40, the unit variable costs is $30, fixed costs are $135,000,

and current sales are 10,000 units. How much would operating income change if sales increase

by 5,000 units?

a. $50,000 increase

b. $65,000 decrease

c. $100,000 increase

d. $50,000 decrease

89. Compute the break-even point(in dollars) if fixed costs are $540,000 and variable cost are 70%

of sales.

a. $3,850,000

b. $1,800,000

c. $1,650,000

d. $900,000

90. If fixed costs are $250,000, the unit selling price is $105, and the unit variable cost is $65,

what is the break-even sales (in units)?

a. 6,250 units

b. 2,381 units

c. 10,000 units

d. 3,846 units

91. If fixed costs are $750,000 and variable costs are 60% of sales, what is the break-even point

(in dollars)?

a. $1,875,000

b. $1,250,000

c. $1,666,667

d. $1,350,000

Chapter 11: Cost Behavior and Cost-Volume-Profit Analysis

92. Foggy Co. has the following operating data for its manufacturing operations:

Unit selling price

$250

Unit variable cost

$100

Total fixed costs

$840,000

The company has decided to increase the wages of hourly workers, which will increase the

unit variable cost by 10%. Increases in the salaries of factory supervisors and property taxes

for the factory will increase fixed costs by 4%. If sales prices are held constant, the break-even

point for Foggy Co. will:

a. increase by 400 units.

b. increase by 640 units.

c. decrease by 640 units.

d. increase by 800 units.

93. If fixed costs are $350,000, the unit selling price is $80, and the unit variable cost is $30, what

is the break-even sales (in units)?

a. 3,200 units

b. 7,000 units

c. 11,667 units

d. 4,375 units

94. Currently, fixed costs are $810,000, the unit selling price is $60, and the unit variable cost is

$48. What would be the break-even sales (in units), if the variable cost is increased by $2?

a. 16,200 units

b. 57,875 units

c. 81,000 units

d. 67,500 units

95. Omega Inc. is expecting a reduction of $25,000 in fixed costs of $725,000. What will be the

change in break-even sales( in units), if selling price per unit is $50 and the unit variable cost

is $35?

a. 48,333 units

b. 46,667 units

c. 1,667 units

d. 2,500 units

Chapter 11: Cost Behavior and Cost-Volume-Profit Analysis

96. Currently, fixed costs are $540,000, the unit selling price is $95, and the unit variable cost is

$60. What would be the break-even sales (in units), if the unit selling price is increased by

$10?

a. 5,294 units

b. 9,000 units

c. 12,857 units

d. 12,000 units

97. Snower Corporation sells product G for $150 per unit, the variable cost per unit is $105, and

the fixed costs are $720,000. What is the sales (in dollars) required to realize income from

operations of $40,000?

a. $2,533,333

b. $1,773,333

c. $2,400,000

d. $1,680,000

98. If fixed costs are $790,000 and the unit contribution margin is $60, what amount of units must

be sold in order to have a zero profit?

a. 8,353 units

b. 13,167 units

c. 6,570 units

d. 65,833 units

99. If fixed costs are $550,000 and the unit contribution margin is $15, what amount of units must

be sold in order to realize an operating income of $125,000?

a. 45,000 units

b. 10,417 units

c. 45,833 units

d. 28,333 units

100. Currently, fixed costs are $500,000 and the unit contribution margin is $40. What would be the

break-even point in units if fixed costs are reduced by $80,000?

a. 14,500 units

b. 20,000 units

c. 10,500 units

d. 12,500 units

Chapter 11: Cost Behavior and Cost-Volume-Profit Analysis

101. Currently, fixed costs are $561,000 and the unit contribution margin is $10. What would be the

break-even point in units if variable cost is decreased by $0.50 per unit?

a. 59,053 units

b. 56,100 units

c. 53,429 units

d. 60,000 units

102. If variable costs per unit increased because of an increase in hourly wage rates, the break-even

point would:

a. decrease.

b. increase.

c. remain the same.

d. increase or decrease, depending upon the percentage increase in wage rates.

103. If variable costs per unit decreased because of a decrease in utility rates, the break-even point

would:

a. decrease.

b. increase.

c. remain the same.

d. increase or decrease, depending upon the percentage increase in utility rates.

104. Which of the following conditions would cause the break-even point to decrease?

a. Increase in total fixed costs

b. Decrease in unit selling price

c. Decrease in unit variable cost

d. Increase in unit variable cost

105. Which of the following conditions would cause the break-even point to increase?

a. Decrease in total fixed costs

b. Increase in unit selling price

c. Decrease in unit variable cost

d. Increase in unit variable cost

Chapter 11: Cost Behavior and Cost-Volume-Profit Analysis

106. Which of the following conditions would cause the break-even point to increase?

a. Increase in total fixed costs

b. Increase in unit selling price

c. Decrease in unit variable cost

d. Decrease in total fixed costs

107. Rouney Co. has budgeted that factory supervisors’ salary will increase by 10%. If selling

prices and all other cost relationships are held constant, next year’s break-even point would:

a. decrease by 10%.

b. increase by 10%.

c. remain constant.

d. increase at a rate greater than 10%.

108. Vest Food Co. has the following operating data:

Unit selling price

$ 10.00

Unit variable

6.00

Fixed costs

960,000

The company is contemplating moving to another state where direct labor costs can be

reduced, thereby reducing the unit variable cost by 10%. The state where the company

currently operates has offered to reduce property taxes to encourage Vest to stay. The

minimum amount of property tax savings necessary to keep the company, assuming no other

changes, would be:

a. $152,016.

b. $240,000.

c. $208,696.

d. $125,217.

109. If the contribution margin ratio for Harrison Company is 38%, sales were $425,000, and fixed

costs were $100,000, what was the income from operations?

a. $163,500

b. $161,500

c. $54,730

d. $61,500

Chapter 11: Cost Behavior and Cost-Volume-Profit Analysis

110. The point where the sales line and the total costs line intersect on the cost-volume-profit chart

represents:

a. the maximum possible operating loss.

b. the maximum possible operating income.

c. the total fixed costs.

d. the break-even point.

111. The point where the profit line intersects the horizontal axis on the profit-volume chart

represents:

a. the maximum possible operating loss.

b. the maximum possible operating income.

c. the total fixed costs.

d. the break-even point.

112. With the aid of computer software, managers can vary assumptions regarding selling prices,

costs, and volume and can immediately see the effects of each change on the break-even point

and profit. Such an analysis is called:

a. “what if” or sensitivity analysis.

b. vary the data analysis.

c. computer-aided analysis.

d. data gathering.

113. The point where the profit line intersects the left vertical axis on the profit-volume chart

represents:

a. the maximum possible operating loss.

b. the maximum possible operating income.

c. the total fixed costs.

d. the break-even point.

114. Clinton Co. has an operating leverage of 4. Sales are expected to increase by 8% next year.

Operating income is:

a. unaffected.

b. expected to increase by 2%.

c. expected to increase by 32%.

d. expected to increase by 4 times.

Chapter 11: Cost Behavior and Cost-Volume-Profit Analysis

Kennedy Co. sells two products, Arks and Bins. Last year, Kennedy sold 32,000 units of Arks

and 18,000 units of Bins. Related data are:

Unit Selling

Unit Variable

Unit Contribution

Product

Price

Cost

Margin

Arks

$ 80

$20

$60

Bins

120

40

80

Use the above given data to solve the following questions:

115. Refer to the information provided for Kennedy Co. What was Kennedy’s sales mix last year?

a. 40% Arks, 60% Bins

b. 43% Arks, 57% Bins

c. 54% Arks, 46% Bins

d. 64% Arks, 36% Bins

116. Refer to the information provided for Kennedy Co. What was Kennedy’s overall product’s unit

selling price?

a. $97.60

b. $104.00

c. $102.40

d. $94.40

117. Refer to the information provided for Kennedy Co. What was Kennedy’s overall product’s unit

variable cost?

a. $32.00

b. $30.00

c. $28.80

d. $27.20

118. Refer to the information provided for Kennedy Co. What was Kennedy’s overall product’s unit

contribution margin?

a. $67.20

b. $70.00

c. $72.00

d. $100.00

Chapter 11: Cost Behavior and Cost-Volume-Profit Analysis

119. Refer to the information provided for Kennedy Co. Assuming that last year’s fixed costs

totaled $910,000, what was Kennedy’s break-even point in units?

a. 9,100 units

b. 13,000 units

c. 13,227 units

d. 13,542 units

120. Assume that Crowson Co. sold 8,000 units of Product A and 2,000 units of Product B in the

last year. The unit contribution margins for Products A and B are $20 and $45, respectively.

Crowson has fixed costs of $350,000. The break-even point in units is:

a. 14,000 units.

b. 25,278 units.

c. 8,000 units.

d. 10,769 units.

121. The relative distribution of sales among the various products sold by a business is termed as:

a. business’s basket of goods.

b. contribution margin mix.

c. sales mix.

d. product portfolio.

122. When a business sells more than one product at varying selling prices, the business’s break-

even point can be determined as long as the number of products does not exceed:

a. two.

b. three.

c. fifteen.

d. there is no limit.

123. If a business had sales of $4,000,000, fixed costs of $1,200,000, a margin of safety of 25%,

and a contribution margin ratio of 40%, what was the break-even point?

a. $3,000,000

b. $2,800,000

c. $4,800,000

d. $2,000,000

Chapter 11: Cost Behavior and Cost-Volume-Profit Analysis

124. If a business had sales of $4,000,000 and a margin of safety of 25%, what was the break-even

point?

a. $5,000,000

b. $3,000,000

c. $12,000,000

d. $1,000,000

125. If a business had a capacity of $10,000,000 of sales, actual sales were $6,000,000, break-even

sales was $4,500,000, fixed costs amounted to $1,800,000, and variable costs amounted to

60% of sales, what is the margin of safety expressed as a percentage of sales?

a. 25%

b. 18%

c. 33.3%

d. 15%

126. If sales amounted to $375,000, variable costs are 70% of sales, and operating income is

$50,000, what is the operating leverage?

a. 8.125

b. 12.750

c. 5.688

d. 2.250

127. The difference between the current sales revenue and the sales at the break-even point is called

the:

a. contribution margin.

b. margin of safety.

c. price factor.

d. operating leverage.

128. Cost-volume-profit analysis cannot be used if which of the following occurs?

a. Costs cannot be properly classified into fixed and variable costs

b. The total fixed costs change

c. The per-unit variable costs change

d. Per-unit sales prices change

Chapter 11: Cost Behavior and Cost-Volume-Profit Analysis

129. The following is a list of various costs of producing sweatshirts. Classify each cost as either a

variable, fixed, or mixed cost for units produced and sold.

(a) Electricity costs of $0.025 per kilowatt-hour

(b) Warehouse rent of $6,000 per month plus $0.50 per square foot of storage used

(c) Thread

(d) Zip used in sweatshirts

(e) Janitorial costs of $2,000 per month

(f) Advertising costs of $10,000 per month

(g) Plant manager salary

(h) Color dyes for producing different colors of sweatshirts

(i) Salary of the production supervisor

(j) Straight-line depreciation on sewing machines

(k) Patterns for different designs. Patterns typically last many years before being replaced

(l) Maintenance costs for the company’s sewing machine. The cost is $2,000 per year

plus $0.001 for each machine hour of use

(m) Property taxes on factory, building, and equipment

(n) Cotton and polyester cloth

(o) Hourly wages of sewing machine operators

Chapter 11: Cost Behavior and Cost-Volume-Profit Analysis

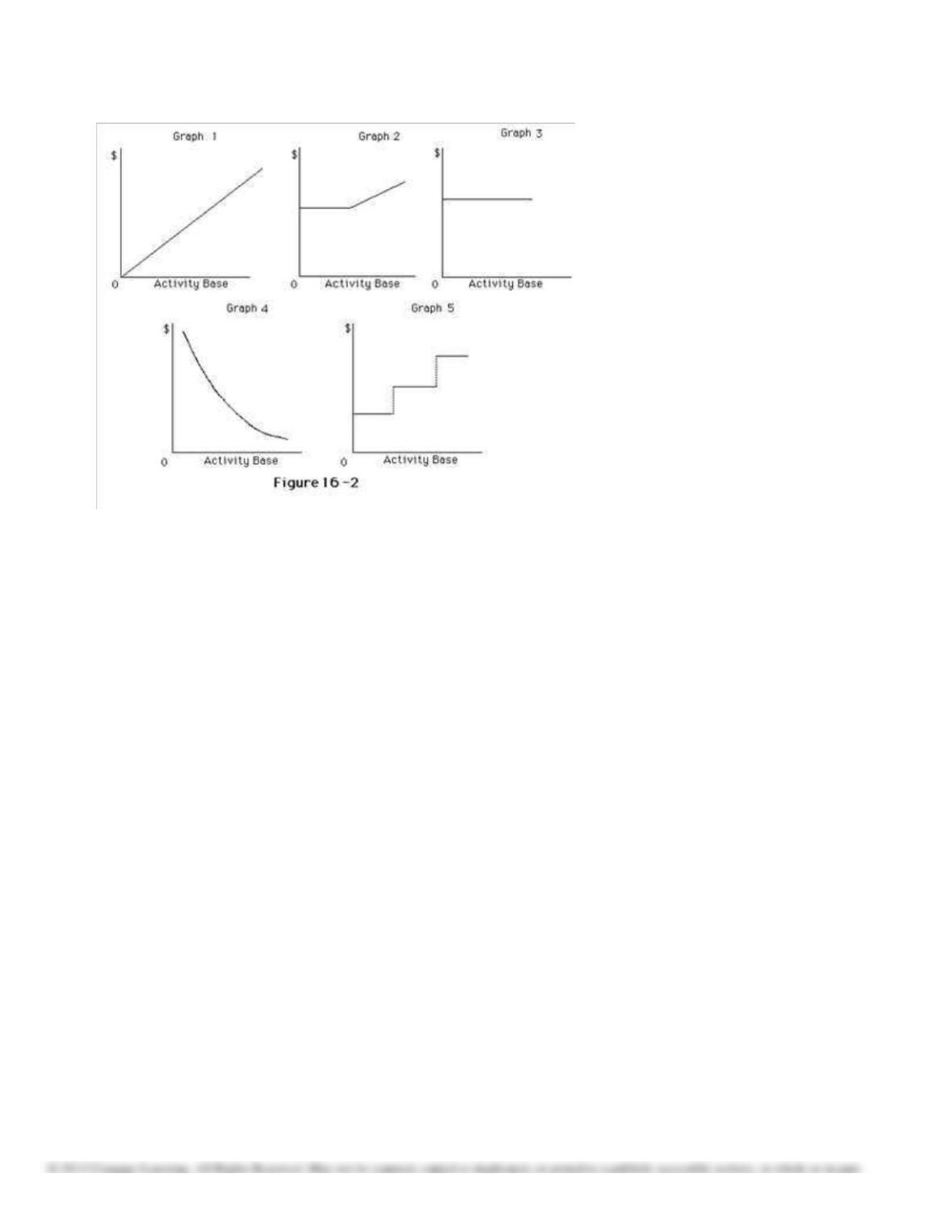

130. The following cost graphs illustrate various types of cost behaviors.

For each of the following costs, identify the cost graph that best describes its cost behavior as

the number of units produced and sold increases.

(a) Per-unit cost of direct labor

(b) Rent on warehouse of $10,000 per month

(c) Insurance costs of $2,500 per month

(d) Sales commissions of $5,000 plus $0.05 for each item sold

(e) Total salaries of quality control supervisors. One supervisor must be added for each

additional work shift

(f) Total employer pension costs of $0.30 per direct labor hour

(g) Per-unit straight-line depreciation costs

(h) Per-unit cost of direct materials

(i) Total direct materials cost

(j) Electricity costs of $5,000 per month plus $0.0004 per kilowatt-hour

(k) Per-unit cost of plant superintendent’s salary

(l) Straight-line depreciation on factory equipment

(m) Repairs and maintenance costs of $3,000 for each 2,000 hours of factory machine

usage

(n) Total direct labor cost

Chapter 11: Cost Behavior and Cost-Volume-Profit Analysis

131. Given below are the two independent situations:

(a)

If Henry Company’s budgeted sales are $800,000, fixed costs are $350,000, and variable

costs are $600,000, what is the budgeted contribution margin ratio?

(b)

If the contribution margin ratio is 30% for Gray Company, sales are $900,000, and fixed

costs are $180,000, what is the operating profit?

132. For the current year ending January 31, Ringo Company expects fixed costs of $178,500 and a

unit variable cost of $41.50. For the coming year, a new wage contract will increase the unit

variable cost to $45. The selling price of $50 per unit is expected to remain the same.

(a) Compute the break-even sales (in units) for the current year.

(b) Compute the anticipated break-even sales (in units) for the coming year, assuming the

new wage contract is signed.

133. For the current year ending April 30, Philip Company expects fixed costs of $70,000, a unit

variable cost of $45, and a unit selling price of $95.

(a) Compute the anticipated break-even sales (in units).

(b) Compute the sales (in units) required to realize an operating profit of $8,000.

Chapter 11: Cost Behavior and Cost-Volume-Profit Analysis

134. Currently, Unicy Company’s unit selling price is $25, the variable cost is $17, and the total

fixed costs are $85,000. A proposal is being evaluated to increase the selling price to $27.

(a) Compute the current break-even sales (in units).

(b) Compute the anticipated break-even sales (in units), assuming that the unit selling price

is increased and all costs remain constant.

135. For the coming year, Belton Company estimates fixed costs of $60,000, the unit variable cost

of $25, and the unit selling price of $50. Determine (a) the break-even point in units of sales,

(b) the unit sales required to realize operating income of $100,000, and (c) the probable

operating income if sales total $400,000.

136. For the past year, LaPrade Company had fixed costs of $70,000, a unit variable costs of $32,

and a unit selling price of $40. For the coming year, no changes are expected in revenues and

costs except that property taxes are expected to increase by $10,000. Determine the break-even

sales (in units) for (a) the past year and (b) the coming year.

137. For the past year, Cline Company had fixed costs of $6,552,000, a unit variable cost of $444,

and a unit selling price of $600. For the coming year, no changes are expected in revenues and

costs except that a new wage contract will increase variable costs by $6 per unit. Determine

the break-even sales (in units) for (a) the past year and (b) the coming year.

138. Lauder Company had fixed costs of $282,500, variable costs of $645,000, and actual sales

amounted to $1,100,000. If the company has a break-even point at $750,000 in sales revenue,

determine (a) the margin of safety expressed in dollars, (b) the margin of safety expressed as a

percentage of sales, (c) the contribution margin ratio, and (d) the operating income.

Chapter 11: Cost Behavior and Cost-Volume-Profit Analysis

139. A company has a margin of safety of 25%, a contribution margin ratio of 30%, and sales of

$1,000,000.

(a) What was the break-even point?

(b) What was the operating income?

(c) If neither the relationship between variable costs and sales nor the amount of fixed costs

is expected to change in the next year, how much additional operating income can be

earned by increasing sales by $110,000?

140. Tops Company sells Products D and E and has made the following estimates for the coming

year:

Product

Unit Selling Price

Unit Variable Cost

Sales Mix

D

$30

$24

60%

E

70

56

40

Fixed costs are estimated at $202,400. Determine (a) the estimated sales in units of the overall

product necessary to reach the break-even point for the coming year, (b) the estimated number

of units of each product necessary to be sold to reach the break-even point for the coming year,

and (c) the estimated sales in units of the overall product necessary to realize an operating

income of $119,600 for the coming year.