Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

11-121

120.

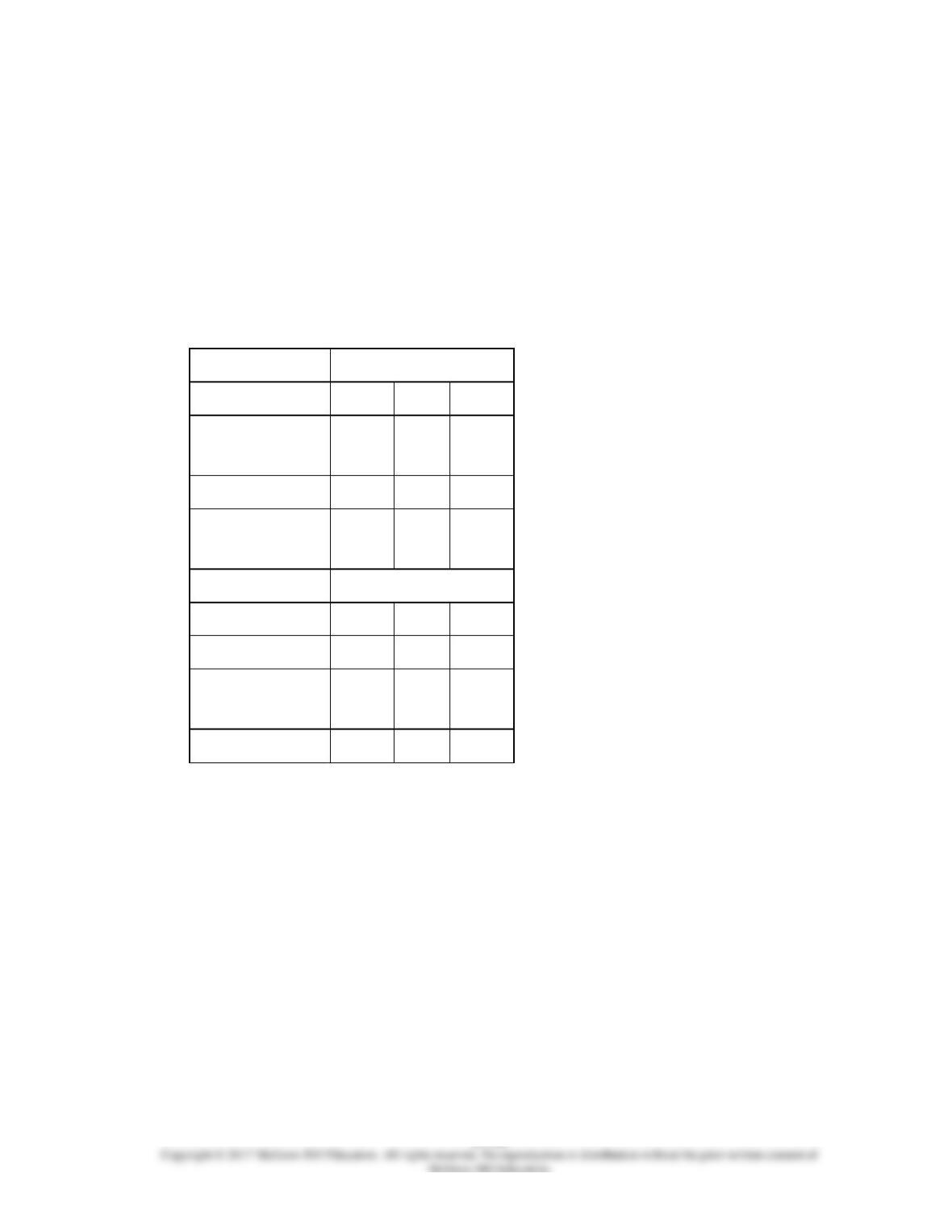

Franklin Corporation has three operating departments (Fabricating, Assembly, and

Finishing) and two service departments (Custodial and Administrative). The following

information has been provided:

Custodial

Admin

Fabricating

Assembly

Finishing

Dept Costs

$250,000

$400,000

--

--

--

# employees

10

--

80

100

60

Sq ft

--

15,000

30,000

35,000

20,000

Allocations are based on the

following:

Custodial:

Square

feet

Administrative:

Number of

employees

121.

The Joplin Company conducts a simple chemical process in Department #1, which

produces three separate items: A, K, and H. A is processed further in Department #2. K is

11-122

processed further in Department #3. Product H is a by-product, to be accounted for by the

cost reduction method. The following information relates to September:

Department #1's costs $420,000.

Department #2's costs $150,000.

Department #3's costs $60,000.

A: 25,000 pounds completed; 23,500 pounds sold for $12 per pound.

K: 75,000 pounds completed; 70,000 pounds sold for $7.50 per pound.

H: 10,000 pounds completed; 10,000 pounds sold for $1.50 per pound. (There are shipping

costs of $0.30 per pound.)

There were no September 1st inventories.

Required:

Prepare a schedule to show the computation for the unit costs per pound for Products A,

K, and H assuming Joplin uses the estimated net realizable value method to allocate joint

costs to the main products.

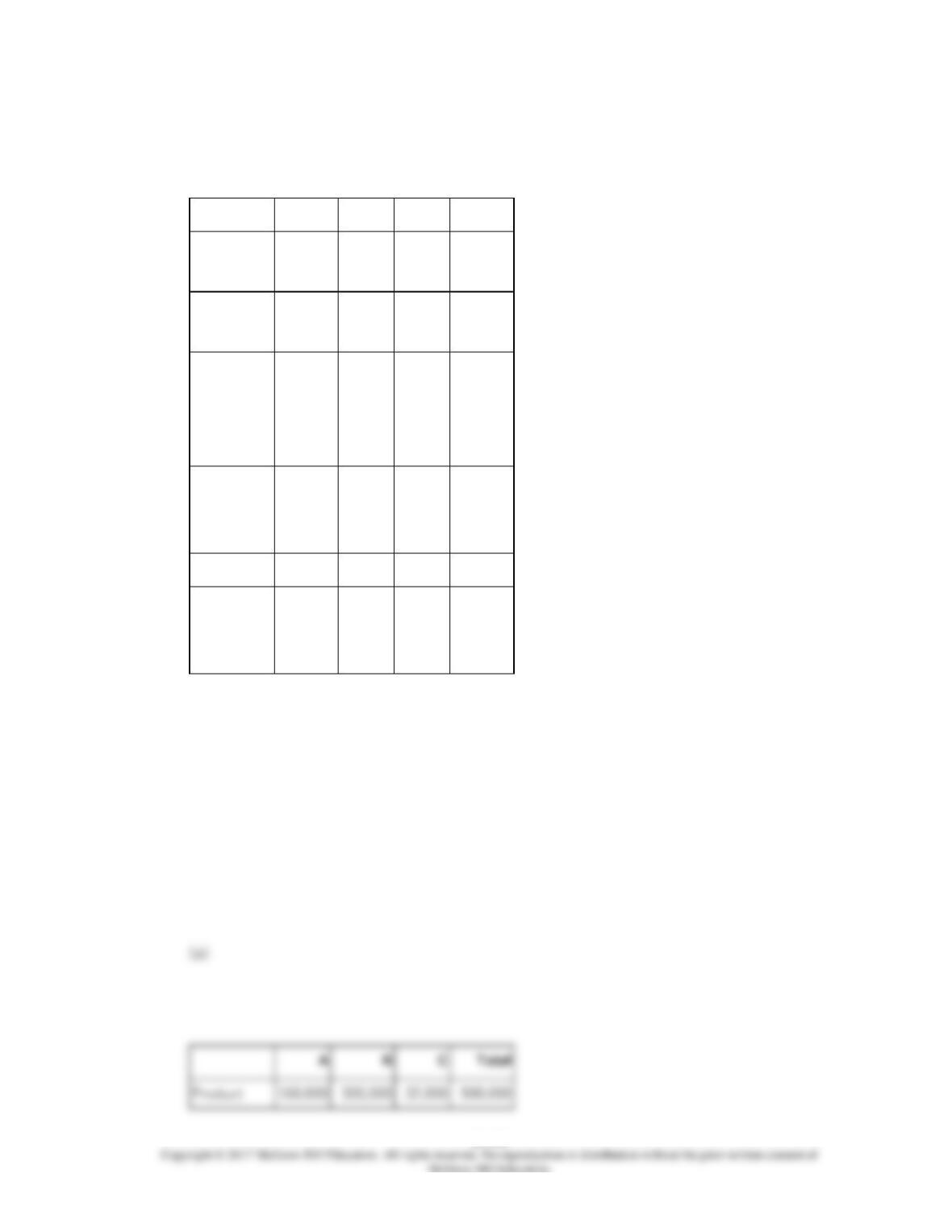

122.

Simpson Manufacturing Enterprises uses a joint production process that produces three

products at the split-off point. Joint production costs during April were $720,000. The

company uses the net realizable value method for allocating joint costs. Product

11-123

information for April was as follows:

Product

R

S

T

Gallons produced

2,500

5,000

7,500

Sales prices per

gallon:

At the split-off

$100

$80

$20

After further

processing

$150

$115

$30

Costs to process

after split-off

$150,000

$150,000

$100,000

11-125

123.

Clean-Burn, Inc. is a small petroleum company that acquires high-grade crude oil from

low-volume production wells owned by individuals and small partnerships. The crude oil is

processed in a single refinery into Two Oil, Six Oil, and impure distillates. Clean-Burn does

not have the technology or capacity to process these products further and sells most of its

output each month to major refineries. There were no inventories on November 1.

Crude oil acquired and placed into

production

$5,000,000

Direct labor and related costs

2,000,000

Refinery overhead

3,000,000

11-126

124.

Smokey Enterprises buys Liquid Charcoal for $0.80 a gallon. At the end of processing in

department 1, the liquid charcoal splits off into Products U, V, and W. Product U is sold at

the split-off point, with no further processing. Products V and W require further processing

before they can be sold; Product V is processed in Department 2, and Product W is

processed in Department 3. Following is a summary of costs and other related data for the

most recent accounting period:

Department

1

2

3

Cost of liquid

charcoal

$104,000

Direct labor

16,000

45,000

65,000

Manufacturing

overhead

10,000

27,000

49,000

Products

U

V

W

Gallons sold

20,000

30,000

50,000

Gallons on hand end

of period

15,000

0

15,000

Sales in dollars

$30,000

$96,000

$142,000

There were no beginning inventories and there was no liquid charcoal on hand at the end

of the period. All gallons on hand in ending inventory were complete as to processing.

Smokey uses the estimated net realizable value method of allocating joint costs.

Required:

a. Determine the product cost for U, V, and W, assuming the physical quantity method is

used to allocate joint costs.

b. Determine the product cost for U, V, and W, assuming the net realizable value method

is used to allocate joint costs.

11-128

125.

11-130

126.

The Marketplace Corporation produces two consumer products and a by-product. Zylon is

ready for sale after split-off, while Qytol must be further processed. The by-product is a

heavy residue in the bottom of the vat. The net realizable value of the by-product is

credited against the $565,000 joint cost of the Heating Department. Volume and cost data

for February is as follows:

Gallons

Produced

Selling

Price

Additional

Processing

Zylon

200,000

$2.00

0

Qytol

400,000

1.10

$40,000

By-Product

5,000

0.50

0

127.

The Delicious Canning Company processes tomatoes into ketchup, tomato juice, and

canned tomatoes. During the summer, the joint costs of processing the tomatoes were

$420,000. There was no beginning or ending inventories for the summer. Production and

11-131

sales value information for the summer were as follows:

Product

Cases

Additional Costs

Selling Price

Ketchup

100,000

$3.00 per case

$28 per case

Juice

150,000

5.00 per case

$25 per case

Canned

200,000

2.50 per case

10 per case

128.

The Joplin Company conducts a simple chemical process in Department #1, which

produces three separate items: A, K, and H. A is processed further in Department #2. K is

processed further in Department #3. Product H is a by-product, to be accounted for by the

other revenue method. The following information relates to September:

Department #1's costs $420,000.

129.

11-134

130.

Voorhees Manufacturing Corporation produces three products in a joint process.

Additional information is as follows:

O

P

Q

Total

Units

produced

42,000

50,000

8,000

100,000

Sales value

at split off

$250,000

$50,000

$20,000

$320,000

Additional

costs if

processed

further

$18,000

$30,000

$10,000

$58,000

Sales value

if processed

further

$290,000

$70,000

$25,000

$385,000

Joint costs

$300,000

Product

weights in

pounds

84,000

150,000

8,000

242,000

11-136

131.

Ridgeline Enterprises produces three products in a joint process. Products A and B were

processed further. Additional information is as follows:

A

B

C

Total

Units

produced

42,000

50,000

8,000

100,000

Sales value

at split-off

$250,000

$30,000

$20,000

$300,000

Additional

costs if

processed

further

$18,000

$30,000

$0

$48,000

Sales value

if processed

further

$290,000

$70,000

$0

$360,000

Joint Costs

$200,000

Product

Weight in

pounds

168,000

300,000

32,000

500,000

11-138

132.

Geneva Powder Company produces body powders in batches. Each type of powder can be

sold in its current condition or processed further and specialized for high priced

department stores. Data concerning the various products appear below. Joint processing

costs are $200,000.

Type of

Powder

Number

of

Pounds

Price

per

Pound

at

Split-

Off

Further

Processing

Costs

Price

after

Processing

Further

Cosmetic

Powder

200,000

$10

$150,000

$11.50

Medicated

Powder

400,000

$8

$60,000

$8.40

Baby

Powder

50,000

$5

$80,000

$5.50

11-139

133.

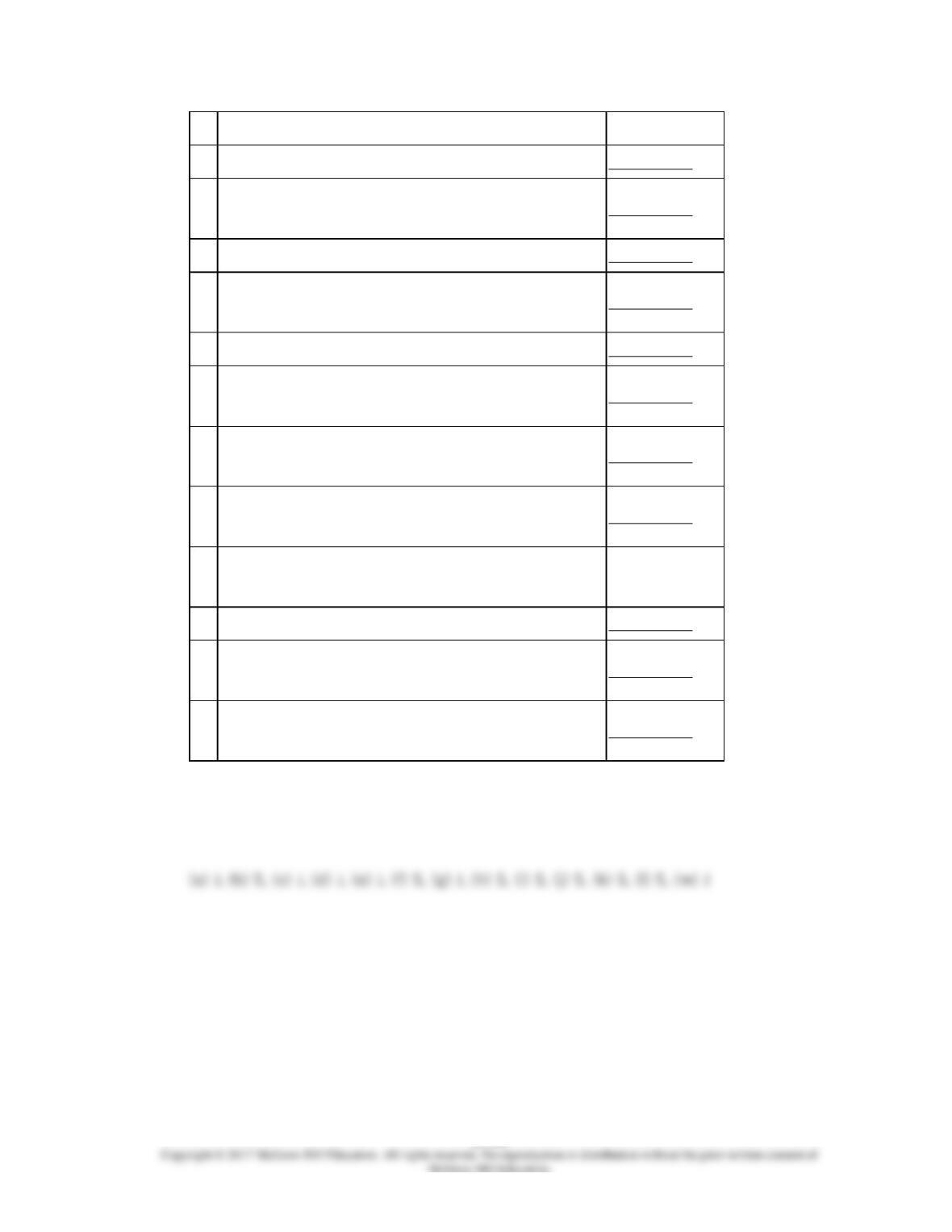

Indicate whether the following costs would be treated as joint-product costs or costs

incurred after the split-off point. Use J for joint product costs and S for costs incurred after

the split-off point.

(a)

Cost of planting, growing and picking pineapples in a

11-140

pineapple factory

(b)

Costs of processing apples at a cider mill

(c)

Costs of processing pineapples into juice and sliced

pineapples

(d)

Depreciation on oil rigs for an oil producer

(e)

Costs of running a fishing boat used to catch varieties of

fish, lobsters, etc.

(f)

Labor costs, of “shucking” clams to produce clam chowder

(g)

Costs of chopping onions to be used in spaghetti sauce

and soup in a food manufacturer

(h)

Cost of processing rejected meat parts into hot dogs in a

meat processing plant

(i)

Cost of processing wood and sawdust into particle board in

a sawmill

(j)

Ingredients and packaging added to batches of spaghetti in

(g) above

__________

(k)

Costs of refining gasoline in (d) above

(l)

Processing of pulp into paperboard in a paper

manufacturer

(m)

Utility costs of processing timber for a lumber

manufacturer

134.

The Macon Industries started the production of K1 (its main product) and S2 (its by-

product) on January 2, 2016. During 2016, 7,500 units of K1 and 1,500 units of S2 were

produced. In 2016, 6,000 units of K1 and 1,000 units of S2 were sold at $57.00 and $1.10

per unit, respectively. Production was halted at the end of 2016 and the inventory was sold

in 2017 at the normal selling prices. The joint production costs were $240,000 and are